|

市場調査レポート

商品コード

1631584

欧州のコワーキングスペース-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Coworking Spaces - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のコワーキングスペース-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

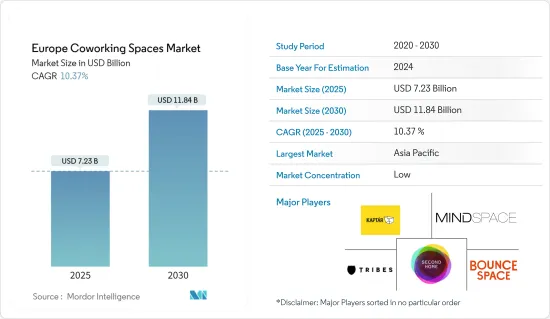

欧州のコワーキングスペース市場規模は2025年に72億3,000万米ドルと予測され、予測期間(2025~2030年)のCAGRは10.37%で、2030年には118億4,000万米ドルに達すると予測されます。

主要ハイライト

- Workthereによると、2023年の欧州のコワーキングスペース市場は予想を覆しました。軟質オフィスのスペシャリストであるWorkthereは、2024年においてもオペレーターは設備と持続可能性を重視した最高級のスペースを探し続けると推定しています。

- 人材の誘致と確保が過去最高水準にある中、最高級のスペースに対する需要は引き続きあり、オペレーターはより多くのアメニティを提供することでゲームをステップアップする必要があります。テナントを獲得し、新たなテナントを誘致するために、事業者はすでにジム、ヨガ、カフェ、屋外スペースにとどまらず、プライベートシェフ付きの5つ星ホテルや屋上バーのようなアメニティを含む基準を設定しています。

- 入居者は最高の立地を求める一方で、交通の便が良く、従業員のためのアメニティが充実した場所を求めています。多くの市場では、これが中心業務地区(CBD)で営業するフレックスオフィス事業者の増加につながっており、これは2024年も続くと予想されています。一方、欧州、特にマドリード、ミュンヘン、バルセロナなどの主要都市では、空室率が5%を大きく下回るなどオフィススペースが不足しており、稼働率と空室率に大きな影響を与えると考えられます。

- 過去2年間で運営コストが上昇し、多くの運営会社の利益率に影響を与えており、欧州のほとんどの都市でデスク価格はハイエンドでは上昇したもの、ローエンドではより厳しい状況となっています。オペレーターは2024年には、会議室やイベントの売上増、コワーキングデスクの売上増、顧客への技術包装のアップセルなど、デスク料金以外のマージンを伸ばす機会を探したり、付帯収益に目を向けたりすることで、収益性を本格的に重視するようになると予測されています。

欧州のコワーキングスペース市場動向

軟質で手頃なオフィススペースを求める欧州の新興企業や中小企業の増加が市場成長を牽引

軟質オフィスやコワーキングスペースは、オフィススペースの賃貸、リース、購入にかかる費用を大幅に節約できるため、新興企業にとって重宝されます。ニーズや予算、時間に合わせてオフィススペースを利用できます。

コワーキングが普及するにつれ、コワーキングが必要不可欠なネットワーキングにも役立つと語る起業家も増えています。コワーキングはリースに関しても柔軟性があり、いくつかの異なるオプションから選ぶことができます。また、世界中どこからでも仕事ができ、プレミアムでアクセスしやすい場所で仕事ができるという利点もあります。

2022年12月、英国には700以上のeコマース・スタートアップが登録しており、欧州最大のeコマース・スタートアップ・エコシステムとなっています。これに対してフランスは、登録されたeコマース新興企業が270社で、250社に満たなかったドイツに次いで2番目でした。そのわずか1年前、ドイツは欧州全体で2番目に大きなeコマースと小売の新興企業エコシステムを持っていました。

ドイツでは、eコマース産業は、2022年にスタートアップ投資が最も多い産業の中で、健康、エネルギー、ソフトウェア、分析などの産業に次いで6位にランクされています。しかし、2022年5月までに、ドイツには、全体的な資金調達の面で欧州のeコマースB2Bスタートアップの上位4社の本拠地があった。

リモートワークの台頭と柔軟な働き方への需要の高まりが市場を牽引

コワーキングスペースはビジネスにとって最適な場所になりつつあります。世界は成長するための柔軟性とスペースを提供するコワーキングスペースへと急速に移行しています。

1,000人のビジネスリーダーを対象とした調査によると、在宅勤務によってもたらされる自由は、人々の働き方を永久に変えようとしています。ある調査によると、オフィススペースを持つ企業の半数近く(45%)が2025年末までに縮小を計画しており、COVID-19の大流行が始まって以来、7社に1社(18%)がすでに縮小しているといいます。この調査によると、今後5年間で約1,800万平方フィートのオフィススペースが老朽化し、現在の占有面積の18%を占めるといいます。これは、英国の都市の姿や印象に大きな影響を与えると予想されます。

英国企業はまた、より短く軟質なリースを求めており、WeWorkのようなコワーキングスペースの採用を増やしています。オフィスに固執する予定の企業のうち、13%はオフィスの主要機能がブレイクアウトエリアやミーティングルームなどのコラボレーション用のスペースにシフトしているため、1人あたりのデスクスペースが少ない宿泊施設を探すと回答しています。

この新しい環境では柔軟性が変化の原動力となり、オフィススペースを可能性のあるスペースへと変貌させる。例えば、ロンドン郊外にある小さなオフィススペースは1人1日265ユーロ(287.51米ドル)以下でチームを集めています。このような軟質なスペースは機能的であるだけでなく、現代のプロフェッショナルな生活の進化するニーズに応え、進化し続ける現代のワークスペースの本質に対応しています。

欧州のコワーキングスペース産業概要

この産業はかなり細分化されており、欧州のコワーキングスペース市場には多くの参入企業が進出しています。また、カジュアルな環境のオフィスに対する急速な需要に応えるため、さらに多くの企業が市場に参入しています。市場の主要企業にはKAPTAR、Mindspace、BounceSpace、Second Home、Tribesなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 柔軟で手頃なオフィススペースを求める欧州の新興企業や中小企業の増加

- リモートワークの増加と柔軟な勤務形態への需要の高まり

- 市場抑制要因

- 経済的な不確実性が市場の進展に影響

- 従来のオフィススペース提供企業との競合

- 市場機会

- 従来のオフィススペース・プロバイダーとの提携

- コミュニティ形成の重視

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- ビジネスタイプ別

- 新規スペース

- 拡大

- チェーン

- ビジネスモデル別

- サブリースモデル

- レベニューシェアモデル

- オーナー・オペレーターモデル

- エンドユーザー別

- 独立プロフェッショナル

- スタートアップ・チーム

- 中小企業(SME)

- 大企業

- 国別

- 英国

- フランス

- ドイツ

- スペイン

- イタリア

- その他の欧州

第6章 競合情勢

- 市場集中度概要

- 企業プロファイル

- KAPT-R

- Mindspace

- BounceSpace

- Second Home

- Tribes

- Mokrin House

- Paper Hub

- Impact Hub

- WeWork

- Mortimer House*

- その他の企業

第7章 投資分析

第8章 市場の将来

第9章 付録

The Europe Coworking Spaces Market size is estimated at USD 7.23 billion in 2025, and is expected to reach USD 11.84 billion by 2030, at a CAGR of 10.37% during the forecast period (2025-2030).

Key Highlights

- The coworking spaces market in Europe defied the odds in 2023, according to Workthere. The flexible office specialist estimated that operators would continue to look for top-of-the-line spaces with more emphasis on facilities and sustainability in 2024.

- With talent attraction and retention at all-time highs, there will continue to be a demand for top-of-the-line space, and operators will need to step up their game by offering more amenities. To compete for tenants and attract new ones, operators are already setting standards that go beyond gyms, yoga, cafes, and outdoor space to include amenities like five-star hotels with private chefs or rooftop bars.

- While occupiers are looking for the best locations, they are also looking for locations that offer the best transport connections and full amenities for their employees. For many markets, this has led to an increase in the number of flex office operators operating in central business districts (CBDs), which is expected to continue in 2024. On the other hand, a shortage of office space in Europe, particularly in major cities such as Madrid, Munich, and Barcelona, where vacancy rates are well below 5%, will have a major impact on occupancies and availability.

- Operational costs have increased over the last two years, impacting profit margins for a number of operators, and while the desk prices increased at the high end in most European cities, it has been more difficult at the low end. Operators are projected to place a genuine emphasis on profitability in 2024 by looking for opportunities to grow margin outside of desk rates and by looking at ancillary revenue, including through more sales of meeting rooms and events, more sales of coworking desks, or upselling technology packages to their customers.

Europe Coworking Spaces Market Trends

Market Growth Driven by the Increasing Number of Startups and Small Businesses in Europe Looking for Flexible and Affordable Office Spaces

Flexible offices and coworking spaces come in handy for startups because they can save a lot of money on renting, leasing, or buying office space. They can avail of office space according to their needs, budget, and time.

As coworking becomes more popular, more entrepreneurs are talking about how coworking also helps with essential networking. Coworking offers a lot of flexibility when it comes to leasing, and there are several different options to choose from. It also offers the advantage of being able to work from anywhere in the world, as well as being able to work in premium and easy-to-access locations.

In December 2022, the United Kingdom had more than 700 e-commerce startups registered, making it the largest e-commerce startup ecosystem across Europe. In comparison, France had 270 e-commerce startup companies registered, second only to Germany, which had less than 250 startups registered. Just one year earlier, Germany had the second-largest e-commerce and retail startup ecosystem across Europe.

In Germany, the e-commerce industry ranked sixth among industries with the highest number of startup investments in 2022, after industries including health, energy, software, and analytics. However, by May 2022, Germany was home to four of the top European e-commerce B2B startups in terms of overall funding.

Rise of Remote Work and Growing Demand for More Flexible Work Arrangements are Driving the Market

Coworking spaces are fast becoming the perfect fit for businesses. The world is rapidly moving toward coworking spaces that offer the flexibility and space to grow.

The freedom afforded by working from home, according to the research of 1,000 business leaders, is set to permanently alter the way people work. A study found that nearly half of the enterprises with office space (45%) plan to downsize by the end of 2025, and one in seven (18%) have already done so since the COVID-19 pandemic began. According to the study, about 18 million sq. ft of office space will become obsolete in the next five years, accounting for 18% of all currently occupied square footage. This is expected to have a significant impact on the way UK cities appear and feel.

UK businesses are also looking for shorter, flexible leases, which is increasing their adoption of coworking spaces such as WeWork, with 12% intending to use these locations more often instead of an 'owned' office. Among businesses planning to stick to the office, 13% stated they would look for accommodation with less desk space per head as the office's main function would now shift toward more space for collaboration, such as break-out areas and meeting rooms.

In this new landscape, flexibility is the driving force for change, transforming office spaces into spaces of possibility. For example, small office spaces outside of London are attracting teams for under EUR 265 (USD 287.51) per person per day. These flexible spaces respond to the ever-evolving nature of modern workspaces that not only function but also respond to the evolving needs of contemporary professional life.

Europe Coworking Spaces Industry Overview

The industry is quite fragmented, with many players operating in the European coworking spaces market. Many more are also entering the market to cater to the rapid demand for offices with casual environments. Some major players in the market include KAPTAR, Mindspace, BounceSpace, Second Home, and Tribes.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Number of Startups and Small Businesses in Europe Looking for Flexible and Affordable Office Space

- 4.2.2 Rise of Remote Work and Growing Demand for More Flexible Work Arrangements

- 4.3 Market Restraints

- 4.3.1 Economic Uncertainties Affecting the Progress

- 4.3.2 Competition from Traditional Office Space Providers

- 4.4 Market Opportunities

- 4.4.1 Partnerships with Traditional Office Space Providers

- 4.4.2 Emphasis on Community Building

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Business Type

- 5.1.1 New Spaces

- 5.1.2 Expansions

- 5.1.3 Chains

- 5.2 By Business Model

- 5.2.1 Sub-lease Model

- 5.2.2 Revenue Sharing Model

- 5.2.3 Owner-operator Model

- 5.3 By End User

- 5.3.1 Independent Professionals

- 5.3.2 Startup Teams

- 5.3.3 Small to Medium-sized Enterprises (SMEs)

- 5.3.4 Large-scale Corporations

- 5.4 By Country

- 5.4.1 United Kingdom

- 5.4.2 France

- 5.4.3 Germany

- 5.4.4 Spain

- 5.4.5 Italy

- 5.4.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 KAPT-R

- 6.2.2 Mindspace

- 6.2.3 BounceSpace

- 6.2.4 Second Home

- 6.2.5 Tribes

- 6.2.6 Mokrin House

- 6.2.7 Paper Hub

- 6.2.8 Impact Hub

- 6.2.9 WeWork

- 6.2.10 Mortimer House*

- 6.3 Other Companies