|

市場調査レポート

商品コード

1644508

インドのコワーキングオフィススペース:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)India Co-working Office Spaces - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのコワーキングオフィススペース:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

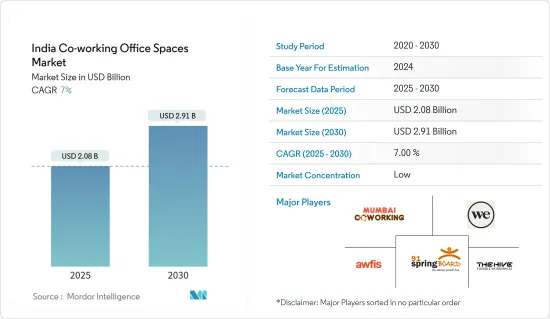

インドのコワーキングオフィススペース市場規模は2025年に20億8,000万米ドルと予測され、予測期間(2025-2030年)のCAGRは7%で、2030年には29億1,000万米ドルに達すると予測されます。

主なハイライト

- パンデミック(世界的大流行)により、従来のワークスペースが危機に直面したため、国内ではコワーキングスペースの成長が加速しました。多くの企業がコワーキングスペースを利用するようになったのは、手頃な価格と作業エリアの柔軟性が理由です。また、コワーキングスペースは安全な労働環境を確実に提供します。

- このセクターは、フリーランサー、中小企業(SME)、新興企業からの需要の高まりによって牽引されています。コワーキングスペースは手ごろな価格で最高の設備を提供しているため、この業界が提供するメリットを実感した大企業もコワーキングスペースを導入しています。また、投資流入率の高い新興企業の増加が、この業界の堅調な成長をもたらしています。

- コワーキングスペース業界は、フレキシブルなオフィススペースに対する需要の高まりを受けて、前年は回復基調にあった。コワーキングスペースはインドの企業の間で人気が高まっており、過去4年間で需要が倍増しています。2023年第1四半期、コワーキングスペースは上位7都市で820万平方フィートの純吸収面積の27%を占め、2019年第1四半期の14%から大幅に上昇しました。

- ベンガルールと首都圏(NCR)を合わせると、2023年第1四半期のコワーキングスペースの純吸収面積の3分の2を占めました。プネとチェンナイは同期間に合わせて約52万平方フィートのコワーキングスペースを吸収しました。上位7都市では、コワーキングスペースの純吸収量が90%増と著しい伸びを示し、2019年第1四半期の130万平方フィートから2023年第1四半期には約218万平方フィートに拡大しました。

- フレキシー事業者によるリーシングのシェアはベンガルールが最も高く、ムンバイ、デリー-NCRがこれに続いた。インドでは、新興企業が最初にコワーキングオフィススペースの需要を牽引し、その後、多国籍企業や大企業がコワーキングオフィススペースのスペース確保に踏み切った。

インドのコワーキングオフィススペース市場動向

コスト最適化が同分野の著しい成長を牽引

インドでは、主に新興企業が費用対効果の面からコワーキングスペースを好んで利用しています。利用者は使用料と賃貸料を支払うだけで、余分なものはなく、従来のオフィスのような面倒な手続きやインフラの維持・修繕費もかからないです。新興企業は当初、限られた資本で機能するため、業務遂行のコストが低いことが有利に働く。定期的に変化する経済環境の中で、厳しい条件の長期リース契約に縛られない企業は、より有利な立場に立つことができます。コワーキングスペースは、利用者のニーズに合ったものを的確に選択するなど、サービスパッケージを組み合わせることができる柔軟な料金体系を提供しています。利用者がプロジェクトチームを減らしたり、逆に増やしたりする必要がある場合、例えば、企業が急成長期に入り、より多くの従業員が必要になった場合、コワーキングスペースを利用すれば、いつでも対応できます。

企業の収益は、コワーキングスペースの需要を促進する重要な要因です。コワーキングスペースは、従来のオフィススペースと比べて12~72%のコスト削減が可能です。従来のオフィススペースにかかるコストはすぐにかさみます。リース料に加え、従来のオフィススペースの価格には、光熱費、インターネット、技術サポートとメンテナンスが含まれています。逆に、コワーキング・メンバーシップには通常、光熱費、インターネット、技術サポート、メンテナンスが含まれています。あらゆる規模の企業が、共有ワークスペースのコスト削減に注目しています。

新興企業やフリーランサーの増加

コワーキングエコシステムは、当初は新興企業やフリーランサーのための選択肢だったが、今では中小企業にとって必須条件となっています。1,200万~1,600万席の潜在的な座席数のうち、1,030万席が大企業に割り当てられています。フリーランサーと中小企業の間には、それぞれ150万人ずつの質の格差があります。

2023年10月3日現在、インドは世界第3位のスタートアップ・エコシステムとしての地位を固めており、全国763地区で112,718以上のスタートアップがDPIITによって認定されています。イノベーションの質に関しては、インドは世界第2位であり、中所得国の中でも特に科学論文の質と大学の質が優れています。インドのイノベーションは特定分野を超えており、新興企業は56の多様な産業領域の課題に取り組んでいます。特筆すべきは、新興企業の13%がITサービス、9%がヘルスケアとライフサイエンス、7%が教育、5%が農業、5%が飲食品です。

最も小規模なのは10万席規模の新興企業です。従来のオフィスからフレキシブルなワークスペースへの大幅なシフトが広く受け入れられるようになるにつれ、コスト効率、柔軟性、技術統合、優れたインフラ、生産性の向上、プラグアンドプレイ・ソリューション、ネットワーキングの機会などを理由に、コワーキングを採用する中小企業が増えています。そのため、中小企業は不動産管理の手間を省き、本来のビジネスに集中することができます。

インドのコワーキングオフィススペース産業概要

インドのコワーキングオフィススペース市場は断片化されており、世界なコワーキング市場プレイヤーとローカルなコワーキング市場プレイヤーが存在します。市場の主要企業には91 Springboard、Awfis、WeWork、Mumbai Coworkingなどがあります。また、カジュアルな環境のオフィスに対する急速な需要を満たすために、さらに多くの企業が参入しています。インドのコワーキングオフィススペース市場の企業は、戦略的提携、合併、買収など、いくつかの成長・拡大戦略に取り組み、競争優位を獲得しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 市場力学

- 市場促進要因

- スタートアップ企業の増加

- 持続可能なコワーキングスペースの開発

- 市場抑制要因

- リモートワークの増加

- インドの伝統的な労働文化とコワーキングスペースのオープンでコラボレーティブな環境との相性の悪さ

- 市場機会

- テクノロジー統合の強化

- 市場促進要因

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者/買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 政府の規制と取り組み

- 産業バリューチェーン分析

- 市場の技術動向

- インドのコワーキング新興企業に関する洞察

- COVID-19パンデミックの市場への影響

第5章 市場セグメンテーション

- タイプ別

- フレキシブルマネージドオフィス

- サービスオフィス

- 用途別

- 情報技術(ITおよびITES)

- リーガルサービス

- BFSI(銀行、金融サービス、保険)

- コンサルティング

- その他サービス

- エンドユーザー別

- 個人ユーザー

- 小規模企業

- 大規模企業

- その他エンドユーザー

- 主要都市別

- デリー

- ムンバイ

- バンガロール

- その他の都市

第6章 競合の情勢

- 市場集中の概要

- 企業プロファイル

- Mumbai Coworking

- We Work-BKC

- Innov8-Vikhroli

- 91 springboard

- Spring House Coworking

- Indi Qube

- Skootr

- Awfis CBD

- Smartworks

- Goodworks

- Cowrks

- Hive

- その他の企業

第7章 市場の将来

第8章 付録

The India Co-working Office Spaces Market size is estimated at USD 2.08 billion in 2025, and is expected to reach USD 2.91 billion by 2030, at a CAGR of 7% during the forecast period (2025-2030).

Key Highlights

- The pandemic accelerated the growth of co-working spaces in the country, as traditional workspaces faced challenges during the crisis. Many enterprises moved toward co-working spaces because of affordable prices and flexibility in working areas. Also, co-working spaces ensure to provide a safe working environment.

- The sector is driven by increasing demand from freelancers, small and medium-scale enterprises (SMEs), and startups. Because the industry provides top facilities at affordable prices, large-scale enterprises are also adopting co-working spaces after realizing the benefits offered by the industry. Also, the increasing number of startups with high investment flow rates has resulted in robust sector growth.

- The previous year has seen a rebound in the co-working space industry, driven by the increased demand for flexible office space. Co-working spaces have grown in popularity among businesses in India, with demand doubling over the past four years. In the first quarter of 2023, co-working spaces accounted for 27% of the net absorption of 8.2 million sq. ft. across the top seven cities, marking a substantial rise from 14% in Q1 2019.

- Bengaluru and the National Capital Region (NCR) together comprised two-thirds of the net absorption of co-working spaces during Q1 2023. Pune and Chennai collectively absorbed about 0.52 million sq. ft. of co-working spaces in the same period. The top seven cities experienced a remarkable 90% growth in net absorption of co-working spaces, escalating from 1.3 million sq. ft. in Q1 2019 to approximately 2.18 million sq. ft. in Q1 2023.

- Bengaluru accounted for the highest share of leasing by Flexi operators, followed by Mumbai and Delhi-NCR. Startups first led the demand for co-working office spaces in India before MNCs and large enterprises took the plunge by taking up space in co-working office spaces.

India Co-working Office Spaces Market Trends

Cost Optimization is Driving the Significant Growth in the Sector

In India, startups mainly prefer co-working spaces for cost-effectiveness. Users only pay for what they use and rent, nothing extra, and there are no hassles or spending on infrastructure maintenance and repair, which conventional offices include. Since startups initially function on limited capital, lower costs of performing work are in their favor. Companies not bound by long-term lease contracts with strict terms in a regularly changing economic environment will be better positioned. Co-working spaces offer flexible tariffs that can combine service packages, such as choosing precisely what suits users' needs. In case users need to reduce or, on the contrary, increase the project team, for example, if companies enter a period of rapid growth and need more employees, using co-working spaces can always do it.

The companies' bottom lines are a crucial factor driving demand for co-working space. Based on locations nationwide, co-working offers a 12-72% cost reduction compared to traditional office space. The cost of traditional office space quickly adds up. In addition to lease payments, prices for conventional office space include utilities, internet, and tech support and maintenance. Conversely, utilities, internet, tech support, and maintenance are typically included in co-working memberships. Businesses of all sizes have caught on to the cost savings of shared workspace.

Increasing Number of Startups and Freelancers in the Country

Co-working ecosystem, initially the go-to option for startups and freelancers, has become a prerequisite for SMEs. The biggest chunk of 10.3 million seats out of the total 12-16 million potential seats is ascribed to large companies. There is a quality divide of 1.5 million each among freelancers and SMEs.

As of October 3, 2023, India cemented its position as the third-largest startup ecosystem globally, boasting over 112,718 startups recognized by DPIIT across 763 districts nationwide. Regarding innovation quality, India ranks second globally, excelling particularly in the quality of scientific publications and the caliber of its universities among middle-income economies. Innovation in India transcends specific sectors, with startups addressing challenges across 56 diverse industrial domains. Notably, 13% of these startups operate in IT services, 9% in healthcare and life sciences, 7% in education, 5% in agriculture, and 5% in food and beverages.

The most minor lot is formed by startups at 100,000 seats. With a substantial shift from traditional offices to flexible workspaces attaining widespread acceptance, more SMEs are embracing coworking due to cost efficiency, flexibility, tech integrations, superior infrastructure, enhanced productivity, plug-and-play solutions, and networking opportunities. Thus, they can concentrate on their fundamental business minus the hassle of managing real estate.

India Co-working Office Spaces Industry Overview

The Indian co-working office space market is fragmented, with global and local co-working market players. Some of the key players in the market are 91 Springboard, Awfis, WeWork, and Mumbai Coworking. Also, many more are entering the need to fulfill the rapid demand for casual environment offices. Companies in the Indian co-working office space market are involved in several growth and expansion strategies, such as strategic partnerships, mergers, and acquisitions, to gain a competitive advantage.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Increase in Number of Startups

- 4.2.1.2 The Development of Sustainable Co-working Spaces

- 4.2.2 Market Restraints

- 4.2.2.1 A Rise in Remote Work

- 4.2.2.2 Traditional Work Culture in India, Which May Not Align Well With the Open and Collaborative Environment of Co-working Spaces

- 4.2.3 Market Opportunities

- 4.2.3.1 Enhanced Technology Integration

- 4.2.1 Market Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers/Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Government Regulations and Initiatives

- 4.5 Industry Value Chain Analysis

- 4.6 Technology Trends in the Market

- 4.7 Insights on Co-working Startups in India

- 4.8 Impact of the COVID - 19 Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Flexible Managed Office

- 5.1.2 Serviced Office

- 5.2 ByApplication

- 5.2.1 Information Technology (IT and ITES)

- 5.2.2 Legal Services

- 5.2.3 BFSI (Banking, Financial Services, and Insurance)

- 5.2.4 Consulting

- 5.2.5 Other Services

- 5.3 By End User

- 5.3.1 Personal User

- 5.3.2 Small Scale Company

- 5.3.3 Large Scale Company

- 5.3.4 Other End Users

- 5.4 By Key Cities

- 5.4.1 Delhi

- 5.4.2 Mumbai

- 5.4.3 Bangalore

- 5.4.4 Other Cities

6 Competitive Land Scape

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Mumbai Coworking

- 6.2.2 We Work-BKC

- 6.2.3 Innov8-Vikhroli

- 6.2.4 91 springboard

- 6.2.5 Spring House Coworking

- 6.2.6 Indi Qube

- 6.2.7 Skootr

- 6.2.8 Awfis CBD

- 6.2.9 Smartworks

- 6.2.10 Goodworks

- 6.2.11 Cowrks

- 6.2.12 Hive*

- 6.3 Other Companies