|

市場調査レポート

商品コード

1550282

米国の監視カメラ:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)United States Surveillance Camera - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の監視カメラ:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

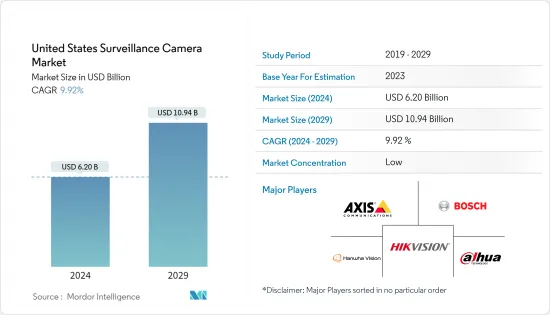

米国の監視カメラ市場規模は2024年に62億米ドルと推定・予測され、2029年には109億4,000万米ドルに達し、予測期間(2024-2029年)のCAGRは9.92%で成長すると予測されます。

主なハイライト

- 過去10年間、米国の監視カメラ市場は、技術の進歩、セキュリティ懸念の高まり、規制の進化に後押しされ、大きく成長してきました。AIとMLの進歩は監視システムに革命をもたらしました。これらはビデオ解析を強化し、顔認識、行動分析、物体検出などの高度な機能を可能にし、システムの有効性を高めています。さらに、モノのインターネット(IoT)技術の採用が進むことで、接続性が合理化され、遠隔監視が可能になり、監視システムの効率と使いやすさが向上しています。

- さらに、米国のマクロ経済情勢は、公共安全に対する政府支出の増加に後押しされ、市場成長に寄与しています。特筆すべきは、米国政府が2025年度に司法省に457億米ドルの大幅な予算を割り当てたことで、セキュリティ・イニシアチブへのコミットメントが強調され、監視カメラ市場に明るい兆しが見えてきたことです。

- 市場の情勢はいくつかの動向によって大きく変わりつつあります。特に、クラウドベースの監視ソリューションへのシフトが顕著で、スケーラブルなストレージとアクセス性の向上が実現されています。ワイヤレスカメラが勢いを増しており、その柔軟性と簡単な設置が評価されています。さらに、監視システムを他のスマートデバイスやプラットフォームと統合する動向も急増しています。

- カメラは、ビデオ監視ツールから、Internet of Everythingにおける極めて重要なAIoT(モノの人工知能)コンポーネントへと進化しています。各社は映像技術に磨きをかけ、多次元的な知覚を強化し、アプリケーションの地平を広げ、さまざまな分野のデジタル化を先導しています。この協調的努力は、インテリジェント・アプリケーションの強固な基盤を築くことを目的としています。

- さらに、各社は光学画像研究をさらに深く掘り下げています。視野の制限、夜間の画像の鮮明さ、インテリジェント・アプリケーションの制限など、従来のカメラの限界を克服することに注力しています。このような動きは、超高解像度、フルカラー、パノラマの細部に重点を置いた製品の強化に現れています。メーカー各社はまた、フルカラーズーム機能、大口径ズーム、鮮やかな画質のための安定した光量といった機能を強調し、夜間適応性を強化しています。

- 米国のいくつかの主要都市は監視の目が厳しく、住民1,000人あたり平均10台以上のカメラが設置されています。これらのカメラは、交通監視から犯罪防止まで、多くの役割を果たしています。最新の監視カメラは高解像度を誇り、ライブ・ストリームへのリモート・アクセスを提供し、顔認識や自動ナンバープレート認識(ALPR)などの高度な技術を組み込んでおり、現代のセキュリティ対策の要としての地位を確固たるものにしています。

- プライバシーの問題に対する一般市民の意識の高まりが、広範な監視に対する潜在的な抵抗につながり、規制の厳格化を促すなど、課題は依然として残っているが、市場の普及は影響を受ける可能性があります。さらに、監視システムの相互接続が進むにつれて、サイバー攻撃のリスクも高まっています。しかし、強固なサイバーセキュリティ対策を実施することは不可欠ではあるが、コストと技術的な負担が大きいです。

- 米国政府は、1兆9,000億米ドルの米国救済計画の下で、150億米ドルを特に公共安全対策に割り当てた。最近の報告書では、全米の犯罪率が顕著に低下したことが強調されており、これは公共の安全への重点が高まったことが原因であるとされています。特に、米国人口の約82%をカバーする約13,000の法執行機関のデータから、2023年には2022年に比べて殺人事件が13%減少し、報告された暴力犯罪と財産犯罪がそれぞれ6%と4%減少することが明らかになった。こうした改善にもかかわらず、監視カメラの需要が衰えることはないと思われます。消費者、企業、政府によるセキュリティ製品への投資が強化される傾向が強まっており、敷地内の強化や治安の強化を目指しています。

米国の監視カメラ市場動向

IPベースの監視カメラが大幅な成長を遂げる見込み

- IPベースの監視カメラは、インターネットネットワークを介してビデオデータを送信し、米国市場における従来のアナログシステムを凌駕しています。IPベースの監視カメラは、先進的な機能、高解像度、適応性により、技術的な進歩や幅広い分野での採用が進む中、セキュリティ意識の高い市場と共鳴しています。これらのカメラはHDやUHDのビデオ画質を提供し、より鮮明で詳細な画像でアナログのものを凌駕しています。リモートアクセス、デジタルズーム、セキュリティシステムとのシームレスな統合を誇るIPカメラは、機能的でユーザーフレンドリーです。その拡張性はさらに際立っており、インフラを大幅に見直すことなくシステムを拡張することができます。

- スマートホーム技術やIoTの急増により、IPカメラの需要は高まっており、より広範なホームセキュリティやオートメーション・セットアップにシームレスに統合されています。初期投資は高くつくかもしれないが、IPカメラは簡単な設置、最小限のケーブル配線、メンテナンスの軽減により、長期的な節約を約束します。企業はますます、リアルタイムの状況認識を強化し、セキュリティを強化し、貴重な運用上の洞察を得るために、ビデオ分析機能を備えたIPベースのセキュリティカメラに目を向けるようになっています。4K解像度カメラの登場により、プロバイダーは管理ソフトウェアに高度な機能を組み込むことができます。

- 人工知能は際立った動向であり、顔認識、行動分析、自動アラートなどの機能を向上させています。企業、特に将来を見据えている企業は、AI対応の監視システムに注目しています。さらに、クラウドベースのソリューションは大幅なコスト効率を提供する一方、運用技術コストは時として隠蔽されることがあります。コンピューティングとビデオ・ストレージをクラウドに移行することで、一般的にオンサイト・システムよりも所有コストが20~50%低くなります。アメリカのEagle Eye Network社は、セキュリティ顧客の約76%がサブスクリプション契約を選択していることを指摘し、こうした節約効果を強調しています。

- スケーラブルでアクセスしやすい映像の保存と分析を容易にするクラウドストレージと管理の動向は、IPカメラ市場をさらに促進しています。一部のVSaaSプロバイダーは、価格保護付きの複数年契約を提供することで、契約を有利にしています。この動きは、特に高解像度カメラがより手頃な価格になるにつれて、顧客の共感を呼んでいます。Eagle Eye Networksのデータは、このシフトを強調しており、過去5年間で高解像度のIPセキュリティカメラが3倍に増加していることを明らかにしています。

- 国内のさまざまな地域で犯罪率が上昇していることから、高度な監視システムへの需要が高まり、調査対象市場の成長に資する環境が整うと予想されています。例えば、国家保険犯罪局(NICB)によると、2023年には100万件以上の車両盗難が報告され、車両盗難全体では全国で約1%増加しました。コロンビアの地区では、前年比で最も高い伸び(64%)を示しました。

小売部門に大きな需要が見込まれる

- 米国では、小売部門が監視カメラの導入に大きく舵を切っています。この動きは主に、紛失防止、顧客の安全性強化、業務の合理化、消費者行動の洞察の必要性によって後押しされています。これらのカメラは単なる道具ではなく、資産を守り、安全なショッピング環境を作り、店舗管理を微調整するための最前線の防衛手段です。

- 監視カメラの導入が急増している背景には、窃盗、万引き、内部不正に対抗する緊急の必要性があります。さらに、小売業者は顧客と従業員の安全を確保するため、監視カメラを店舗敷地や駐車場まで拡大するケースが増えています。セキュリティだけでなく、これらのカメラは現在、日々の店舗活動の監視、待ち行列の管理、スタッフ配置の最適化にも欠かせないものとなっています。

- 米国小売業協会(National Retail Federation)の報告によると、小売業における犯罪被害額は1,000億米ドルを超えるといいます。NRFによる2023年の調査では、回答した小売企業の52%がテクノロジーとソフトウェアの予算を増やしていると回答しています。また、小売企業が損失を抑制するために最も効果的と考えるセキュリティ対策の上位10項目には、CCTVやビデオ監視、アップグレードまたは統合されたCCTVシステムなどが含まれています。

- 小売企業は、ロス防止のために新たなテクノロジーを活用する傾向が強まっています。調査によると、回答者の37%がeコマース詐欺の検知に人工知能ベースの分析を検討しており、13%がすでにこれらのシステムを導入しています。さらに、35%が従業員用の身体装着カメラを検討しています。また、18%が駐車場にモバイル監視ユニットを導入済みで、さらに10%が導入中、19%が店舗での導入を検討しています。

- 小売企業は、新たなテクノロジーを積極的に模索しています。NRFによると、顔認識技術を完全に導入しているのはわずか3%に過ぎないが、実に40%が顔認識技術や特徴照合技術を調査中、試験中、またはすでに導入しています。NRFは、2024年の小売売上高成長率を2.5%から3.5%と予測しています。

- さらに、米国国勢調査局によると、2023年の米国の小売総売上高は7兆2,400億米ドルに達しました。したがって、予想される小売売上高の増加は、高度な監視カメラの採用の急増と相まって、市場を前進させる態勢を整えています。

米国の監視カメラ産業概要

米国の監視カメラ市場は細分化されており、国内外の大手企業が技術的に高度な製品を提供して競争しています。同市場には、高度な技術とソリューションを提供する幅広いメーカーが存在します。中国メーカーは主要な競合であり、厳しい競争をもたらしています。多くの世界企業や国内企業が市場で競合し、さまざまなタイプの監視カメラ、ソフトウェア・ソリューション、統合サービスを提供しています。各社は、遠隔監視、クラウド・ストレージ、既存のセキュリティ・システムとの容易な統合、カスタマー・サポート・サービスなどの機能で差別化を図っています。

- 2024年4月北米における音声、セキュリティ、データソリューションの著名なインテグレーターであるBearCom社は、カナダを拠点とするトップクラスの商業セキュリティインテグレーターであるThe Surveillance Shop(TSS)を正式に買収しました。TSSはセキュリティカメラシステム、侵入アラーム、インターホン、入退室管理、境界警備、陸上移動無線を専門としています。

- 2024年2月韓国のビデオ技術メーカーIDISは、エッジAIカメラのラインアップを拡充しました。同社は、この新しいAIエッジカメラは、商業環境、公共エリア、境界での用途を見いだす汎用性があると強調しています。AIを活用することで、カメラは人間、車両、その他の物体を区別します。IDISは北米で、2MPや5MPの弾丸カメラからドームカメラやタレットカメラまで12種類の新モデルを発表しました。特筆すべきは、NIRライトマスター技術を展示するモデルもあり、低照度下での画像キャプチャを強化します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- マクロ経済動向の市場への影響評価

第5章 市場力学

- 市場促進要因

- 小売業における紛失防止と業務効率化のための利用の増加

- 人工知能や機械学習などの技術進歩

- 市場抑制要因

- プライバシー侵害とデータ悪用に対する社会的懸念

第6章 市場セグメンテーション

- タイプ別

- アナログベース

- IPベース

- エンドユーザー産業別

- 政府機関

- 銀行

- ヘルスケア

- 運輸・物流

- 産業

- 小売

- その他のエンドユーザー産業

第7章 競合情勢

- 企業プロファイル

- Axis Communications AB

- Hangzhou Hikvision Digital Technology Co. Ltd

- Hanwha Vision America

- Dahua Technology

- Bosch Sicherheitssysteme GmbH

- Pelco

- Avigilon Corporation(Motorola Solutions Inc.)

- Vivotek Inc.

- Teledyne FLIR(Teledyne Technologies)

- Zhejiang Uniview Technologies Co. Ltd

- IDIS Ltd

第8章 投資分析

第9章 市場の将来

The United States Surveillance Camera Market size is estimated at USD 6.20 billion in 2024, and is expected to reach USD 10.94 billion by 2029, growing at a CAGR of 9.92% during the forecast period (2024-2029).

Key Highlights

- Over the past decade, the United States surveillance camera market has grown significantly, propelled by technological advancements, rising security concerns, and evolving regulations. Advancements in AI and ML have revolutionized surveillance systems. They bolster video analytics, enabling sophisticated features like facial recognition, behavior analysis, and object detection, enhancing system efficacy. Furthermore, the increasing adoption of Internet of Things (IoT) technology has streamlined connectivity and enabled remote monitoring, elevating the efficiency and user-friendliness of surveillance systems.

- Moreover, the US's macroeconomic conditions have been conducive to market growth, buoyed by heightened government spending on public safety. Notably, the US government allocated a substantial budget of USD 45.7 billion for the Department of Justice in FY2025, underscoring its commitment to security initiatives and setting a positive trajectory for the surveillance camera market.

- Several trends are reshaping the market landscape-notably, a pronounced shift towards cloud-based surveillance solutions, offering scalable storage and enhanced accessibility. Wireless cameras are gaining momentum and are lauded for their flexibility and straightforward installation. Furthermore, the trend of integrating surveillance systems with other smart devices and platforms is on a sharp rise.

- Cameras have evolved from video surveillance tools to pivotal AIoT (Artificial Intelligence of Things) components in the Internet of Everything. Companies are honing their visual technology, bolstering multi-dimensional perception, expanding application horizons, and spearheading the digitization of various sectors. This concerted effort aims to lay a robust foundation for intelligent applications.

- Moreover, companies are delving deeper into optical imaging research. They focus on overcoming traditional camera limitations, such as restricted views, night-time image clarity, and limited intelligent applications. This drive manifests in product enhancements, emphasizing ultra-HD, full-color, and panoramic details. Manufacturers also enhance night-time adaptability, highlighting features like full-color zoom capabilities, large aperture zooms, and stable light amounts for vivid picture quality.

- Several major US cities are heavily surveilled, with an average of over ten cameras per 1,000 residents. These cameras serve many functions, from traffic monitoring to crime prevention. Modern surveillance cameras boast high resolutions, offer remote access to live streams, and incorporate advanced technologies like facial and automatic license plate recognition (ALPR), cementing their status as a cornerstone of contemporary security measures.

- While challenges persist, such as heightened public awareness of privacy concerns leading to potential resistance against widespread surveillance and prompting stricter regulations, the market's adoption could be impacted. Additionally, as surveillance systems grow more interconnected, they face an escalating cyber-attack risk. Yet, implementing robust cybersecurity measures, though essential, can be both costly and technically demanding.

- Under the USD 1.9 trillion American Rescue Plan, the US government allocated USD 15 billion specifically for public safety initiatives. A recent report highlights a notable drop in crime rates nationwide, attributed to the increased focus on public safety. Notably, data from approximately 13,000 law enforcement agencies, covering about 82% of the US population, revealed a 13% decrease in murders and 6% and 4% drops in reported violent and property crimes, respectively, in 2023 compared to 2022. Despite these improvements, the demand for surveillance cameras is unlikely to wane. There's a growing trend of heightened investments in security products by consumers, businesses, and governments, aiming to fortify their premises and bolster public safety.

United States Surveillance Camera Market Trends

IP-based Surveillance Cameras is Expected to Witness Growth at a Significant Rate

- IP-based surveillance cameras transmit video data over an internet network, outshining traditional analog systems in the US market. Their ascendancy is fueled by advanced features, high resolutions, and adaptability, resonating with a security-conscious market amidst technological strides and broadening sectoral adoption. These cameras offer HD and UHD video quality, outclassing analog counterparts with crisper, more detailed imagery. Boasting remote access, digital zoom, and seamless integration with security systems, IP cameras are functional and user-friendly. Their scalability further stands out, enabling system expansions without significant infrastructure overhauls.

- The surge in smart home tech and IoT has heightened the demand for IP cameras, seamlessly integrating into broader home security and automation setups. While the initial investment might be steeper, IP cameras promise long-term savings through easy installation, minimal cabling, and reduced maintenance. Organizations increasingly turn to IP-based security cameras with video analytics, enhancing real-time situational awareness, fortifying security, and gaining valuable operational insights. With analytics proving pivotal, the advent of 4K resolution cameras empowers providers to embed advanced features into their management software.

- Artificial intelligence is a standout trend, elevating functionalities like facial recognition, behavior analysis, and automated alerts. Businesses, especially those eyeing future readiness, gravitate towards AI-capable surveillance systems. Furthermore, Cloud-based solutions offer significant cost efficiencies, while operational technology costs can sometimes be hidden. Transitioning computing and video storage to the cloud typically results in 20-50% lower ownership costs than onsite systems. Eagle Eye Network, an American company, highlights these savings, noting that approximately 76% of security customers opt for subscription agreements.

- The trend towards cloud storage and management, which facilitates scalable and accessible video storage and analysis, is further propelling the IP camera market. Some VSaaS providers are sweetening the deal, offering multiyear subscriptions with price protection, a move that's resonating with customers, especially as higher-resolution cameras become more affordable. Eagle Eye Networks' data underscores this shift, revealing a three-fold increase in high-resolution IP security cameras over the past five years.

- With the crime rate increasing across different parts of the country, the demand for advanced surveillance systems is anticipated to grow, creating a conducive environment for the studied market's growth. For instance, according to the National Insurance Crime Bureau (NICB), in 2023, more than one million vehicle theft cases were reported, with overall vehicle thefts increasing by about 1 % nationwide. The district of Colombia reported the highest growth (64%) compared to the previous year.

Retail Sector is Expected to Witness Significant Demand

- In the United States, the retail sector is witnessing a pivotal shift towards adopting surveillance cameras. This move is primarily fueled by the imperatives of loss prevention, bolstering customer safety, streamlining operations, and delving into consumer behavior insights. These cameras are not just tools but the frontline defense for safeguarding assets, creating secure shopping environments, and fine-tuning store management.

- One of the primary drivers behind this surge in surveillance camera deployment is the urgent need to combat theft, shoplifting, and internal fraud. Moreover, retailers are increasingly leveraging these cameras to ensure the safety of both customers and staff, extending their surveillance to store premises and parking lots. Beyond security, these cameras are now integral in monitoring day-to-day store activities, managing queues, and optimizing staff deployment.

- The US National Retail Federation reports that retail crime costs the industry over USD 100 billion. In a 2023 survey by the NRF, 52% of responding retailers indicated they are boosting their technology and software budgets. The top 10 security measures retailers find most effective in curbing losses include CCTV and video surveillance and upgraded or integrated CCTV systems.

- Retailers are increasingly turning to emerging technologies for loss prevention. The study reveals that 37% of respondents are exploring artificial intelligence-based analytics for e-commerce fraud detection, with 13% already having these systems in place. Additionally, 35% are looking into body-worn cameras for their staff. While 18% have already deployed mobile surveillance units in their parking lots, another 10% are in the process, and 19% are considering this technology for their stores.

- Retailers are actively exploring emerging technologies. While just 3% have fully embraced facial recognition, a significant 40% are either researching, piloting, or already implementing facial recognition or feature-matching technologies, as per NRF. NRF projects a 2024 retail sales growth of 2.5% to 3.5%.

- Furthermore, according to the US Census Bureau, in 2023, total retail sales in the United States reached USD 7.24 trillion. Hence, the anticipated rise in retail sales, coupled with the surge in the adoption of advanced surveillance cameras, is poised to propel the market forward.

United States Surveillance Camera Industry Overview

The United States Surveillance Camera market is fragmented, with major domestic and international players competing by offering technologically advanced products. The market features a wide range of manufacturers offering advanced technologies and solutions. Chinese manufacturers are major contenders and provide tough competition. Many global and domestic companies compete in the market, offering various surveillance camera types, software solutions, and integration services. Companies differentiate themselves through features like remote monitoring, cloud storage, easy integration with existing security systems, and customer support services.

- April 2024: BearCom, a prominent integrator of voice, security, and data solutions in North America, officially acquired The Surveillance Shop (TSS), a top-tier commercial security integrator based in Canada. TSS specializes in security camera systems, intrusion alarms, intercoms, access control, perimeter security, and land mobile radios.

- February 2024: South Korean video technology manufacturer IDIS broadened its lineup of Edge AI cameras; the company highlights that these new AI Edge cameras are versatile, finding applications in commercial settings, public areas, and perimeters. Leveraging AI, the cameras distinguish between humans, vehicles, and other objects. IDIS unveiled 12 new models in North America, ranging from 2MP and 5MP bullets to dome and turret cameras. Notably, some models will showcase NIR Lightmaster technology, enhancing image capture in low-light conditions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 An Assessment of Impact of Macroeconomic Trends on The Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Use in Retail for Loss Prevention and Operation Efficiency

- 5.1.2 Technological Advancements Such As Use of Artificial Intelligence and Machine Learning

- 5.2 Market Restraints

- 5.2.1 Public Concern Over Privacy Invasion and Data Misuse

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Analog-based

- 6.1.2 IP-based

- 6.2 By End-user Industry

- 6.2.1 Government

- 6.2.2 Banking

- 6.2.3 Healthcare

- 6.2.4 Transportation & Logistics

- 6.2.5 Industrial

- 6.2.6 Retail

- 6.2.7 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Axis Communications AB

- 7.1.2 Hangzhou Hikvision Digital Technology Co. Ltd

- 7.1.3 Hanwha Vision America

- 7.1.4 Dahua Technology

- 7.1.5 Bosch Sicherheitssysteme GmbH

- 7.1.6 Pelco

- 7.1.7 Avigilon Corporation (Motorola Solutions Inc.)

- 7.1.8 Vivotek Inc.

- 7.1.9 Teledyne FLIR (Teledyne Technologies)

- 7.1.10 Zhejiang Uniview Technologies Co. Ltd

- 7.1.11 IDIS Ltd