|

市場調査レポート

商品コード

1686530

北米のエナジードリンク:市場シェア分析、産業動向、成長予測(2025年~2030年)North America Energy Drinks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のエナジードリンク:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 225 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

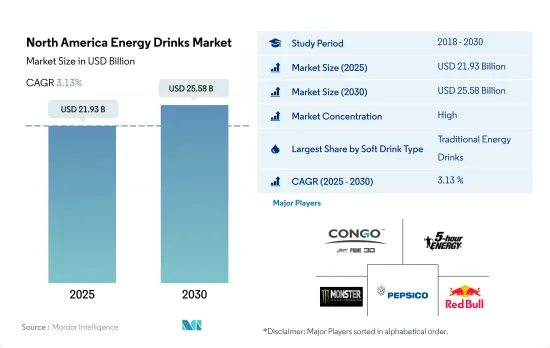

北米のエナジードリンク市場規模は2025年に219億3,000万米ドルと推定・予測され、2030年には255億8,000万米ドルに達し、予測期間(2025年~2030年)のCAGRは3.13%で成長すると予測されます。

クリーンラベルで砂糖不使用のエナジードリンクに対する需要の高まりが、このセグメントの売上を促進しています。

- エナジードリンクは北米の消費者、特にミレニアル世代とZ世代の消費者の間で急速に人気が高まりました。エナジードリンクは、消費者に1容器当たり70~250ミリグラムのカフェインを供給することで、精神的覚醒と身体的パフォーマンスを高めながらエネルギーを増加させ、米国人がより長く働けるようにすると主張しています。その結果、北米におけるエナジードリンクの販売額は、2021年から2023年にかけて金額ベースで5.6%の成長率を記録しました。伝統的なエナジードリンクが最大のシェアを占めており、レッドブルやモンスターといった人気ブランドがエナジードリンクを提供しています。

- また、米国人が栄養豊富で砂糖不使用、オーガニックのエナジードリンクを消費するようになっていることから、クリーンラベル製品に対する需要が高まり、健康食品に対する意識が高まっています。2022年現在、米国の消費者の37%以上が、エナジードリンクを含むクリーンラベル製品を好んでいます。Guruは、植物由来で、ビタミン、ミネラル、ハーブを含むヌートロピック成分で満たされたオーガニック・エナジードリンクを発売し、エナジードリンク業界の常識を覆しました。さらに、No Sugar Company社は2022年、Joyburstという名の自然エネルギー、自然カフェイン、植物由来のエナジードリンクのラインナップの発売を発表しました。

- エナジードリンクのカテゴリーの中で、無糖/低カロリーのエナジードリンクは、北南北アメリカで最も急成長しているエナジードリンクのタイプであり、2024年から2030年までのCAGRは5.74%を記録すると予想されています。この成長を後押ししているのは、糖尿病に対する関心の高まりから、消費者の間で糖分の摂取を制限する意識が高まっていることです。2022年の米国内の糖尿病患者数は3,730万人を超えており、北米で突出したシェアを占めています。

若者のアウトドア活動やレクリエーションへの参加急増がエナジードリンク需要を牽引

- 北米のエナジードリンク市場は急成長しており、販売額は2021年~2023年にかけて5.85%増加します。同地域の消費者はエナジードリンクの提供を求める傾向が強まっており、メーカーは革新的な新製品で対応しています。2022年から2023年にかけて、レッドブル、モンスター、VPX、ロックスター、レインといった人気ブランドは、一貫して様々なエナジードリンクを発売し、顧客を引き付けています。

- 米国は北米のエナジードリンク市場で最大の市場シェアを占めているが、これは同国でハイキング、サイクリング、ランニング、その他のスポーツ活動など、さまざまな高強度の身体活動に従事する人が多いためと考えられます。ハイキングは同国で最も人気のあるアウトドア・アクティビティに選ばれており、2022年時点で約6,000万人がハイキングに参加し、新たに88万1,000人が加わりました。飲料にはカフェインが含まれており、心臓や脳の機能を向上させ、エネルギー・レベルを高めるだけでなく、ハイキングのようなアクティビティに必要な注意力や集中力を高める効果もあります。

- 北米以外では、カナダが2024年~2030年のCAGR(年間平均成長率)5.83%で最速の成長国になると予想されます。この成長軌道を下支えしているのは、教育水準と雇用見通しの向上に牽引される若者層の増加です。2022年現在、カナダの人口の65%近くが15~64歳の年齢層であり、スポーツやその他のレクリエーション活動への参加率の高さとともに、市場の成長を促進すると予想されます。

北米のエナジードリンク市場動向

特に若者の間で、瞬発力と覚醒に対するニーズが高まっており、エナジードリンクの需要を促進しています。

- アメリカの大学生のエナジードリンク消費率は約42%。北米のエナジードリンク消費者の約3分の2は13~35歳で、そのうち男性が市場の3分の2を占めています。

- 消費者は、天然素材や植物由来の素材を使ったエナジードリンクを求めています。この動向は、より健康的でクリーンな製品を求める幅広い動きと一致しています。

- 100ミリリットルあたり20ミリグラム以上のカフェインを含むエナジードリンクには25%の税金がかかります。製品の高価格は、同地域での販売に悪影響を及ぼします。

- 健康志向の消費者は、糖分の少ないエナジードリンクや、"無糖"や"減糖"と表示されたエナジードリンクを求めることが多いです。糖分の多量摂取は、肥満や糖尿病など様々な健康問題に関連しています。

北米のエナジードリンク産業の概要

北米のエナジードリンク市場はかなり統合されており、上位5社で72.01%を占めています。この市場の主要企業は以下の通り。 Congo Brands, Living Essentials, LLC, Monster Beverage Corporation, PepsiCo, Inc. and Red Bull GmbH(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 消費者の購買行動

- イノベーション

- ブランドシェア分析

- 規制の枠組み

第5章 市場セグメンテーション

- 清涼飲料水のタイプ

- エナジーショット

- ナチュラル/オーガニック・エナジードリンク

- 無糖または低カロリーのエナジードリンク

- 伝統的エナジードリンク

- その他のエナジードリンク

- 包装タイプ

- ガラス瓶

- 金属缶

- ペットボトル

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- スーパーマーケット/ハイパーマーケット

- その他

- オン・トレード

- オフトレード

- 国名

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Aje Group

- Congo Brands

- DAS Labs LLC

- Living Essentials, LLC

- Monster Beverage Corporation

- N.V.E. Pharmaceuticals

- PepsiCo, Inc.

- Red Bull GmbH

- Seven & I Holdings Co., Ltd.

- The Coca-Cola Company

- Woodbolt Distribution, LLC

- Zevia LLC

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The North America Energy Drinks Market size is estimated at 21.93 billion USD in 2025, and is expected to reach 25.58 billion USD by 2030, growing at a CAGR of 3.13% during the forecast period (2025-2030).

Rising demand for clean-label and sugar-free energy drinks is propelling the sales of the segment

- Energy drinks rapidly gained popularity among consumers in North America, especially those from the millennial and Gen Z populations. Energy drinks claim to increase energy while enhancing mental alertness and physical performance by providing consumers with 70 to 250 milligrams of caffeine per container, allowing Americans to work longer. As a result, the sales value of energy drinks in North America registered a growth rate of 5.6% by value from 2021 to 2023. Traditional energy drinks account for the largest share, with popular brands like Red Bull and Monster serving energy drinks.

- Also, there is a growing demand for clean-label products and a rising awareness of healthy food, as Americans are increasingly consuming energy drinks that are nutrient-rich, sugar-free, and organic. As of 2022, more than 37% of consumers in the United States preferred clean-label products, including energy drinks. Guru turned the energy drink industry on its head with the release of their organic, plant-based energy beverage, which is plant-based and filled with nootropic components that include vitamins, minerals, and herbs. Furthermore, No Sugar Company, in 2022, announced the launch of a line of natural energy, naturally caffeinated, and plant-based energy drinks named Joyburst.

- Among the energy drinks category, sugar-free/low-calorie energy drinks are expected to be the fastest-growing energy drink type in the North American states, registering a value CAGR of 5.74% from 2024 to 2030. The growth is aided by growing awareness among consumers to limit the consumption of sugar content due to increased diabetic concerns. There were over 37.3 million diabetic people in 2022 within the United States, which holds a prominent share in North America.

The surging participation of youth in outdoor activities and recreational pursuits is driving the demand for energy drinks

- The North American energy drinks market is growing rapidly, with sales value increasing at 5.85% over 2021-2023. Consumers in the region are increasingly demanding energy drink offerings, and manufacturers are responding with new and innovative products. During 2022-23, popular brands like Red Bull, Monster, VPX, Rockstar, and Reign consistently launched a variety of energy drink offerings to attract customers.

- The United States occupies the largest market share in the North American energy drinks market, which can be due to the larger number of people in the country engaging in a variety of high-intensity physical activities like hiking, cycling, running, and other sports activities. Hiking is voted the most popular outdoor activity in the country, with approximately 60 million people participating in hiking as of 2022 and 881,000 people newly added. Apart from improving heart and brain function, along with increasing energy levels, the beverages contain caffeine, which helps increase alertness and attention, necessary attributes for activities like hiking.

- Canada is expected to be the fastest-growing country, apart from the Rest of North America, with a CAGR of 5.83% by value during 2024-2030. This growth trajectory is underpinned by a growing youth demographic driven by rising education and job prospects. As of 2022, almost 65% of the Canadian population was in the age group of 15-64 years, which is expected to propel the market's growth, along with a high rate of participation in sports and other recreational activities.

North America Energy Drinks Market Trends

The growing need for instant boost and alertness, especially among youngsters fuels the demand for energy drink

- The prevelance of energy drink consumption is around 42% among the university students in America. Around two thirds of energy drink consumers in North America are between 13-35 years old of which men account for two thirds of the market.

- Consumers are looking for energy drinks made with natural or plant-based ingredients. This trend aligns with the broader movement toward healthier and cleaner products.

- An energy drink containing 20 milligrams of caffeine per 100 milliliters or more is taxed at 25%. The high price of the product will negatively effects the sales in the region.

- Health-conscious consumers often seek energy drinks with lower sugar content or those labeled as "sugar-free" or "reduced sugar." High sugar intake is associated with various health issues, including obesity and diabetes.

North America Energy Drinks Industry Overview

The North America Energy Drinks Market is fairly consolidated, with the top five companies occupying 72.01%. The major players in this market are Congo Brands, Living Essentials, LLC, Monster Beverage Corporation, PepsiCo, Inc. and Red Bull GmbH (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumer Buying Behaviour

- 4.2 Innovations

- 4.3 Brand Share Analysis

- 4.4 Regulatory Framework

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Soft Drink Type

- 5.1.1 Energy Shots

- 5.1.2 Natural/Organic Energy Drinks

- 5.1.3 Sugar-free or Low-calories Energy Drinks

- 5.1.4 Traditional Energy Drinks

- 5.1.5 Other Energy Drinks

- 5.2 Packaging Type

- 5.2.1 Glass Bottles

- 5.2.2 Metal Can

- 5.2.3 PET Bottles

- 5.3 Distribution Channel

- 5.3.1 Off-trade

- 5.3.1.1 Convenience Stores

- 5.3.1.2 Online Retail

- 5.3.1.3 Supermarket/Hypermarket

- 5.3.1.4 Others

- 5.3.2 On-trade

- 5.3.1 Off-trade

- 5.4 Country

- 5.4.1 Canada

- 5.4.2 Mexico

- 5.4.3 United States

- 5.4.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Aje Group

- 6.4.2 Congo Brands

- 6.4.3 DAS Labs LLC

- 6.4.4 Living Essentials, LLC

- 6.4.5 Monster Beverage Corporation

- 6.4.6 N.V.E. Pharmaceuticals

- 6.4.7 PepsiCo, Inc.

- 6.4.8 Red Bull GmbH

- 6.4.9 Seven & I Holdings Co., Ltd.

- 6.4.10 The Coca-Cola Company

- 6.4.11 Woodbolt Distribution, LLC

- 6.4.12 Zevia LLC

7 KEY STRATEGIC QUESTIONS FOR SOFT DRINK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms