|

市場調査レポート

商品コード

1636549

フランスの二次電池:市場シェア分析、産業動向、成長予測(2025~2030年)France Rechargeable Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フランスの二次電池:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

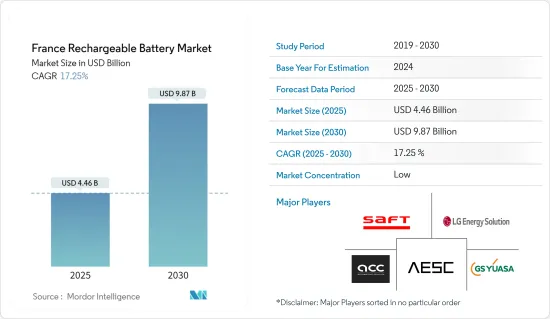

フランスの二次電池市場規模は2025年に44億6,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは17.25%で、2030年には98億7,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、リチウムイオン電池の価格下落、電気自動車の普及拡大、政府支援による再生可能エネルギーセグメントの拡大が、予測期間中のフランスの二次電池市場を牽引すると予想されます。

- 一方、原料の需給ミスマッチや電池技術に関する安全性の問題が、予測期間中の市場成長の妨げになる可能性が高いです。

- 新しい電池技術や先進的な電池化学品の開発が進んでいることから、フランスの二次電池市場にビジネス機会が生まれる可能性は高いです。

フランスの二次電池市場の動向

自動車用電池が大きく成長

- フランスでは、自動車用途が二次電池市場を独占する構えです。同国で電気自動車(EV)が普及するにつれ、二次電池、特にリチウムイオンタイプの需要が急増します。

- さらに、鉛蓄電池は自動車の始動、照明、点火(SLI)アクセサリーに電力を供給しています。これらのSLI電池は、エンジン始動に必要な重要な初期電力を供給します。ディープサイクル電池よりも小型で軽量であるため、その需要は持続すると予測され、フランスの二次電池市場を強化しています。

- 国際自動車工業連合会(OICA)のデータによると、フランスの2023年の新車販売台数は220万台を超え、2022年の192万台から14.67%、2021年の214万台から3.12%増加しました。このような自動車販売の増加は、自動車用途での二次電池の採用をさらに促進すると予想されます。

- さらに、フランスの自動車部門では、電気自動車(EV)の採用が顕著に増加しています。国際エネルギー機関(IEA)の報告によると、フランスにおける電池式電気自動車(BEV)の販売台数は2023年に約31万台に達し、2022年の21万台から47%の大幅増となります。この急速なEVの普及は、フランスにおける二次電池の需要に拍車をかけることになります。

- 2024年5月、フランス政府は、中国との激しい競合にもかかわらず、2030年までに200万台の電気自動車またはハイブリッド車を生産することを自動車メーカーに課題として提示しました。新たな中期協定の一環として、産業は2027年までに80万台の電気自動車販売を目標としており、これは2022年の20万台から大幅に急増します。さらに、自動車メーカーは、電気自動車(EV)の年間販売台数を2022年の16,500台から100,000台に増やすことを目標としています。

- EVの生産と購入をさらに強化するため、フランス政府は2024年に15億ユーロ(16億米ドル)を割り当てた。フランスで販売される新車の20%近くが電気自動車だが、国産車はわずか12%にすぎないです。政府と産業の合意はまた、2030年までに40万カ所の充電ポイントを、2027年までに2万5,000カ所の急速充電ポイントを、主要ルート沿いや主要都市に戦略的に配置することを想定しています。これらの構想は、今後数年間で、二次電池、特にリチウムイオン・タイプの需要を大幅に押し上げる構えです。

- 2023年5月、StellantisはTotalEnergies、Mercedes-Benzと共同で、フランスのビリー・ベルクロー・ドゥブランにAutomotive Cells Company(ACC)の電池ギガ工場を開設しました。これは、欧州で計画されている3つのギガファクトリーの第1号となります。13ギガワット時(GWh)の生産能力からスタートし、2030年までに40GWhまで拡大するこの施設は、CO2排出量を最小限に抑えながら高性能のリチウムイオン電池を生産することを目指しています。このギガファクトリーは、2030年までに欧州で250GWhの電池生産能力を達成するというStellantisの野心的な目標に沿ったものです。

- 2024年1月、台湾の電気自動車用電池メーカーであるProLogium Technology Co.は、2027年にフランスの新工場で量産を開始し、株式公開を目指す計画を発表しました。2023年初め、フランスのエマニュエル・マクロン大統領は、プロロジムによるダンケルクの電池工場への52億ユーロ(56億7,000万米ドル)の巨額投資を強調し、欧州の電気自動車産業のハブとしてのフランスの地位をさらに強固なものにしました。こうした戦略的な動きは、フランスが二次電池セグメントで前進するというコミットメントを強調するものです。

- こうした新興国市場の開発により、フランスの二次電池市場は自動車セグメントで急拡大が見込まれています。

市場を牽引する再生可能エネルギーセグメントの採用拡大

- フランスでは再生可能エネルギーの導入が進んでおり、二次電池市場を大きく牽引することになります。国際再生可能エネルギー機関(IRENA)の報告によると、フランスの再生可能エネルギーの累積容量は2023年に約69.3GWに達し、2022年から7%増加しました。フランスが太陽エネルギーと風力エネルギーに傾注するにつれて、効率的な電池エネルギー貯蔵システム(BESS)の需要が急増し、これらの電源の断続的な性質のバランスをとるために重要です。このシナリオの主役であるリチウムイオン電池は、ピーク時に余剰エネルギーを貯蔵し、需要が急増したときや生産が衰えたときにそれを放出します。

- 2050年までに温室効果ガス排出量の80%削減(1990年比)を目指すフランスの野心的なエネルギー転換プロジェクトは、BESS市場を牽引することになります。さらに、新しい法律では、2035年までに原子力エネルギー消費を75%から50%に削減することが義務付けられています。このシフトは、原子力の出力減少を補い、再生可能エネルギーへの取り組みを強化する態勢を整えています。このような動きは、再生可能エネルギーへの投資を呼び込むだけでなく、先進的電池エネルギー貯蔵システムの緊急の必要性を強調し、最先端の二次電池の需要を増幅させる。

- 2023年9月、Q ENERGYはフランスのサン・アヴォルドにあるエミール・ユシェ発電所で「メルベット」エネルギー貯蔵プロジェクトを開始しました。35MW、44MWhの容量を持つこのシステムは、約1万人の住民の1日の電力需要を満たすことができます。最先端の電池コンテナ24個を備えたこのプロジェクトは、再生可能エネルギーの統合を支援し、より環境に優しいエネルギーミックスに貢献するエネルギー貯蔵部門の成長を象徴しています。

- さらに、複数の企業が新たな蓄電池プロジェクトを発表しています。2022年12月、TeslaはElectricite de Franceに196MWhの電池システムを提供し、太陽光発電所とリンクさせました。2022年8月、BayWa r.e.はオート・サントンジュ共同体から、40MWpの太陽光発電所と年間出力52GWhの蓄電池を備えた太陽光発電・蓄電施設の設立を依頼されました。

- 再生可能エネルギーの導入と電池技術の進歩の相互作用が、活気ある市場風景を生み出しています。企業は、効率的で耐久性があり、費用対効果の高い電池ソリューションを考案するため、研究開発に多額の投資を行っています。このような技術革新への取り組みは、エネルギー貯蔵の課題を克服し、フランスの野心的な再生可能エネルギー目標を達成するために不可欠です。

- 2024年5月、Skeleton Technologiesはフランスのオクシタニー地方への進出を発表し、5年間で6億ユーロの投資を約束しました。事業拡大の手始めとして、Skeletonはトゥールーズで次世代電池技術の研究開発を開始します。続いて、オクシタニーに「スーパー電池」の製造部門を設立します。高出力で急速充電が可能なエネルギー貯蔵に重点を置くSkeletonの製品は、EVから航空宇宙まで多様なセグメントに対応し、CO2削減と省エネルギーに重点を置いています。

- 2024年4月、Schneider Electricは最新の電池蓄電システム(BESS)を発表しました。マイクログリッドシステムに統合されたBESSは、さまざまなエネルギー源からエネルギーを回収し、将来の使用のために貯蔵します。ユニークな分散型エネルギー資源(DER)として、BESSは需要充電の削減から再生可能な自己消費まで、幅広いエネルギー用途をサポートします。

- まとめると、フランスがサステイナブル低炭素エネルギーの未来に向かって前進する中、再生可能エネルギーの採用と信頼性の高いエネルギー貯蔵の需要との相乗効果は、二次電池市場の主要な触媒となる準備が整っています。

フランスの二次電池産業概要

フランスの二次電池市場は半細分化されています。同市場の主要企業(順不同)には、Saft Groupe SAS、LG Energy Solution Ltd.、AESC Group Ltd.、Automotive Cells Company(ACC)、GS Yuasa Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の普及拡大

- 再生可能エネルギーセグメントの採用拡大

- リチウムイオン電池コストの低下

- 抑制要因

- 原料の需給ミスマッチ

- 促進要因

- サプライチェーン分析

- PESTLE分析

- 投資分析

第5章 市場セグメンテーション

- 技術

- 鉛蓄電池

- リチウムイオン

- その他の技術(NiMh、Nicdなど)

- 用途

- 自動車用電池

- 産業用電池(動力用、据置型(テレコム、UPS、エネルギー貯蔵システム(ESS)など))

- ポータブル電池(民生用電子機器製品など)

- その他

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Saft Groupe SAS

- LG Energy Solution Ltd.

- AESC Group Ltd.

- Automotive Cells Company(ACC)

- GS Yuasa Corporation

- Exide Technologies

- Panasonic Corporation

- Duracell Inc.

- Schneider Electric SE

- Contemporary Amperex Technology Co., Limited

- EnerSys

- その他の著名な企業一覧(会社名、本社所在地、関連製品とサービス、連絡先など)

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 新しい電池技術と先進電池化学の開発の進展

目次

Product Code: 50004025

The France Rechargeable Battery Market size is estimated at USD 4.46 billion in 2025, and is expected to reach USD 9.87 billion by 2030, at a CAGR of 17.25% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, declining lithium-ion battery prices, increasing adoption of electric vehicles, and the growing renewable energy sector aided by government are expected to drive the France rechargeable battery market during the forecast period.

- On the other hand, the demand-supply mismatch of raw materials, and the safety issues related to battery technologies are likely to hinder the market's growth during the forecast period.

- Nevertheless, the growing progress in developing new battery technologies and advanced battery chemistries will likely create opportunities for the France rechargeable battery market.

France Rechargeable Battery Market Trends

Automotive Batteries Segment to Witness Significant Growth

- In France, automotive applications are poised to dominate the rechargeable batteries market. As electric vehicles (EVs) gain traction in the country, the demand for rechargeable batteries, particularly lithium-ion types, is set to surge.

- Moreover, lead-acid batteries power the starting, lighting, and ignition (SLI) accessories in vehicles. These SLI batteries provide the crucial initial power burst needed to start an engine. Being smaller and lighter than deep-cycle batteries, their demand is projected to persist, bolstering the French rechargeable battery market.

- Data from the International Organization of Motor Vehicle Manufacturers (OICA) reveals that France sold over 2.20 million new motor vehicles in 2023, marking a 14.67% jump from 2022's 1.92 million and a 3.12% rise from 2021's 2.14 million. This uptick in vehicle sales is expected to further drive the adoption of rechargeable batteries in automotive applications.

- Furthermore, the French automotive sector has witnessed a notable uptick in the adoption of electric vehicle (EV). The International Energy Agency (IEA) reported that battery electric vehicle (BEV) sales in France hit approximately 310,000 units in 2023, a robust 47% increase from 2022's 210,000 units. This rapid EV adoption is set to fuel the demand for rechargeable batteries in France.

- In May 2024, the French government challenged its carmakers to produce two million electric or hybrid vehicles by 2030, despite fierce competition from China. As part of a new medium-term agreement, the industry targets 800,000 electric vehicle sales by 2027, a significant jump from 200,000 in 2022. Furthermore, carmakers aim to boost annual sales of electric light utility vehicles to 100,000, up from 16,500 in 2022.

- To further bolster EV production and purchases, the French government allocated EUR 1.5 billion (USD 1.6 billion) in 2024. While nearly 20% of new cars sold in France are electric, only 12% are domestically produced. The government-industry agreement also envisions 400,000 charging points by 2030 and 25,000 quick charging points by 2027, strategically located along major routes and in major cities. These initiatives are poised to significantly boost the demand for rechargeable batteries, especially lithium-ion types, in the coming years.

- In May 2023, Stellantis, in collaboration with TotalEnergies and Mercedes-Benz, inaugurated the Automotive Cells Company's (ACC) battery gigafactory in Billy-Berclau Douvrin, France. This marks the first of three planned gigafactories in Europe. Starting with a production line capacity of 13 gigawatt-hours (GWh), set to expand to 40GWh by 2030, the facility aims to produce high-performance lithium-ion batteries with a minimal CO2 footprint. This gigafactory aligns with Stellantis' ambitious target of achieving a 250 GWh battery manufacturing capacity in Europe by 2030.

- In January 2024, ProLogium Technology Co., a Taiwanese electric vehicle battery manufacturer, announced plans to commence mass production at its new French factory in 2027, with aspirations for an initial public offering. Earlier in 2023, French President Emmanuel Macron highlighted ProLogium's significant EUR 5.2 billion (USD 5.67 billion) investment in a Dunkirk-based battery factory, further solidifying France's emerging status as a hub for Europe's electric car industry. These strategic moves underscore France's commitment to advancing in the rechargeable battery domain.

- Given these developments, the automotive segment is set for rapid expansion in France's rechargeable battery market.

Growing Adoption of Renewable Energy Sector To Drive the Market

- France's increasing embrace of renewable energy is set to significantly propel the rechargeable batteries market. The International Renewable Energy Agency (IRENA) reported that France's cumulative renewable energy capacity hit approximately 69.3 GW in 2023, marking a 7% rise from 2022. As France leans into solar and wind energy, the demand for efficient battery energy storage systems (BESS) surges, which is crucial for balancing the intermittent nature of these sources. Lithium-ion batteries, a key player in this scenario, store excess energy during peak production and release it when demand spikes or production wanes.

- France's ambitious energy transition projects, aiming for an 80% reduction in greenhouse gas emissions by 2050 (relative to 1990 levels), are set to drive the BESS market. Additionally, a new law mandates a reduction in nuclear energy consumption from 75% to 50% by 2035. This shift is poised to bolster renewable energy initiatives, compensating for the diminished nuclear output. Such moves not only attract investments in renewables but also underscore the urgent need for advanced battery energy storage systems, amplifying the demand for cutting-edge rechargeable batteries.

- In September 2023, Q ENERGY kicked off the "Merbette" energy storage project at the Emile Huchet power plant in Saint-Avold, France. With a capacity of 35 MW and 44 MWh, the system can meet the daily electricity needs of about 10,000 residents. Featuring 24 state-of-the-art battery containers, this project symbolizes the energy storage sector's growth, aiding in renewable energy integration and contributing to a greener energy mix.

- Moreover, several companies have unveiled new battery energy storage projects. In December 2022, Tesla provided a 196 MWh battery system to Electricite de France, linking it to a solar power plant. In August 2022, BayWa r.e. was selected by the Haute-Saintonge Community to establish a solar and battery storage facility, featuring a 40MWp PV park and an annual output of 52 GWh.

- The interplay between renewable energy adoption and battery technology advancements is creating a vibrant market landscape. Companies are heavily investing in R&D to devise efficient, durable, and cost-effective battery solutions. This commitment to innovation is vital for overcoming energy storage challenges and achieving France's ambitious renewable energy goals.

- In May 2024, Skeleton Technologies announced its expansion into France's Occitanie region, committing EUR 600 million over five years. Kicking off its expansion, Skeleton is initiating R&D in Toulouse for next-gen battery tech. Following this, they'll establish a manufacturing unit in Occitanie for their "SuperBattery." Focusing on high-power, fast-charging energy storage, Skeleton's products cater to diverse sectors, from EVs to aerospace, emphasizing CO2 reduction and energy conservation.

- In April 2024, Schneider Electric unveiled its latest Battery Energy Storage System (BESS). Integrated into microgrid systems, BESS captures and stores energy from various sources for future use. As a unique Distributed Energy Resource (DER), BESS supports a wide array of energy applications, from demand-charge reduction to renewable self-consumption.

- In summary, as France strides towards a sustainable, low-carbon energy future, the synergy between renewable energy adoption and the demand for reliable energy storage is poised to be a major catalyst for the rechargeable batteries market.

France Rechargeable Battery Industry Overview

The France rechargeable battery market is semi-fragmented. Some of the key players in the market (not in any particular order) include Saft Groupe SAS, LG Energy Solution Ltd., AESC Group Ltd., Automotive Cells Company (ACC), and GS Yuasa Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, in USD till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles

- 4.5.1.2 Growing Adoption of Renewable Energy Sector

- 4.5.1.3 Declining Lithium-ion Battery Cost

- 4.5.2 Restraints

- 4.5.2.1 Demand-Supply Mismatch of Raw Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lead-Acid

- 5.1.2 Lithium-Ion

- 5.1.3 Other Technologies (NiMh, Nicd, etc.)

- 5.2 Application

- 5.2.1 Automotive Batteries

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.2.3 Portable Batteries (Consumer Electronics, etc.)

- 5.2.4 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Saft Groupe SAS

- 6.3.2 LG Energy Solution Ltd.

- 6.3.3 AESC Group Ltd.

- 6.3.4 Automotive Cells Company (ACC)

- 6.3.5 GS Yuasa Corporation

- 6.3.6 Exide Technologies

- 6.3.7 Panasonic Corporation

- 6.3.8 Duracell Inc.

- 6.3.9 Schneider Electric SE

- 6.3.10 Contemporary Amperex Technology Co., Limited.

- 6.3.11 EnerSys

- 6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Progress in Developing New Battery Technologies and Advanced Battery Chemistries