|

市場調査レポート

商品コード

1683972

米国の自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)US Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

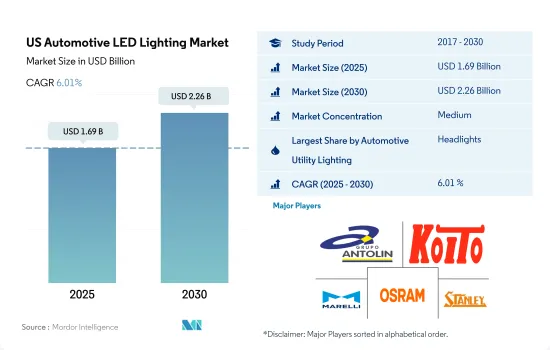

米国の自動車用LED照明市場規模は、2025年に16億9,000万米ドルと推定され、2030年には22億6,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは6.01%で成長します。

EV需要の拡大と事故件数の増加が市場成長を牽引

- 2020年、COVID-19の大流行により車載用LEDの生産が減少し、車載用半導体が不足しました。また、中米貿易戦争により主要原材料の入手が困難となり、サプライチェーンにも影響が出ていました。

- 金額シェアでは、2023年にはその他が大半を占め、次いでヘッドライト(35.1%)、方向指示灯(DSL)(12.7%)、ストップライト、昼間走行用ライト(DRL)と続きます。調査期間中、市場シェアはすべての照明で横ばいが予想されるが、その他は若干減少するとみられます。事故動向の上昇に伴い、フォグLEDランプの普及率は上昇すると予想されます。米国では、2022年の自動車事故死者数が推定4万6,000人に達しました。パンデミック前の死亡率と比較すると、22%近く増加しています。

- 数量シェアでは、2023年にはDSLが過半数のシェア(26.2%)を占め、次いでヘッドライト(17.4%)、その他、ストップライトと続きます。予測期間中は、DSLが若干減少するもの、すべてのライトで市場シェアは変わらないとみられます。

- 拡大と技術革新という点では、米国は世界有数の自動車生産国です。2022年、米国の自動車産業は約1,006万台の自動車を生産しました。これには乗用車、小型商用車、大型トラック、バス、コーチが含まれます。同市場の主要自動車メーカーは、電気自動車の拡大に注力しています。充電・燃料補給インフラ助成プログラムは、5年間で25億米ドルを助成する予定です。このように、NEV(近隣電気自動車)の成長は、市場における自動車用LEDの普及を増加させると思われます。

米国の自動車用LED照明市場動向

自動車のアップグレードとEVの増加によりLED照明の使用が増加

- 南米の自動車生産台数は2023年に983万台に達する見込みCOVID-19パンデミックは、世界経済のほとんどすべての国とセクターに大きな影響を与えました。自動車産業は特に大きな影響を受け、2019年から2020年にかけて米国の自動車販売台数は15%減少しました。2020年、自動車革新同盟によると、4月の総生産台数は月間最低水準となり、米国の全自動車生産の93%が3月下旬までに一時的に停止したと算出されました。そのため、生産台数の少なさは、自動車産業におけるLEDライトの生産に必要なLEDチップの需要に悪影響を及ぼしました。

- アメリカのトップ自動車メーカーには、BMW、フォード、ゼネラルモーターズ、ホンダ、ヒュンダイ、KIA、テスラ、日産、メルセデス・ベンツ、トヨタ、フォルクスワーゲン、ボルボなどがあります。これらのメーカーは絶えず自動車をアップグレードしています。最近、2023年4月、ボルボはボルボEX90の車内をLED照明で改装しました。72個のSunLike LEDで構成されるシステム全体が車内に設置され、太陽光に近い感覚を提供しています。このような技術的進歩は、自動車分野でのLED拡大の必要性を煽っています。

- 電気自動車(EV)市場は急速に拡大しており、今後10年間も拡大が見込まれています。2011年には全自動車販売台数のわずか0.2%に過ぎなかった米国における電気自動車販売台数は、2021年には4.6%にまで成長しました。2011年から21年の10年間で、EVの走行台数は約2万2,000台から200万台以上へと大幅に増加しました。その結果、EVの普及とともに、さまざまなEVアプリケーションで使用される半導体チップのニーズが高まり、LED照明の必要性が高まっています。

税制優遇やEV充電ステーションへの資金提供によるEV製造への政府投資がLED市場を牽引

- 米国では電気自動車化が進んでいます。電気自動車は、自動車産業におけるアウトライナーから未来の波へと移行しつつあり、2022年には販売台数が65%増加します。さらに拡大するために、政府は2021年に1兆ドル規模のインフラ法案を発表し、2030年までに公共EV充電器を50万台増設するために75億米ドルを割り当て、米国内で組み立てられたEVを購入すると7,500米ドルの税制優遇を提供することで、EV製造への投資も行いました。また、EVの重要なプレーヤーの一人であるテスラは、2024年末までに米国で約3,500基のスーパーチャージャーステーションと4,000基のレベル2充電ドックをすべてのブランドの電気自動車に提供することを約束しました。

- 2023年3月、バイデン-ハリス政権は、電気自動車(EV)充電と代替燃料インフラに資金を提供する数十億米ドル規模の新プログラムの申請受付を全国の町や指定道路、州間高速道路、主要ルート沿いで開始すると発表しました。超党派インフラ法は、米国運輸省の新しい充電・燃料補給インフラ(CFI)裁量補助金プログラムを設立し、市、郡、地方自治体、部族を含む幅広い申請者に5年間で25億米ドルを交付します。

- 2030年までに、米国ではジョージア州、ケンタッキー州、ミシガン州が電気自動車用バッテリー製造の大半を占めると予想されています。この電気自動車用バッテリー製造能力は、年間1,000万台から1,300万台のオール電化車の生産を促進し、米国を世界の電気自動車の競争相手として位置づけると思われます。このように、上記のような事例は、EVの需要増加による新しい発電所の開発と生産につながり、同国の自動車用LEDの需要を押し上げます。

米国の自動車用LED照明産業の概要

米国の自動車用LED照明市場は適度に統合されており、上位5社で51.04%を占めています。この市場の主要企業は以下の通りです。GRUPO ANTOLIN IRAUSA, S.A., KOITO MANUFACTURING, Marelli Holdings, OSRAM GmbH. and Stanley Electric(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 自動車生産台数

- 人口

- 一人当たり所得

- 自動車ローン金利

- 充電ステーション数

- 自動車保有台数

- LED総輸入数

- 世帯数

- 道路ネットワーク

- 普及率

- 規制の枠組み

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 自動車用ユーティリティ照明

- 日中走行用ライト(DRL)

- 方向指示灯

- ヘッドライト

- リバースライト

- ストップライト

- テールライト

- その他

- 自動車用照明

- 2輪車

- 商用車

- 乗用車

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- GRUPO ANTOLIN IRAUSA, S.A.

- HELLA GmbH & Co. KGaA(FORVIA)

- Hyundai Mobis

- KOITO MANUFACTURING CO., LTD.

- Marelli Holdings Co., Ltd.

- Nichia Corporation

- OSRAM GmbH.

- Signify(Philips)

- Stanley Electric Co., Ltd.

- Valeo

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The US Automotive LED Lighting Market size is estimated at 1.69 billion USD in 2025, and is expected to reach 2.26 billion USD by 2030, growing at a CAGR of 6.01% during the forecast period (2025-2030).

Growing demand for EVs and increasing number of accidents drive the market's growth

- In 2020, automotive LED production decreased because of the COVID-19 pandemic, leading to an automotive semiconductor shortage. The supply chain was also being impacted by difficulties in gaining access to key materials because of the China-US trade war.

- In terms of value share, in 2023, others accounted for the majority of the share, followed by headlights (35.1%), directional signal lights (DSL) (12.7%), stoplights, and daytime running lights (DRL). The market share is expected to remain the same for all lighting during the study period, with a small reduction in others. With the rising accident trend, the penetration rate of fog LED lamps is anticipated to rise. In the United States, the number of motor vehicle deaths reached an estimated 46,000 in 2022. Compared to the pre-pandemic death rate, it increased by nearly 22%.

- In terms of volume share, in 2023, DSL accounted for the majority of the share (26.2%), followed by headlights (17.4%), others, and stoplights. The market share is expected to remain the same for all the lights during the forecast period, with a small reduction in DSLs.

- In terms of expansion and innovations, the United States is one of the significant auto-producing nations in the world. In 2022, the auto industry in the United States produced approximately 10.06 million motor vehicles. It includes passenger cars, light commercial vehicles, heavy trucks, buses and coaches. The key automotive manufacturers in the market are focusing on expanding electric vehicles. The Charging and Fueling Infrastructure Grant Program would grant USD 2.5 billion over five years. Thus, the growth in NEVs (neighborhood electric vehicles) would increase the penetration of automotive LEDs in the market.

US Automotive LED Lighting Market Trends

Upgradation of automobiles and more EV are seen on road, indicating more use of LED lights

- The total automobile vehicle production in South America was expected to reach 9.83 million units in 2023. The COVID-19 pandemic significantly impacted almost every nation and sector of the global economy. The automotive industry was particularly exposed and badly affected, with a 15% decline in US vehicle sales from 2019 to 2020. In 2020, the total production in April was the lowest monthly production level, according to the Alliance for Automobile Innovation, which calculated that 93 percent of all automobile production in the United States was temporarily halted by late March. Thus, the low production negatively affected the demand for LED chips required to produce LED lights in the automotive industry.

- The top American automakers include BMW, Ford, General Motors, Honda, Hyundai, KIA, Tesla, Nissan, Mercedes-Benz, Toyota, Volkswagen, Volvo, and many more. These producers upgrade their automobiles constantly. Recently, in April 2023, Volvo renovated the inside of the Volvo EX90 using LED lighting. An entire system of 72 SunLike LEDs was installed inside the car to provide a near-sunlight sensation. Such technical advancement fuels the need to expand LED in the automobile sector.

- The market for electric cars (EVs) has expanded quickly and is anticipated to do so throughout the next ten years. From just 0.2 percent of all car sales in 2011 to 4.6 percent in 2021, electric car sales in the US grew. Over the decade of 2011-21, the number of EVs on the road increased significantly, from around 22,000 to over 2 million. As a result, the need for semiconductor chips used in various EV applications rises along with the popularity of EVs, raising the need for LED illumination.

Government investments in EV manufacturing by providing tax benefits and funding of EV charging stations to drive the LED market

- The United States is turning electric. Electric vehicles are transitioning from an outliner in the automotive industry to the wave of the future, with sales increasing by 65% in 2022. To expand further, the government issued a trillion-dollar infrastructure bill in 2021 that allocates USD 7.5 billion toward building 500,000 more public EV chargers by 2030 and also made investments in EV manufacturing by providing tax benefits of USD 7,500 for purchasing an EV assembled in the US. Also, Tesla, one of the significant players in EVs, committed to delivering around 3,500 of its US Supercharger stations and 4,000 Level 2 charging docks available to all brands of electric vehicles by the end of 2024.

- In March 2023, the Biden-Harris Administration announced the availability of applications for a new multibillion-dollar program to fund electric vehicle (EV) charging and alternative-fuel infrastructure in towns around the country and along designated roads, interstates, and major routes. The Bipartisan Infrastructure Act established the US Department of Transportation's new Charging and Fueling Infrastructure (CFI) Discretionary Grant Programme, which would grant USD 2.5 billion over five years to a wide range of applicants, including cities, counties, local governments, and Tribes.

- By 2030, Georgia, Kentucky, and Michigan are expected to dominate electric vehicle battery manufacturing in the United States. This EV battery manufacturing capacity will facilitate the production of 10 to 13 million all-electric vehicles per year, positioning the United States as a global EV competitor. Thus, the above instances lead to the development and production of new power stations because of the growing demand for EVs, which boosts the demand for automotive LEDs in the country.

US Automotive LED Lighting Industry Overview

The US Automotive LED Lighting Market is moderately consolidated, with the top five companies occupying 51.04%. The major players in this market are GRUPO ANTOLIN IRAUSA, S.A., KOITO MANUFACTURING CO., LTD., Marelli Holdings Co., Ltd., OSRAM GmbH. and Stanley Electric Co., Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 United States

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 GRUPO ANTOLIN IRAUSA, S.A.

- 6.4.2 HELLA GmbH & Co. KGaA (FORVIA)

- 6.4.3 Hyundai Mobis

- 6.4.4 KOITO MANUFACTURING CO., LTD.

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 Nichia Corporation

- 6.4.7 OSRAM GmbH.

- 6.4.8 Signify (Philips)

- 6.4.9 Stanley Electric Co., Ltd.

- 6.4.10 Valeo

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms