中東の二次電池:市場シェア分析、産業動向、成長予測(2025~2030年)

Middle East Rechargeable Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636565

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

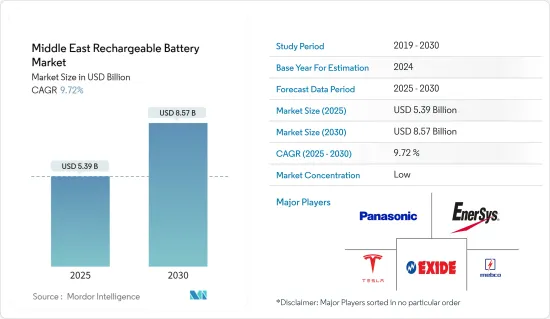

中東の二次電池市場規模は2025年に53億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは9.72%で、2030年には85億7,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、リチウムイオン電池価格の下落、電気自動車の普及拡大、再生可能エネルギーセグメントの拡大が、予測期間中の中東の二次電池市場を牽引すると予想されます。

- 一方、原料の需給ミスマッチが予測期間中の市場成長の妨げになると予想されます。

- 新しい電池技術や先進的電池化学品の開発が進み、電池リサイクルの必要性が高まっていることから、中東の二次電池市場には大きなビジネス機会が生まれる可能性が高いです。

- アラブ首長国連邦は、民生用電子機器部門の拡大と再生可能エネルギー設備の迅速な導入により、予測期間中に大きな成長を達成する可能性があり、注目すべき成長を経験すると予測されています。

中東の二次電池市場動向

リチウムイオン電池が急成長

- 様々な電池技術の中で、リチウムイオン電池(LIB)が中東の二次電池市場で予測期間中に最も急成長するセグメントとして浮上する展望です。リチウムイオン電池は、その優れた容量対重量比を主要理由として、他のタイプの電池を凌駕する勢いで普及しています。リチウムイオン電池の採用は、最小限のメンテナンスで性能が向上し、保存可能期間が長く、価格が一貫して低下しているなどの利点によってさらに促進されています。

- リチウムイオン電池は、従来の技術、特に鉛蓄電池と比較して、いくつかの技術的利点を誇っています。充電式リチウムイオン電池は平均して5,000回以上のサイクルを提供し、一般的な鉛蓄電池のサイクルが400~500回であるのとは対照的です。さらに、リチウムイオン電池はメンテナンスや交換の頻度が少ないです。また、放電サイクルを通じて電圧を維持するため、電気部品の効率が向上し、長持ちします。

- 近年、産業の大手企業は投資を拡大し、規模の経済の達成と研究開発活動の強化に注力しています。このような競合の急増により、リチウムイオン電池の価格は著しく低下しています。技術革新、製造の進歩、原料コストの低下により、リチウムイオン電池の数量加重平均価格は2013年の780米ドル/kWhから2023年には139米ドル/kWhに急落しました。予測によると、2025年には113米ドル/kWh程度までさらに下落し、2030年には80米ドル/kWhに達します。このような電池コストの低下動向は、すべての電池の中でリチウム電池を有利な選択肢にする可能性が高いです。

- 歴史的に、リチウムイオン電池は携帯電話やノートパソコンなどの民生用電子機器が主要用途でした。しかし、その役割は大幅に拡大しています。現在では、ハイブリッド車、電池電気自動車(BEV)全般、再生可能エネルギーセグメントの電池エネルギー貯蔵システム(BESS)の電源として好まれています。

- 中東のリチウムイオン電池製造産業はまだ初期段階にあり、中国、米国、欧州といった世界のトップランナーに後れを取っているが、このセグメントを強化するための協調的な取り組みが行われています。特にアラブ首長国連邦とサウジアラビアは、電池製造と関連技術で躍進しています。こうした動きは、経済の多様化を図り、再生可能エネルギーの目標を支援し、急増する電気自動車の需要に対応することを目的としています。

- 例えば、Titan Lithiumは2024年2月、Khalifa Economic Zones Abu Dhabi(KEZAD)Groupと提携し、最先端のリチウム加工施設の計画を発表しました。KEZAD Al Mamourahの29万平方メートルに及ぶこの50億AED(約13億5,000万米ドル)のベンチャーは、リチウムイオン電池とEVセグメントに不可欠な電池用炭酸リチウムと水酸化リチウムを生産する予定です。

- 同様に、サウジアラビアは世界の二次電池セグメントで大きく前進しています。2023年6月、Obeikan Investment Groupはオーストラリアの新興企業European Lithiumと提携し、水酸化リチウム精製所を設立しました。翌月には、サウジの国営鉱山会社Ma'adenと米国のIvanhoe Electricが、rabian Shieldの4万8,500平方キロメートルでリチウムやその他のレアメタルを探鉱する権利を獲得しました。

- 2023年9月、サウジの投資会社Energy Capital Groupは、米国のハイテク新興企業Pure Lithiumと協力し、油田かん水から供給されるリチウムを使用した電池の革新に取り組みました。5,000万米ドルの初期投資で、このイニシアチブはリチウムイオン電池用金属の急増する需要に応えることを目的としています。さらに、ERGの世界の電池アライアンスへの加盟は、リチウムイオン電池のサステイナブル世界のサプライチェーンへのコミットメントを強調するものです。このようなイニシアチブは、この地域のリチウムイオン電池産業にとって有望な軌道を示すものです。

- リチウムイオン電池は軽量で急速充電が可能であり、充電サイクルが長く、コストが下がっていることから、予測期間中は中東の二次電池市場を独占することになると考えられます。

アラブ首長国連邦が著しい成長を遂げる

- 予測期間中、アラブ首長国連邦の二次電池市場は大幅な成長を遂げ、同国を地域のリーダーとして位置付けています。この勢いは、急速な工業化、再生可能エネルギーに対する政府の支援、急成長する電気自動車(EV)セクター、技術の進歩、アラブ首長国連邦のこの地域における戦略的な経済姿勢によって後押しされています。これらの要素が相まって、二次電池の採用と技術革新に適した環境が整っています。

- アラブ首長国連邦の急速な産業拡大により、信頼性の高いエネルギー貯蔵ソリューションへの需要が高まっており、さまざまなセグメントで二次電池が広く受け入れられています。さらに、持続可能性と再生可能エネルギーに対する国の取り組みは、極めて重要な役割を果たすことになります。二酸化炭素排出量を削減し、エネルギー・ポートフォリオにおける再生可能エネルギーの役割を増大させるという野心を持つアラブ首長国連邦は、クリーンエネルギー技術を支持する政府のイニシアチブによって支えられています。これには太陽光発電の重視も含まれ、効率的な電池エネルギー貯蔵システム(BESS)の需要を高めています。アラブ首長国連邦は野心的なエネルギー目標を掲げており、再生可能エネルギー容量を2023年の約605万kWから、2030年には現在の3倍以上となる1,420万kWに拡大することを目指しています。このような飛躍は、BESSに対する大きな需要を生み出すと予想されます。

- 近年、アラブ首長国連邦では電気自動車(EV)の急速な普及が見られます。国際エネルギー機関(IEA)のデータはこの動向を浮き彫りにしており、電池電気自動車(BEV)の販売台数は2023年に約2万3,000台に急増し、前年の1万5,000台から53%増という顕著な伸びを示しました。このようなEV普及の高まりは、二次電池市場を後押しすることになると考えられます。

- さらにアラブ首長国連邦は、2050年までに電気自動車とハイブリッド車が道路交通の50%を占めるようになることを想定しています。EVインフラへの多額の投資と、気候変動と闘い化石燃料への依存を軽減する戦略としてのEV導入の推進により、高容量で耐久性のある二次電池の需要が高まっている

- この電池需要の急増に伴い、アラブ首長国連邦は電池のリサイクルで躍進しています。その証拠に、インドを拠点とするLOHUMクリーンテックは2023年12月、アラブ首長国連邦市場への進出を発表しました。アラブ首長国連邦のエネルギーインフラ省と中東における持続可能性とデジタル化のリーダーである中東との協力により、LOHUMはアラブ首長国連邦初のEV電池リサイクル工場を設立する予定です。このイニシアチブは、アラブ首長国連邦のCOP28アジェンダ、2050年までのネット・ゼロ戦略イニシアチブ、循環経済施策に沿ったもので、排出ガスのないモビリティを提唱しています。

- この野心的なプロジェクトは、リチウム電池の再生とリサイクルに特化した8万平方フィートの広大な施設を特徴とします。年間3,000トンのリチウムイオン電池をリサイクルし、15MWhをエネルギー貯蔵システム(ESS)に再利用する能力を持つこの施設は、予想されるEV電池管理ニーズの80%以上を満たすと見込まれています。

- 電池技術の進歩、特にソリッド・ステート電池の出現は、効率性、安全性、消費者と企業の両方に対する二次電池の総合的な魅力を増幅させています。この動向を浮き彫りにしているのが、米国を拠点とする著名な電池メーカーStatevoltが2024年4月に発表した、2026年までにアラブ首長国連邦で固体電池セルを生産するという計画です。同社は、ラスアルハイマに32億米ドルの巨大なギガ工場を建設し、年間生産量40ギガワット時(GWh)という驚異的な目標を掲げています。この戦略的な動きは、中東・アフリカ、インドなどの地域を視野に入れ、電池ストレージと電動モビリティの急成長する輸出市場に参入することを目的としています。

- このような力学から、アラブ首長国連邦は予測期間中に二次電池市場が顕著に急増することが予想されます。

中東の二次電池産業概要

中東の二次電池市場は細分化されています。同市場の主要企業(順不同)には、Tesla Inc.、Exide Industries Ltd.、Middle East Battery Company(MEBCO)、EnerSys、Panasonic Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の普及拡大

- リチウムイオン電池コストの低下

- 抑制要因

- 原料の需給ミスマッチ

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 技術

- 鉛蓄電池

- リチウムイオン

- その他の技術(NiMh、Nicdなど)

- 用途

- 自動車用電池

- 産業用電池(動力用、据置型(テレコム、UPS、エネルギー貯蔵システム(ESS)など))

- ポータブル電池(民生用電子機器製品など)

- その他

- 地域

- アラブ首長国連邦

- サウジアラビア

- カタール

- その他の中東地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Panasonic Corporation

- Tesla Inc.

- Saft Groupe SA

- Middle East Battery Company(MEBCO)

- EnerSys

- Exide Industries Ltd

- FIAMM Energy Technology SpA

- Statevolt

- Statron Ltd

- Amara Raja Energy & Mobility Limited.

- C&D Technologies Inc.

- その他の著名な企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- 新しい電池技術と先進電池化学の開発の進展

目次

Product Code: 50004071

The Middle East Rechargeable Battery Market size is estimated at USD 5.39 billion in 2025, and is expected to reach USD 8.57 billion by 2030, at a CAGR of 9.72% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, declining lithium-ion battery prices, increasing adoption of electric vehicles, and the growing renewable energy sector are expected to drive the Middle East rechargeable battery market during the forecast period.

- On the other hand, the demand-supply mismatch of raw materials is expected to hinder the market's growth during the forecast period.

- Nevertheless, the growing progress in developing new battery technologies and advanced battery chemistries and the need for battery recycling will likely create vast opportunities for the Middle East rechargeable battery market.

- The United Arab Emirates is projected to experience notable growth, potentially achieving significant growth during the forecast period, driven by its expanding consumer electronics sector and swift adoption of renewable energy installations.

Middle East Rechargeable Battery Market Trends

Lithium-ion Battery to be the Fastest Growing

- Among various battery technologies, lithium-ion batteries (LIBs) are poised to emerge as the fastest-growing segment in the Middle East's rechargeable battery market during the forecast period. LIBs are outpacing other battery types in popularity, primarily due to their superior capacity-to-weight ratio. Their adoption is further fueled by advantages such as extended performance with minimal maintenance, a longer shelf life, and a consistent decline in prices.

- Li-ion batteries boast several technical advantages over traditional technologies, notably lead-acid batteries. On average, rechargeable Li-ion batteries offer over 5,000 cycles, a stark contrast to the 400-500 cycles typical of lead-acid batteries. Moreover, Li-ion batteries demand less frequent maintenance and replacement. They also sustain their voltage throughout the discharge cycle, ensuring enhanced and prolonged efficiency of electrical components.

- In recent years, major industry players have ramped up investments, focusing on achieving economies of scale and enhancing R&D activities. This surge in competition has led to a notable drop in lithium-ion battery prices. Due to technological innovations, manufacturing advancements, and a decrease in raw material costs, the volume-weighted average price of lithium-ion batteries plummeted from USD 780/kWh in 2013 to USD 139/kWh in 2023. Projections suggest it will further dip to around USD 113/kWh in 2025 and reach USD 80/kWh by 2030. Such declining trends in battery costs are likely to make it a lucrative choice among all batteries.

- Historically, lithium-ion batteries found their primary application in consumer electronics like mobile phones and laptops. However, their role has expanded significantly. Today, they are the preferred power source for hybrids, the entire range of battery electric vehicles (BEVs), and battery energy storage systems (BESS) in the renewable energy sector.

- While the Middle East's lithium-ion battery manufacturing industry is still in its nascent stages, trailing behind global frontrunners like China, the United States, and Europe, there's a concerted effort to bolster this sector. Countries, especially the United Arab Emirates and Saudi Arabia, are making strides in battery manufacturing and related technologies. These moves aim to diversify their economies, support renewable energy goals, and address the surging demand for electric vehicles.

- For instance, in February 2024, Titan Lithium, in partnership with Khalifa Economic Zones Abu Dhabi (KEZAD) Group, unveiled plans for a state-of-the-art lithium processing facility. This AED 5 billion (~USD 1.35 billion) venture, spanning 290,000 square meters in KEZAD Al Mamourah, is set to produce battery-grade lithium carbonate and hydroxide, crucial for the lithium-ion battery and EV sectors.

- Similarly, Saudi Arabia is making significant strides in the global rechargeable battery arena. In June 2023, Obeikan Investment Group teamed up with Australian startup European Lithium to establish a lithium hydroxide refinery. The following month, Saudi state mining company Ma'aden and US-based Ivanhoe Electric secured rights to explore 48,500 sq km of the Arabian Shield for lithium and other rare metals.

- In September 2023, Saudi investment firm Energy Capital Group collaborated with US tech startup Pure Lithium to innovate batteries using lithium sourced from oilfield brines. With an initial investment of USD 50 million, this initiative aims to cater to the burgeoning demand for lithium-ion battery metals. Additionally, ERG's membership in the Global Battery Alliance underscores its commitment to a sustainable global supply chain for lithium-ion batteries. Such initiatives signal a promising trajectory for the region's lithium-ion battery industry.

- Given their lightweight nature, rapid charging capabilities, extended charging cycles, and decreasing costs, lithium-ion batteries are set to dominate the Middle East's rechargeable battery market during the forecast period.

United Arab Emirates to Witness Significant Growth

- During the forecast period, the rechargeable battery market in the United Arab Emirates (UAE) is poised for substantial growth, positioning the nation as a regional leader. This momentum is fueled by rapid industrialization, government backing for renewable energy, a burgeoning electric vehicle (EV) sector, technological strides, and the UAE's strategic economic stance in the region. Collectively, these elements foster an environment ripe for the adoption and innovation of rechargeable batteries.

- The UAE's swift industrial expansion is driving a heightened demand for dependable energy storage solutions, leading to a broader acceptance of rechargeable batteries across multiple sectors. Moreover, the nation's dedication to sustainability and renewable energy is set to play a pivotal role. With ambitions to curtail its carbon footprint and amplify the role of renewables in its energy portfolio, the UAE is bolstered by governmental initiatives championing clean energy technologies. This includes a pronounced emphasis on solar power, which subsequently elevates the demand for efficient battery energy storage systems (BESS). Illustratively, the UAE has set ambitious energy targets, aiming to escalate its renewable energy capacity from approximately 6.05 GW in 2023 to a projected 14.2 GW by 2030, more than tripling its current capacity. Such a leap is anticipated to generate a substantial demand for BESS.

- In recent years, the UAE has witnessed a swift embrace of electric vehicles (EVs). Data from the International Energy Agency (IEA) highlights this trend, noting that battery electric vehicle (BEV) sales surged to about 23,000 units in 2023, marking a notable 53% increase from the previous year's 15,000 units. This rising tide of EV adoption is poised to bolster the rechargeable battery market.

- Moreover, the UAE envisions electric and hybrid vehicles constituting 50% of its road traffic by 2050. With significant investments in EV infrastructure and a push for EV adoption as a strategy to combat climate change and lessen fossil fuel dependence, the demand for high-capacity, durable rechargeable batteries is escalating.

- In tandem with this surging battery demand, the UAE is making strides in battery recycling. A testament to this is the December 2023 announcement by India-based LOHUM Cleantech, marking its foray into the UAE market. Through a collaboration with the UAE's Ministry of Energy & Infrastructure and BEEAH, a leader in sustainability and digitalization in the Middle East, LOHUM is set to establish the UAE's inaugural EV Battery Recycling plant. This initiative aligns with the UAE's COP28 agenda, its Net Zero by 2050 Strategic Initiative, and its Circular Economy Policy, all while championing emissions-free mobility.

- The ambitious project will feature an expansive 80,000 sq ft facility dedicated to refurbishing and recycling Lithium batteries. With an annual capacity to recycle 3,000 tons of Lithium-ion batteries and repurpose 15MWh into Energy Storage Systems (ESS), the facility is projected to meet over 80% of the anticipated EV battery management needs.

- Advancements in battery technology, notably the emergence of solid-state batteries, are amplifying the efficiency, safety, and overall appeal of rechargeable batteries to both consumers and businesses. Highlighting this trend, US-based Statevolt, a prominent battery manufacturer, unveiled plans in April 2024 to produce solid-state battery cells in the UAE by 2026. The company is laying the groundwork for a monumental USD 3.2 billion gigafactory in Ras Al Khaimah, targeting an impressive annual output of 40 gigawatt-hours (GWh). This strategic move aims to penetrate the burgeoning export markets for battery storage and electric mobility, eyeing regions like the Middle East, Africa, and India.

- Given these dynamics, the United Arab Emirates (UAE) is set to experience a pronounced surge in its rechargeable battery market during the forecast period.

Middle East Rechargeable Battery Industry Overview

The Middle East rechargeable battery market is semi-fragmented. Some of the key players in the market (not in any particular order) include Tesla Inc., Exide Industries Ltd., Middle East Battery Company (MEBCO), EnerSys and Panasonic Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles

- 4.5.1.2 Declining Lithium-ion Battery Cost

- 4.5.2 Restraints

- 4.5.2.1 Demand-Supply Mismatch of Raw Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lead-Acid

- 5.1.2 Lithium-Ion

- 5.1.3 Other Technologies (NiMh, Nicd, etc.)

- 5.2 Application

- 5.2.1 Automotive Batteries

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.2.3 Portable Batteries (Consumer Electronics, etc.)

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 United Arab Emirates

- 5.3.2 Saudi Arabia

- 5.3.3 Qatar

- 5.3.4 Rest of Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Panasonic Corporation

- 6.3.2 Tesla Inc.

- 6.3.3 Saft Groupe SA

- 6.3.4 Middle East Battery Company (MEBCO)

- 6.3.5 EnerSys

- 6.3.6 Exide Industries Ltd

- 6.3.7 FIAMM Energy Technology SpA

- 6.3.8 Statevolt

- 6.3.9 Statron Ltd

- 6.3.10 Amara Raja Energy & Mobility Limited.

- 6.3.11 C&D Technologies Inc.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Progress in Developing New Battery Technologies and Advanced Battery Chemistries

中東の二次電池:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日