|

市場調査レポート

商品コード

1685917

アフリカのエナジードリンク:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Africa Energy Drinks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカのエナジードリンク:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 217 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

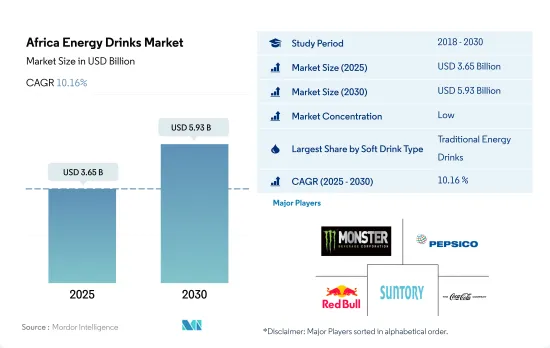

アフリカのエナジードリンクの市場規模は2025年に36億5,000万米ドルと推定され、2030年には59億3,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは10.16%で成長する見込みです。

活動的で多忙なライフスタイルに従事する若者人口の増加は、エナジードリンクの購入意思決定にプラスの影響を与えています。

- 2019年から2023年にかけて、アフリカではエナジードリンクの人気が急上昇し、その販売額は32.92%、販売量は26.70%の成長率を記録しました。このような需要の高まりは、急増する若年人口、都市化、急速なライフスタイルの変化といった要因によるものと考えられます。Nigerian Breweries PLCのような地域のプレーヤーと並んで、レッドブルやモンスターのような世界的大手がアフリカでの足跡を拡大しています。

- 調査期間中、伝統的なエナジードリンクが市場を独占し、2023年の市場金額の48.05%以上を占めました。この優位性は、多様なフレーバーと成分の組み合わせによるエナジードリンクの入手可能性が高まっていることに後押しされています。ナイジェリアは、従来のエナジードリンクの最大の消費国として際立っており、2023年に50.38%の数量シェアを獲得しました。この動向は、2022年の年齢中央値が19.4歳と若く、活気に満ちたペースの速いライフスタイルを示すナイジェリアの人口動態によって後押しされています。

- アフリカ市場では天然飲料と有機飲料の需要が顕著に急増しており、2024~2030年のCAGRはそれぞれ12.17%と12.21%と予測されます。このような上昇の背景には、クリーンラベル製品に対する嗜好の高まりと、健康的な食品と飲飲料の選択に対する意識の高まりがあります。2020年の調査では、エジプト、ケニア、南アフリカの都市人口の20%以上が有機食品を好んでいることが浮き彫りになり、アフリカ全域で有機飲食品の需要が拡大していることが明らかになりました。

エネルギー補給製品に関する意識の高まりが同分野の売上を押し上げそうです。

- アフリカのエナジードリンク市場は力強い成長を示し、2021年から2023年にかけて売上高は金額ベースで18.73%急増しました。この急成長の背景には、都市化の進展と消費者のペースの速いライフスタイルがあります。疲労回復や覚醒作用で知られるエナジードリンクは、消費者の間で人気を集めています。アフリカの都市人口は着実に増加しており、2023年には6億5,200万人に達し、2026年にはさらに増加して7億2,200万人に達すると予測されています。

- アフリカの都市化は、消費者の健康パターンに変化をもたらしています。運動量が制限され、肥満や心血管疾患などの疾病リスクが高まる中、エナジードリンクのようなエネルギー補給のための代替品に対する需要が増加しています。2022年には、南アフリカの成人人口の半数が太りすぎ(23%)または肥満(27%)でした。世界肥満連盟は、成人の肥満がさらに10%増加し、2030年には37%に達すると予測しています。

- ナイジェリアはアフリカのエナジードリンク市場をリードする勢いであり、2024年から2030年までの予測数量CAGRは14.14%です。ナイジェリア市場には、レッドブル、パワーホース、パワーフィストなど、さまざまなエナジードリンクブランドがあり、クランベリー、スイカ、オレンジ、ブルーベリーなどの新フレーバーを積極的に投入しています。ナイジェリアにおけるフィットネスサービスの拡大も、エナジードリンクを含む健康・ウェルネス製品の需要を促進しています。フィットネス活動の急増とフィットネスセンターのインフラ整備により、ナイジェリアではエナジードリンクの売上が顕著に増加すると予想されます。

アフリカのエナジードリンク市場動向

アフリカにおけるエナジードリンクに対する消費者の認識は、主に過剰摂取や潜在的な副作用に関連する懸念の影響を受けています。

- エナジードリンク製品の消費は、アフリカ地域のさまざまな年齢層の個人によって高く評価されており、特に20~30歳代で顕著です。エナジードリンクの消費量は、若く教育レベルの高い人々の間で高いです。

- 砂糖不使用、天然成分配合といったエナジードリンクの製品特性は、砂糖摂取に伴う健康リスクへの意識が高まるアフリカ地域の消費者を惹きつけています。砂糖入り飲料は、肥満、糖尿病、心臓病など、多くの健康問題に関連しています。

- アフリカの大都市圏に住む人口は増加の一途をたどり、エナジードリンクの人気を支えています。平均的なエナジードリンクの小売価格は、250mlあたり1~1.5米ドルです。

- 砂糖の大量摂取による健康への影響、糖尿病や肥満の消費により、低カロリーで砂糖不使用の代替品への需要が国内の消費者の間で高まっています。ガーナでは人口の約43%が肥満に苦しんでいます。

アフリカのエナジードリンク産業概要

アフリカのエナジードリンク市場は断片化されており、上位5社で38.81%を占めています。この市場の主要企業は以下の通り。 Monster Beverage Corporation, PepsiCo, Inc., Red Bull GmbH, Suntory Holdings Limited and The Coca-Cola Company(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 消費者の購買行動

- イノベーション

- ブランドシェア分析

- 規制の枠組み

第5章 市場セグメンテーション

- ソフトドリンクタイプ

- エナジーショット

- ナチュラル/オーガニックエナジードリンク

- 無糖または低カロリーエナジードリンク

- 従来のエナジードリンク

- その他のエナジードリンク

- 包装タイプ

- ガラス瓶

- 金属缶

- ペットボトル

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- スーパーマーケット/ハイパーマーケット

- その他

- オントレード

- オフトレード

- 国名

- エジプト

- ナイジェリア

- 南アフリカ

- その他のアフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Aje Group

- Halewood International South Africa(Pty)Ltd

- Mofaya Beverage Company(PTY)Ltd

- Monster Beverage Corporation

- Mutalo Group sp. z o.o

- PepsiCo, Inc.

- Red Bull GmbH

- S. Spitz GmbH

- Suntory Holdings Limited

- The Alternative Power(Pty)Ltd

- The Coca-Cola Company

- Tiger Brands Ltd.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Africa Energy Drinks Market size is estimated at 3.65 billion USD in 2025, and is expected to reach 5.93 billion USD by 2030, growing at a CAGR of 10.16% during the forecast period (2025-2030).

The rising youth population engaged in active and busy lifestyles is positively influencing energy drink purchase decisions

- From 2019 to 2023, Africa witnessed a surge in the popularity of energy drinks, with both their sales value and volume registering a growth rate of 32.92% and 26.70%, respectively. This uptick in demand can be attributed to factors like a burgeoning young population, urbanization, and rapid lifestyle changes. Global giants like Red Bull and Monster, alongside regional players like Nigerian Breweries PLC, are expanding their footprint in Africa.

- Over the study period, traditional energy drinks dominated the market, accounting for over 48.05% of the market's value in 2023. This dominance is fueled by the increasing availability of energy drinks in diverse flavors and ingredient combinations. Nigeria stands out as the largest consumer of traditional energy drinks, capturing a 50.38% volume share in 2023. This trend is bolstered by Nigeria's youthful demographic, with a median age of 19.4 in 2022, indicative of a vibrant and fast-paced lifestyle.

- The African market is witnessing a notable surge in demand for natural and organic energy drinks, projecting robust CAGRs of 12.17% and 12.21%, respectively, during 2024-2030. This uptick is driven by a rising preference for clean-label products and a heightened awareness of healthy food and beverage choices. A 2020 survey highlighted that over 20% of the urban populations in Egypt, Kenya, and South Africa favored organic food, underscoring the growing demand for organic beverages across Africa.

Growing awareness regarding energy-boosting products likely to boost the segment's sales

- The African energy drinks market witnessed robust growth, with sales surging by 18.73% in value from 2021 to 2023. This surge can be attributed to the rising urbanization and the fast-paced lifestyles of consumers. Energy drinks, known for their fatigue-fighting and alertness-enhancing properties, are gaining traction among consumers. The urban population in Africa has been on a steady rise, reaching 652 million in 2023, and is projected to climb further to 722 million by 2026.

- Urbanization in Africa has brought about a shift in consumer health patterns. With limited physical activity and an increased risk of diseases like obesity and cardiovascular ailments, the demand for energy-boosting alternatives, such as energy drinks, is on the rise. In 2022, half of South Africa's adult population was either overweight (23%) or obese (27%). The World Obesity Federation predicts a further 10% rise in adult obesity, reaching 37% by 2030.

- Nigeria is poised to lead the African energy drink market, with a projected volume CAGR of 14.14% during the period from 2024 to 2030. The Nigerian market boasts a range of energy drink brands, including Red Bull, Power Horse, and Power Fist, which are actively introducing new flavors like cranberry, watermelon, orange, and blueberry. The expanding fitness services landscape in Nigeria is also driving the demand for health and wellness products, including energy drinks. With a surge in fitness activities and improved fitness center infrastructure, Nigeria is expected to witness a notable uptick in energy drink sales.

Africa Energy Drinks Market Trends

Consumer perception of energy drinks in Africa is primarily influenced by concerns associated with excessive consumption and potential side effects

- Consumption of energy drinks products is highly valued by individuals of different ages in the African region particularly prevalent among those aged 20 to 30. Energy drink consumption was higher among people who were younger and had higher levels of education.

- Product attributes such as sugar-free and natural ingrdients enrgy drinks attract the consumers in the African region with the rising awareness of the health risks associated with sugar consumption. Sugary drinks have been linked to a number of health problems, including obesity, diabetes, and heart disease.

- The population living in large urban areas in the country has increased constantly supporting the gorwth of energy drinks. The retail price of an average energy drinks ranges between USD 1 to USD 1.50 per 250ml.

- Demand for low calories and sugar free alternatives has risen among consumers in the country due to health effects of high sugar intake and consumption diabetes and obesity. Although approximately 43% of the population is suffering from obesity in Ghana.

Africa Energy Drinks Industry Overview

The Africa Energy Drinks Market is fragmented, with the top five companies occupying 38.81%. The major players in this market are Monster Beverage Corporation, PepsiCo, Inc., Red Bull GmbH, Suntory Holdings Limited and The Coca-Cola Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumer Buying Behaviour

- 4.2 Innovations

- 4.3 Brand Share Analysis

- 4.4 Regulatory Framework

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Soft Drink Type

- 5.1.1 Energy Shots

- 5.1.2 Natural/Organic Energy Drinks

- 5.1.3 Sugar-free or Low-calories Energy Drinks

- 5.1.4 Traditional Energy Drinks

- 5.1.5 Other Energy Drinks

- 5.2 Packaging Type

- 5.2.1 Glass Bottles

- 5.2.2 Metal Can

- 5.2.3 PET Bottles

- 5.3 Distribution Channel

- 5.3.1 Off-trade

- 5.3.1.1 Convenience Stores

- 5.3.1.2 Online Retail

- 5.3.1.3 Supermarket/Hypermarket

- 5.3.1.4 Others

- 5.3.2 On-trade

- 5.3.1 Off-trade

- 5.4 Country

- 5.4.1 Egypt

- 5.4.2 Nigeria

- 5.4.3 South Africa

- 5.4.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Aje Group

- 6.4.2 Halewood International South Africa (Pty) Ltd

- 6.4.3 Mofaya Beverage Company (PTY) Ltd

- 6.4.4 Monster Beverage Corporation

- 6.4.5 Mutalo Group sp. z o.o

- 6.4.6 PepsiCo, Inc.

- 6.4.7 Red Bull GmbH

- 6.4.8 S. Spitz GmbH

- 6.4.9 Suntory Holdings Limited

- 6.4.10 The Alternative Power (Pty) Ltd

- 6.4.11 The Coca-Cola Company

- 6.4.12 Tiger Brands Ltd.

7 KEY STRATEGIC QUESTIONS FOR SOFT DRINK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms