|

市場調査レポート

商品コード

1687058

欧州のエナジードリンク:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Energy Drinks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のエナジードリンク:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 248 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

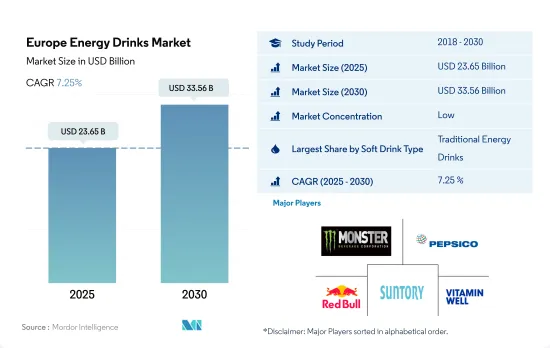

欧州のエナジードリンク市場規模は2025年に236億5,000万米ドルと推定され、2030年には335億6,000万米ドルに達し、予測期間中(2025~2030年)にCAGR 7.25%で成長すると予測されます。

消費者が健康を優先する中、天然/有機エナジードリンクがエナジードリンク市場の成長の波を牽引

- エナジードリンクは、パフォーマンス、持久力、覚醒度を高める効果があるとして知られ、主にアスリートが飲む飲料から主流飲料へと変遷してきました。この変化は、社会人、若年層、さらには大学生までもがこうした飲料をますます受け入れていることからも明らかです。2023年には、欧州人の70%がエナジードリンクを常飲していると報告しました。さらに2022年には、英国の青少年のほぼ3分の1が、エナジードリンクを週単位で消費していると報告しました。

- 欧州市場では、従来のエナジードリンクと無糖・低カロリーのエナジードリンクの両方が優勢で、2023年には合計で62%の金額シェアを占める。この優位性は、革新的なフレーバーと成分の組み合わせによるエナジードリンクの入手可能性が高まっていることに後押しされています。これらの飲料は現在、単独製品として、あるいはジュースや蒸留酒と混ぜて提供され、モクテルからカクテルまで多様な嗜好に対応しています。

- 特に、天然/有機エナジードリンク分野は、消費者層全体での人気急上昇に牽引され、欧州で著しい成長を遂げています。2023年には、ドイツの消費者の41%が、天然成分のみを使用したエナジードリンクにプレミアムを支払う意向を示しています。テンジング(Tenzing)、セルシウス(Celsius)、ヌーン(Nuun)のような世界的大手や新興ブランドも、ガラナ、緑茶、天然カフェインのような成分を取り入れており、持続可能で健康的なエネルギー源を求める需要に合致しています。この動向は、特に成熟市場と新興市場の双方で大きな可能性を秘めており、このセグメントは2024~2030年に7.80%のCAGRで推移すると予測されています。

同地域における支持とソーシャルメディア・マーケティングの影響力の高まりがエナジードリンク市場を牽引

- 2020年から2023年にかけて、欧州のエナジードリンク市場は金額ベースで12.63%の堅調な売上成長を記録したが、これは主に販促活動の強化が要因となっています。同市場の大手企業は、スポーツクラブと戦略的に提携し、ツイッター、フェイスブック、インスタグラムなどのプラットフォームでのデジタルプレゼンスを強化しています。これは消費者の注目を集めるだけでなく、ブランドの認知度を高めることにもつながります。例えば、主要企業であるレッドブルは、オーストリア、ドイツ、ブラジルのクラブとサッカーのオーナーシップを結んでいます。同様に、モンスター・エナジーはリバプールFC(イングランド)のような有名クラブとパートナーシップを結んでいます。

- ドイツでは近年、より健康的で自然な代替品に対する消費者の需要が高まり、製品の発売が増加しているため、エナジードリンク市場は大きく成長し、人気を博しています。例えば、GONRGY社は、ドイツのソーシャルメディア・スターであるMontanaBlack氏による缶入りエナジードリンクの新シリーズを発売しました。このドリンクはカロリーゼロで、2023年にREWEとKauflandの協力で発売されました。同様に、ペプシコは、カフェイン、ガラナ、タウリン、麻の実エキスを含む新しい飲料「Rockstar Energy+Hemp」を発売しました。このように、同国のエナジードリンク市場は、2020年から2023年にかけて金額ベースで22.77%の成長率を記録しています。

- トルコはエナジードリンク市場のフロントランナーとして際立っており、2024年から2030年にかけて金額ベースで9.32%のCAGRを達成する見込みです。トルコ市場の注目すべきブランドには、エナジードリンク0MaxやQpowerエナジードリンクなどがあります。より健康的な選択肢を求める需要の高まりを受けて、これらのブランドは無糖、低カロリー、さらにはカロリーゼロのバリエーションを展開し、アスリートや健康志向の高い人々に対応しています。

欧州のエナジードリンク市場動向

特に若者の間で、瞬時に活力を与え、覚醒させたいというニーズが高まっていることが、エナジードリンクの需要を促進しています。

- エナジードリンクの消費は女性よりも男性に多く、年齢とともに消費量が増加します。英国の青少年の19%が、週に4~5日以上エナジードリンクを消費しています。

- 消費者は糖分の摂取を気にしており、糖分を抑えたエナジードリンクや、"無糖"や"低糖"と表示されたエナジードリンクを選んでいます。

- 1本買うと1本無料になるキャンペーンや、複数本がセットになったお得なキャンペーンなどの割引やキャンペーンは、特に消費者がお得だと感じる場合、消費者の行動に影響を与えています。

- 欧州の清涼飲料部門は、欧州清涼飲料協会連合(UNESDA)が掲げた健康・栄養へのコミットメントの強化に基づき、過去7年間で平均17.7%の添加糖を削減しています。

欧州エネルギー飲料産業の概要

欧州のエナジードリンク市場は細分化されており、上位5社で18.58%を占めています。この市場の主要企業は以下の通り。 Monster Beverage Corporation, PepsiCo, Inc., Red Bull GmbH, Suntory Holdings Limited and Vitamin Well Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 消費者の購買行動

- イノベーション

- ブランドシェア分析

- 規制の枠組み

第5章 市場セグメンテーション

- ソフトドリンクタイプ

- エナジーショット

- ナチュラル/オーガニックエナジードリンク

- 無糖または低カロリーエナジードリンク

- 従来のエナジードリンク

- その他のエナジードリンク

- 包装タイプ

- ガラス瓶

- 金属缶

- ペットボトル

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- スーパーマーケット/ハイパーマーケット

- その他

- オントレード

- オフトレード

- 国

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Beverage Brands Holding Limited

- Congo Brands

- Dark Dog Drink Co.(Asia)Pte Ltd

- Hell Energy Magyarorszag Korlatolt Felelossegu Tarsasag

- Monster Beverage Corporation

- PepsiCo, Inc.

- Primo Water Corporation

- Red Bull GmbH

- S. Spitz GmbH

- Suntory Holdings Limited

- The Coca-Cola Company

- The Monarch Beverage Company Inc.

- Vitamin Well Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Europe Energy Drinks Market size is estimated at 23.65 billion USD in 2025, and is expected to reach 33.56 billion USD by 2030, growing at a CAGR of 7.25% during the forecast period (2025-2030).

Natural/organic energy drinks drive a wave of growth in the energy drinks market as consumers prioritize well-being

- Energy drinks, known for their purported benefits in enhancing performance, endurance, and alertness, have transitioned from being primarily consumed by athletes to becoming mainstream beverages. This shift is evident as working professionals, young adults, and even college students increasingly embrace these drinks. In 2023, a significant 70% of Europeans reported regular energy drink consumption. Furthermore, in 2022, nearly a third of UK adolescents reported consuming energy drinks on a weekly basis.

- Within the European market, both traditional and sugar-free/low-calorie energy drinks dominate, collectively accounting for a substantial 62% value share in 2023. This dominance is fueled by the rising availability of energy drinks in innovative flavors and ingredient combinations. These drinks are now offered as standalone products or mixed with juices or spirits, catering to diverse preferences, from mocktails to cocktails.

- Notably, the natural/organic energy drinks segment is witnessing remarkable growth in Europe, driven by its surging popularity across consumer segments. In 2023, a noteworthy 41% of German consumers expressed a willingness to pay a premium for energy drinks solely made from natural boosters. Global giants and emerging brands like Tenzing, Celsius, and Nuun are also incorporating ingredients like guarana, green tea, and natural caffeine, aligning with the demand for sustainable and healthier energy sources. This trend holds immense promise, particularly in both mature and emerging markets, with the segment projected to register a value CAGR of 7.80% during 2024-2030.

Growing influence of endorsements and social media marketing in the region is driving the energy drinks market

- From 2020 to 2023, the European energy drinks market witnessed a robust sales growth of 12.63% by value, primarily fueled by intensified promotional efforts. Leading players in the market have strategically aligned with sports clubs, bolstering their digital presence on platforms such as Twitter, Facebook, and Instagram. This not only grabs consumer attention but also amplifies brand visibility. For instance, Red Bull, a key player, has ventured into football ownership with clubs in Austria, Germany, and Brazil. Similarly, Monster Energy has forged partnerships with prominent clubs like Liverpool FC (England).

- The energy drinks market has witnessed significant growth and popularity in recent years in Germany, driven by increasing consumer demand for healthier and more natural alternatives and increasing product launches in the country. For instance, GONRGY launched a new range of canned energy drinks by German social media star MontanaBlack. The drinks are calorie-free and were made available in cooperation with REWE and Kaufland in 2023. Similarly, PepsiCo launched a new beverage, Rockstar Energy + Hemp, that contains caffeine, guarana, taurine, and hemp seed extract. Thus, the energy drinks market has registered a growth rate of 22.77% by value from 2020 to 2023 in the country.

- Turkey stands out as the frontrunner in the energy drinks market, and it is poised to achieve a CAGR of 9.32% by value from 2024 to 2030. Notable brands in the Turkish market include Energy Drink 0Max and Qpower Energy Drink. Responding to the rising demand for healthier options, these brands are rolling out sugar-free, low-calorie, and even calorie-free variants, catering to athletes and the health-conscious alike.

Europe Energy Drinks Market Trends

The growing need for instant boost and alertness, especially among youngsters fuels the demand for energy drink

- Consumption of energy drink is more common in males than in females, with consumption increasing with age. 19% of UK adolescents consume an energy drink 4-5 days per week or more.

- Consumers are concerned about sugar intake, and are opting for energy drinks with reduced sugar or those labeled as "sugar-free" or "low-sugar."

- Discounts and promotions, such as buy-one-get-one-free offers or multi-pack deals are impacting consumer behavior, especially when consumers perceive good value for money.

- The European soft drinks sector has reduced 17.7% of average added sugars in the last seven years based on the bolstered health and nutrition commitments set out by the Union of European Soft Drinks Associations (UNESDA).

Europe Energy Drinks Industry Overview

The Europe Energy Drinks Market is fragmented, with the top five companies occupying 18.58%. The major players in this market are Monster Beverage Corporation, PepsiCo, Inc., Red Bull GmbH, Suntory Holdings Limited and Vitamin Well Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumer Buying Behaviour

- 4.2 Innovations

- 4.3 Brand Share Analysis

- 4.4 Regulatory Framework

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Soft Drink Type

- 5.1.1 Energy Shots

- 5.1.2 Natural/Organic Energy Drinks

- 5.1.3 Sugar-free or Low-calories Energy Drinks

- 5.1.4 Traditional Energy Drinks

- 5.1.5 Other Energy Drinks

- 5.2 Packaging Type

- 5.2.1 Glass Bottles

- 5.2.2 Metal Can

- 5.2.3 PET Bottles

- 5.3 Distribution Channel

- 5.3.1 Off-trade

- 5.3.1.1 Convenience Stores

- 5.3.1.2 Online Retail

- 5.3.1.3 Supermarket/Hypermarket

- 5.3.1.4 Others

- 5.3.2 On-trade

- 5.3.1 Off-trade

- 5.4 Country

- 5.4.1 Belgium

- 5.4.2 France

- 5.4.3 Germany

- 5.4.4 Italy

- 5.4.5 Netherlands

- 5.4.6 Russia

- 5.4.7 Spain

- 5.4.8 Turkey

- 5.4.9 United Kingdom

- 5.4.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Beverage Brands Holding Limited

- 6.4.2 Congo Brands

- 6.4.3 Dark Dog Drink Co. (Asia) Pte Ltd

- 6.4.4 Hell Energy Magyarorszag Korlatolt Felelossegu Tarsasag

- 6.4.5 Monster Beverage Corporation

- 6.4.6 PepsiCo, Inc.

- 6.4.7 Primo Water Corporation

- 6.4.8 Red Bull GmbH

- 6.4.9 S. Spitz GmbH

- 6.4.10 Suntory Holdings Limited

- 6.4.11 The Coca-Cola Company

- 6.4.12 The Monarch Beverage Company Inc.

- 6.4.13 Vitamin Well Limited

7 KEY STRATEGIC QUESTIONS FOR SOFT DRINK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms