|

|

市場調査レポート

商品コード

1683929

欧州の自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の自動車用LED照明:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

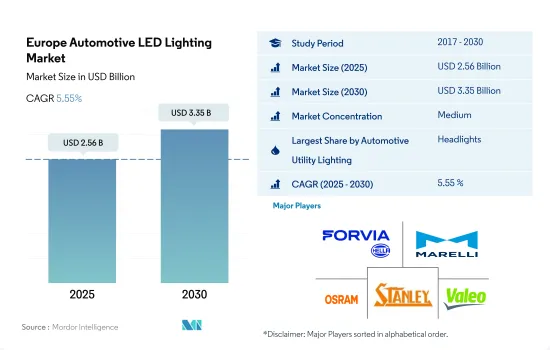

欧州の自動車用LED照明市場規模は、2025年に25億6,000万米ドルと推定され、2030年には33億5,000万米ドルに達し、予測期間(2025-2030年)のCAGRは5.55%で成長すると予測されています。

メーカーはLEDによる車外照明の認可を取得し、自動車メーカーはLED照明の使用を増やすために交通安全、技術、デジタル化に投資すると予想されます。

- 金額シェアでは、2023年にはヘッドライトが大半を占め、次いでその他のライトと方向指示灯が続きます。ヘッドライトは日常的な死者や事故を減少させました。前年の交通事故死者数は約20,600人で、パンデミックからの回復に伴い2021年から3%増加しました。しかし、これはパンデミック前の2019年と比較すると、交通事故死者数が2,000人減少(10%減)したことになります。EUと国連は2030年までに交通事故死者数を削減するという目標を掲げています。したがって、既存の交通事故死者数を減らすために、自動車にLEDヘッドライトが装着されることが期待されています。

- 数量シェアでは、2023年には方向指示灯が大半を占め、次いでヘッドライト、その他のライトと続きます。これらのライトの市場シェアは、ほとんど変動することなく変わらないと予想されます。フォルクスワーゲン、ダイムラー、ボッシュ、ZF、その他欧州のトップサプライヤーなどの自動車メーカーは、デジタル化、エレクトロモビリティと運転、水素技術、交通安全に今後数年間で(1,619億米ドル)を費やします。これにより、信号灯の使用が増加するため、国内でのLEDライトの使用が増加します。

- 同市場の主要自動車メーカーは、電気自動車市場の拡大に注力しています。このため、2009年4月23日付の欧州議会と欧州理事会は、理事会規則(EC)No.443/2009に基づき、小型商用車からのCO2排出量を削減するための共同体の統合的アプローチの一環として、新型乗用車の排出ガス基準を設定しました。各メーカーは共同で、内燃機関搭載車および外部充電を必要としないハイブリッド電気自動車向けの革新的技術として、LEDによる効率的な車外照明の認可を申請しました。このことが国産LED照明の市場シェアを拡大しました。

自動車のCO2排出量を削減するための規制の高まりと、EV需要を高めるための磁気電気モーターの開発が市場の成長を後押しすると予想されます。

- この分野では、その他欧州が2023年に30%以上の市場シェアを占めると予想され、次いでドイツが20%以上、スペインが15%以上の市場シェアを占める。これは商用車、二輪車、乗用車の増加によるものです。電気自動車の普及拡大も、欧州の他の地域での市場成長に対応すると予想されます。

- 2021年には、ポーランドは非常に古い乗用車の割合が最も高く、乗用車の41.3%が20年以上経過していました。2023年の新興諸国における乗用車の前向きな開発は、国レベルでも反映されました。最も力強い成長を記録したのはスペイン(+51.4%)とイタリア(+19.0%)であり、次いでフランス(+8.8%)は緩やかではあるが着実な成長でした。ハイブリッド電気自動車(HEV)も2021年に好調なスタートを切りました。販売台数は22.1%増の19万7,982台となりました。これは、この地域の4大市場での2桁成長が牽引した:スペイン(59.3%増)、イタリア(24.7%増)、ドイツ(19.0%増)、フランス(12.5%増)です。その結果、市場シェアは26.0%となり、2022年1月と比較して2.3ポイント改善しました。

- 自動車のCO2排出量削減を目的とした政府規制は、欧州自動車メーカーによるLED光源の採用をさらに後押しすると思われます。自動車メーカーはまた、持続可能性に貢献するための新しいプログラムを数多く立ち上げています。例えば、電気自動車(EV)用の、より安価で、より効率的で、より高出力の永久磁石電気モーターを開発するための欧州の新しい研究開発プログラムは、2023年に開始される予定でした。モンドラゴン大学は欧州の8つのパートナーからなるコンソーシアムを率いており、GKNオートモーティブも参加しています。

欧州自動車用LED照明市場動向

EV販売の増加が欧州のLED市場を牽引する見込み

- 韓国の自動車総生産台数は2022年に1,767万台、2023年には1,833万台に達すると予想されています。中国初の工場閉鎖は欧州自動車セクターのサプライチェーンを混乱させました。EU加盟国全体の自動車工場の平均ダウンタイムは30日で、スウェーデンのダウンタイムが最も短く(15日)、イタリアのダウンタイムが最も長かった(41日)。EUの自動車部門は2020年上半期に360万台の生産台数を失い、1,000億ユーロ(1,079億米ドル)の損失を計上しました。この数字は2020年9月末までに402万4,036台まで上昇し、EUの2020年生産台数の22.3%を占めました。欧州におけるこのような生産減は、最終的に自動車セクターのLED照明に悪影響を与えました。

- フォルクスワーゲン・グループ、ステランティス、メルセデス・ベンツ、BMW、ポルシェ、Hurtan、GTAモーターズ、アウディ、プジョーがこの地域の主要自動車メーカーです。EVの台頭と、自動車に使用される燃料タイプの技術的進歩により、この地域の自動車産業は大きな変貌を遂げています。EUにおけるバッテリー式電気自動車の販売台数は、現在も急速に増加しています。例えば、2022年にEU市場で販売された910万台のうち12.1%が完全バッテリー電気自動車であったのに対し、2019年のシェアはわずか1.9%、2021年は9.1%でした。販売台数の約22.6%はハイブリッド電気自動車で、9.4%は最近の環境に優しいプラグインハイブリッド車でした。EVの普及に伴い、車載照明用の半導体やLEDの需要は、その効率の高さから高いです。

EV登録台数の増加とEV普及のための政府政策がLED市場の成長を促進する可能性

- 欧州全域でEVの普及が急速に進んでいます。欧州における電気自動車(BEV、PHEV、EREV、FCEV)の販売台数は259万台で、2021年比15%増、2020年比92%増となりました。2022年の欧州におけるEV販売シェアは、ノルウェー(79%)、スウェーデン(33%)、オランダ(23%)、デンマーク(21%)が最も高く、フィンランド、スイス、ドイツがそれぞれ18%で続いた。2022年の市場シェアでは、バッテリー式電気自動車(BEV)が全体の12.1%を占め、2021年の9.1%、2019年の1.9%から上昇しました。

- 2016年、英国のバッテリー電気自動車は3万669台であったが、2023年5月には78万4,968台に達しました。2022年には26万5,000台以上のバッテリー電気自動車が登録され、2021年比で40%増加しました。英国政府は、英国における電気自動車の登録台数を増やすため、EVを選択する人々を強力に支援しています。購入者は、新車のEVに最大2,500ユーロ(2,699米ドル)の割引を提供するプラグイン補助金の恩恵を受けることができます。またスコットランドでは、EVの新車・中古車購入に無利子ローンを提供しています。

- フランスは自動車産業再編戦略の一環として、2020年5月に補助金の引き上げを計画していました。主な理由は、COVID-19の大流行による販売の落ち込みです。その際、補助率の上限は6,479米ドルから7,558.8米ドルに引き上げられました。2021年半ばには、上限が7,558.8米ドルから6,478.9米ドルに引き下げられました。2023年、政府は2023年1月から電気自動車への補助金を6,478.9米ドルから5,399米ドルに引き下げました。また、2030年までに年間200万台の電気自動車を生産するという目標も掲げています。このような市場の進歩により、この地域の自動車用LEDの需要は今後数年で増加すると見られています。

欧州の自動車用LED照明産業概要

欧州の自動車用LED照明市場は適度に統合されており、上位5社で48.57%を占めています。この市場の主要企業は以下の通りです。HELLA GmbH & Co. KGaA, Marelli Holdings, OSRAM GmbH., Stanley Electric and Valeo(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 自動車生産台数

- 人口

- 一人当たり所得

- 自動車ローン金利

- 充電ステーション数

- 自動車保有台数

- LED総輸入数

- 世帯数

- 道路ネットワーク

- 普及率

- 規制の枠組み

- フランス

- ドイツ

- スペイン

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 自動車用ユーティリティ照明

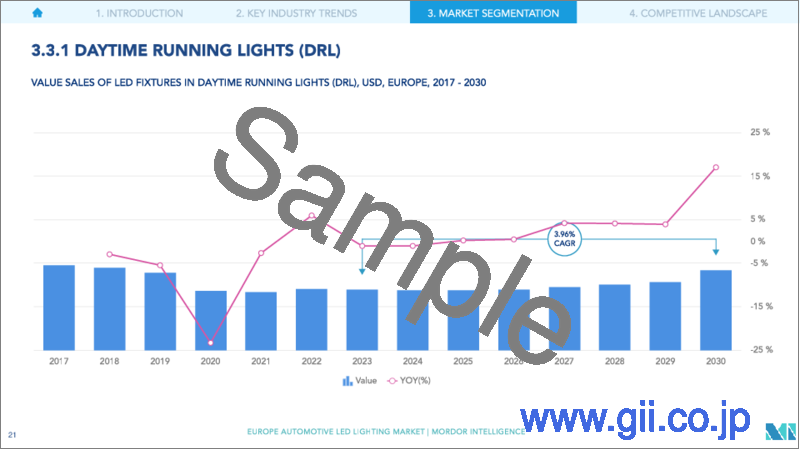

- デイタイム・ランニング・ライト(DRL)

- 方向指示器

- ヘッドライト

- リバースライト

- ストップライト

- テールライト

- その他

- 自動車用照明

- 2輪車

- 商用車

- 乗用車

- 国名

- フランス

- ドイツ

- スペイン

- 英国

- その他欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- HELLA GmbH & Co. KGaA

- HYUNDAI MOBIS

- KOITO MANUFACTURING CO., LTD.

- Marelli Holdings Co., Ltd.

- OSRAM GmbH.

- Phoenix Lamps Ltd(Suprajit Engineering Ltd)

- Signify(Philips)

- Stanley Electric Co., Ltd.

- Valeo

- ZKW Group

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Europe Automotive LED Lighting Market size is estimated at 2.56 billion USD in 2025, and is expected to reach 3.35 billion USD by 2030, growing at a CAGR of 5.55% during the forecast period (2025-2030).

Manufacturers are expected to get approval for exterior vehicle lighting with LED and automakers are expected to invest in road safety, technology, and digitization to increase the use of LED lights

- In terms of value share, in 2023, headlights accounted for the majority, followed by other lights and directional signal lights. Headlights have reduced daily fatalities and accidents. About 20,600 people died in road crashes the previous year, up by 3% from 2021 as traffic recovered from the pandemic. However, this represented 2,000 fewer road fatalities (10% less) compared to the pre-pandemic year of 2019. The goal of reducing road fatalities by 2030 was set by the EU and UN. Hence, it is expected that vehicles will be fitted with LED headlights to reduce the existing rate of road fatalities.

- In terms of volume share, in 2023, directional signal lights accounted for the majority, followed by headlights and other lights. The market share of these lights is expected to remain the same with little fluctuation. Automakers such as Volkswagen, Daimler, Bosch, ZF, and other top European suppliers will spend (USD 161.9 billion) over the next few years on digitalization, electromobility and driving, hydrogen technology, and road safety. This will increase the use of signal lights, thus increasing the use of LED lights in the country.

- The major automakers in the market are focusing on expanding the electric vehicle market. To this end, the European Parliament and Council of 23 April 2009 set emissions standards for new passenger cars as part of the community's integrated approach to reducing CO2 emissions from light commercial vehicles under Council Regulation (EC) No. 443/2009. Manufacturers jointly applied for the approval of efficient exterior vehicle lighting with LED as an innovative technology for vehicles with internal combustion engines and hybrid electric vehicles that do not require external charging. This factor increased the market share of domestic LED lighting.

Increasing regulations to reduce vehicle CO2 emissions and the development of magnetic electric motors to boost EV demand are expected to boost the market's growth

- In this segment, the Rest of Europe is expected to occupy a market share of more than 30% in 2023, followed by Germany and Spain, with market shares of more than 20% and 15%, respectively. This is due to an increase in the number of commercial vehicles, two-wheelers, and passenger cars. An increase in electric vehicle adoption is also anticipated to correspond to the market's growth in other parts of Europe.

- In 2021, Poland had the highest proportion of very old passenger cars, with 41.3% of passenger cars being over 20 years old. The positive development of passenger cars in the region in 2023 was reflected at the country level. The strongest growth was recorded in Spain (+51.4%) and Italy (+19.0%), followed by France (+8.8%), which had slow but steady growth. Hybrid electric vehicles (HEVs) also got off to a strong start in 2021. Sales increased by 22.1% to 197,982 units. This was driven by double-digit growth in the region's four largest markets: Spain (+59.3%), Italy (+24.7%), Germany (+19.0%), and France (+12.5%). This resulted in a market share of 26.0%, an improvement of 2.3 points compared to January 2022.

- Government regulations aimed at reducing vehicle CO2 emissions will further encourage the adoption of LED light sources by European automakers. Automakers are also launching a number of new programs to contribute to sustainability. For example, a new European R&D program to develop cheaper, more efficient, and power-dense permanent magnet electric motors for electric vehicles (EVs) was expected to start in 2023. Mondragon University leads the consortium of eight European partners and includes GKN Automotive.

Europe Automotive LED Lighting Market Trends

Increasing EV sales are expected to drive the LED market in Europe

- The total automobile vehicle production in South Korea was 17.67 million units in 2022, and it is expected to reach 18.33 million units in 2023. The first Chinese factory closures disrupted the supply chains of the European automotive sectors. The average downtime for automotive plants throughout EU Member States was 30 days, with Sweden experiencing the most minor downtime (15 days) and Italy experiencing the highest (41 days). The EU automobile sector lost 3.6 million vehicles from production in the first half of 2020, amounting to a loss of EUR 100 billion (USD 107.9 billion). This number climbed to 4,024,036 motor vehicles by the end of September 2020, accounting for 22.3% of the EU's 2020 production. Such production loss in Europe ultimately had a negative impact on LED lights in the automotive sector.

- Volkswagen Group, Stellantis, Mercedes-Benz, BMW, Porsche, Hurtan, GTA Motors, Audi, and Peugeot are the major automotive car manufacturers in the region. With the rise in EVs and technological advancements in the fuel types utilized in vehicles, the region is seeing a significant transformation in its automotive industry. Battery electric vehicle sales in the EU are still rising quickly. For instance, 12.1% of the 9.1 million vehicles sold in EU markets in 2022 were fully battery electric vehicles, as compared to a share of just 1.9% in 2019 and 9.1% in 2021. About 22.6% of sales were made up of hybrid electric cars, and 9.4% of sales were made up of the more recent and eco-friendly plug-in hybrids. With the growing usage of EVs, the demand for semiconductors and LEDs in vehicle lighting is high due to their efficiency.

Increasing EV registrations and government policies for EV adoption may drive the growth of the LED market

- The adoption of EVs across Europe is growing rapidly. In Europe, sales of electric vehicles (BEVs, PHEVs, EREVs, and FCEVs) totaled 2.59 million units, up by 15% from 2021 and by 92% from 2020. Norway (79%), Sweden (33%), the Netherlands (23%), and Denmark (21%) had the highest market shares of EV sales in Europe in 2022, followed by Finland, Switzerland, and Germany, with an 18% share of EV registrations each in Europe in 2022. In 2022, battery electric vehicles (BEVs) accounted for 12.1% of the total market share, up from 9.1% in 2021 and 1.9% in 2019.

- In 2016, the number of battery-electric cars in the United Kingdom was 30,669, and by May 2023, this number reached 784,968. More than 265,000 battery-electric vehicles were registered in 2022, a 40% increase over 2021. The British government strongly supports the people who are choosing EVs to increase the number of registered electric vehicles in the United Kingdom. Buyers can benefit from the Plug-In Grant, which offers a discount of up to EUR 2,500 (USD 2,699) on new EVs. Scotland also offers interest-free loans on purchases of new and used EVs.

- As part of a restructuring strategy for the automotive industry, France planned to raise subsidy rates in May 2020. The main reason was a drop in sales caused by the COVID-19 pandemic. The maximum subsidy rate was increased from USD 6,479 to USD 7,558.8 at the time. In mid-2021, the maximum rate was reduced from USD 7,558.8 to USD 6,478.9. In 2023, the government reduced subsidies for electric cars to USD 5,399 from USD 6,478.9, effective from January 2023. It also set a target of producing two million electric vehicles per year by 2030. These advancements in the market are expected to drive the demand for automotive LEDs in the region in the coming years.

Europe Automotive LED Lighting Industry Overview

The Europe Automotive LED Lighting Market is moderately consolidated, with the top five companies occupying 48.57%. The major players in this market are HELLA GmbH & Co. KGaA, Marelli Holdings Co., Ltd., OSRAM GmbH., Stanley Electric Co., Ltd. and Valeo (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 France

- 4.11.2 Germany

- 4.11.3 Spain

- 4.11.4 United Kingdom

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Spain

- 5.3.4 United Kingdom

- 5.3.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 HELLA GmbH & Co. KGaA

- 6.4.2 HYUNDAI MOBIS

- 6.4.3 KOITO MANUFACTURING CO., LTD.

- 6.4.4 Marelli Holdings Co., Ltd.

- 6.4.5 OSRAM GmbH.

- 6.4.6 Phoenix Lamps Ltd (Suprajit Engineering Ltd)

- 6.4.7 Signify (Philips)

- 6.4.8 Stanley Electric Co., Ltd.

- 6.4.9 Valeo

- 6.4.10 ZKW Group

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms