ラテンアメリカの二次電池:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Latin America Rechargeable Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636566

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

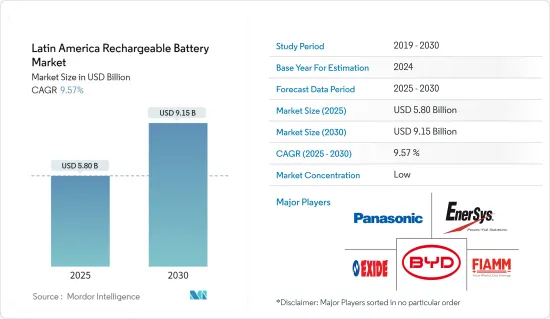

ラテンアメリカの二次電池市場規模は2025年に58億米ドルと推定され、予測期間(2025~2030年)のCAGRは9.57%で、2030年には91億5,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、リチウムイオン電池価格の下落、電気自動車の普及拡大、再生可能エネルギーの採用拡大が、予測期間中のラテンアメリカの二次電池市場を牽引すると予想されます。

- 逆に、原料の需要と供給のミスマッチは、予測期間中の市場成長を阻害する構えです。

- しかし、データセンターのような商業インフラからの需要の増加と、電池のリサイクルや電池のセカンドライフ用途のニーズの高まりが、ラテンアメリカの二次電池市場に大きな機会をもたらすと考えられます。

- ブラジルは、電気自動車の販売台数の急増と再生可能エネルギーの普及により、二次電池市場の大幅な成長が見込まれています。

ラテンアメリカの二次電池市場動向

リチウムイオン電池が大きく成長

- 予測期間中、リチウムイオン電池(LIB)は、ラテンアメリカの二次電池市場で最も急成長しているセグメントのひとつとなる見込みです。リチウムイオン電池は容量対重量比が良好なため、他のタイプに比べて人気が高まっています。リチウムイオン電池の普及を促進するその他の要因としては、優れた性能(長寿命と低メンテナンスが特徴)、長期の保存可能期間、価格の下落動向などが挙げられます。

- 明確な技術的利点を提供するリチウムイオン(Li-ion)電池は、従来の鉛蓄電池よりも優れています。例えば、鉛蓄電池の寿命は通常約400~500サイクルですが、充電式リチウムイオン電池は平均5,000サイクル以上という驚異的な寿命を誇ります。さらに、リチウムイオン電池はメンテナンスや交換の頻度が少ないです。また、放電サイクルを通じて安定した電圧を維持するため、接続された電気部品の効率が長持ちします。

- 近年、産業の大手企業は投資を拡大し、スケールメリットと研究開発に重点を置いて電池の性能を高めています。このような競合の急増により、リチウムイオン電池の価格は著しく低下しています。技術の進歩、製造の最適化、原料コストの低下により、リチウムイオン電池の体積加重平均価格は2013年の780米ドル/kWhから2023年には139米ドル/kWhに急落しました。予測では、2025年には約113米ドル/kWh、2030年には80米ドル/kWhまでさらに低下するとみられ、リチウムイオン電池はますます魅力的な選択肢となっています。

- 歴史的に、リチウムイオン電池は携帯電話やノートパソコンなどの民生用電子機器が主要用途でした。しかし、電気自動車や再生可能エネルギーセグメントの電池エネルギー貯蔵システム(BESS)がリチウムイオン電池への依存度を高めており、その役割は拡大しています。

- ラテンアメリカリチウムイオン電池製造産業はまだ初期段階にあるが、この地域には必須原料が豊富に埋蔵されており、多様なエンドユーザーからの需要が急増していることから、市場の急成長が見込まれています。

- リチウム・トライアングルと呼ばれるラテンアメリカは、リチウムイオン電池に不可欠な膨大なリチウム埋蔵量を誇る。この三角地帯にはアルゼンチン、ボリビア、チリが含まれ、合わせて世界のリチウム埋蔵量の半分以上を保有しています。チリは、アタカマ砂漠にリチウムを豊富に含む鹹水(かんすい)鉱床が広く存在するため、リチウム生産でリードしています。ボリビアのウユニ塩湖は、採掘の課題にもかかわらず、世界最大級のリチウム埋蔵量として際立っています。プナ地域の塩田を有するアルゼンチンも重要な役割を果たしています。これらの国々が一体となって、世界のリチウムイオン電池生産のサプライチェーンに不可欠な存在となっています。

- 米国地質調査所によると、2023年半ばのリチウム生産量は、チリが約4万4,000トン、アルゼンチンが9,600トン、ブラジルが4,900トンとなっています。このような大幅な生産量により、ラテンアメリカは世界のリチウムイオン電池において極めて重要な位置を占めています。

- ラテンアメリカ諸国は、電気自動車のサプライチェーンへの関与を深める努力を強めています。アルゼンチン、チリ、ボリビア、ブラジルのような国々は、豊富な鉱物資源を活用し、加工能力を高め、自動車製造を視野に入れることで、採掘されたリチウムの多くを電池用化学品に変換することを目指しています。また、アルゼンチンの鉱山関係者が強調したように、電池や電気自動車の製造にも乗り出しています。

- 2023年4月、中国の大手電気自動車メーカーBYDは、チリのアントファガスタ地方に2億9,000万米ドルのリチウム正極工場を建設する計画を発表しました。このような戦略的な動きは、今後数年で急増すると予想されます。

- 2023年半ば、アルゼンチン政府は初のリチウムイオン電池工場の計画を明らかにしました。この工場では、米国の大手鉱山会社Livent Corporationが現地で調達・加工した炭酸リチウムを利用します。国営YPFの子会社であるYPF Tecnologia(Y-TEC)が建設するこの工場は、豊富なリチウム埋蔵量に付加価値をつけるというアルゼンチンのコミットメントを意味します。700万米ドルを投資し、年間生産能力13MWh、据置型蓄電池1,000台を目指します。さらに、リチウムイオン電池の生産に熱心な地元企業への技術移転の機会を重視しています。

- リチウムイオン電池は、その軽量性、急速充電機能、充電サイクルの延長、コスト低下の背景から、特にこの地域のリチウム埋蔵量の多さと産業の進歩によって、市場を独占することになると考えられます。

著しい成長が期待されるブラジル

- ブラジルは近い将来、ラテンアメリカの二次電池市場で支配的な参入企業として台頭すると見られています。この急成長の主要要因は、電動モビリティ、再生可能エネルギー、消費財など、さまざまなセグメントで電池需要が高まっていることです。さらに、同産業の拡大は、政府の支援策や国内の技術革新によって後押しされています。

- 最近ブラジルは、政府の奨励策によって電気自動車(EV)の普及が急速に進んでいます。2023年のブラジルのEV販売台数は約5万2,000台(PHEV3万3,000台、BEV1万9,000台)に達し、2022年の1万8,500台(PHEV1万台、BEV8,500台)から大幅に増加しました。このEV販売台数の急増は、今後の二次電池市場を活性化させると予想されます。

- ブラジルは2024年1月より、100%輸入の電気自動車(EV)に対して10%の課税を開始しました。これを受けて、中国の自動車メーカー数社が現地での投資を活発化させています。特に、BYDはブラジルに生産拠点を設立し、2024年後半から2025年前半の生産を目指しており、長城汽車の工場は2024年の操業開始を目指しています。これらの動きにより、ブラジルの国内EV製造が強化され、二次電池の需要が拡大すると期待されています。

- 世界の動向を反映して、ブラジルは二酸化炭素排出量の削減と化石燃料への依存度の低減に積極的に取り組んでいます。電動モビリティへの移行を促進するため、政府はさまざまな補助金や優遇措置を展開しています。その代表例が、2023年末に開始された「グリーンモビリティ・イノベーション・プログラム」で、2024~2028年にかけて、低排出交通技術を開発する企業に対して190億ブラ以上の税制優遇措置が提供されます。このようなイニシアチブはEVセクターを強化し、二次電池市場に利益をもたらします。

- 自動車セグメント以外では、産業セグメントも市場の成長を牽引しています。バックアップ電源や再生可能エネルギー貯蔵などの用途で二次電池を利用する産業が増加しています。急成長する再生可能エネルギーセグメント、特に太陽光発電と風力発電は、先進的電池技術の需要を促進しています。

- 国際再生可能エネルギー機関(IRENA)によると、ブラジルの再生可能エネルギー容量は2023年に約194GWに達し、2020年から28.8%増加しました。2023年、ブラジルの太陽光発電容量は37GW以上、風力発電容量は29GW以上です。政府がこれらの能力をさらに増強する計画を立てているため、電池エネルギー貯蔵システム(BESS)の需要は増加するとみられます。

- 2024年5月、ノルウェーの巨大エネルギー企業Statkraft ASは、ブラジルのバイーアにある2つの風力発電所に275MWの太陽光発電容量を設置するための9億2,600万BRL(1億8,070万米ドル)の投資を発表しました。Sol de Brotasと名付けられたこの太陽光発電資産は、519MWのVentos de Santa Eugenia複合発電所と79.8MWのMorro do Cruzeiro風力発電複合発電所と統合されます。

- 2024年に建設予定のSol de BrotasはBESS技術を利用し、段階的に運転を開始:Morro do Cruzeiroは2025年8月、Ventos de Santa Eugeniaは2025年11月となります。

- 2023年初め、米国のフラクタルEMSとブラジルのYou.Onは、ブラジルで30MW/60MWhの蓄電池システム(BESS)を統合しました。フラクタルEMSは、BESSがピーク負荷時の電力供給を最適化し、送電の回復力を高め、ピーカープラントへの依存を減らすと強調しました。このようなプロジェクトは、特にフラクタルEMSの機器にとらわれないアプローチとYou.OnがKehuaインバータとCATL液冷電池を選択したことで、ブラジルで産業用二次電池の需要が高まる傾向を示しています。

- このような力学を考えると、ブラジルの二次電池市場は当面、大幅な成長を遂げると考えられます。

ラテンアメリカの二次電池産業概要

ラテンアメリカの二次電池市場は細分化されています。同市場の主要企業(順不同)には、Exide Industries Ltd、BYD Company Ltd、FIAMM Energy Technology SpA、Panasonic Holdings Corporation、EnerSysなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の普及拡大

- 再生可能エネルギー導入の増加

- 抑制要因

- 原料の需給ミスマッチ

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 技術

- 鉛蓄電池

- リチウムイオン

- その他の技術(NiMh、Nicdなど)

- 用途

- 自動車用電池

- 産業用電池(動力用、据置型(テレコム、UPS、エネルギー貯蔵システム(ESS)など))

- ポータブル電池(民生用電子機器製品など)

- その他

- 地域

- ブラジル

- メキシコ

- チリ

- コロンビア

- アルゼンチン

- その他のラテンアメリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- BYD Company Ltd

- EnerSys

- Panasonic Holdings Corporation

- Exide Industries Ltd

- FIAMM Energy Technology SpA

- C&D Technologies Inc.

- Duracell Inc.

- Saft Groupe SA

- Clarios

- Acumuladores Moura S.A.

- その他の著名な企業一覧(会社名、本社所在地、収益、関連製品、事業部門、連絡先など)

- 市場ランキング分析

第7章 市場機会と今後の動向

- データセンターなど商業インフラからの需要

- 電池リサイクルとセカンドライフ用途へのニーズ

目次

Product Code: 50004072

The Latin America Rechargeable Battery Market size is estimated at USD 5.80 billion in 2025, and is expected to reach USD 9.15 billion by 2030, at a CAGR of 9.57% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, declining lithium-ion battery prices, increasing adoption of electric vehicles, and the growing adoption of renewable energy are expected to drive the Latin America rechargeable battery market during the forecast period.

- Conversely, a mismatch in the demand and supply of raw materials is poised to impede the market's growth during the forecast period.

- However, rising demand from commercial infrastructures like data centers, coupled with the growing need for battery recycling and the second-life application of batteries, is set to unlock vast opportunities for the rechargeable battery market in Latin America.

- Brazil stands to see substantial growth in the rechargeable battery market, driven by surging electric vehicle sales and a broader adoption of renewable energy in the region.

Latin America Rechargeable Battery Market Trends

Lithium-ion Batteries to Witness Significant Growth

- During the forecast period, lithium-ion batteries (LIB) are poised to be among the fastest-growing segments in the Latin American rechargeable battery market. Their favorable capacity-to-weight ratio is making lithium-ion batteries increasingly popular compared to other types. Additional factors driving their adoption include superior performance (characterized by longevity and low maintenance), an extended shelf life, and a downward trend in prices.

- Offering distinct technical advantages, lithium-ion (Li-ion) batteries outshine traditional lead-acid batteries. For instance, while lead-acid batteries typically last for about 400-500 cycles, rechargeable Li-ion batteries boast an impressive average of over 5,000 cycles. Furthermore, Li-ion batteries demand less frequent maintenance and replacement. They also maintain consistent voltage throughout their discharge cycle, ensuring prolonged efficiency for connected electrical components.

- In recent years, major industry players have ramped up investments, focusing on economies of scale and R&D to boost battery performance. This surge in competition has led to a notable drop in lithium-ion battery prices. Thanks to technological advancements, manufacturing optimizations, and falling raw material costs, the volume-weighted average price of lithium-ion batteries plummeted from USD 780/kWh in 2013 to USD 139/kWh in 2023. Projections suggest a further decline to approximately USD 113/kWh by 2025 and USD 80/kWh by 2030, making lithium-ion batteries an increasingly attractive option.

- Historically, lithium-ion batteries found their primary application in consumer electronics like mobile phones and laptops. However, their role has expanded, with electric vehicles and battery energy storage systems (BESS) in the renewable energy sector increasingly relying on them.

- While the lithium-ion battery manufacturing industry in Latin America is still in its nascent stages, the region's abundant reserves of essential raw materials and the surging demand from diverse end-users signal a rapid market growth.

- Latin America, often dubbed the Lithium Triangle, boasts vast lithium reserves, a crucial component for lithium-ion batteries. This triangle encompasses Argentina, Bolivia, and Chile, collectively holding over half of the world's known lithium reserves. Chile leads in production, thanks to its extensive lithium-rich brine deposits in the Atacama Desert. Bolivia's Salar de Uyuni stands out as one of the globe's largest lithium reserves, despite extraction challenges. Argentina, with its salt flats in the Puna region, also plays a significant role. Together, these nations are integral to the global lithium-ion battery production supply chain.

- According to the US Geological Survey, lithium production figures for mid-2023 were approximately 44,000 metric tons in Chile, 9,600 metric tons in Argentina, and 4,900 metric tons in Brazil. Such substantial output positions Latin America as a pivotal player in the global lithium-ion battery landscape.

- Latin American countries are intensifying efforts to deepen their involvement in the electric vehicle supply chain. By capitalizing on their mineral wealth, enhancing processing capabilities, and eyeing vehicle manufacturing, nations like Argentina, Chile, Bolivia, and Brazil aim to transform more of their mined lithium into battery chemicals. They're also venturing into battery and electric vehicle manufacturing, as highlighted by Argentina's mining officials.

- In April 2023, BYD Co Ltd, China's leading electric vehicle manufacturer, announced plans for a USD 290 million lithium cathode factory in Chile's Antofagasta region, as reported by Chile's economic development agency, CORFO. Such strategic moves are expected to proliferate in the coming years.

- In mid-2023, the Argentinean government revealed plans for its inaugural lithium-ion battery plant. This facility will utilize lithium carbonate sourced and processed locally by US mining giant Livent Corporation. Constructed by YPF Tecnologia (Y-TEC), a subsidiary of the state-owned YPF, the plant signifies Argentina's commitment to adding value to its rich lithium reserves. With a USD 7 million investment, the facility aims for an annual production capacity of 13MWh, translating to 1,000 stationary energy storage batteries. Moreover, it emphasizes technology transfer opportunities for local firms keen on lithium-ion battery production.

- Given their lightweight nature, rapid charging capabilities, extended charging cycles, and the backdrop of declining costs, lithium-ion batteries are set to dominate the market, especially with the region's significant lithium reserves and industry advancements.

Brazil is Expected to Witness Significant Growth

- Brazil is poised to emerge as a dominant player in the Latin American rechargeable battery market in the near future. This surge is primarily fueled by the escalating demand for batteries across diverse sectors, notably electric mobility, renewable energy, and consumer goods. Furthermore, the industry's expansion is bolstered by supportive government initiatives and technological innovations within the nation.

- Recently, Brazil has seen a swift uptick in electric vehicle (EV) adoption, thanks to government-backed incentives. In 2023, Brazil's EV sales reached approximately 52,000 units (33,000 PHEV and 19,000 BEV), a substantial leap from 2022's 18,500 units (10,000 PHEV and 8,500 BEV). This surge in EV sales is anticipated to bolster the rechargeable battery market in the years ahead.

- Starting January 2024, Brazil imposed a 10% tax on imported 100% electric vehicles (EVs), set to escalate to 18% in July and peak at 35% by July 2026. In response, several Chinese automakers are ramping up local investments. Notably, BYD is establishing a manufacturing complex in Brazil, targeting production by late 2024 or early 2025, while Great Wall Motor's plant is set to commence operations in 2024. These moves are expected to enhance Brazil's domestic EV manufacturing and amplify the demand for rechargeable batteries.

- Echoing global trends, Brazil is actively working to curtail carbon emissions and reduce fossil fuel reliance. To facilitate this transition to electric mobility, the government has rolled out various subsidies and incentives. A prime example is the Green Mobility and Innovation Programme launched at the end of 2023, offering over BRA 19 billion in tax incentives from 2024 to 2028 for companies developing low-emission transport technologies. Such initiatives are poised to bolster the EV sector, subsequently benefiting the rechargeable battery market.

- Beyond the automotive realm, the industrial sector is also driving market growth. Industries are increasingly turning to rechargeable batteries for applications like backup power and renewable energy storage. The burgeoning renewable energy sector, especially solar and wind, is fueling the demand for advanced battery technologies.

- According to the International Renewable Energy Agency (IRENA), Brazil's renewable energy capacity reached about 194 GW in 2023, marking a 28.8% increase from 2020. In 2023, Brazil boasted over 37 GW in solar and 29 GW in wind energy capacities. With government plans to further boost these capacities, the demand for battery energy storage systems (BESS) is set to rise.

- In May 2024, Norwegian energy giant Statkraft AS unveiled a BRL 926 million (USD 180.7 million) investment to install 275 MW of solar capacity at two wind parks in Bahia, Brazil. The solar asset, named Sol de Brotas, will integrate with the 519 MW Ventos de Santa Eugenia complex and the 79.8 MW Morro do Cruzeiro wind power complex.

- Scheduled for construction in 2024, Sol de Brotas will utilize BESS technology, with operations commencing in phases: Morro do Cruzeiro in August 2025 and Ventos de Santa Eugenia in November 2025.

- In early 2023, United States-based Fractal EMS Inc and Brazil's You.On integrated a 30 MW/60 MWh battery energy storage system (BESS) in Brazil. Fractal EMS highlighted that the BESS will optimize power delivery during peak loads, enhancing transmission line resilience and reducing reliance on peaker plants. Such projects, especially with Fractal EMS's equipment-agnostic approach and You.On's choice of Kehua inverters and CATL liquid-cooled batteries, signal a growing trend in Brazil, boosting the demand for industrial rechargeable batteries.

- Given these dynamics, Brazil's rechargeable battery market is set for substantial growth in the foreseeable future.

Latin America Rechargeable Battery Industry Overview

The Latin Americarechargeable battery market is semi-fragmented. Some of the key players in the market (not in any particular order) include Exide Industries Ltd, BYD Company Ltd, FIAMM Energy Technology SpA, Panasonic Holdings Corporation, and EnerSys.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles

- 4.5.1.2 Growing Renewable Energy Installation

- 4.5.2 Restraints

- 4.5.2.1 Demand-Supply Mismatch of Raw Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lead-Acid

- 5.1.2 Lithium-Ion

- 5.1.3 Other Technologies (NiMh, Nicd, etc.)

- 5.2 Application

- 5.2.1 Automotive Batteries

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.2.3 Portable Batteries (Consumer Electronics, etc.)

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Brazil

- 5.3.2 Mexico

- 5.3.3 Chile

- 5.3.4 Colombia

- 5.3.5 Argentina

- 5.3.6 Rest of Latin America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Company Ltd

- 6.3.2 EnerSys

- 6.3.3 Panasonic Holdings Corporation

- 6.3.4 Exide Industries Ltd

- 6.3.5 FIAMM Energy Technology SpA

- 6.3.6 C&D Technologies Inc.

- 6.3.7 Duracell Inc.

- 6.3.8 Saft Groupe SA

- 6.3.9 Clarios

- 6.3.10 Acumuladores Moura S.A.

- 6.4 List of Other Prominent Companies (Company Name, Headquarters, Revenue, Relevant Products, Operating Sector, Contact Details, etc.) (In Brief Tabular Format)

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Demand from Commercial Infrastructures Such as Data Centers

- 7.2 Need for a Battery Recycling and Second-life Applications

ラテンアメリカの二次電池:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日