北米の無糖エナジードリンク:市場シェア分析、産業動向、成長予測(2025年~2030年)

North America Sugar Free Energy Drinks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 195 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684097

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

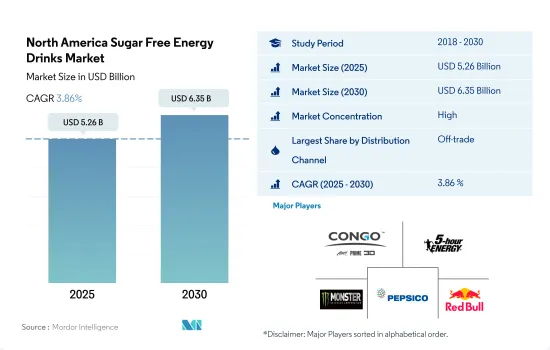

北米の無糖エナジードリンク市場規模は2025年に52億6,000万米ドルと推定・予測され、2030年には63億5,000万米ドルに達し、予測期間(2025年~2030年)のCAGRは3.86%で成長すると予測されます。

多様なフレーバーオプションと低カロリーエナジードリンクの人気の高まりが成長を牽引

- 2023年、北米の流通チャネルは2020年から20.52%の大幅な成長を遂げました。この急増は、ブルースラッシュ、ベリーポップ、チェリースラッシュのようなフレーバーを特徴とする多様な無糖エナジードリンクの入手可能性が高まっていることに起因しています。小売業者は、低カロリーエナジードリンクブランドの幅広い品揃えを提供することで対応しています。特に、この地域の消費者の嗜好は、Vエナジー、パワーホース、C4エナジー、NOCCOといったブランドに傾いており、2022年時点の市場シェアはそれぞれ28%、19%、18%、17%となっています。

- スーパーマーケットとハイパーマーケットが北米市場を独占し、大きなシェアを占めています。非商業小売部門では、これらの店舗が金額ベースで44.9%の市場シェアを占めています。この分野の有力企業には、ウォルマート、ターゲット、クローガー、アマゾン、コストコ・ホールセール・コーポレーション、アルバートソンズ・コス、アホールド・デルハイズUSA、パブリックス・スーパー・マーケッツなどがあります。これらの小売業者は、幅広い無糖エナジードリンクを提供することで需要に応えています。2023年現在、低カロリー・低エナジードリンクの価格帯は2.20~3.10米ドルです。

- オンライン・チャネルは、現代の消費者に提供する利便性によって、最も急成長する流通手段となる見込みです。2022年には、低カロリーエナジードリンクを求める人を含め、カナダ人の約22.2%が食料品を定期的にオンラインで購入しています。オンライン・プラットフォームを通じた無糖エナジードリンクの売上は、2018年から2023年にかけて38.56%という驚異的な成長率を示しました。Amazon、Walmart、Target、Walgreensがこのオンライン空間の主要企業です。これらのプラットフォームは、大量購入割引、季節のオファー、無料配送、クーポンコードで購入者を誘惑します。

スポーツ活動の需要の高まりにより、北米では無糖または低カロリーのエナジードリンクに消費者の関心が移っています。

- 2018年から2022年にかけて、エナジードリンク市場は、主に18~31歳の年齢層によって人気が急上昇しました。これらの飲料は、覚醒度と集中力を高める可能性があることで知られ、その効能は主成分であるカフェインに負うところが大きいです。2023年には、アメリカ人の驚異的な85%が少なくとも1種類のカフェイン入り飲料を消費しており、こうしたエネルギーを高める飲料に対する国民の親近感が浮き彫りになっています。

- 北米市場では、米国が2023年に無糖・低カロリー・エナジードリンクセグメントの支配的プレイヤーに浮上しました。フィットネス愛好家に好まれるこれらの飲料は、活力剤として機能するだけでなく、炭水化物からグルコースへの変換を助ける。2023年には、アメリカ人全体のほぼ半数にあたる49.9%が週に2回以上ジムに通うようになり、国民のフィットネス志向が浮き彫りになります。

- カナダの無糖・低カロリー・エナジードリンク市場は北米市場を上回り、2018年から2023年までのCAGRは5.60%と堅調な伸びを示しました。この成長は、より健康的な飲料選択の利点に対する意識の高まりによって促進されました。2022年には、カナダ人の18%がすでに無糖飲料を好んでおり、従来の選択肢からのシフトを示唆しています。

- 2024年~2027年の予測期間中、北米のエナジードリンク市場は金額ベースで11.51%の成長が見込まれます。この成長の主な原動力は、健康志向の高まりです。一方、小売業者は、この地域の消費者基盤を拡大するための戦略として、製品開発に注力すると予想されます。

北米の無糖エナジードリンク市場動向

健康と福祉に関連し、消費者は従来の代替品よりも砂糖不使用のエナジードリンクを好む傾向が強いです。

- 北米地域におけるエナジードリンクの消費は、特にティーンエイジャーや若年層の間で急激に伸びています。エナジードリンクは、アメリカの若者にとって2番目によく飲まれている栄養補助食品と考えられており、約30%が定期的に消費されています。

- 2022年現在、米国で発売されているエナジードリンク全体のうち、無糖または低カロリーのエナジードリンクが41%を占めています。現在、レッドブル、モンスター、ロックスターはすべて、北米地域の市場で無糖・カロリーゼロ版を展開しています。

- エナジードリンクの価格は、消費者の意思決定に重要な役割を果たしています。消費者は、景気後退期には価格に敏感になり、予算に見合った選択肢を求めるようになるかもしれないです。

- 砂糖の大量摂取と消費による健康への影響から、北米の消費者の間では低カロリーで砂糖不使用の代替品への需要が高まっています。2023年現在、米国では2022年に1億3,000万人以上の成人が糖尿病または糖尿病予備軍となり、カナダでは1,170万人が糖尿病または糖尿病予備軍となります。

北米の無糖エナジードリンク産業概要

北米の無糖エナジードリンク市場はかなり統合されており、上位5社で67.57%を占めています。この市場の主要企業は以下の通り。 Congo Brands, Living Essentials, LLC, Monster Beverage Corporation, PepsiCo, Inc. and Red Bull GmbH.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 消費者の購買行動

- イノベーション

- ブランドシェア分析

- 規制の枠組み

第5章 市場セグメンテーション

- 包装タイプ

- ガラス瓶

- 金属缶

- ペットボトル

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- スーパーマーケット/ハイパーマーケット

- その他

- オン・トレード

- オフトレード

- 国名

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Congo Brands

- G Fuel LLC

- Ghost Beverages, LLC

- Jocko Fuel LLC

- Living Essentials, LLC

- Monster Beverage Corporation

- PepsiCo, Inc.

- Performix LLC

- Red Bull GmbH

- The Coca-Cola Company

- Vitamin Well Limited

- Woodbolt Distribution, LLC

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The North America Sugar Free Energy Drinks Market size is estimated at 5.26 billion USD in 2025, and is expected to reach 6.35 billion USD by 2030, growing at a CAGR of 3.86% during the forecast period (2025-2030).

Diverse flavor options and growing popularity of low-calorie energy drinks drives growth

- In 2023, North American distribution channels experienced a significant growth of 20.52% from 2020. This surge can be attributed to the rising availability of a diverse range of sugar-free energy drinks featuring flavors like blue slush, berry pop, and cherry slush. Retailers have responded by offering an extensive selection of low-calorie energy drink brands. Notably, consumer preferences in the region lean toward brands like V Energy, Power Horse, C4 Energy, and NOCCO, with respective market shares of 28%, 19%, 18%, and 17% as of 2022.

- Supermarkets and hypermarkets dominate the North American market, accounting for a significant share. In the off-trade retailing segment, these establishments command a 44.9% market share by value. Prominent players in this space include Walmart, Target, Kroger, Amazon, Costco Wholesale Corporation, Albertsons Cos., Ahold Delhaize USA, and Publix Super Markets Inc. These retailers have responded to the demand by offering an extensive range of sugar-free energy drinks. As of 2023, the price range for low-calorie and low-energy drinks falls between USD 2.20 and USD 3.10.

- The online channel is poised to be the fastest-growing distribution avenue, driven by the convenience it offers to modern consumers. In 2022, approximately 22.2% of Canadians, including those seeking low-calorie energy drinks, regularly purchased groceries online. Sales of sugar-free energy drinks through online platforms witnessed an impressive growth rate of 38.56% from 2018 to 2023. Amazon, Walmart, Target, and Walgreens are key players in this online space. These platforms entice buyers with bulk purchase discounts, seasonal offers, free deliveries, and coupon codes.

Rising demand for sports activities has shifted the consumer's focus toward sugar-free or low-calorie energy drinks in North America

- Between 2018 and 2022, the energy drink market witnessed a surge in popularity, primarily driven by the 18-31 age group. These beverages, known for their potential to enhance alertness and concentration, owe their efficacy to caffeine, their primary ingredient. In 2023, a staggering 85% of Americans consumed at least one caffeinated beverage, highlighting the nation's affinity for these energy-boosting drinks.

- Within the North American market, the United States emerged as the dominant player in the sugar-free and low-calorie energy drink segment in 2023. These drinks, favored by fitness enthusiasts, not only serve as energizers but also aid in carbohydrate-to-glucose conversion. In 2023, nearly half of all Americans, 49.9%, hit the gym at least twice a week, underscoring the nation's fitness consciousness.

- Canada's sugar-free and low-calorie energy drink market outpaced its North American counterparts, boasting a robust CAGR of 5.60% from 2018 to 2023. This growth was fueled by a rising awareness of the benefits of healthier beverage choices. In 2022, a notable 18% of Canadians already preferred unsweetened beverages, signaling a shift away from traditional options.

- During the forecast period of 2024-2027, the North American energy drink market is projected to grow by 11.51% in value. This growth will be primarily driven by a health-conscious population. Retailers, on the other hand, are expected to focus on product development as their go-to strategy to expand their consumer base in the region.

North America Sugar Free Energy Drinks Market Trends

Pertaining to health and well-being, consumers are more likely to prefer sugar-free energy drinks than their conventional alternatives

- Consumption of energy drinks in the North American region has been growing exponentially, especially among teenagers and younger audience. Energy beverages are considered to be the 2nd most commonly consumed dietary supplement for young Americans, consuming approximately 30% of them on a regular basis.

- As of 2022, among the overall energy drink launches in the United States, sugar-free or low-calorie energy drinks accounted for 41%. Currently, Red Bull, Monster, and Rockstar all have sugar-free and calorie-free version in the market across the North American region.

- The price of energy drinks plays a significant role in consumer decisions. Consumers may be more price-sensitive during economic downturns and seek budget-friendly options.

- The health implications of high sugar intake and consumption have given rise to a higher demand for low calorie and sugar free alternatives among consumers in North America. As of 2023, more than 130 million adults are living with diabetes or prediabetes in the United States in 2022, while Canada has an 11.7 million population living with diabetes or prediabetes.

North America Sugar Free Energy Drinks Industry Overview

The North America Sugar Free Energy Drinks Market is fairly consolidated, with the top five companies occupying 67.57%. The major players in this market are Congo Brands, Living Essentials, LLC, Monster Beverage Corporation, PepsiCo, Inc. and Red Bull GmbH (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumer Buying Behaviour

- 4.2 Innovations

- 4.3 Brand Share Analysis

- 4.4 Regulatory Framework

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Packaging Type

- 5.1.1 Glass Bottles

- 5.1.2 Metal Can

- 5.1.3 PET Bottles

- 5.2 Distribution Channel

- 5.2.1 Off-trade

- 5.2.1.1 Convenience Stores

- 5.2.1.2 Online Retail

- 5.2.1.3 Supermarket/Hypermarket

- 5.2.1.4 Others

- 5.2.2 On-trade

- 5.2.1 Off-trade

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Congo Brands

- 6.4.2 G Fuel LLC

- 6.4.3 Ghost Beverages, LLC

- 6.4.4 Jocko Fuel LLC

- 6.4.5 Living Essentials, LLC

- 6.4.6 Monster Beverage Corporation

- 6.4.7 PepsiCo, Inc.

- 6.4.8 Performix LLC

- 6.4.9 Red Bull GmbH

- 6.4.10 The Coca-Cola Company

- 6.4.11 Vitamin Well Limited

- 6.4.12 Woodbolt Distribution, LLC

7 KEY STRATEGIC QUESTIONS FOR SOFT DRINK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 195 Pages

- 納期

- 2~3営業日