|

|

市場調査レポート

商品コード

1636548

スペインの二次電池:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Spain Rechargeable Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スペインの二次電池:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

スペインの二次電池市場規模は2025年に26億米ドルと推定され、予測期間(2025~2030年)のCAGRは14.72%で、2030年には51億7,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、リチウムイオン電池価格の下落、電気自動車の普及拡大、政府主導による再生可能エネルギーセグメントの拡大が、予測期間中のスペインの二次電池市場を牽引すると予想されます。

- 一方、原料の需給ミスマッチや電池技術に関する安全性の問題が、予測期間中の市場成長の妨げになると予想されます。

- 新しい電池技術や先進的な電池化学品の開発が進んでいることから、スペインの二次電池市場にビジネス機会が生まれる可能性は高いです。

スペインの二次電池市場動向

リチウムイオン電池が急成長

- 様々な電池技術の中で、リチウムイオン電池(LIB)が二次電池市場を独占し、予測期間中に急成長を遂げると考えられます。リチウムイオン電池の人気が他の電池に比べて高まっているのは、容量対重量比が優れていること、保存可能期間が長いこと、メンテナンスの必要性が少ないこと、価格が低下していることなどがその理由です。

- リチウムイオン電池は、従来の鉛蓄電池と比較して技術的に明確な優位性を誇っています。例えば、鉛蓄電池の寿命が約400~500サイクルであるのに対し、充電式リチウムイオン電池は5,000サイクルを超えることができます。さらに、リチウムイオン電池はメンテナンスや交換の頻度が少ないです。また、放電サイクルを通じて安定した電圧を維持するため、接続された電気部品の効率も長持ちします。

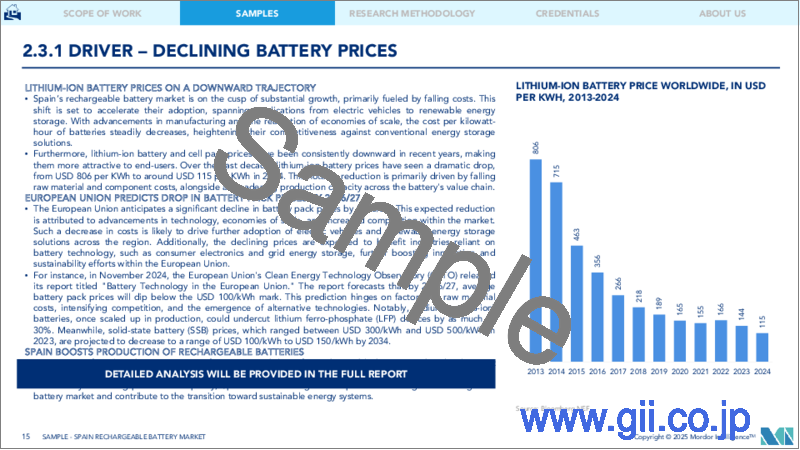

- 近年、産業の大手企業は、リチウムイオン電池の性能を向上させるため、研究開発と生産への投資を強化し、競争を激化させ、価格を引き下げています。技術の進歩、製造の最適化、原料コストの低下により、リチウムイオン電池の平均価格は2013年の780米ドル/kWhから2023年には139米ドル/kWhに急落しました。2025年には約113米ドル/kWh、2030年には約80米ドル/kWhまでさらに下落すると予測されており、リチウムイオン電池はますます魅力的な選択肢となっています。

- 歴史的に、リチウムイオン電池は携帯電話やノートパソコンなどの民生用電子機器製品に電力を供給してきました。しかし、その用途はハイブリッド車、完全電気自動車(BEV)、再生可能エネルギーセグメントの電池エネルギー貯蔵システム(BESS)などへと拡大しています。

- 2022年初頭、Volkswagen Groupはパートナーと共同で、バレンシア近郊のサグントにリチウムイオン電池のギガファクトリーを建設する計画を発表しました。この場所は、近隣のマルトレルとパンプローナのEV工場に電池セルを供給するために戦略的に選ばれました。推定コスト32億5,000万米ドルのこのプロジェクトは、年間生産能力40GWhを目指しています。建設は2023年第1四半期に開始され、2026年に生産を開始する予定です。このギガファクトリーは、スウェーデンとドイツにある既存の拠点に続く、Volkswagenにとって3番目の拠点となります。さらにVolkswagenグループは、欧州全域にさらに6つの40GWhギガファクトリーを設立し、2030年までに累積生産能力240GWhを達成することを構想しています。

- サステイナブル活動の重要性を認識するスペインでは、リチウムイオン電池のリサイクルへの取り組みが急増しています。安全なリサイクルは必須ミネラルを保護するだけでなく、廃棄に代わるサステイナブル選択肢を提示します。2023年7月、韓国の電池・リサイクル専門企業であるSungEel HiTechは、スペインのBeePlanet Factoryと提携し、電気自動車のリチウムイオン電池の再利用とリサイクルに焦点を当てたコンソーシアムを設立しました。

- BeeCycleと名付けられたこのコンソーシアムは、カパロソ(ナバラ州)にリサイクル工場を建設し、事業を開始します。2025年に操業開始予定のこの施設では、ライフサイクルが終了した電池や電池セル製造時のスクラップを処理します。年間1万トンの処理能力を持ち、年間2万5,000台の自動車生産量に相当する「ブラックマス」(電池から粉砕された金属複合体)を生産することを目指しています。

- 2023年4月、Glencore、FCC Ambito、Iberdrolaは、スペインで大規模なリチウムイオン電池のリサイクルソリューションを確立するための共同取り組みを発表しました。彼らの目標は、セカンドライフ再利用と使用済みリサイクルソリューションの両方を提供する専用施設を設置することで、リチウムイオン電池のリサイクルという差し迫った課題に対処することです。

- リチウムイオン電池は、その軽量性、急速充電機能、充電サイクルの延長、コストの低下、産業の進歩を考慮すると、予測期間中、スペインの二次電池市場で最も急成長する電池技術になると考えられています。

電気自動車の普及が市場を牽引

- スペインの二次電池市場、特にリチウムイオン電池市場は、同国の電気自動車(EV)普及の加速によって急成長します。国際エネルギー機関(IEA)の最新データは、この動向を浮き彫りにしています。スペインにおけるBEVの販売台数は、2023年には約5万7,000台に急増し、2022年の3万3,000台から72%増加します。さらに、PEVの販売台数は2023年に約6万5,000台に達しました。このようなEVの普及は、スペインにおける二次電池の需要増を示唆しています。

- 2023年、スペインのBEV在庫は約16万台に達し、2022年の9万6,000台から66%増加しました。一方、PEVの在庫は50%増加し、約20万台に達しました。このような成長にもかかわらず、スペインの総自動車在庫は、2030年までに550万台の電気自動車という政府の野心的な目標には達していないです。このギャップは、二次電池に対する将来の需要が旺盛であることを裏付けています。

- スペインは近年、EV参入企業にとっての焦点となっています。特に2024年4月、Ebro-EV MotorsとChery Automobileはバルセロナで合弁会社を設立し、Chery AutomobileはEbroの旧Nissan工場を活用して欧州で生産する初の中国自動車メーカーとなりました。

- もうひとつの重要な動きとして、EVサプライヤーのMobisは2024年4月、スペインのナバラ州に1億2,800万米ドルを投資する計画を発表しました。この投資は、西欧初の電動化専用工場の設立を目指しています。ナバーラはスペインの北端に位置し、フランスと国境を接する戦略的な立地で、欧州本土へのゲートウェイとなります。ソウル出身のMobisは、韓国、中国、チェコに電池システムの生産拠点を持ち、米国とインドネシアにも工場を建設中です。

- 2026年に大量生産を開始する予定のMobisのスペイン工場は、年間36万台の電池システムアセンブリ(BSA)の意欲的な生産を目指しています。これらのアセンブリは、EVの効率性と安全性にとって重要であり、電子部品と電池管理システム(BMS)を統合しています。戦略的な動きとして、Mobisは2023年にVolkswagenと重要なBSA契約を締結しました。新工場で生産されるBSAは、Volkswagenの次世代EVプラットフォーム向けで、パンプローナで生産される予定です。

- このような開発により、スペインの二次電池市場は、進化するEV事情に後押しされ、成長する態勢が整っています。

スペインの二次電池産業概要

スペインの二次電池市場は細分化されています。同市場の主要企業(順不同)には、Panasonic Corporation、BYD Company Ltd.、AESC Group Ltd.、Samsung SDI、LG Energy Solution Ltd.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の普及拡大

- リチウムイオン電池コストの低下

- 抑制要因

- 原料の需給ミスマッチ

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- 技術

- 鉛蓄電池

- リチウムイオン

- その他の技術(NiMh、Nicdなど)

- 用途

- 自動車用電池

- 産業用電池(動力用、据置型(テレコム、UPS、エネルギー貯蔵システム(ESS)など))

- ポータブル電池(民生用電子機器製品など)

- その他

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Panasonic Corporation

- BYD Company Ltd.

- AESC Group Ltd.

- Contemporary Amperex Technology Co. Limited

- Exide Technologies

- Toshiba Corporation

- Samsung SDI Co. Ltd

- Duracell Inc.

- Clarios, LLC.

- その他の著名な企業一覧

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 新しい電池技術と先進電池化学の開発の進展

目次

Product Code: 50004024

The Spain Rechargeable Battery Market size is estimated at USD 2.60 billion in 2025, and is expected to reach USD 5.17 billion by 2030, at a CAGR of 14.72% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the declining lithium-ion battery prices, increasing adoption of electric vehicles, and the growing renewable energy sector aided by government initiatives are expected to drive the Spain rechargeable battery market during the forecast period.

- On the other hand, the demand-supply mismatch of raw materials, and the safety issues related to battery technologies are expected to hinder the market's growth during the forecast period.

- Nevertheless, the growing progress in developing new battery technologies and advanced battery chemistries will likely create opportunities for the Spain rechargeable battery market.

Spain Rechargeable Battery Market Trends

Lithium-ion Battery to be the Fastest Growing

- Among various battery technologies, lithium-ion batteries (LIBs) are poised to dominate the rechargeable battery market, experiencing rapid growth during the forecast period. Their rising popularity over other battery types can be attributed to their superior capacity-to-weight ratio, extended shelf life, reduced maintenance needs, and declining prices.

- Li-ion batteries boast distinct technical advantages over traditional lead-acid batteries. For instance, while lead-acid batteries offer a lifespan of approximately 400-500 cycles, rechargeable Li-ion batteries can exceed 5,000 cycles. Moreover, Li-ion batteries require less frequent maintenance and replacement. They also maintain consistent voltage throughout their discharge cycle, ensuring prolonged efficiency for connected electrical components.

- In recent years, major industry players have ramped up investments in R&D and production to enhance lithium-ion battery performance, intensifying competition and driving down prices. Due to technological advancements, manufacturing optimizations, and falling raw material costs, the average price of lithium-ion batteries plummeted from USD 780/kWh in 2013 to USD 139/kWh in 2023. Projections suggest a further decline to around USD 113/kWh by 2025 and USD 80/kWh by 2030, making lithium-ion batteries an increasingly attractive option.

- Historically, lithium-ion batteries powered consumer electronics like mobile phones and laptops. However, their application has expanded to include hybrids, fully electric vehicles (BEVs), and battery energy storage systems (BESS) in the renewable energy sector.

- In early 2022, the Volkswagen Group, in collaboration with partners, announced plans for a lithium-ion battery gigafactory in Sagunto, near Valencia. This location was strategically selected to supply battery cells to nearby EV plants in Martorell and Pamplona. The project, with an estimated cost of USD 3.25 billion, aims for an annual production capacity of 40 GWh. Construction commenced in Q1 2023, with production slated to begin in 2026. This gigafactory will be Volkswagen's third, joining existing sites in Sweden and Germany. Furthermore, the group envisions establishing six additional 40 GWh gigafactories across Europe, targeting a cumulative capacity of 240 GWh by 2030.

- Recognizing the importance of sustainable practices, Spain has seen a surge in lithium-ion battery recycling initiatives. Safe recycling not only conserves essential minerals but also presents a sustainable alternative to disposal. In July 2023, South Korean battery recycling specialist SungEel HiTech partnered with Spain's BeePlanet Factory to form a consortium focused on reusing and recycling lithium-ion batteries from electric vehicles.

- This consortium, named BeeCycle, will kick off its operations by constructing a recycling plant in Caparroso (Navarre). Set to commence in 2025, the facility will handle batteries at the end of their life cycle and scrap from battery cell manufacturing. With a processing capacity of 10,000 tonnes annually, it aims to produce 'black mass' - a crushed metal composite from batteries - equivalent to the output of 25,000 cars per year.

- In April 2023, Glencore, FCC Ambito, and Iberdrola announced a collaborative effort to establish large-scale lithium-ion battery recycling solutions in Spain. Their goal is to address the pressing challenge of lithium-ion battery recycling by setting up a dedicated facility that offers both second-life repurposing and end-of-life recycling solutions.

- Given their lightweight nature, rapid charging capabilities, extended charging cycles, decreasing costs, and advancements in the industry, lithium-ion batteries are set to become the fastest-growing battery technology in Spain's rechargeable battery market during the forecast period.

Increasing Adoption of Electric Vehicles To Drive the Market

- Spain's rechargeable battery market, especially for lithium-ion batteries, is set to surge, driven by the country's accelerating adoption of electric vehicles (EVs). Recent data from the International Energy Agency (IEA) highlights this trend: BEV sales in Spain jumped to approximately 57,000 units in 2023, marking a 72% increase from 33,000 units in 2022. Additionally, PEV sales reached around 65,000 units in 2023. This uptick in EV adoption signals a corresponding rise in demand for rechargeable batteries in Spain.

- In 2023, BEV stocks in Spain hit about 160,000 units, a notable 66% increase from 96,000 in 2022. Meanwhile, PEV stocks grew by 50%, reaching around 200,000 units. Despite this growth, Spain's total vehicle stock falls short of the government's ambitious target of 5.5 million electric vehicles by 2030. This gap underscores a robust future demand for rechargeable batteries.

- Spain has become a focal point for EV players in recent years. Notably, in April 2024, Ebro-EV Motors and Chery Automobile forged a joint venture in Barcelona, marking Chery as the first Chinese automaker to produce in Europe, utilizing Ebro's former Nissan plant.

- In another significant move, EV supplier Mobis, in April 2024, unveiled plans for a USD 128 million investment in Navarre, Spain. This investment aims to establish Western Europe's inaugural electrification-dedicated plant. Navarre, strategically located at Spain's northern tip bordering France, offers a gateway into mainland Europe. Mobis, hailing from Seoul, boasts battery system production facilities across Korea, China, and the Czech Republic, with additional plants underway in the U.S. and Indonesia.

- Set to commence mass production in 2026, Mobis' Spanish facility aims for an ambitious output of 360,000 annual battery system assemblies (BSA). These assemblies, crucial for EV efficiency and safety, integrate electronic components and the Battery Management System (BMS). In a strategic move, Mobis clinched a significant BSA contract with Volkswagen in 2023. The BSAs from the new plant are destined for Volkswagen's next-gen EV platforms, set to be produced in Pamplona.

- Given these developments, Spain's rechargeable battery market is poised for growth, driven by the nation's evolving EV landscape.

Spain Rechargeable Battery Industry Overview

The Spain rechargeable battery market is semi-fragmented. Some of the key players in the market (not in any particular order) include Panasonic Corporation, BYD Company Ltd., AESC Group Ltd., Samsung SDI Co. Ltd., and LG Energy Solution Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles

- 4.5.1.2 Declining Lithium-ion Battery Cost

- 4.5.2 Restraints

- 4.5.2.1 Demand-Supply Mismatch of Raw Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lead-Acid

- 5.1.2 Lithium-Ion

- 5.1.3 Other Technologies (NiMh, Nicd, etc.)

- 5.2 Application

- 5.2.1 Automotive Batteries

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.2.3 Portable Batteries (Consumer Electronics, etc.)

- 5.2.4 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Panasonic Corporation

- 6.3.2 BYD Company Ltd.

- 6.3.3 AESC Group Ltd.

- 6.3.4 Contemporary Amperex Technology Co. Limited

- 6.3.5 Exide Technologies

- 6.3.6 Toshiba Corporation

- 6.3.7 Samsung SDI Co. Ltd

- 6.3.8 Duracell Inc.

- 6.3.9 Clarios, LLC.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Progress in Developing New Battery Technologies and Advanced Battery Chemistries