自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 224 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683948

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

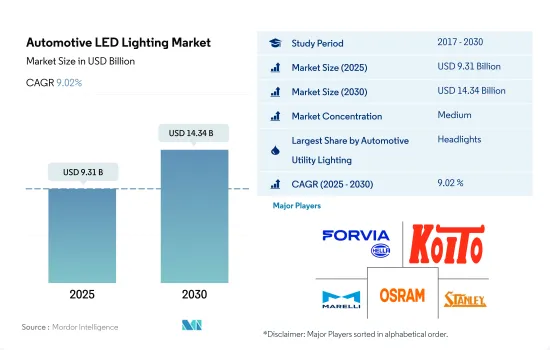

自動車用LED照明市場規模は2025年に93億1,000万米ドルと予測され、2030年には143億4,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは9.02%で成長します。

事故率の上昇、EV需要の拡大、政府の支援政策が市場成長を牽引

- 金額シェアでは、2022年にヘッドライトが市場シェアの大部分(51.8%)を占め、次いでその他(小型LEDライト、LEDナンバープレートライト、フォグライト、室内LEDライト)、方向指示灯(DSL)、デイタイムランニングライト、ストップライトが続きます。ヘッドライト・セグメントは今後高い市場シェアを獲得すると予想されます。事故件数の増加に伴い、フォグLEDランプとヘッドランプの普及率も上昇すると予想されます。世界では毎年約130万人が交通事故により死亡しています。

- 数量シェアでは、2023年にDSLが市場シェアの大半(27.9%)を占め、次いでヘッドライト(17.7%)、その他(小型LEDライト、LEDナンバープレートライト、フォグランプ、室内LEDライト)(16.4%)、ストップランプの順となっています。予測期間中、市場シェアはすべてのセグメントで横ばいが予想されるが、その他とストップライトのセグメントが若干減少し、DSLとヘッドライトのセグメントが増加するとみられます。外部ライト(主に信号灯)は、あらゆるタイプの自動車において軽微な事故から重大な事故まで影響を受ける可能性が高く、交換が必要です。

- EVは、世界的に自動車用LEDの需要が急増している主な要因の一つです。中国がEV市場をリードし、2022年の世界の電気自動車販売台数の60%を占め、次いで欧州と米国がそれぞれ15%と55%の高い伸びを示しました。

- 欧州連合(EU)のFit for 55パッケージや米国のインフレ抑制法など、主要国の野心的な政策プログラムがEVの市場シェアを押し上げると予想されます。市場の主なプレーヤーは、先進国におけるEV工場の拡大にも注力しています。

EVの成長、自律走行車、政府のインセンティブは、自動車産業におけるLEDライトの採用を促進すると予想されます。

- 金額シェアでは、2022年の自動車用LED照明市場はアジア太平洋が大半を占め、北米と欧州がそれぞれこれに続きます。中国、日本、タイ、台湾、マレーシア、インドといったアジア6カ国のほとんどが、国内市場の保護や自動車産業振興における自動車メーカーへの優遇措置といったインセンティブを導入しているため、2029年のアジア太平洋地域の市場シェアは増加すると予想されます。

- 数量シェアでは、アジア太平洋の自動車用LED照明市場が2022年に大半のシェアを占め、次いで欧州、北米となっています。欧州では、電気自動車の台頭と自動車に使用される燃料の種類における技術進歩が、同地域の自動車産業を変革しています。欧州連合におけるバッテリー式電気自動車の販売は、現在も急速に伸びています。例えば、2022年にEU市場で販売された910万台の自動車のうち12.1%が純粋なバッテリー電気自動車でした。対照的に、2019年にはこのシェアはわずか1.9%、2021年には9.1%でした。

- 電動化は、業界が世界的に進めている最も大きな変革です。もう一つの動向は自律走行車です。テクノロジーが自動車会社のカーボンニュートラル目標に貢献することは重要です。中東は日産にとって重要な市場です。現代の多くの自動車は、よりスマートでコネクテッドになってきています。日産アリヤのようなインテリジェントモビリティと自律走行が搭載されるでしょう。このような変革は、この地域の他の地域でも行われています。したがって、この地域の自動車セグメントの成長により、LEDの市場浸透が進む可能性があります。

世界の自動車用LED照明市場動向

EV需要の増加が市場価値を高めると予測

- 2022年の世界の自動車生産台数は1億4,396万台で、2023年には1億5,092万台に達すると予測されています。収集されたデータによると、すでに世界の自動車生産台数がおよそ5%減少した2019年に続き、2020年も自動車生産台数が16%減少することが示されました。欧州全体の平均減少率は21%以上でした。すべての主要生産国における急激な減少は、11%からおよそ40%に及びました。欧州の製造業は総生産台数の約22%を占めました。南北アメリカの自動車生産は、2020年の世界生産の20%を占めました。アフリカ大陸の製造業は35%以上と激減しました。一方、アジアは10%の減少にとどまり、よく持ちこたえています。提供された数字によると、COVID-19の流行は自動車産業に多大な影響を与え、LEDの需要を減少させました。

- フォルクスワーゲン・グループ、ステランティス、メルセデス・ベンツ、BMW、ポルシェ、Hurtan、GTAモーターズ、アウディ、TATAモーターズ、マヒンドラ&マヒンドラ、上海汽車、現代自動車、起亜自動車、KGモビリティ、ルノー韓国自動車が世界の主要自動車製造企業です。2022年の世界の電気自動車販売台数は1,000万台を超え、2023年の販売台数はさらに35%増の1,400万台に達すると予想されています。この急速な拡大により、電気自動車の市場シェアは2020年の4%から2022年には14%に増加しました。また、電気自動車の普及に伴い、従来の自動車よりも1台当たりのプロセッサー数が増えるため、車載用半導体チップの需要が高まっています。LED照明市場は、自動車産業における半導体需要の増加から恩恵を受けると予想されます。

バッテリー交換ステーションやバッテリー・リサイクル・サービス店舗の増加、EV需要の高まりが市場成長の原動力になると予想されます。

- EV市場は急激な勢いで拡大しており、2022年には販売台数が1,000万台を超えます。2022年には、電気自動車が全新車販売台数の14%を占め、2021年の約9%、2020年の5%未満から増加します。世界の販売台数は3つの市場が牽引しました。中国がトップで、世界の電気自動車販売台数の60%近くを占めました。中国は、世界で走行する電気自動車の半分以上を占めており、政府はすでに新エネルギー車販売の2025年目標を上回っています。

- 2022年までに、中国には1,973ヵ所のバッテリー交換ステーション(2022年に建設された675ヵ所を含む)があり、1万ヵ所以上の電源バッテリー・リサイクル・サービス店舗があります。このように、充電施設の急速な増加は、同国における新エネルギー車(NEV)セクターの活況を示しています。2022年10月、ドイツ政府は電気自動車の充電インフラを強化する計画を発表しました。この計画は63億ユーロ(61億7,000万米ドル)の提案で構成されており、2030年までに全国の充電ポイントを100万カ所に増やすというものでした。

- 主要市場において、2022年の電気自動車販売は例年低水準だったが、インド、タイ、インドネシアでは成長の年となりました。これらの国々での電気自動車の販売台数は2021年から3倍以上に増加し、8万台に達しました。米国では、インフレ抑制法(IRA)と、カリフォルニア州の先進クリーンカーⅡ規則を採用する多くの州とが相まって、2030年には電気自動車の市場シェアが国の目標に合わせて50%になる可能性が高いです。上記のような事例を考慮すると、世界中の主なメーカーは車載用LEDの開発と生産にさらに投資すると予想されます。

自動車用LED照明産業の概要

自動車用LED照明市場は適度に統合されており、上位5社で51.31%を占めています。この市場の主要企業は以下の通りです。HELLA GmbH & Co. KGaA(FORVIA), KOITO MANUFACTURING, Marelli Holdings, OSRAM GmbH. and Stanley Electric(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 自動車生産台数

- 人口

- 一人当たり所得

- 自動車ローン金利

- 充電ステーション数

- 自動車走行台数

- LED総輸入数

- 世帯数

- 道路ネットワーク

- 普及率

- 規制の枠組み

- アルゼンチン

- ブラジル

- 中国

- フランス

- ドイツ

- 湾岸協力会議

- インド

- 日本

- 南アフリカ

- 韓国

- スペイン

- 英国

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 自動車用ユーティリティ照明

- デイタイム・ランニング・ライト(DRL)

- 方向指示器

- ヘッドライト

- リバースライト

- ストップライト

- テールライト

- その他

- 自動車用照明

- 2輪車

- 商用車

- 乗用車

- 地域

- アジア太平洋

- 欧州

- 中東・アフリカ

- 北米

- 南米

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- GRUPO ANTOLIN IRAUSA, S.A.

- HELLA GmbH & Co. KGaA(FORVIA)

- Hyundai Mobis

- KOITO MANUFACTURING CO., LTD.

- Marelli Holdings Co., Ltd.

- Nichia Corporation

- OSRAM GmbH.

- Signify(Philips)

- Stanley Electric Co., Ltd.

- Valeo

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The Automotive LED Lighting Market size is estimated at 9.31 billion USD in 2025, and is expected to reach 14.34 billion USD by 2030, growing at a CAGR of 9.02% during the forecast period (2025-2030).

The rising accident rates, growing demand for EVs, and supportive government policies drive the market's growth

- In terms of value share, in 2022, headlights accounted for most of the market share (51.8%), followed by others (miniature LED lights, LED license plate lights, fog Lights, and interior LED lights), directional signal lights (DSLs), day time running lights, and stop lights. The headlights segment is expected to gain a higher market share in the future. Along with the rising number of accidents, the penetration rate of fog LED lamps and headlamps is anticipated to rise. Approximately 1.3 million people die each year as a result of road traffic crashes globally.

- In terms of volume share, in 2023, DSLs accounted for most of the market share (27.9%), followed by headlights (17.7%), others (miniature LED lights, LED license plate lights, fog Lights, and interior LED lights) (16.4%), and stop lights. The market share is expected to remain the same for all the segments during the forecast period, with a slight reduction in the others and stop lights segment and an increase in the DSLs and headlights segments. External lights (primarily signal lights) are highly likely to be affected in minor to major accidents in all types of vehicles and require replacement.

- EVs are one of the primary drivers for the surging demand for automotive LEDs globally. China led the EV market, accounting for 60% of global electric car sales in 2022, followed by Europe and the United States, which saw strong sales growth of 15% and 55%, respectively.

- The ambitious policy programs in major economies, such as the Fit for 55 package in the European Union and the Inflation Reduction Act in the United States, are expected to boost the market share of EVs. Key players in the market are also focusing on expanding their EV plants in developed nations.

Growth in EVs, autonomous vehicles, and government incentives are expected to boost the adoption of LED lights in the automotive industry

- In terms of value share, the Asia-Pacific automotive LED lighting market accounted for the majority share in 2022, followed by North America and Europe, respectively. The market share is expected to increase for Asia-Pacific in 2029, as most of the six Asian countries, such as China, Japan, Thailand, Taiwan, Malaysia, and India, have introduced incentives such as protecting their domestic markets and giving preferential treatment to automakers in promoting their automobile industries.

- In terms of volume share, the Asia-Pacific automotive LED lighting market accounted for the majority share in 2022, followed by Europe and North America. In Europe, the rise of electric vehicles and technological advances in the types of fuels used in vehicles are transforming the region's automotive industry. Sales of battery electric vehicles in the European Union are still growing rapidly. For example, 12.1% of the 9.1 million cars sold on the EU market in 2022 were pure battery electric vehicles. By contrast, in 2019, this share was just 1.9%, and in 2021 it was 9.1%.

- Electrification is the most significant transformation the industry is undergoing worldwide. Another trend rising is autonomous vehicles. It is important to note that technology contributes to auto companies' carbon-neutral goals. The Middle East is an important market for Nissan. Many modern vehicles are getting smarter and more connected. It will be equipped with intelligent mobility and autonomous driving, similar to the Nissan Ariya. Such transformations are undertaken in other parts of the region. Thus, growth in the regional automotive segment may increase the penetration of LEDs in the market.

Global Automotive LED Lighting Market Trends

The increasing demand for EVs is anticipated to raise the market value

- The total automobile production globally was 143.96 million units in 2022, and it was expected to reach 150.92 million units in 2023. The gathered data indicated a 16% reduction in the manufacturing of automotive cars in 2020, following a dismal 2019, which already showed a noticeable decline of roughly 5% in global auto output. The average decline across all of Europe was more than 21%. Sharp decreases in all major producing nations ranged from 11% to roughly 40%. Manufacturing in Europe accounted for roughly 22% of the total production. Vehicle manufacturing in the Americas accounted for 20% of global production in 2020. The African continent had a severe decrease of more than 35% in manufacturing. Asia, on the other hand, held up very well, with a decline of only 10%. According to the numbers provided, the COVID-19 pandemic had a tremendous impact on the automotive industry, which decreased the demand for LEDs.

- Volkswagen Group, Stellantis, Mercedes-Benz, BMW, Porsche, Hurtan, GTA Motors, Audi, TATA Motors, Mahindra & Mahindra, SAIC Motor, Hyundai Motor Company, Kia Corporation, KG Mobility, and Renault Korea Motors are the major automotive manufacturing companies globally. In 2022, there were more than 10 million electric vehicle sales worldwide, and the sales in 2023 were anticipated to increase by another 35% to a total of 14 million. Due to this rapid expansion, the market share of electric automobiles increased from 4% in 2020 to 14% in 2022. In addition, as more electric vehicles are being used, there is a rising demand for automotive semiconductor chips because they require more processors per vehicle than conventional cars. The market for LED lighting is expected to benefit from the increase in semiconductor demand in the automobile industry.

The increasing number of battery swapping stations and battery recycling service outlets and the rising demand for EVs are expected to drive the growth of the market

- The EV markets are expanding at an exponential rate, with sales exceeding 10 million in 2022. In 2022, electric vehicles accounted for 14% of all new vehicle sales, up from roughly 9% in 2021 and less than 5% in 2020. Global sales were led by three markets. China was the leader, accounting for almost 60% of global electric vehicle sales. China accounts for more than half of all the electric vehicles on the road worldwide, and the government has already exceeded its 2025 target for new energy vehicle sales.

- By 2022, China had 1,973 battery swapping stations, including 675 built in 2022 and over 10,000 power battery recycling service outlets. Thus, the rapid growth of charging facilities indicates the booming new energy vehicle (NEV) sector in the country. In October 2022, the German government unveiled plans to boost charging infrastructure for electric vehicles. The plan consisted of a EUR 6.3 billion (USD 6.17 billion) proposal that would increase the number of charging points across the country to 1 million by 2030.

- In major markets, electric car sales were normally low in 2022, but it was a growth year in India, Thailand, and Indonesia. Sales of electric vehicles in these countries more than tripled since 2021, reaching 80,000 units. In the United States, the Inflation Reduction Act (IRA), combined with a number of states adopting California's Advanced Clean Cars II rule, is likely to produce a 50% market share for electric cars in 2030, in line with the national target. Considering the abovementioned instances, key manufacturers across the world are expected to invest more in developing and producing automotive LEDs.

Automotive LED Lighting Industry Overview

The Automotive LED Lighting Market is moderately consolidated, with the top five companies occupying 51.31%. The major players in this market are HELLA GmbH & Co. KGaA (FORVIA), KOITO MANUFACTURING CO., LTD., Marelli Holdings Co., Ltd., OSRAM GmbH. and Stanley Electric Co., Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 Argentina

- 4.11.2 Brazil

- 4.11.3 China

- 4.11.4 France

- 4.11.5 Germany

- 4.11.6 Gulf Cooperation Council

- 4.11.7 India

- 4.11.8 Japan

- 4.11.9 South Africa

- 4.11.10 South Korea

- 4.11.11 Spain

- 4.11.12 United Kingdom

- 4.11.13 United States

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.2 Europe

- 5.3.3 Middle East and Africa

- 5.3.4 North America

- 5.3.5 South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 GRUPO ANTOLIN IRAUSA, S.A.

- 6.4.2 HELLA GmbH & Co. KGaA (FORVIA)

- 6.4.3 Hyundai Mobis

- 6.4.4 KOITO MANUFACTURING CO., LTD.

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 Nichia Corporation

- 6.4.7 OSRAM GmbH.

- 6.4.8 Signify (Philips)

- 6.4.9 Stanley Electric Co., Ltd.

- 6.4.10 Valeo

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 224 Pages

- 納期

- 2~3営業日