|

市場調査レポート

商品コード

1644870

英国のコワーキングオフィス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)UK Co-Working Office Spaces - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国のコワーキングオフィス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

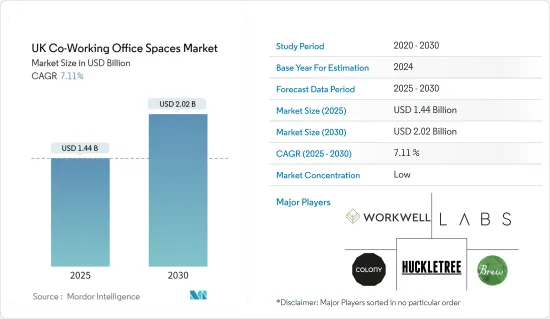

英国のコワーキングスペース市場規模は2025年に14億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは7.11%で、2030年には20億2,000万米ドルに達すると予測されています。

コワーキングスペースは急速にビジネスに最適なものになりつつあります。従来の働き方は、もはや私たちの生活スタイルに合わないです。世界は、柔軟性と成長スペースを提供するコワーキングスペースへと急速に移行しています。

1,000人のビジネスリーダーを対象とした調査によると、在宅勤務によって得られる自由は、働き方を永久に変えることになりそうです。オフィススペースを持つ企業の半数近く(45%)が2025年末までに縮小を計画しており、パンデミックが始まって以来、7社に1社(18%)がすでに縮小しています。この調査によると、今後5年間で約1,800万平方フィートのオフィススペースが老朽化し、現在の占有面積の18%を占めることになります。

また、英国の企業は、より短くフレキシブルなリースを求め、WeWorkのようなコワーキングスペースを活用するようになり、12%が「自社所有」のオフィスよりもこうした場所を頻繁に利用する意向を示しています。オフィスに固執する予定の企業では、13%が一人当たりのデスクスペースが少ない宿泊施設を探すといわれています。

この新しい環境では柔軟性が変化の原動力となり、オフィススペースを可能性のあるスペースへと変貌させます。例えば、ロンドン郊外にある小さなオフィススペースは1人 1日265ユーロ(287.51米ドル)以下でチームを集めています。このようなフレキシブルなスペースは常に進化し続ける現代のワークスペースの性質に対応し、機能的であるだけでなく、現代のプロフェッショナルライフの進化するニーズに応えています。

英国のコワーキングスペース市場動向

コスト上昇と空室率低下の中、賃貸オフィススペースへの需要が急増

フィッティングアウトやファイナンスコストの上昇、開発完了時期の遅れにより、フレキシブルで家主にフィットしたオフィススペースに対する入居者の需要が高まっています。これらのオプションは、こうしたリスクを軽減し、入居者に柔軟性と利便性を提供するのに役立ちます。また、主要な立地ではフレキシブルなオフィススペースが不足していることも、貸主設置型オフィススペースへの需要を後押ししています。稼働率は多くの拠点で満室まで上昇しています。

しかし、5,000~1万平方フィート台のフィットアウト・オフィススペース取引が増加しています。これは特にシティで顕著で、2022年には貸主によるフィッティングアウトの取引件数が倍増しました。

また、2022年のシティにおける1万平方フィート以下のオフィス賃貸取引のうち、貸主によるフィットアウトが占める割合は42%であった(2021年はわずか21%)。家主がソフトサービスを提供するフルマネージドスペースへの関心も高まっています。特に、ソフトサービスがセットになった「包装契約」の台頭により、小規模テナントがフィットネススペースを好む傾向は今後も続くと予想されます。

ロンドンのコワーキングオフィス需要が市場を牽引

現地調査によると、ロンドンはコワーキングオフィスを開設するのに最適な場所と言われています。この調査では、コワーキングの需要と供給、平均月額費用、インターネットスピードなどを考慮し、世界53ヶ所を調査しました。

その結果、ロンドンが他の都市を凌駕し、フレキシブルなオフィススペースで1位を獲得しました。ハイブリッドワークに加え、コワーキングの需要も増加傾向にあります。

Instant Groupは昨年、英国の稼働率が83%に達し、パンデミック(世界的大流行)前以来の高水準になったと報告しました。この動向は2024年も続くと予想され、企業は景気低迷を乗り切り、諸経費を削減するためにサービスオフィスへの移転を検討しています。

ロンドンには世界で最も多くのコワーキングスペースがあり、英国の首都全体で1,400室が利用可能です。世界第2位の都市パリでは1,000以上のコワーキングスペースがあることになります。ロンドンにおけるコワーキングスペースの月間平均検索数は4,400件で、コワーキングスペースに対する需要の高さを示しています。最近の報告によると、フルタイムのオフィスワークスペースを借りる代わりに、費用対効果の高い選択肢としてコワーキングに注目する企業が全米に広がっています。

Google Trendsのデータによると、2023年3月31日現在、コワーキングオフィスを検索する企業数が急増しています。検索数の急増は、2023年4月1日に施行された中小企業料金の引き上げによるものと考えられます。政府は、新料金の導入により、事業所料金を市場規模に合わせるとしています。今月初めのオフィス物件の平均的な値上げ率は約10%でした。

英国のコワーキングスペース産業概要

英国のコワーキングスペース市場は細分化されており、多くの企業が参入しています。開発企業は現在の需要を満たすため、新商品や低コストの商品を提供しようとしています。新しいプロプテックソリューションなど進化する技術的進歩は、取引の増加や不動産サービスのより良い管理という点で市場を牽引しています。英国の大手企業には、Work Well Offices、Labs、The Brew、Huckle Tree、Jactin Houseなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 市場力学

- 促進要因

- コワーキングスペースへのシフトの高まりが市場を牽引

- 持続可能性への関心の高まりが市場を牽引

- 抑制要因

- 経済の不確実性が市場に影響

- 機会

- 共同作業環境に対する需要の高まりが市場を牽引

- 促進要因

- 技術動向

- 産業のバリューチェーン分析

- 政府の規制と取り組み

- 英国のコワーキングスタートアップに関する洞察

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19パンデミックの影響

第5章 市場セグメンテーション

- エンドユーザー別

- 個人ユーザー

- 小規模企業

- 大規模企業

- その他

- 地域別

- ロンドン

- マンチェスター

- バーミンガム

- リーズ

- その他の都市

- タイプ別

- フレキシブルマネージドオフィス

- サービスオフィス

- 用途別

- 情報技術(ITとITES)

- 法律サービス

- BFSI(銀行、金融サービス、保険)

- コンサルティング

- その他

第6章 競合情勢

- 市場集中度概要

- 企業プロファイル

- Work Well Offices

- Labs

- The Brew

- Huckle Tree

- Jactin House

- The Skiff

- Icon Offices

- Wimbletech CIC

- Regus

- Creative Works

- The Office Group

- Foyles

- Soho Works

- The Hoxton

- Mare Street Market

- Southbank Centre*

- その他の企業

第7章 市場の将来

第8章 付録

The UK Co-Working Office Spaces Market size is estimated at USD 1.44 billion in 2025, and is expected to reach USD 2.02 billion by 2030, at a CAGR of 7.11% during the forecast period (2025-2030).

Co-working spaces are fast becoming the perfect fit for businesses. Traditional ways of working do not fit the way we live anymore. The world is rapidly moving towards co-working spaces that offer flexibility and space to grow.

The freedom afforded by working from home, according to the research of 1,000 business leaders, is set to alter the way they work permanently. Nearly half of the enterprises with office space (45%) plan to downsize by the end of 2025, and one in seven (18%) have already done so since the pandemic began. According to the study, about 18 million sq. ft of office space will become obsolete in the next five years, accounting for 18% of all currently occupied square footage, significantly impacting how cities in the United Kingdom appear and feel.

Businesses in the United Kingdom will also be looking for shorter, flexible leases and utilizing co-working spaces such as WeWork, with 12% intending to use these locations more often than an 'owned' office. For those businesses planning to stick to the office, 13% will look for accommodation with less desk space per head as the office's main function is set to shift with more space for collaboration, such as break-out areas and meeting rooms.

In this new landscape, flexibility is the driving force for change, transforming office spaces into spaces of possibility. For example, small office spaces outside of London are attracting teams for under EUR 265 (USD 287.51) per person per day. These are flexible spaces that respond to the ever-evolving nature of modern workspaces that not only function but also respond to the evolving needs of contemporary professional life.

UK Co-Working Office Space Market Trends

The Demand for Landlord-Fitted Office Space Surges Amid Rising Costs and Shrinking Availability

Occupants' demand for flexible and landlord-fitted office space is on the rise due to increasing fit-out and finance costs, as well as delayed development completion dates. These options help to mitigate these risks and offer flexibility and convenience for occupiers. The prime flexible office space shortage in key locations also drives demand for landlord-fitted office space. Occupancy rates are increasing to full capacity in many centers.

Fitted space has traditionally been more attractive to smaller tenants, with most transactions being under 5,000 sq. ft. However, there is an increasing number of fit-out office space deals in the 5,000-10,000 sq. ft range. This is especially true in the City, where the number of landlord-fitted transactions doubled in 2022.

Landlord-fitted office space also made up 42% of the total City of London office leasing transactions under 10,000 sq. ft in 2022, compared to just 21% in 2021. There is also a growing interest in fully managed space, where landlords offer soft services. A preference for fitted space among smaller tenants is anticipated to persist, particularly with the rise of 'package deals' where soft services are included as an offer.

The Demand for Co-working Office Space in London is Driving the Market

According to a local survey, London is said to be the best place to open a coworking office. The study looked at 53 locations around the world, taking into account the supply and demand of coworking, average monthly costs, and internet speeds.

The results showed that London outperformed all other cities, taking the number one spot for flexible office spaces. In addition to hybrid working, demand for coworking has been on the rise.

The Instant Group reported last year that occupancy rates in the United Kingdom stood at 83%, the highest level since before the pandemic. This trend is expected to continue in 2024 as companies look to move to serviced offices to weather the economic downturn and reduce overhead costs.

London has the most coworking spaces in the world, with 1,400 available across the UK capital. That's more than 1,000 coworking spaces in Paris, the second-largest city in the world. The average monthly search for coworking spaces in London was 4,400, demonstrating the high demand for coworking spaces. According to recent reports, organizations across the country are turning to coworking as a cost-effective alternative to renting full-time office workspace.

According to Google Trends data, the number of companies searching for coworking offices soared as of March 31, 2023. The spike in searches is likely due to the increase in small business rates, which entered into force on April 1, 2023. The government has said that the new rates will align business premises fees with their market value. Office properties had an average increase in rateable values of around 10% at the start of this month.

UK Co-Working Office Space Industry Overview

The UK co-working spaces market is fragmented, with many companies in the industry. Developers are trying to bring new and lower-cost products to meet the current demand. Evolving technological advancements such as new proptech solutions drive the market in terms of increased transactions and better management of real estate services. Some of the major players in the United Kingdom are Work Well Offices, Labs, The Brew, Huckle Tree, and Jactin House.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increasing Shift Toward Co-working Spaces is Driving the Market

- 4.2.1.2 Increasing Focus on Sustainability is Driving the Market

- 4.2.2 Restraints

- 4.2.2.1 Economic Uncertainty is Affecting the Market

- 4.2.3 Opportunities

- 4.2.3.1 Increasing Demand for Collaborative Work Environments is Driving the Market

- 4.2.1 Drivers

- 4.3 Technological Trends

- 4.4 Industry Value Chain Analysis

- 4.5 Government Regulations and Initiatives

- 4.6 Insights on Co-working Startups in the United Kingdom

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of the COVID-19 Pandemic

5 MARKET SEGMENTATION

- 5.1 By End User

- 5.1.1 Personal User

- 5.1.2 Small Scale Company

- 5.1.3 Large Scale Company

- 5.1.4 Other End Users

- 5.2 By Geography

- 5.2.1 London

- 5.2.2 Manchester

- 5.2.3 Birmingham

- 5.2.4 Leeds

- 5.2.5 Other UK Cities

- 5.3 By Type

- 5.3.1 Flexible Managed Office

- 5.3.2 Serviced Office

- 5.4 By Application

- 5.4.1 Information Technology (IT and ITES)

- 5.4.2 Legal Services

- 5.4.3 BFSI (Banking, Financial Services, and Insurance)

- 5.4.4 Consulting

- 5.4.5 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Work Well Offices

- 6.2.2 Labs

- 6.2.3 The Brew

- 6.2.4 Huckle Tree

- 6.2.5 Jactin House

- 6.2.6 The Skiff

- 6.2.7 Icon Offices

- 6.2.8 Wimbletech CIC

- 6.2.9 Regus

- 6.2.10 Creative Works

- 6.2.11 The Office Group

- 6.2.12 Foyles

- 6.2.13 Soho Works

- 6.2.14 The Hoxton

- 6.2.15 Mare Street Market

- 6.2.16 Southbank Centre*

- 6.3 Other Companies