|

市場調査レポート

商品コード

1636178

ハイブリッド電気自動車用電池:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Hybrid Electric Vehicle Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ハイブリッド電気自動車用電池:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

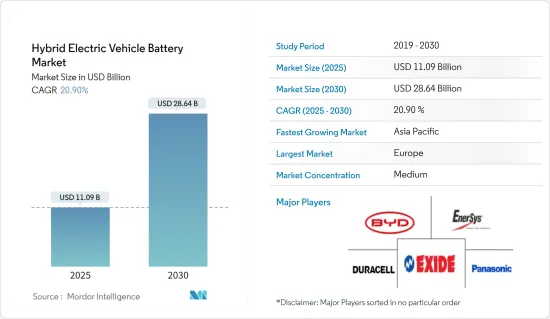

ハイブリッド電気自動車用電池市場規模は2025年に110億9,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは20.9%で、2030年には286億4,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、電気自動車(EV)の普及台数の増加とリチウムイオン電池価格の下落が、予測期間中のハイブリッド電気自動車用電池の需要を牽引すると予想されます。

- 一方、原料の埋蔵量不足はハイブリッド電気自動車用電池市場の成長を大きく抑制する可能性があります。

- エネルギー密度の向上、充電時間の短縮、安全性の向上、寿命の延長など、電池材料の技術的進歩は、近い将来、ハイブリッド電気自動車用電池市場の参入企業に大きな機会をもたらすと予想されます。

- アジア太平洋は、電気自動車の採用が増加しているため、予測期間中、世界のハイブリッド電気自動車用電池市場で最も急成長している地域です。

ハイブリッド電気自動車用電池市場動向

リチウムイオン電池タイプが市場を独占

- 世界のリチウムイオン電気自動車用電池市場は、機会と課題の魅力的な風景を提示しています。有利な容量対重量比により、リチウムイオン二次電池は他の電池技術よりも人気を集めています。リチウムイオン二次電池の普及を後押ししているその他の要因には、性能の向上(長寿命、低メンテナンス)、保存性の向上、価格の低下などがあります。

- リチウムイオン電池の価格は通常、他の電池よりも高いです。しかし、市場全体の主要企業は、スケールメリットを得るための投資や性能向上のための研究開発活動を行っており、競争が激化し、その結果、リチウムイオン電池の価格が低下しています。

- 電気自動車(EV)と電池エネルギー貯蔵システム(BESS)の平均電池パック価格が上昇しているため、電池価格は2023年には139米ドル/kWhまで下落し、13%以上低下しました。技術革新と製造の強化により、電池パック価格はさらに低下し、2025年には113米ドル/kWh、2030年には80米ドル/kWhに達すると予想されます。

- さらに、環境問題への関心の高まりから、世界中の政府が電気自動車を大幅に推進しています。政府は、純炭素排出ゼロ目標に大きく注目しています。リチウムは、電気自動車に貯蔵能力を提供する電池に不可欠な要素です。世界の主要企業は、リチウムイオン電池の需要増加を満たすためにリチウムを抽出しています。

- 例えば、2023年11月、Exxon Mobil Corporationは、重要なリチウム鉱床を保有することで知られるアーカンソー州南西部で、北米リチウム生産の第1段階を開始する可能性が高いと発表しました。最初の生産は2027年を目標としています。このようなプロジェクトは、リチウムの生産を加速させ、予測期間中にリチウムイオン電池の需要増を満たす可能性が高いです。

- さらに、世界各国政府は電気自動車を促進するために様々な施策やインセンティブを実施しています。これらの施策は、リチウムイオン電池の需要にプラスの影響を与えています。政府は、地域全体でEVを促進するために数多くのイニシアチブを発表しました。

- 例えば、英国は、2030年までに新車販売台数の80%、新車販売台数の70%のバンをゼロエミッション車にすることを義務付け、2035年までに100%に到達させるZEV義務付けを制定しました。さらに、ガソリン車やディーゼル車、バンの新車販売は2030年までに禁止され、2035年までにすべての新車とバンがテールパイプでゼロエミッションになることが義務づけられるようです。このような取り組みにより、今後数年間、国全体でEVの生産と需要が加速し、予測期間中のリチウムイオン電池の需要が高まる可能性が高いです。

- このようなプロジェクトや投資は、予測期間中に地域全体のEV生産を増加させ、リチウムイオン電池の需要を高める可能性が高いです。

アジア太平洋が著しい成長を遂げる

- アジア太平洋のハイブリッド電気自動車(HEV)用電池市場は、環境意識の高まり、政府の支援施策、技術の進歩によって急成長しているセグメントです。

- 中国、日本、韓国、インドといった国々を含むアジア太平洋は、HEV電池市場で著しい成長を遂げています。この背景には、環境に優しい自動車に対する需要の高まりと、二酸化炭素排出量削減に向けた政府の強力な後押しがあります。

- ハイブリッド電気自動車(HEV)の需要は、この地域全体で大幅に増加しています。この地域では中国がHEVの主要生産国です。例えば、国際エネルギー機関(IEA)によると、2023年のプラグイン・ハイブリッド電気自動車の販売台数は270万台、次いで日本の5万2,000台となっています。アジア太平洋全体で数多くのEV生産工場が設立され、ハイブリッド電気自動車(HEV)用電池の需要が増加しているため、EV販売は今後数年間で増加します。

- この地域の政府は、ハイブリッド車や電気自動車の導入を促進するために、さまざまな施策やインセンティブを実施しています。これには、補助金、税制優遇措置、厳しい排ガス規制などが含まれ、メーカーはより多くのHEVを生産するよう奨励されています。

- オーストラリア政府は、EVをより手頃な価格で購入できるよう、税制優遇措置やリベートを導入しています。これには、EVの輸入関税の引き下げや、インフラ開発への補助金提供などが含まれます。いくつかの州では、独自のEVインセンティブを設けています。例えば、ニューサウスウェールズ州では、6万8,750米ドル以下で販売される最初の2万5,000台のEVに対して3,000米ドルのリベートを提供しており、2030年までに全乗用車を電気自動車にすることを目指しています。ビクトリア州は、6万8,740米ドル以下のEV販売台数2万台に対して3,000米ドルの補助金を支給し、印紙税も免除します。

- また、インド政府は2030年以降の新車販売を完全電動化するという野心的な目標を設定しました。インド政府は、2030年までに自家用車の30%、商用車の70%、二輪車と三輪車の80%をEVが占めるという目標を設定しました。さらに政府は、1kWhあたり1万インドルピー(120米ドル)から1万5,000インドルピー(180米ドル)の補助金優遇措置も提供しています。このような取り組みにより、今後数年間は全国的にEVの生産と需要が加速し、予測期間中にHEV用電池の需要が高まる可能性が高いです。

- このようなプロジェクト開発は、EVの電池エネルギー貯蔵システムのためのHEV電池ソリューションの実現可能性と重要性を示すものであり、今後数年間、国全体のHEV電池の需要を高める可能性が高いです。

ハイブリッド電気自動車用電池産業概要

ハイブリッド電気自動車用電池市場は半分裂状態です。主要参入企業(順不同)は、BYD Company Ltd.、Duracell Inc.、Exide Industries Ltd.、EnerSys、Panasonic Holdings Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車(EV)生産の増加

- リチウムイオン電池価格の下落

- 抑制要因

- 原料の埋蔵量不足

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 電池タイプ

- リチウムイオン電池

- 鉛蓄電池

- ナトリウムイオン電池

- その他

- 2029年までの市場規模・需要予測(地域別)

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- ノルディック

- ロシア

- トルコ

- その他の欧州

- アジア太平洋

- 中国

- インド

- オーストラリア

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- エジプト

- カタール

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略とSWOT分析

- 企業プロファイル

- BYD Company Ltd

- Duracell Inc.

- EnerSys

- Panasonic Holdings Corporation

- Energizer

- Exide Industries Ltd

- Saft Groupe SA

- AMTE Power

- Amperex Technology Co. Limited

- Gotion High tech Co Ltd

- その他の著名な企業一覧

- 市場ランキング/シェア分析

第7章 市場機会と今後の動向

- 電池材料の技術進歩

目次

Product Code: 50002587

The Hybrid Electric Vehicle Battery Market size is estimated at USD 11.09 billion in 2025, and is expected to reach USD 28.64 billion by 2030, at a CAGR of 20.9% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, rising adoption of electric vehicles (EV) and declining lithium-ion battery prices are expected to drive the demand for hybrid electric vehicle batteries during the forecast period.

- On the other hand, the lack of raw material reserves can significantly restrain the growth of the hybrid electric vehicle battery market.

- Nevertheless, technological advancements in battery materials like higher energy density, faster charging times, improved safety, and longer lifespan are expected to create significant opportunities for hybrid electric vehicle battery market players in the near future.

- Asia Pacific is the fastest-growing region in the global hybrid electric vehicle battery market during the forecast period due to the rising adoption of electric vehicle.

Hybrid Electric Vehicle Battery Market Trends

Lithium-Ion Battery Type Dominate the Market

- The lithium-ion electric vehicle battery market worldwide presents a fascinating landscape of opportunities and challenges. Due to their favorable capacity-to-weight ratio, lithium-ion rechargeable batteries are gaining more popularity than other battery technologies. Other factors contributing to boosting their adoption include better performance (long life and low maintenance), better shelf life, and decreasing price.

- The price of lithium-ion batteries is usually higher than that of other batteries. However, major players across the market have been investing to gain economies of scale and R&D activities to enhance their performance, increasing the competition and, in turn, resulting in declining prices of lithium-ion batteries.

- Owing to the increasing average battery pack prices of electric vehicles (EV) and battery energy storage systems (BESS), the battery prices declined in 2023 to USD 139 /kWh, a decrease of over 13%. The trajectory of technological innovation and manufacturing enhancements is anticipated to decrease the battery pack prices further, projecting the price to reach USD 113/kWh in 2025 and USD 80/kWh in 2030.

- Furthermore, governments all over the world are significantly promoting electric vehicles due to rising environmental concerns. The government is significantly focused on net zero carbon emission targets. Lithium is a vital element in batteries that provides the storage capacity for EVs. The leading companies around the globe are extracting lithium to fulfill the rising demand for lithium-ion batteries.

- For instance, in November 2023, Exxon Mobil Corporation announced that it was likely to start the first phase of North American lithium production in southwest Arkansas, an area known to hold significant lithium deposits. The first production is targeted for 2027. Such projects are likely to accelerate the production of lithium and fulfill the rising demand for lithium-ion batteries during the forecast period.

- Additionally, the government worldwide has implemented various policies and incentives to promote electric vehicles. These policies have positively impacted the demand for lithium-ion batteries. The government announced numerous initiatives to promote EVs across the region.

- For instance, the United Kingdom has established a ZEV mandate that requires 80% of new cars and 70% of new vans sold to be zero-emission by 2030, reaching 100% by 2035. Furthermore, the sale of new petrol and diesel cars and vans is likely to be banned by 2030, with all new cars and vans required to be zero-emission at the tailpipe by 2035. Such initiatives are likely to accelerate the production and demand of EVs across the country in the coming years and are likely to raise the demand for lithium-ion batteries in the forecast period.

- Such type of projects and investments likely to increase the EV production across the region and rising demand of lithium-ion battery during the forecast period.

Asia Pacific to Witness Significant Growth

- The Asia Pacific hybrid electric vehicle (HEV) battery market is a rapidly growing sector driven by increasing environmental awareness, supportive government policies, and technological advancements.

- The Asia Pacific region, including countries like China, Japan, South Korea, and India, is experiencing significant growth in the HEV battery market. This is due to rising demand for eco-friendly vehicles and a robust governmental push towards reducing carbon emissions.

- The demand for hybrid electric vehicles (HEV) is rising significantly across the region. China is the leading producer of HEV in the region. For instance, according to the International Energy Agency (IEA), in 2023, the sale of Plug-in Hybrid Electric Vehicles was 2.7 million units, followed by Japan with 52 thousand units. EV Sales are rising in the coming years as numerous EV production plants are set up across the Asian Pacific region, and the demand for hybrid electric vehicle (HEV) batteries is increasing.

- Governments in the region are implementing various policies and incentives to promote the adoption of hybrid and electric vehicles. These include subsidies, tax benefits, and stringent emission norms which encourage manufacturers to produce more HEVs.

- The Australian government has introduced tax incentives and rebates to make EVs more affordable. This includes reducing the import duty on EVs and offering grants for infrastructure development. Several states have their own EV incentives. For instance, New South Wales offers a USD 3,000 rebate for the first 25,000 EVs sold under USD 68,750 and aims for its entire passenger fleet to be electric by 2030. Victoria provides a USD 3,000 subsidy for the first 20,000 EVs sold under USD 68,740, along with stamp duty exemptions.

- Morover, The Indian government set an ambitious target for new vehicle sales after 2030 to be fully electric. The Indian government set a target of EV sales accounting for 30% of private cars, 70% of commercial vehicles, and 80% of two and three wheelers by 2030. Further, the government has also offered subsidy incentives from INR 10,000 per kWh (USD 120) to INR 15,000 per kWh (USD 180). Such initiatives are likely to accelerate the production and demand of EVs across the country in the coming years and are likely to raise the demand for HEV batteries during the forecast period.

- Such project developments showcase the feasibility and importance of HEV battery solutions for battery energy storage systems in EVs and are likely to raise the demand for HEV batteries across the country in the coming year.

Hybrid Electric Vehicle Battery Industry Overview

The hybrid electric vehicle battery market is semi-fragmented. Some key players (not in particular order) are BYD Company Ltd, Duracell Inc., Exide Industries Ltd, EnerSys, and Panasonic Holdings Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Increasing Electric Vehicle (EV) Production

- 4.5.1.2 Declining Lithium-ion Battery Prices

- 4.5.2 Restraints

- 4.5.2.1 Lack of Raw Material Reserves

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Sodium-ion Battery

- 5.1.4 Others

- 5.2 Geography [Market Size and Demand Forecast till 2029 (for regions only)]

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 United Kingdom

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 NORDIC

- 5.2.2.7 Russia

- 5.2.2.8 Turkey

- 5.2.2.9 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Australia

- 5.2.3.4 Japan

- 5.2.3.5 South Korea

- 5.2.3.6 Malaysia

- 5.2.3.7 Thailand

- 5.2.3.8 Indonesia

- 5.2.3.9 Vietnam

- 5.2.3.10 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 Saudi Arabia

- 5.2.4.2 United Arab Emirates

- 5.2.4.3 Nigeria

- 5.2.4.4 Egypt

- 5.2.4.5 Qatar

- 5.2.4.6 South Africa

- 5.2.4.7 Rest of Middle East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Colombia

- 5.2.5.4 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted & SWOT Analysis for Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Company Ltd

- 6.3.2 Duracell Inc.

- 6.3.3 EnerSys

- 6.3.4 Panasonic Holdings Corporation

- 6.3.5 Energizer

- 6.3.6 Exide Industries Ltd

- 6.3.7 Saft Groupe SA

- 6.3.8 AMTE Power

- 6.3.9 Amperex Technology Co. Limited

- 6.3.10 Gotion High tech Co Ltd

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in Battery Materials