アジア太平洋地域のコワーキングオフィススペース:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Asia Pacific Co-Working Office Spaces - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644506

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

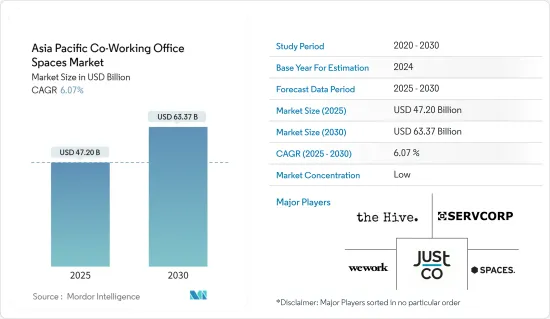

アジア太平洋のコワーキングオフィススペース市場規模は2025年に472億米ドルと推定され、予測期間(2025-2030年)のCAGRは6.07%で、2030年には633億7,000万米ドルに達すると予測されます。

主なハイライト

- コスト削減と柔軟性の向上を背景に、コワーキング・コンセプトを採用する企業が増えています。予測によると、2024年末までに世界のコワーキングスペース数は約41,975に達します。

- フリーランサー、中小企業(SME)、新興新興企業がコワーキングスペースセクターの主な牽引役となっています。大企業でさえも、競争力のある価格でのプレミアムな設備に魅力を感じ、コワーキングスペースを利用するようになってきています。この分野の急成長は、資金力のある新興企業の急増に起因しています。さらに、中国やインドなどではデジタルノマドの人口が増加しており、コワーキングスペースの拡大をさらに後押ししています。

- 業界団体の報告によると、2025年までにアジア太平洋地域は386万台のフレキシブルワークスペースデスクを誇ると予測されています。メルボルン、シンガポール、香港、ムンバイのような主要都市が最前線で、フレキシブルオフィスやコワーキングオフィスセンターの著しい成長を目の当たりにしています。

アジア太平洋地域のコワーキングオフィススペース市場動向

フレキシブルなマネージドオフィスが市場成長を促進

同地域で適応性の高いワークスペースに対する需要が急増する中、フレキシブル・マネージド・オフィスは、俊敏性とコスト効率を優先する企業にとって最適なソリューションになりつつあります。この分野の台頭が市場拡大の主要因となっています。フレキシブルな働き方は、従業員に場所や時間、働き方の選択肢を与えます。多様なタイプのワークスペースを提供することで、企業はチームの職場環境をより自由にコントロールできるようになります。

2024年の業界団体の調査によると、地域企業の60%以上がオフィスへの出勤を安定させており、フレキシブルでハイブリッドなモデルが将来の標準として広く受け入れられていることを示しています。興味深いことに、32%の企業がオフィス利用の増加を予測している一方で、減少を予測している企業はわずか4%に過ぎないです。さらにこの調査では、アジア太平洋企業の43%が80%以上という驚異的な利用率を達成しています。このような動向は、企業がワークスタイルの変化に合わせてワークプレイスを再編成し、優秀な人材へのアピールを強化するチャンスとなります。

主要都市では、新興企業も既存企業もプロジェクトベースのチームによりよく対応し、コラボレーションを促進するために、フレキシブルなマネージドオフィスに引き寄せられ、急増しています。例えば、ベンガルールはアジア太平洋地域のフレキシブル・オフィス・スペースの分野で、上海、ソウル、東京などの有名都市を抜いてトップに立っていることが、2024年8月にZoltan Properties(不動産サービス会社)によって明らかにされました。ベンガルールは、2024年半ばまでに1,550万平方フィートのフレキシブルオフィススペースを確保し、順応性の高い職場環境を求める企業にとって最適な都市としての地位を確固たるものにします。

結論として、フレキシブルな管理オフィスへの嗜好の高まりが、市場の展望を再構築しています。企業は、進化する従業員のニーズに応え、ダイナミックなビジネス環境で競合を勝ち抜くために、適応性の高いワークスペースを採用する傾向が強まっています。

この分野で著しい成長を遂げる中国と日本

中国と日本では、新興企業の急増と従業員や企業の柔軟性に対する需要の高まりにより、コワーキングスペースの数が急速に増加しています。コワーキングスペースは、従来のオフィスに代わる費用対効果の高い選択肢を提供しています。注目すべきは、これまで国内外の投資家が支配してきた香港のフレキシブル・ワーキング市場への参入を狙う中国本土の大家が多いことです。この動きは、広大なオフィス市場への低リスクの入り口と考えられています。

日本では、コワーキングスペースがフリーランサーやスタートアップ企業、中小企業にますます支持されています。これらのスペースは、高速インターネット、24時間アクセス、会議室、家具付きと家具なしのオプションなど、プレミアムな機能を誇っています。2024年10月にデジタル・ノマド・アジアが取り上げたように、2024年現在、S-Tokyo(日本橋)は、多様なニーズに合わせた特徴的なアメニティを提供するフロントランナーとして台頭しています。

2024年第1四半期、香港のセントラル地区のグレードAオフィススペースの平均月額賃料は122.59米ドル/㎡を記録し、香港で最も割高なオフィス不動産となった。アジア太平洋の他の主要都市と比較した場合、香港のグレードAのオフィス賃料はトップとなった。このプレミアムは、特にインターネット、デジタルサービス、メディアなど、参入障壁が著しく低い分野で、若く急成長中の企業の間でコワーキングスペースが人気を博していることが主な原因です。

コワーキングオフィススペースはここ数年で急成長を遂げ、個人事業主、新興企業、中小企業の多くがこれらの施設を最大限に活用しています。結論として、中国と日本のコワーキングスペース・セクターは、現代企業の進化するニーズと柔軟な職場環境に対する需要の高まりによって、継続的な成長を遂げる態勢が整っています。この動向は、この地域の伝統的なオフィス市場情勢を再構築する可能性が高いです。

アジア太平洋地域のコワーキングオフィススペース産業の概要

アジア太平洋地域のコワーキングオフィススペース市場は、世界企業とローカル企業が混在しているのが特徴です。カジュアルなオフィス環境に対する需要の高まりに対応し、数多くの新規参入企業が頭角を現しています。競争力を確保するため、各社は提携、合併、買収などの成長戦略を積極的に推進しています。この分野の注目すべきプレーヤーには、JustCo、WeWork Management LLC、Spaces、Hive Worldwide Ltd.などがいます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 技術動向

- 業界のバリューチェーン分析

- 政府の規制と取り組み

- アジア太平洋地域のコワーキング新興企業に関する洞察

- 市場力学

- 市場促進要因

- 新興企業と中小企業の増加

- ワークプレイスダイナミクスの変化

- 市場抑制要因

- 経済の不確実性

- 高い不動産コスト

- 市場機会

- テクノロジーの統合

- 持続可能性とウェルネス

- 市場促進要因

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 地政学とパンデミックが市場に与える影響

第5章 市場セグメンテーション

- エンドユーザー別

- 情報技術(ITおよびITES)

- BFSI(銀行、金融サービス、保険)

- ビジネスコンサルティング&プロフェッショナルサービス

- その他サービス(小売、ライフサイエンス、エネルギー、法律サービス)

- ユーザー別

- フリーランサー

- 企業

- スタートアップ

- その他

- 地域別

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

第6章 競合情勢

- 現在の市場集中度

- 企業プロファイル

- the Hive Worldwide Ltd.

- WeWork Management LLC

- Spaces

- JustCo

- Servcorp

- Compass Offices

- The Work Project Management Pte Ltd.

- GARAGE SOCIETY

- THE GREAT ROOM

- IWG

- WOTSO Limited

- The Executive Centre

第7章 市場の将来

第8章 付録

- マクロ経済指標(GDP分布、活動別)

- 経済統計-運輸・倉庫業の経済への貢献

- 対外貿易統計-品目別、仕向地・原産地別輸出入額

目次

The Asia Pacific Co-Working Office Spaces Market size is estimated at USD 47.20 billion in 2025, and is expected to reach USD 63.37 billion by 2030, at a CAGR of 6.07% during the forecast period (2025-2030).

Key Highlights

- Corporate companies are increasingly embracing the coworking concept, driven by reduced costs and enhanced flexibility. Projections indicate that by the end of 2024, the global tally of coworking spaces will reach approximately 41,975.

- Freelancers, small and medium-sized enterprises (SMEs), and emerging startups are the primary drivers of the co-working space sector. Even large corporations are increasingly turning to co-working spaces, attracted by their premium facilities at competitive prices. The rapid growth of the sector can be attributed to a surge in well-funded startups. Additionally, the rising population of digital nomads in nations such as China and India further propels the expansion of co-working spaces.

- The Asia-Pacific region, demonstrating a strong interest in flexible office spaces, is home to nearly one-third of all co-working spaces globally.As reported by Industry Associations, projections indicate that by 2025, the Asia-Pacific region will boast 3.86 million flexible workspace desks. Major cities like Melbourne, Singapore, Hong Kong, and Mumbai are at the forefront, witnessing significant growth in flexible and co-working office centers.

APAC Co-Working Office Spaces Market Trends

Flexible Managed Offices Propel Market Growth

As demand for adaptable workspaces surges in the region, flexible managed offices are becoming the go-to solution for businesses prioritizing agility and cost-effectiveness. This sector's rise is a key driver of the market's expansion. Flexible work empowers employees with choices about where, when, and how they operate. By offering diverse workspace types, companies grant their teams enhanced control over their work environments.

In 2024 Industry Association survey indicates that over 60% of regional companies have stabilized their office attendance, signaling a broad acceptance of flexible and hybrid models as the future norm. Interestingly, while 32% of firms foresee an uptick in office usage, a mere 4% predict a decline. Furthermore, the survey notes that 43% of Asia Pacific firms have hit an impressive utilization rate of 80% or more. Such trends offer companies a chance to realign their workplaces with shifting work styles, enhancing their appeal to top talent.

Major cities are witnessing a surge, with both startups and established firms gravitating towards flexible managed offices to better accommodate project-based teams and promote collaboration. For example, Bengaluru has taken the lead in the Asia Pacific's flexible office space arena, surpassing renowned cities like Shanghai, Seoul, and Tokyo, as highlighted by Zoltan Properties (a real estate service company) in August 2024. With a commanding 15.5 million square feet of flexible office space by mid-2024, Bengaluru cements its status as the go-to city for businesses in search of adaptable work environments.

In conclusion, the growing preference for flexible managed offices is reshaping the market landscape. Companies are increasingly adopting these adaptable workspaces to meet evolving employee needs and stay competitive in a dynamic business environment.

China and Japan Witnessing Significant Growth in the Sector

China and Japan are witnessing a swift rise in the number of co-working spaces, driven by the surge of start-ups and a growing demand for flexibility among employees and companies. Co-working spaces offer a cost-effective alternative to traditional offices. Notably, many landlords from mainland China are eyeing entry into Hong Kong's flexible working market, a domain historically ruled by local and international investors. This move is seen as a low-risk gateway to the expansive office market.

In Japan, co-working spaces are increasingly favored by freelancers, start-ups, and small to medium-sized enterprises (SMEs). These spaces boast premium features, including high-speed internet, round-the-clock access, meeting rooms, and both furnished and unfurnished options. As of 2024, S-Tokyo (Nihobashi) has emerged as a frontrunner, offering distinctive amenities tailored to diverse needs, as highlighted by Digital Nomad Asia in October 2024.

In Q1 2024, Hong Kong's Central district recorded an average monthly rent of USD 122.59 per square meter for grade A office spaces, making it the priciest office real estate in the city. When stacked against other major cities in the Asia-Pacific, Hong Kong's grade A office rents topped the charts. This premium is largely attributed to the popularity of co-working spaces among youthful, burgeoning businesses, especially in sectors like internet, digital services, and media, where entry barriers are notably low.

Co-working office spaces have seen a meteoric rise over the years, with a significant chunk of independent contractors, nascent businesses, and SMEs making the most of these facilities. In conclusion, the co-working space sector in China and Japan is poised for continued growth, driven by the evolving needs of modern businesses and the increasing demand for flexible working environments. This trend is likely to reshape the traditional office market landscape in the region.

APAC Co-Working Office Spaces Industry Overview

The Asia-Pacific co-working office space market features a mix of global and local players. Responding to the surging demand for casual office environments, numerous newcomers are making their mark. To secure a competitive edge, companies are actively pursuing growth strategies, including partnerships, mergers, and acquisitions. Notable players in this arena encompass JustCo, WeWork Management LLC, Spaces, and Hive Worldwide Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Industry Value Chain Analysis

- 4.4 Government Regulations and Initiatives

- 4.5 Insights on Co-working Start-ups in Asia-Pacific

- 4.6 Market Dynamics

- 4.6.1 Market Drivers

- 4.6.1.1 Grwoth of Startups and SMEs

- 4.6.1.2 Changing Workplace Dynamics

- 4.6.2 Market Restraints

- 4.6.2.1 Economic Uncertainty

- 4.6.2.2 High Real Estate Costs

- 4.6.3 Market Opportunities

- 4.6.3.1 Technology Integration

- 4.6.3.2 Sustainability and Wellness

- 4.6.1 Market Drivers

- 4.7 Industry Attractiveness- Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Geopolitics and Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By End User

- 5.1.1 Information Technology (IT and ITES)

- 5.1.2 BFSI (Banking, Financial Services, and Insurance)

- 5.1.3 Business Consulting & Professional Services

- 5.1.4 Other Services (Retail, Lifesciences, Energy, Legal Services)

- 5.2 By User

- 5.2.1 Freelancers

- 5.2.2 Enterprises

- 5.2.3 Start Ups

- 5.2.4 Others

- 5.3 By Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Australia

- 5.3.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Current Market Concentration

- 6.2 Company Profiles

- 6.2.1 the Hive Worldwide Ltd.

- 6.2.2 WeWork Management LLC

- 6.2.3 Spaces

- 6.2.4 JustCo

- 6.2.5 Servcorp

- 6.2.6 Compass Offices

- 6.2.7 The Work Project Management Pte Ltd.

- 6.2.8 GARAGE SOCIETY

- 6.2.9 THE GREAT ROOM

- 6.2.10 IWG

- 6.2.11 WOTSO Limited

- 6.2.12 The Executive Centre*

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, by Activity)

- 8.2 Economic Statistics - Transport and Storage Sector Contribution to Economy

- 8.3 External Trade Statistics - Exports and Imports by Product and by Country of Destination/Origin

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日