|

市場調査レポート

商品コード

1644788

欧州のリアルタイム決済:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Real Time Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のリアルタイム決済:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

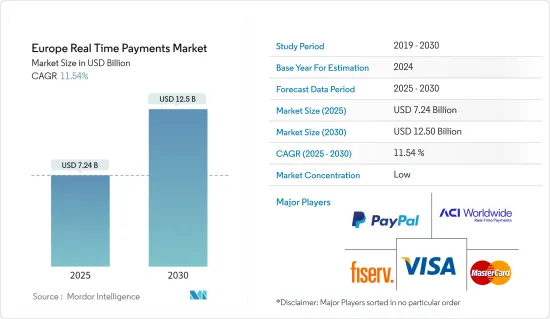

欧州のリアルタイム決済の市場規模は2025年に72億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは11.54%で、2030年には125億米ドルに達すると予測されます。

スマートフォンの急速な普及、迅速な決済を求める消費者のニーズ、欧州地域における政府の取り組みなどが、市場の成長を促す主な要因となっています。

主なハイライト

- 欧州全域でリアルタイム決済の普及率が高まり、インフラが継続的に開発・進化していることから、同地域では今後数年間、リアルタイム決済が力強い成長を遂げることが見込まれます。英国やオランダを含むほとんどの欧州市場では、リアルタイム資金移動の件数と金額が大きく伸びています。北欧地域でのP27のイントロダクションより、リアルタイム決済市場の成長が見込まれます。

- 欧州決済協議会(EPC)は、欧州におけるリアルタイム決済の開発を加速させるため、汎欧州インスタント決済システムを設計しました。SEPA Instant Credit Transfer(SCT Inst)プロセスは、EPCの現行のSEPA Credit Transfer(SCT)スキームに基づいています。

- さらに、この決済システムでは、欧州36カ国に順次拡大される地域の口座で、いつでも数秒で資金が利用可能になるユーロ信用送金が可能です。いくつかの地域銀行がSEPA Instant Credit Transfer(SCT inst.)を利用しています。例えばシティは、欧州全域で単一ユーロ決済圏(SEPA)即時決済を導入したばかりです。

- さらに、欧州ではISO20022に基づくリアルタイム決済の取り組みがいくつか存在します。英国ではニュー・ペイメント・アーキテクチャー(NPA)、北欧諸国ではP27、ドイツではSCT Inst.があり、EUでは欧州ペイメント・イニシアチブ(EPI)が推進されています。これらのリアルタイム決済システムは、よりシンプルなアクセスを提供することで参加者を増やし、継続的な安定性と弾力性を高め、リアルタイム決済市場の競争激化を通じてイノベーションを促進します。

- さらに、ISO 20022の利用により、国境を越えた地域間の接続性が向上し、新たなサービスの構築に利用できるデータフレームが追加されることが期待されます。さらに、スウェーデン、スペイン、デンマーク、ポーランドなど、EUの多くの国々ではモバイルやインターネットの普及が進んでおり、同地域におけるリアルタイム決済の成長に強力な足場を提供しています。

- しかし、Authorized Push決済のようなリアルタイム決済における不正行為の増加は、同地域のリアルタイム決済市場の成長を妨げる可能性があります。PSD2に対応するための3Dセキュア2.2プロトコルやその他のSCA技術により、同地域のカード不正は減少したが、オーソライズドプッシュペイメントの不正は同地域で増加しました。

- COVID-19の大流行は、当地域の人々の買い物や支払い方法に多大な影響を与えました。リアルタイム決済やデジタル決済を含む新たな慣行は、顧客にとってより便利であり、今後数年で成長する可能性が高いです。

欧州のリアルタイム決済市場動向

スマートフォンの普及が市場成長を促進する見込み

- 多くの欧州諸国でスマートフォンの普及が進み、同地域のリアルタイム決済市場が拡大しています。GSMA Intelligenceが報告したデータによると、2023年初頭のフィンランドのスマートフォン普及率は総人口の169.5%でした。同様に、オーストリア、ドイツ、スペイン、英国など他の欧州諸国では、それぞれ総人口の138.8%、141%、119%、105%でした。

- さらに、多くのeコマースプラットフォームが同地域のeコマースユーザーにリアルタイム・クレジットや後払いサービスを提供しているため、モバイル・コマースの台頭は同地域でのリアルタイム決済をさらに促進しています。

- 消費者は、手頃な価格と利便性からモバイルBNPLサービスを好みます。BNPL、消費者信用、またはアフターペイは、消費者が金銭のみを支払うことを可能にします。BNPLサービスを提供する欧州の主要企業には、Klarna、PayPal Credit、Splitなどがあります。

- さらに、個人間(P2P)や個人から企業(P2B)へのリアルタイムの資金移動のためにスマートフォンの利用が増加していることは、地域全体におけるスマートフォンの普及率の高さにも支えられています。これらの要因により、予測期間中、欧州のリアルタイム決済市場はさらに拡大すると予想されます。

最大のシェアを占めると予想される英国

- 英国では、Pay.the U.K.が運営するFaster Payments System(FPS)と呼ばれるリアルタイム決済システムが2008年に開始されて以来、リアルタイム決済が可能となっています。さらに、Faster Payment Systemは、同国のモバイル決済サービスであるPaymにも対応しており、携帯電話番号を使って家族や友人、中小企業への支払いを可能にしています。

- さらに、国内のほとんどの金融機関がFPSに参加しているため、何百万人もの人々に利用されています。さらに、この地域の多くの銀行がFPSを採用しています。例えば、2022年5月、主要企業のひとつであるロンドン銀行は、英国の24時間365日リアルタイム決済インフラであるFPS(Faster Payment System)の直接接続決済参加者になったと発表しました。

- 英国の決済インフラは、消費者がリアルタイム決済にアクセスするのが簡単で安価であるにもかかわらず、依然として従来のツール、特にカードに強く結びついています。さらに、英国におけるリアルタイム決済は、日常的な支出ではなく、少量、高額な送金が中心となっています。しかし、このシナリオは絶えず変化しており、同地域ではリアルタイム決済の採用が増加しており、予測期間中にさらに拡大する見込みです。

- 英国はさらに、英国のリアルタイム決済システムの成長を支えています。例えば、リアルタイム決済事業者のPay.U.K.はNew Payments Architecture(NPA)プログラムの一環としてFaster Payments Serviceの近代化を進めており、これにはISO 20022に対応した新しい中央インフラの調達も含まれています。新ペイメント・アーキテクチャー(NPA)は、英国におけるリアルタイム決済の成長を拡大する、弾力性と拡張性のあるプラットフォームとなります。

- 上記の要因はすべて、予測期間を通じて英国のリアルタイム決済業界の需要を押し上げると予想されます。

欧州のリアルタイム決済産業の概要

欧州のリアルタイム決済市場の競合は激化しており、多数のプレーヤーが存在するため市場は断片化しているように見えます。これらの市場競争プレーヤーは、革新的な決済ソリューションを提供し、競争優位性を獲得するためにM&Aなど様々な戦略に取り組んでいます。欧州リアルタイム決済市場の主要企業には、ACI Worldwide Inc.、Fiserv Inc.、Mastercard Inc.、Visa Inc.などが含まれます。

- 2023年6月- 世界のペイテック企業であるACIワールドワイドは、欧州および英国の加盟店向けにリアルタイム決済ソリューション「ACI Instant Pay」の提供を開始しました。インスタント・ペイを利用する加盟店は、ACIのペイメント・オーケストレーション・プラットフォームとの単一のAPI統合を通じて、オンライン、モバイル、店舗での即時決済を受け付けることができます。

- 2023年4月-PayPalのオンライン決済ソリューションにより、中小企業はPayPal決済、クレジットカード、デビットカード、デジタルウォレットなどを利用できるようになります。また、インターチェンジ・プラス(IC++)価格でのグロス決済など、中小企業のビジネス運営に役立つ機能も利用できるようになります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 欧州における決済環境の進化

- 欧州におけるキャッシュレス取引の拡大に関連する主な市場動向

- COVID-19が欧州の決済市場に与える影響

第5章 市場力学

- 市場促進要因

- スマートフォン普及率の増加

- 従来型バンキングへの依存度の低下

- リアルタイム決済の即時性と利便性

- 市場の課題

- 公認プッシュペイメント詐欺などの決済詐欺

- ドイツなど主要国における現金依存の現状

- 市場機会

- デジタル決済の成長を奨励する政府政策により、一般消費者の間でリアルタイム決済の成長が期待されます。

- デジタル決済業界における主な規制と基準

- 世界各国の規制状況

- 規制上の障害となりうるビジネスモデル

- ビジネス情勢の変化に伴う開発余地

- 主要事例と使用事例の分析

- 全取引に占めるリアルペイメント取引のシェアと主要国の取引量・取引額の地域別分析

- 非現金取引に占めるリアルペイメント取引の割合と主要国の地域別取引量分析

第6章 市場セグメンテーション

- 決済タイプ別

- P2P

- P2B

- 国別

- 英国

- ドイツ

- フランス

- イタリア

- その他欧州

第7章 競合情勢

- 企業プロファイル

- ACI Worldwide Inc.

- Fiserv Inc.

- Paypal Holdings Inc.

- Mastercard Inc.

- VISA Inc.

- FIS Global

- Apple Inc.

- Finastra

- Volante Technologies Inc

- Nets(Nexi Group)

第8章 投資分析

第9章 市場の将来展望

The Europe Real Time Payments Market size is estimated at USD 7.24 billion in 2025, and is expected to reach USD 12.50 billion by 2030, at a CAGR of 11.54% during the forecast period (2025-2030).

The rapid proliferation of smartphones, consumers' need for quicker settlements, and government initiatives in the European region, among others, are the key reasons driving the market's growth.

Key Highlights

- Increasing real-time payment adoption rates and continuous development and evolution of infrastructure across Europe indicate strong growth of real-time payments in the region in the coming years. Most European markets, including the UK and the Netherlands, experienced significant growth in volumes and values of real-time fund transfers; with the introduction of the P27 in the Nordic region, the real-time payment market is anticipated to grow.

- The European Payments Council (EPC) designed a pan-European instant payment system to accelerate the development of real-time payments in Europe. The SEPA Instant Credit Transfer (SCT Inst) process is based on the EPC's current SEPA credit transfer (SCT) scheme.

- Furthermore, this payment system enables euro credit transfers, with funds becoming available on the account in seconds at any time and in a region that will progressively expand to encompass 36 European countries. Several regional banking institutions are using SEPA Instant Credit Transfer (SCT inst.). Citi, for example, just implemented Single Euro Payments Area (SEPA) Instant Payments throughout Europe.

- Moreover, several initiatives based on ISO 20022 for real-time payments exist in Europe. In the United Kingdom, there is the New Payments Architecture (NPA), P27 in the Nordic region countries, SCT Inst. in Germany, and the EU is pushing on with the European Payments Initiative (EPI). These real-time payment systems will provide simpler access for increased participation, boost ongoing stability and resilience, and increase innovation through greater competition in the real-time payments market.

- Furthermore, the use of ISO 20022 is anticipated to improve cross-border and regional connectivity and enable additional data frames that can use to build new services. Furthermore, strong mobile and internet penetration in many countries of the EU, such as Sweden, Spain, Denmark, Poland, etc., is providing a strong platform for the growth of real-time payments in the region.

- However, growing payment frauds in real-time payments, such as Authorized Push payments, can hamper the growth of the real-time payments market in the region. With the 3D Secure 2.2 protocol and other SCA technologies to accommodate PSD2, card fraud in the region declined, but Authorized Push Payments frauds increased in the region.

- The COVID-19 pandemic enormously impacted how people shop and pay in the region. The new practices, including real-time and digital payments, are more convenient for customers and are likely to grow in the coming years.

Europe Real Time Payments Market Trends

Rising Penetration of Smartphone is Expected to Foster the Market Growth

- The increasing penetration of smartphones across many European countries is increasing the real-time payment market in the region. As per data reported by GSMA Intelligence, the smartphone penetration in Finland at the start of 2023 was 169.5% of the total population. Similarly, in other European countries such as Austria, Germany, Spain, and the United Kingdom was 138.8%, 141%, 119%, and 105% of the total population, respectively.

- Furthermore, the rise of mobile commerce is further proliferating real-time payments in the region as many e-commerce platforms offer real-time credit or buy now pay later services to the e-commerce users in the region.

- Consumers prefer mobile BNPL services due to their affordability and convenience. BNPL, consumer credit, or after-pay enables consumers to pay money only. Some key European players offering BNPL service include Klarna, PayPal Credit, and Splitit.

- Furthermore, the increasing adoption of smartphone usage for real-time fund transfer from Person to Person (P2P) and Person to business (P2B) is further supported by the strong smartphone penetration across the region. These factors are further expected to augment the real-time payments market in Europe over the forecast period.

United Kingdom is Anticipated to Hold the Largest Share

- Real-time payments have been available in the United Kingdom since 2008 with the launch of the U.K.'s real-time payments system called the Faster Payments System (FPS), operated by Pay. the U.K. in the country. Furthermore, the Faster Payment System also powers Paym, the country's mobile payments service, making it possible to pay family, friends, and small businesses using mobile numbers.

- Furthermore, most financial institutions in the country are participants of the FPS, making it reach millions of people. Moreover, many banking institutions in the region are adopting FPS. For instance, in May 2022, The Bank of London, one of the leading-edge technology companies, announced that it had become a Directly Connected Settling Participant of the Faster Payment System (FPS), the United Kingdom's 24*7 real-time payments infrastructure.

- Payment infrastructure in the United Kingdom is still very much tied to traditional tools, especially cards, despite being easy and cheap for consumers to access real-time payments. Further, real-time payments in the U.K. are still focused on low-volume, high-value transfers, not everyday expenditures. However, the scenario is continuously changing, and the adoption of real-time payments is increasing in the region and is further expected to grow over the forecast period.

- The U.K. further supports the growth of the United Kingdom's real-time payments system. For instance, real-time payments operator Pay. U.K. is modernizing the Faster Payments Service as part of its New Payments Architecture (NPA) program, which also involves procuring a new ISO 20022-ready central infrastructure. The New Payments Architecture (NPA) will be a resilient, scalable platform that will expand the growth of real-time payments in the United Kingdom.

- All the abovementioned factors are expected to boost demand for the UK real-time payments industry throughout the forecast period.

Europe Real Time Payments Industry Overview

The competition in the Europe real-time payments market is intensifying, and the market appears to be fragmented due to the presence of numerous players. These market players offer innovative payment solutions and are involved in various strategies, such as mergers and acquisitions, to gain a competitive advantage. Major players in the Europe real-time payments market include ACI Worldwide Inc., Fiserv Inc., Mastercard Inc., and Visa Inc., among others.

- June 2023 - Global paytech firm ACI Worldwide has launched ACI Instant Pay, a real-time payment solution for European and UK merchants. Merchants using Instant Pay can accept instant online, mobile, and in-store payments through a single API integration with the ACI payments orchestration platform.

- April 2023 - PayPal's online payment solution enables SMBs to accept PayPal payments, credit and debit cards, digital wallets, and more. Beginning, SMBs will also be able to accept payments with Apple Pay, allow their customers to save payment methods with the PayPal vault and keep their cards up to date with real-time account updater, as well as get access to features to help them run their business including interchange plus (IC++) pricing with gross settlement.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness-Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Evolution of the payments landscape in Europe

- 4.4 Key market trends pertaining to the growth of cashless transaction in Europe

- 4.5 Impact of COVID-19 on the payments market in Europe

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Smartphone Penetration

- 5.1.2 Falling Reliance on Traditional Banking

- 5.1.3 Immediacy and Ease of Convenience of the Real Time Payments

- 5.2 Market Challenges

- 5.2.1 Payment Fraud such as Authorized Push Payment Scams

- 5.2.2 Existing Dependence on Cash in Major Countries such as Germany

- 5.3 Market Opportunities

- 5.3.1 Government Policies Encouraging the Growth of Digital Paymentis expected to aid the growth of Real Time Payment methods amongst commoners

- 5.4 Key Regulations and Standards in the Digital Payments Industry

- 5.4.1 Regulatory Landscape Across the World

- 5.4.2 Business Models with Potential Regulatory Roadblocks

- 5.4.3 Scope for Development in Lieu of Evolving Business Landscape

- 5.5 Analysis of major case studies and use-cases

- 5.6 Analysis of Real Payments Transactions as a share of all Transactions with a regional breakdown of key countries by volume and transacted value

- 5.7 Analysis of Real Payments Transactions as a share of Non-Cash Transactions with a regional breakdown of key countries by volumes

6 Market Segmentation

- 6.1 By Type of Payment

- 6.1.1 P2P

- 6.1.2 P2B

- 6.2 By Country

- 6.2.1 United Kingdom

- 6.2.2 Germany

- 6.2.3 France

- 6.2.4 Italy

- 6.2.5 Rest of Europe

7 Competitive Landscape

- 7.1 Company Profiles

- 7.1.1 ACI Worldwide Inc.

- 7.1.2 Fiserv Inc.

- 7.1.3 Paypal Holdings Inc.

- 7.1.4 Mastercard Inc.

- 7.1.5 VISA Inc.

- 7.1.6 FIS Global

- 7.1.7 Apple Inc.

- 7.1.8 Finastra

- 7.1.9 Volante Technologies Inc

- 7.1.10 Nets (Nexi Group)