ASEAN諸国のハイブリッド電気自動車用電池:市場シェア分析、産業動向、成長予測(2025年~2030年)

ASEAN Countries Hybrid Electric Vehicle Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636530

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

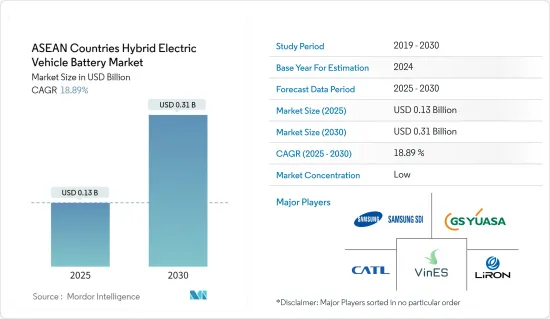

ASEAN諸国のハイブリッド電気自動車用電池市場規模は、2025年に1億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは18.89%で、2030年には3億1,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、リチウムイオン電池価格の低下と電気自動車の普及拡大が、予測期間中のASEAN諸国のハイブリッド電気自動車用電池市場の需要を牽引すると予測されます。

- 一方、原料の需給ミスマッチが予測期間中の市場成長の妨げになると予想されます。

- 電池技術の技術的進歩や自動車メーカーと電池メーカーの協力関係は、将来的にASEAN諸国のハイブリッド電気自動車用電池市場に大きな機会をもたらすと予想されます。

- 特にタイは際立っており、自動車部門における電気自動車の存在感を高めるというコミットメントに後押しされ、顕著な成長が見込まれています。

ASEAN諸国のハイブリッド電気自動車用電池市場動向

乗用車セグメントが著しい成長を遂げる

- ASEAN(東南アジア諸国連合)諸国は、ハイブリッド電気自動車(HEV)用電池、特に乗用車用電池の市場で大きな成長を遂げようとしています。この急成長の背景には、電気自動車(EV)の普及拡大、クリーンエネルギーを支持する政府の取り組み、環境問題に対する消費者の意識の高まりがあります。近年では、インドネシア、マレーシア、タイ、ベトナム、フィリピンといった国々が、EVを取り巻く情勢において極めて重要な参入企業として台頭してきています。

- ASEAN自動車連盟(AAF)のデータによると、ASEAN地域の2023年の乗用車生産台数は274万8,000台で、2022年の266万5,000台から3.11%増加しました。2022年の生産台数は約221万2,000台で、2023年の数字は228万3,000台となり、3.21%の上昇となります。特筆すべきは、インドネシア、マレーシア、タイがこの地域の乗用車生産台数の83%以上を占めていることです。

- 今後、この地域の乗用車の成長は、電気自動車の普及を促進する政府の取り組みによって強化されると予想され、HEV用電池の需要も促進されます。タイ、インドネシア、シンガポール、マレーシア、フィリピンのような国々は、政府の支援策により、急速なEV普及が見込まれています。例えばフィリピンは、2030年までにEVが自動車全体の21%を占め、2040年までに50%を占めることを目指しています。その他の特典として、フィリピン電気自動車協会(EVAP)は、EVの普及目標を2030年の30万台から大胆にも100万台に引き上げ、セクターのインセンティブ、規制の明確化、EVの恩恵に対する意識の高まりに期待しています。

- インドネシアの野心も同様に顕著で、2025年までに自動車販売に占めるEVの割合を20%とし、2030年までに60万台のEV国産化を目標としています。これらの目標には、販売、生産、充電インフラなど、EVサプライチェーンにおけるさまざまなマイルストーンが含まれており、これらすべてがHEV電池の成長に拍車をかけることになります。

- 2024年初頭、タイのEV委員会は、EV産業の勢いを加速させ、現地製造業への投資を呼び込むことを目的とした4年間(2024~2027年)の構想であるEV 3.5包装を承認しました。この包括的な包装は、EVエコシステム全体の活性化を目指すだけでなく、車種や電池容量に合わせたEV購入に対する政府補助金も含まれており、HEV電池市場にとって有益な環境を醸成するものです。

- 2023年、フィリピンのエネルギー省(DOE)は、2040年までに電気自動車(EV)を630万台普及させ、道路交通量の50%を目標にする計画を発表しました。この野心的な目標は、約14万7,000カ所のEV充電ステーションの設置によって補完されます。DOEの当面の目標には、2028年までに245万台の電気自動車、二輪車、バスを配備することが含まれています。このような大規模な計画は、乗用車セグメントにおける電池市場の急成長を裏付けるものであり、HEV電池市場の成長をさらに後押しするものです。

- このような力学を考えると、乗用車セグメントは今後数年で大幅な成長を遂げると考えられます。

著しい成長を遂げるタイ

- タイは自動車セグメントへの投資先として際立っています。過去50年間、タイは単に自動車部品を組み立てるだけの国から、東南アジア随一の自動車生産・輸出拠点へと発展してきました。自動車メーカーからの投資が増加する中、タイの電池産業は、特にハイブリッド車を含む電気自動車(EV)生産の急増に伴い、着実な成長を遂げようとしています。

- タイ電気自動車協会(EVAT)の報告によると、タイでは2023年に約8万5,069台のハイブリッド電気自動車(HEV)が新規登録され、前年比32%の大幅増となりました。さらに、2024年2月末までに、HEVの新規登録台数は約2万6,134台に達し、タイにおける急速な成長と電池需要の高まりを裏付けています。

- EV、特にHEVの導入が急増している背景には、購入者に対する政府の優遇措置やメーカーに対する支援策があります。例えば、タイは国産EVに対する購入補助金制度をイントロダクションとして導入しており、東南アジアのEV生産ハブになるという野心を強調しています。2024~2027年まで有効なEV3.5スキームは、1台あたり5万バーツ(1,397.02米ドル)から10万バーツ(2,794.04米ドル)の補助金を提供するもので、EVセクターの育成と海外からの投資誘致に熱心な政府の姿勢を浮き彫りにしています。

- タイは、2030年までに自動車販売台数の30%をEVにすることを目指しています。この野心と現在の取り組みにより、タイはHEV用電池、特にリチウムイオン・タイプの将来のハブとして位置づけられ、電池・メーカーにとって大きな機会となります。

- このビジョンに沿って、多くの電池メーカーがタイでの生産能力を増強しています。例えば、BMWグループは2024年3月、タイで「Gen-5」高電圧電池製造施設の起工式を行った。東海岸のラヨーンに位置する4,000平方メートルの電池組立工場は、BMWの既存の自動車工場に統合されています。BMWは2025年後半にこのラヨーン工場からEVを発売する準備を進めており、新しい電池組立ラインは、輸入された電池セルを高電圧電池のモジュールに変換するという極めて重要な役割を果たすことになります。BMWはこの事業に4,500万米ドル以上を投資したと言われています。

- こうした開発を踏まえると、予測期間中、タイはASEAN地域のHEV用電池市場をリードすることになると考えられます。

ASEAN諸国のハイブリッド電気自動車用電池産業概要

ASEAN諸国のハイブリッド電気自動車用電池は半分断されています。市場の主要企業(順不同)には、Samsung SDI、VinES Energy Solutions Joint Stock Company、Contemporary Amperex Technology(CATL)、LiRON LIB Power Pte Ltd、GS Yuasa Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- リチウムイオン電池価格の下落

- 電気自動車の普及拡大

- 抑制要因

- 原料の需給ミスマッチ

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 電池タイプ

- リチウムイオン電池

- 鉛蓄電池

- ナトリウムイオン電池

- その他電池タイプ

- 車種

- 乗用車

- 商用車

- 地域

- タイ

- インドネシア

- フィリピン

- マレーシア

- ベトナム

- その他のASEAN諸国

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Panasonic Corporation

- Samsung SDI Co., Ltd.

- Contemporary Amperex Technology Co. Ltd(CATL)

- LG Energy Solution Ltd.

- LiRON LIB Power Pte Ltd

- GS Yuasa Corporation

- VinES Energy Solutions Joint Stock Company

- SVOLT Energy Technology Co., Ltd.

- Energy Absolute Public Company Limited

- その他の著名な企業一覧(会社名、本社所在地、関連製品とサービス、連絡先など)

- 市場ランキング/シェア分析

第7章 市場機会と今後の動向

- 電池技術の技術的進歩

目次

The ASEAN Countries Hybrid Electric Vehicle Battery Market size is estimated at USD 0.13 billion in 2025, and is expected to reach USD 0.31 billion by 2030, at a CAGR of 18.89% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, declining lithium-ion battery prices, and growing adoption of electric vehicles are expected to drive the demand for the ASEAN countries hybrid electric vehicle battery market during the forecast period.

- On the other hand, the demand-supply mismatch of raw materials is expected to hinder the market's growth during the forecast period.

- Nevertheless, the technological advancements in battery technologies and the automaker-battery manufacturer collaborations are expected to create vast opportunities for ASEAN countries hybrid electric vehicle battery market in the future.

- Particularly, Thailand stands out, anticipating notable growth, driven by its commitment to amplifying the electric vehicle's presence in its automotive sector.

ASEAN Countries Hybrid Electric Vehicle Battery Market Trends

Passenger Vehicle Segment to Witness Significant Growth

- The ASEAN (Association of Southeast Asian Nations) countries are poised for significant growth in the market for hybrid electric vehicle (HEV) batteries, especially for passenger vehicles. This surge is driven by the increasing adoption of electric vehicles (EVs), government initiatives championing clean energy, and heightened consumer awareness of environmental concerns. In recent years, nations like Indonesia, Malaysia, Thailand, Vietnam, and the Philippines have emerged as pivotal players in the EV landscape.

- Data from the ASEAN Automotive Federation (AAF) reveals that the ASEAN region produced 2.748 million passenger vehicles in 2023, marking a 3.11% rise from 2.665 million in 2022. In 2022, production was approximately 2.212 million units, and the 2023 figure of 2.283 million units represents a 3.21% uptick. Notably, Indonesia, Malaysia, and Thailand collectively accounted for over 83% of the region's passenger vehicle output.

- Looking ahead, the region's growth in passenger vehicles is anticipated to be bolstered by government initiatives promoting electric vehicle adoption, subsequently driving demand for HEV batteries. Countries like Thailand, Indonesia, Singapore, Malaysia, and the Philippines are set to experience swift EV adoption, thanks to supportive government measures. For instance, the Philippines aims for EVs to constitute 21% of its total vehicles by 2030 and 50% by 2040. Additionally, the Electric Vehicle Association of the Philippines (EVAP) has upped its e-vehicle adoption target from 300,000 units in 2030 to a bold 1.0 million, banking on sector incentives, clearer regulations, and rising EV benefits awareness.

- Indonesia's ambitions are equally pronounced, targeting 20% EV representation in car sales by 2025 and a goal of 600,000 domestically produced EVs by 2030. These targets encompass various milestones in the EV supply chain, including sales, production, and charging infrastructure, all of which are set to spur HEV battery growth.

- In early 2024, Thailand's EV Board greenlit the EV 3.5 package, a four-year initiative (2024-2027) aimed at propelling the EV industry's momentum and attracting investments in local manufacturing. This comprehensive package not only seeks to invigorate the entire EV ecosystem but also includes government subsidies for EV purchases, tailored to vehicle types and battery capacities, fostering a conducive environment for the HEV battery market.

- In 2023, the Philippines' Department of Energy (DOE) unveiled plans to have 6.3 million electric vehicles (EVs) by 2040, targeting 50% of the road traffic. This ambitious goal is complemented by the installation of approximately 147,000 EV charging stations. The DOE's immediate objective includes deploying 2.45 million electric cars, motorcycles, and buses by 2028. Such expansive plans underscore the burgeoning battery market within the passenger vehicle segment, further propelling the HEV battery market's growth.

- Given these dynamics, the passenger vehicle segment is set for substantial growth in the coming years.

Thailand to Witness a Significant Growth

- Thailand stands out as a prime destination for investments in the automobile sector. Over the past five decades, Thailand has evolved from merely assembling auto components to becoming Southeast Asia's foremost automotive production and export hub. With rising investments from automakers, Thailand's battery industry is poised for steady growth, especially with the surge in electric vehicle (EV) production, including hybrids.

- As reported by the Electric Vehicle Association of Thailand (EVAT), Thailand registered approximately 85,069 new hybrid electric vehicles (HEVs) in 2023, marking a significant 32% increase from the previous year. Furthermore, by the end of February 2024, new HEV registrations reached around 26,134 units, underscoring the rapid growth and heightened demand for batteries in the nation.

- The surge in EV adoption, particularly HEVs, can be attributed to government incentives for buyers and supportive measures for manufacturers. For instance, Thailand's introduction of a purchase subsidy scheme for domestically produced EVs underscores its ambition to be Southeast Asia's EV production hub. The EV3.5 scheme, active from 2024 to 2027, offers subsidies between THB 50,000 (USD 1,397.02) and THB 100,000 (USD 2,794.04) per vehicle, highlighting the government's dedication to nurturing the EV sector and drawing in foreign investments.

- Thailand aims to have EVs make up 30% of all vehicle sales by 2030. This ambition, coupled with current initiatives, positions Thailand as a future hub for HEV batteries, especially lithium-ion types, presenting vast opportunities for battery manufacturers.

- In line with this vision, numerous battery manufacturers are ramping up their production capabilities in Thailand. For instance, in March 2024, BMW Group broke ground on its 'Gen-5' high-voltage battery manufacturing facility in Thailand. Situated in Rayong, on the eastern coast, the 4,000 square meter battery assembly is integrated into BMW's existing car plant. As BMW gears up to launch EVs from this Rayong facility in the latter half of 2025, the new battery assembly line will play a pivotal role, converting imported battery cells into modules for high-voltage batteries. BMW has reportedly invested over USD 45 million in this venture.

- Given these developments, Thailand is poised to lead the HEV battery market in the ASEAN region during the forecast period.

ASEAN Countries Hybrid Electric Vehicle Battery Industry Overview

The ASEAN Countries Hybrid Electric Vehicle Battery is semi-fragmented. Some of the key players in the market (not in any particular order) include Samsung SDI Co. Ltd., VinES Energy Solutions Joint Stock Company, Contemporary Amperex Technology Co. Ltd (CATL), LiRON LIB Power Pte Ltd and GS Yuasa Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Declining Lithium-Ion Battery Prices

- 4.5.1.2 Increasing Adoption of Electric Vehicles

- 4.5.2 Restraints

- 4.5.2.1 Demand-Supply Mismatch of Raw Materials

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-acid Battery

- 5.1.3 Sodium-ion Battery

- 5.1.4 Others Battery Types

- 5.2 Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 Geography

- 5.3.1 Thailand

- 5.3.2 Indonesia

- 5.3.3 Philippines

- 5.3.4 Malaysia

- 5.3.5 Vietnam

- 5.3.6 Rest of ASEAN Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Panasonic Corporation

- 6.3.2 Samsung SDI Co., Ltd.

- 6.3.3 Contemporary Amperex Technology Co. Ltd (CATL)

- 6.3.4 LG Energy Solution Ltd.

- 6.3.5 LiRON LIB Power Pte Ltd

- 6.3.6 GS Yuasa Corporation

- 6.3.7 VinES Energy Solutions Joint Stock Company

- 6.3.8 SVOLT Energy Technology Co., Ltd.

- 6.3.9 Energy Absolute Public Company Limited.

- 6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

- 6.5 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in Battery Technologies

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日