アジア太平洋の二次電池:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Asia-Pacific Rechargeable Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636545

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

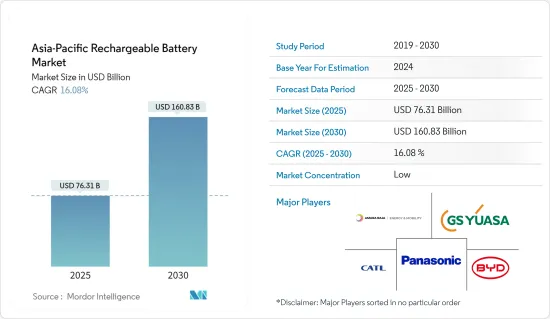

アジア太平洋の二次電池市場規模は2025年に763億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは16.08%で、2030年には1,608億3,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、リチウムイオン電池価格の下落、電気自動車の普及拡大、再生可能エネルギーセグメントの拡大が、予測期間中のアジア太平洋の二次電池市場を牽引すると予想されます。

- 一方、原料の需給ミスマッチが予測期間中の市場成長の妨げになると予想されます。

- 新しい電池技術や先進的な電池化学品の開発が進んでいることから、アジア太平洋の二次電池市場には大きなビジネス機会が生まれる可能性が高いです。

- 同地域の国々の中では、電気自動車、民生用電子機器製品、再生可能プロジェクトにおけるエネルギー貯蔵システムの採用が増加しているインドが大きな成長を遂げると予想されます。

アジア太平洋の二次電池市場動向

リチウムイオン電池が急成長

- さまざまな電池技術の中で、リチウムイオン電池(LIB)が二次電池市場を独占し、予測期間中に急成長を遂げる展望です。リチウムイオン電池の人気が他のタイプの電池よりも高まっているのは、容量対重量比が優れていること、保存可能期間が長いこと、メンテナンスの必要性が少ないこと、価格が急落していることに起因しています。

- リチウムイオン電池は、従来の鉛蓄電池に比べて技術的にいくつかの利点を誇っています。鉛電池は通常400~500サイクルですが、充電式リチウムイオン電池は5,000サイクルを超えることができます。さらに、リチウムイオン・電池はメンテナンスや交換の頻度が少ないです。また、放電サイクルを通じて安定した電圧を維持するため、接続された電気部品の効率が長持ちします。

- アジア太平洋の主要企業は、研究開発と規模の経済に重点を置き、リチウムイオン電池に多額の投資を行っています。この競合の急増が、リチウムイオン電池の価格を引き下げています。技術の進歩、製造の最適化、原料コストの低下により、リチウムイオン電池の平均価格は2013年の780米ドル/kWhから2023年には139米ドル/kWhに急落しました。予測では、2025年には約113米ドル/kWh、2030年には約80米ドル/kWhまでさらに下落します。地域別では、中国が最も低い平均電池パック価格を記録し、2023年には126米ドル/kWhとなります。中国国内での激しい競争により、メーカー各社は急成長する電池需要を取り込むために生産量を増やしています。このような電池コストの低下動向は、あらゆる電池の中でリチウム電池を有利な選択肢にする可能性が高いです。

- 歴史的に、リチウムイオン電池は携帯電話やノートパソコンなどの民生用電子機器製品に電力を供給してきました。最近では、ハイブリッド車、あらゆる種類の電池電気自動車(BEV)、再生可能エネルギーにおける電池エネルギー貯蔵システム(BESS)などに採用されています。

- 例えば、グリッド規模のBESSは、ネット・ゼロ・エミッションを達成する上で極めて重要です。短期的なバランシングや送電網の安定性から、長期的なエネルギー貯蔵や停電後の復旧に至るまで、不可欠なサービスを記載しています。国際エネルギー機関(IEA)は、グリッド規模の蓄電池がエネルギー貯蔵の成長の先頭に立つと予測しています。2022年には、年間1,121万kWの系統規模蓄電池増設のうち、中国が42%以上、合計481万kW以上を占めます。2025年までに、主にリチウムイオン電池を使用した3,000万kW以上のBESSを設置する計画で、中国の野心はBESSの好景気の将来を示し、その結果、アジア太平洋における二次電池の需要が急増します。

- 2023年12月、韓国財務省は今後5年間でリチウム電池産業に38兆ウォンを投入する計画を発表しました。韓国は1兆ウォンの振興基金を設立するとともに、736億ウォンを研究開発費に投入し、国内のリチウム電池生産に不可欠な鉱物の埋蔵量を強化します。これらの動きは、電池の再利用とリサイクルのエコシステムを育成する努力と相まって、リチウムイオン電池部門を活性化し、二次電池市場を強化することになります。

- 2024年3月、Panasonic GroupはIndian Oil Corporation Ltd(IOCL)との円筒形リチウムイオン電池生産の合弁事業を発表しました。インドにおける二輪・三輪車とBESSの需要予測を背景としたこのベンチャーは、同地域のリチウムイオン二次電池製造動向の拡大を強調するものです。

- リチウムイオン電池は軽量で、急速充電が可能で、充電サイクルが長く、コストが下がっており、産業が進歩していることから、予測期間中、アジア太平洋の二次電池市場で最も急成長している電池技術になると考えられます。

著しい成長を遂げるインド

- 電気自動車(EV)の普及拡大、民生用電子機器需要の急増、エネルギー貯蔵ソリューションを支持する政府の取り組みに後押しされ、インドの二次電池市場は大きく成長しようとしています。市場拡大にとって極めて重要な二次電池需要の急増は、スマートフォン、ノートパソコン、その他の携帯機器の民生用電子機器セグメントでの普及に大きく起因しています。

- さらに、インド政府が電動モビリティを積極的に推進していることが、特にEVセグメントにおける二次電池の需要を拡大しています。国際エネルギー機関(IEA)のデータはこの動向を浮き彫りにしており、インドにおける電池電気自動車(BEV)の販売台数は2023年に約8万2,000台に急増し、前年比70%増という著しい伸びを示しました。インド政府は2030年に向けて、新たに登録される自家用車の30%、バスの40%、商用車の70%、二輪車と三輪車の80%を電気自動車にするという野心的な目標を掲げており、二次電池、特にリチウムイオン電池の需要は急増する展望です。

- 国内生産を強化し、電気自動車用電池の輸入依存度を下げるため、インド政府は2021年初めに生産連動奨励金(PLI)制度を導入しました。5年間で21億2,000万米ドルという多額の資金を投入するこの制度は、国内で競合ACC電池製造体制を確立することを目的としており、50GWhの生産能力を目標とし、さらに5GWhのニッチACC技術に重点を置いています。PLIスキームでは、1KWhあたりの補助金と、実際の販売による付加価値額の達成率によって決定される生産連動型の補助金が支給されます。2022年までに、Reliance New Energy Solar Limited、Hyundai Global Motors Company Limited、Ola Electric Mobility Private Limited、Rajesh Exports Limitedの著名な4社がこのスキームによる奨励金を獲得しており、国産電池の生産拡大に対する政府のコミットメントが明確に示されています。

- インドのエネルギー貯蔵需要の高まりとサステイナブルソリューションへのシフトに乗じて、国内外の参入企業がインドの二次電池市場に大規模な投資を行っています。例えば、2022年4月、電池セグメントの大手企業であるExide Industriesは、カルナータカ州に約7億1,800万米ドルを投資するリチウムイオン電池製造工場の計画を発表しました。6GWhの生産能力でスタートするこの施設は、2024年までに稼働を開始する予定で、その後数年で12GWhの総合リチウムイオン電池施設に拡大する計画です。

- もうひとつの注目すべき動きとして、電池技術の新興企業であるLog9 Materialsが、2023年4月にベンガルールのJakkurにインド初のリチウムイオン電池製造施設を開設しました。50MWhの生産能力からスタートするLog9は、2025年第1四半期までにセル製造用に1GWh、電池パック製造用に2GWhまで規模を拡大する野心的な計画を持っています。2024年3月、GoodEnough Energyは、2024年10月までにジャンムー・カシミール州でインド初の蓄電池ギガファクトリーの操業を開始する計画を発表しました。最初の7GWhの施設に15億インドルピー(1,807万米ドル)を投資し、2027年までに30億インドルピー(3,700万米ドル)を投じて20GWhに能力を引き上げる計画で、GoodEnoughの施設は産業に大きな影響を与え、年間500万トン以上の二酸化炭素排出量を削減する可能性があります。このギガファクトリーは、再生可能エネルギー容量を2030年までに500GWに増強するというインドの野心的な目標に沿ったもので、2023年の約176GWから大きく飛躍しました。こうした取り組みをさらに強化するため、インド政府は蓄電池プロジェクトの推進に取り組む企業に対し、4億5,200万米ドル相当の奨励金を支給しています。

- 膨大な消費者基盤、政府の支援施策、電池製造の躍進により、インドの二次電池市場は当面力強い成長を遂げると考えられます。

アジア太平洋の二次電池産業概要

アジア太平洋の二次電池市場は細分化されています。同市場の主要企業(順不同)には、Panasonic Corporation、Contemporary Amperex Technology Co.Ltd.、BYD Company Ltd.、GS Yuasa Corporation、Amara Raja Energy &Mobility Ltd.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の普及拡大

- リチウムイオン電池コストの低下

- 抑制要因

- 原料の需給ミスマッチ

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 技術

- 鉛蓄電池

- リチウムイオン

- その他の技術(NiMh、Nicdなど)

- 用途

- 自動車用電池

- 産業用電池(動力用、据置型(テレコム、UPS、エネルギー貯蔵システム(ESS)など))

- ポータブル電池(民生用電子機器製品など)

- その他

- 地域

- インド

- 中国

- 日本

- 韓国

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Panasonic Corporation

- Contemporary Amperex Technology Co. Limited

- BYD Co.Ltd.

- GS Yuasa Corporation

- Samsung SDI Co. Ltd

- LG Chem Ltd.

- Clarios, LLC.

- Amara Raja Energy & Mobility Ltd

- Exide Industries Ltd

- Duracell Inc.

- Saft Groupe SA

- Tianjin Lishen Battery Joint-Stock Co. Ltd.

- Tesla Inc.

- その他の著名な企業一覧(会社名、本社所在地、関連製品とサービス、連絡先など)

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 新しい電池技術と先進電池化学の開発の進展

目次

The Asia-Pacific Rechargeable Battery Market size is estimated at USD 76.31 billion in 2025, and is expected to reach USD 160.83 billion by 2030, at a CAGR of 16.08% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, declining lithium-ion battery prices, increasing adoption of electric vehicles, and the growing renewable energy sector are expected to drive the Asia-Pacific rechargeable battery market during the forecast period.

- On the other hand, the demand-supply mismatch of raw materials is expected to hinder the market's growth during the forecast period.

- Nevertheless, the growing progress in developing new battery technologies and advanced battery chemistries will likely create vast opportunities for the Asia-Pacific rechargeable battery market.

- Among the countries in the region, India is expected to have significant growth due to the rise in the adoption of electric vehicles, consumer electronics, and energy storage systems in renewable projects.

Asia-Pacific Rechargeable Battery Market Trends

Lithium-ion Battery to be the Fastest Growing

- Among various battery technologies, lithium-ion batteries (LIBs) are poised to dominate the rechargeable battery market, showcasing rapid growth during the forecast period. Their rising popularity over other battery types can be attributed to their superior capacity-to-weight ratio, extended shelf life, reduced maintenance needs, and plummeting prices.

- Li-ion batteries boast several technical advantages over traditional lead-acid batteries. While lead-acid batteries typically offer 400-500 cycles, rechargeable Li-ion batteries can exceed 5,000 cycles. Moreover, Li-ion batteries demand less frequent maintenance and replacements. They also maintain consistent voltage throughout their discharge cycle, ensuring prolonged efficiency for connected electrical components.

- Major players in the Asia-Pacific region are heavily investing in lithium-ion batteries, focusing on R&D and economies of scale. This surge in competition has driven down lithium-ion battery prices. Thanks to technological advancements, manufacturing optimizations, and falling raw material costs, the average price of lithium-ion batteries plummeted from USD 780/kWh in 2013 to USD 139/kWh in 2023. Projections suggest a further drop to around USD 113/kWh by 2025 and USD 80/kWh by 2030. Regionally, China recorded the lowest average battery pack prices at USD 126/kWh in 2023. Intense local competition in China saw manufacturers ramping up production to capture the burgeoning battery demand. Such declining trends in battery costs are likely to make it a lucrative choice among all batteries.

- Historically, lithium-ion batteries powered consumer electronics like mobile phones and laptops. Recently, they've been adapted for hybrids, the full range of battery electric vehicles (BEVs), and battery energy storage systems (BESS) in renewable energy, largely due to their reduced environmental impact.

- Grid-scale BESS, for instance, is pivotal in achieving Net Zero Emissions. They provide essential services, from short-term balancing and grid stability to long-term energy storage and post-blackout restoration. The International Energy Agency (IEA) forecasts that grid-scale battery energy storage will spearhead energy storage growth. In 2022, China contributed over 42% of the 11.21 GW annual grid-scale battery storage additions, totaling over 4.81 GW. With plans to install over 30 GW of BESS by 2025, predominantly using lithium-ion batteries, China's ambitions signal a booming future for BESS and, consequently, a surging demand for rechargeable batteries in the Asia-Pacific.

- In December 2023, South Korea's Ministry of Finance unveiled a plan to inject KRW 38 trillion into the lithium battery industry over the next five years, with formal implementation set for 2024. Alongside establishing a KRW 1 trillion promotion fund, South Korea is channeling KRW 73.6 billion into R&D and bolstering reserves of critical minerals for domestic lithium battery production. These moves, coupled with efforts to foster a battery reuse and recycling ecosystem, are set to invigorate the lithium-ion battery sector and bolster the rechargeable battery market.

- March 2024 saw Panasonic Group announce a joint venture with Indian Oil Corporation Ltd (IOCL) for cylindrical lithium-ion battery production. This venture, driven by anticipated demand for two and three-wheel vehicles and BESS in India, underscores the region's growing lithium-ion battery manufacturing trend.

- Given their lightweight nature, rapid charging capabilities, extended charging cycles, declining costs, and industry advancements, lithium-ion batteries are set to emerge as the fastest-growing battery technology in the Asia-Pacific rechargeable battery market during the forecast period.

India to Witness Significant Growth

- Driven by the rising adoption of electric vehicles (EVs), surging demand for consumer electronics, and government initiatives championing energy storage solutions, the Indian rechargeable battery market is on the brink of significant growth. The surge in demand for rechargeable batteries, pivotal for the expansion of the market, is largely attributed to the widespread adoption of smartphones, laptops, and other portable devices in the consumer electronics sector.

- Moreover, the Indian Government's aggressive push towards electric mobility is amplifying the demand for rechargeable batteries, especially in the EV segment. Data from the International Energy Agency (IEA) highlights this trend, noting that battery electric vehicle (BEV) sales in India soared to approximately 82,000 units in 2023, marking a remarkable 70% uptick from the previous year. With the Indian Government setting ambitious targets for 2030 - envisioning 30% of newly registered private cars, 40% of buses, 70% of commercial cars, and a staggering 80% of two-wheelers and three-wheelers to be electric - the demand for rechargeable batteries, particularly lithium-ion variants, is set to surge.

- In a bid to bolster local manufacturing and reduce reliance on imported Advance Chemistry Cell (ACC) batteries for electric vehicles, the Indian Government rolled out a Production Linked Incentive (PLI) Scheme in early 2021. With a substantial outlay of USD 2.12 billion spread over five years, the scheme aims to establish a competitive ACC battery manufacturing setup in the country, targeting a capacity of 50 GWh, with an additional focus on 5 GWh of niche ACC technologies. The PLI Scheme offers a production-linked subsidy, determined by the applicable subsidy per KWh and the achieved percentage of value addition based on actual sales. By 2022, four prominent companies - Reliance New Energy Solar Limited, Hyundai Global Motors Company Limited, Ola Electric Mobility Private Limited, and Rajesh Exports Limited - secured incentives under this scheme, underscoring the government's commitment to boosting local battery cell production.

- Capitalizing on India's growing energy storage demands and its shift towards sustainable solutions, both local and international players are making significant investments in the Indian rechargeable battery market. For instance, in April 2022, Exide Industries, a major player in the battery sector, unveiled plans for a lithium-ion cell manufacturing plant in Karnataka, with an investment of approximately USD 718 million. The facility, starting with a 6 GWh capacity, is set to become operational by 2024, with plans to expand to a 12 GWh integrated lithium-ion battery facility in subsequent years.

- In another notable move, battery technology startup Log9 Materials inaugurated India's inaugural lithium-ion cell manufacturing facility in Jakkur, Bengaluru, in April 2023. Starting with a capacity of 50 MWh, Log9 has ambitious plans to scale up to 1 GWh for cell manufacturing and 2 GWh for battery pack manufacturing by Q1 2025. March 2024 saw GoodEnough Energy announcing its plans to commence operations at India's first battery energy storage gigafactory in Jammu and Kashmir by October 2024. With an investment of INR 1.5 billion (USD 18.07 million) for the initial 7 GWh facility and a projected spend of INR 3 billion (USD 37 million) by 2027 to elevate capacity to 20 GWh, GoodEnough's facility aims to significantly impact the industry, potentially cutting over 5 million tons of carbon emissions annually. This gigafactory aligns with India's ambitious goal to ramp up its renewable energy capacity to 500 GW by 2030, a significant leap from around 176 GW in 2023. To further bolster these efforts, the Indian government is extending incentives worth USD 452 million to companies engaged in promoting battery storage projects.

- With a vast consumer base, supportive governmental policies, and strides in battery manufacturing, the Indian rechargeable battery market is set for robust growth in the foreseeable future.

Asia-Pacific Rechargeable Battery Industry Overview

The Asia-Pacific rechargeable battery market is fragmented. Some of the key players in the market (not in any particular order) include Panasonic Corporation, Contemporary Amperex Technology Co. Limited, BYD Company Ltd., GS Yuasa Corporation, and Amara Raja Energy & Mobility Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles

- 4.5.1.2 Declining Lithium-ion Battery Cost

- 4.5.2 Restraints

- 4.5.2.1 Demand-Supply Mismatch of Raw Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lead-Acid

- 5.1.2 Lithium-Ion

- 5.1.3 Other Technologies (NiMh, Nicd, etc.)

- 5.2 Application

- 5.2.1 Automotive Batteries

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.2.3 Portable Batteries (Consumer Electronics, etc.)

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 India

- 5.3.2 China

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Thailand

- 5.3.6 Indonesia

- 5.3.7 Vietnam

- 5.3.8 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Panasonic Corporation

- 6.3.2 Contemporary Amperex Technology Co. Limited

- 6.3.3 BYD Co.Ltd.

- 6.3.4 GS Yuasa Corporation

- 6.3.5 Samsung SDI Co. Ltd

- 6.3.6 LG Chem Ltd.

- 6.3.7 Clarios, LLC.

- 6.3.8 Amara Raja Energy & Mobility Ltd

- 6.3.9 Exide Industries Ltd

- 6.3.10 Duracell Inc.

- 6.3.11 Saft Groupe SA

- 6.3.12 Tianjin Lishen Battery Joint-Stock Co. Ltd. Source: https://www.mordorintelligence.com/industry-reports/southeast-asia-battery-market

- 6.3.13 Tesla Inc.

- 6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Progress in Developing New Battery Technologies and Advanced Battery Chemistries

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日