|

市場調査レポート

商品コード

1636533

欧州の二次電池:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Europe Rechargeable Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の二次電池:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

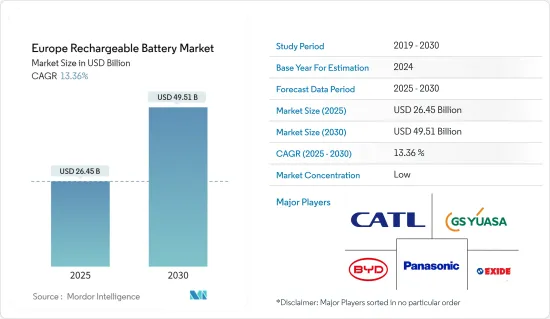

欧州の二次電池市場規模は2025年に264億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは13.36%で、2030年には495億1,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、電気自動車需要の増加や再生可能エネルギーの採用拡大といった要因が、予測期間中の欧州の二次電池市場の最も大きな促進要因の1つになると予想されます。

- 逆に、電池調達におけるサプライチェーンの制約が大きいことが、予測期間中の欧州の二次電池市場を脅かします。

- しかし、電池化学の開発における継続的な進歩は、より効率的な二次電池を生み出し、市場に多くの将来機会をもたらしています。

- ドイツが市場をリードする態勢を整えており、急成長している民生用電子機器セグメントと迅速な再生可能エネルギー導入が原動力となって、予測期間中に最も高い成長を達成すると予測されています。

欧州の二次電池市場動向

自動車が大きく成長

- 近年、欧州連合(EU)は、温室効果ガスの排出を抑制し、よりクリーンなエネルギー技術を地域全体に普及させることを目的とした厳しい措置を実施しています。これらのイニシアチブはまた、運輸部門における電動化の推進を強調しています。EU内の各国もこうした取り組みを反映し、電気自動車(EV)の導入を促進するための税制優遇措置や補助金を提供する施策を展開しています。その結果、電気自動車の主要部品である二次電池の需要急増が予想されます。

- さらに、環境の持続可能性をめぐる意識の高まりと化石燃料依存からの脱却の動きが、消費者の嗜好を環境に優しい輸送へとシフトさせています。直接排出ガスがゼロである電気自動車は、従来の内燃エンジン車に代わるサステイナブル選択肢と見なされるようになっています。このような消費者のEV志向の高まりは、欧州における二次電池市場の成長を促進するものと考えられます。

- 国際エネルギー機関(IEA)のデータによると、欧州全域で電気自動車の販売台数が一貫して増加しています。2023年の販売台数は約220万台に達し、2021年の160万台から顕著に増加し、成長率は37.5%を超えます。このような勢いは、電気自動車の急速な普及を裏付けるものであり、二次電池市場をさらに活性化させる。

- さらに、電池技術における継続的な技術進歩により、電気自動車のエネルギー密度の向上、航続距離の延長、充電時間の短縮といった機能強化がもたらされています。こうした進歩は、特に新しい電池製造施設の設立など、欧州全域での投資の増加に拍車をかけています。

- 例えば、2023年7月、インドの著名な自動車メーカーであるTata Motorsは、英国に年間セル生産能力40GWの電気自動車用電池工場を建設する計画を発表しました。この施設は、電池生産を現地化することで国内自動車産業を強化し、長期的な持続可能性を確保する構えです。タタ・モーターズと政府関係者はともに、この工場に40億英ポンドという多額の投資を行うことを明らかにしました。

- こうした開発を踏まえると、自動車産業の電気自動車部門は今後数年で大きく成長することになります。

市場を独占するドイツ

- ドイツは、産業・製造の中心地としての地位と強力な自動車産業によって、欧州の二次電池市場をリードする態勢を整えています。この産業は革新的な電気自動車に軸足を移しつつあり、世界のエネルギー転換と歩調を合わせています。欧州の電気自動車への意欲が高まるにつれ、ドイツの自動車メーカーは二次電池の需要を大幅に押し上げることになり、このセグメントでのドイツのリーダーシップは揺るぎないものとなります。

- さらに、ドイツは再生可能エネルギー発電の導入に力を入れているため、二次電池のニーズが高まっています。再生可能エネルギー源の断続的な性質を考慮すると、エネルギー貯蔵はそのポテンシャルを最大限に活用するために不可欠です。電池エネルギー貯蔵システムの採用が増加していることから、ドイツの再生可能エネルギー部門は二次電池の需要をさらに促進する態勢を整えています。

- 国際再生可能エネルギー機関のデータは、ドイツの再生可能エネルギーの迅速な受け入れを強調しています。国の再生可能エネルギー設備容量は、2022~2023年にかけて約12%急増し、5年間の一貫した平均成長率5.6%以上を上回りました。

- さらに、ドイツは政府と民間企業の両方からの多額の投資により、電池の研究開発におけるリーダー的存在となっています。国内の研究機関や企業は、エネルギー密度、充電速度、全体的な効率の向上に重点を置き、電池技術の限界に課題しています。

- その一例として、2024年5月、ドイツの著名な電池サプライヤーであるVartaは、工業規模のナトリウムイオン二次電池技術の開拓を目的としたプロジェクトを開始しました。3年間で750万ユーロ(808万米ドル)を投資し、セル化学を工業規模に引き上げることを目指します。目標は、電気自動車や据置型蓄電池に適した丸型セルを限定生産することです。このプロジェクトは2027年半ばまでに完了する予定で、技術的、経済的、生態学的な徹底的な評価が行われます。

- こうした新興国市場の開拓を考えると、予測期間中、欧州の二次電池市場におけるドイツの優位は確実と考えられます。

欧州の二次電池産業概要

欧州の二次電池市場は細分化されています。この市場の主要企業(順不同)には、BYD、Contemporary Amperex Technology、Exide Industries、Panasonic Corporation、GS Yuasa Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車需要の拡大

- 再生可能エネルギーの普及拡大

- 抑制要因

- サプライチェーンの制約

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 電池タイプ

- 鉛酸

- リチウムイオン

- その他(NiMh、NiCdなど)

- 用途

- 自動車用

- 産業用電池

- 携帯用電池

- その他

- 地域

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- ノルディック

- ロシア

- トルコ

- その他の欧州

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- BYD Co. Ltd.

- LG Chem Ltd.

- Contemporary Amperex Technology Co Ltd

- Exide Industries

- Saft Groupe SA

- Samsung SDI Co., Ltd.

- Murata Manufacturing Co., Ltd.

- Panasonic Corporation

- GS Yuasa Corporation

- Tesla, Inc.

- その他の著名な企業一覧

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 新しい電池化学の技術的進歩

目次

Product Code: 50003928

The Europe Rechargeable Battery Market size is estimated at USD 26.45 billion in 2025, and is expected to reach USD 49.51 billion by 2030, at a CAGR of 13.36% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as increasing demand for electric vehicles and growing adoption of renewable energy are expected to be among the most significant drivers for the Europe rechargeable battery market during the forecast period.

- Conversely, high supply chain constraints in battery procurement threaten the European rechargeable battery market during the forecast period.

- However, ongoing advancements in battery chemistry development have resulted in more efficient rechargeable batteries, presenting numerous future opportunities for the market.

- Germany is poised to lead the market and is projected to achieve the highest growth during the forecast period, driven by a burgeoning consumer electronics segment and swift renewable energy installations.

Europe Rechargeable Battery Market Trends

Automobile to Witness Significant Growth

- In recent years, the European Union has implemented stringent measures aimed at curbing greenhouse gas emissions and promoting cleaner energy technologies across the region. These initiatives also emphasize a heightened electrification push within the transportation sector. Individual countries within the EU have mirrored these efforts, rolling out policies that offer tax incentives and subsidies to bolster the adoption of electric vehicle (EV). Consequently, this has led to an anticipated surge in demand for rechargeable batteries, a pivotal component of electric vehicles.

- Additionally, heightened awareness surrounding environmental sustainability and a collective move away from fossil fuel reliance has shifted consumer preferences towards eco-friendly transportation. Electric vehicles, with their zero direct emissions, are increasingly viewed as a sustainable alternative to traditional internal combustion engine vehicles. This rising consumer inclination towards EVs is poised to propel the rechargeable battery market's growth in Europe.

- Data from the International Energy Agency highlights a consistent uptick in electric vehicle sales across Europe. In 2023, sales reached approximately 2.2 million units, a notable increase from 1.6 million units in 2021, marking a growth rate exceeding 37.5%. Such momentum underscores the burgeoning traction of electric vehicles, further fueling the rechargeable battery market.

- Moreover, ongoing technological advancements in battery technology have ushered in enhancements like improved energy density, extended ranges, and expedited charging times for electric vehicles. These advancements have catalyzed increased investments across Europe, particularly in establishing new battery manufacturing facilities.

- For example, in July 2023, Tata Motors, a prominent Indian automobile manufacturer, unveiled plans for a 40 GW annual cell production capacity electric vehicle battery plant in Britain. This facility is poised to fortify the domestic car industry by localizing battery production, ensuring long-term sustainability. Both Tata Motors and government officials disclosed a hefty investment of GBP 4 Billion for the factory.

- Given these developments, the electric vehicle segment of the automobile industry is set for substantial growth in the coming years.

Germany to Dominate the Market

- Germany is poised to lead the European rechargeable battery market, bolstered by its status as an industrial and manufacturing hub and a strong automobile industry. This industry is pivoting towards innovative electric vehicles, aligning with the global energy transition. As Europe's appetite for electric vehicles grows, German automakers are set to significantly boost the demand for rechargeable batteries, solidifying Germany's leadership in this segment.

- Furthermore, Germany's dedication to incorporating renewable energy into its power generation amplifies its need for rechargeable batteries. Given the intermittent nature of renewable sources, energy storage becomes crucial to harness their full potential. With the rising adoption of battery energy storage systems, Germany's renewable energy sector is poised to further fuel the demand for rechargeable batteries.

- Data from the International Renewable Energy Agency highlights Germany's swift embrace of renewables: the nation's installed renewable energy capacity surged by about 12% from 2022 to 2023, outpacing a consistent five-year average growth rate of over 5.6%.

- Moreover, Germany is a leader in battery R&D, due to substantial investments from both government and private entities. Domestic research institutions and companies are pushing the envelope in battery technologies, emphasizing enhancements in energy density, charging speed, and overall efficiency.

- As an illustration, in May 2024, Varta, a prominent German battery supplier, launched a project aimed at pioneering industrial-scale rechargeable sodium-ion battery technology. With a three-year investment of EUR 7.5 million (USD 8.08 million), the initiative seeks to elevate cell chemistry to an industrial scale. The goal is to produce a limited batch of round cells, tailored for electric vehicles and stationary storage. Set to wrap up by mid-2027, the project will undergo a thorough technical, economic, and ecological evaluation.

- Given these developments, Germany's dominance in the European rechargeable battery market appears assured during the forecast period.

Europe Rechargeable Battery Industry Overview

The Europe Rechargeable Battery Market is fragmented. Some of the key players in this market (in no particular order) are BYD Co. Ltd., Contemporary Amperex Technology Co. Ltd., Exide Industries, Panasonic Corporation, and GS Yuasa Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Demand for Electric Vehicles

- 4.5.1.2 Growing Renewable Energy Penetration

- 4.5.2 Restraints

- 4.5.2.1 Supply Chain Constraints

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lead Acid

- 5.1.2 Lithium-Ion

- 5.1.3 Others (NiMh, NiCd, etc.)

- 5.2 Applications

- 5.2.1 Automobiles

- 5.2.2 Industrial Batteries

- 5.2.3 Portable Batteries

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 France

- 5.3.3 United Kingdom

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 NORDIC

- 5.3.7 Russia

- 5.3.8 Turkey

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd.

- 6.3.2 LG Chem Ltd.

- 6.3.3 Contemporary Amperex Technology Co Ltd

- 6.3.4 Exide Industries

- 6.3.5 Saft Groupe SA

- 6.3.6 Samsung SDI Co., Ltd.

- 6.3.7 Murata Manufacturing Co., Ltd.

- 6.3.8 Panasonic Corporation

- 6.3.9 GS Yuasa Corporation

- 6.3.10 Tesla, Inc.

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in New Battery Chemistry