欧州の仮想移動体通信事業者(MVNO)-市場シェア分析、産業動向と統計、成長予測(2024年~2029年)

Europe Mobile Virtual Network Operator (MVNO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1549950

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

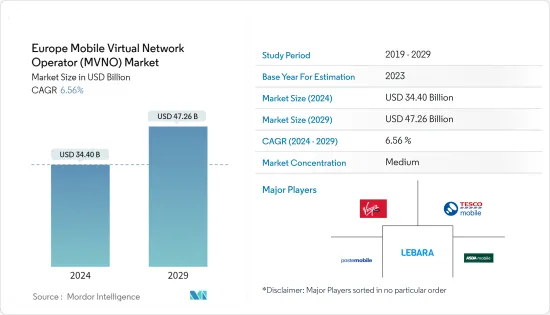

欧州のモバイルバーチャルネットワークオペレーター市場規模は、2024年に344億米ドルと推定され、2029年には472億6,000万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは6.56%で成長する見込みです。

欧州ではモバイル仮想ネットワーク事業者(MVNO)の総数が増加し、その存在感を大きく強めています。この成長は、主に非通信事業者ブランド主導のMVNOがモバイルサービスプロバイダの領域に参入してきたことが牽引しており、市場の成長機会を押し上げました。

主要ハイライト

- 5Gネットワークのスライシングにより、欧州では特定の業種を対象とするMVNOが急増する展望です。これらのMVNOは、特殊な接続ニーズに対応し、クラウドサービスやAI/ビッグデータソリューションを統合したソリューションの構築に注力しています。これらの新興MVNOは、AI、ビッグデータ、クラウドサービスを活用することで、中小企業や起業家に力を与えます。

- Ericssonによると、西欧の5G加入者は2028年までに4億4,300万人に達すると推定されています。また、クラウドコンピューティング、M2M(Machine-to-Machine)トランザクション、モバイルマネーなどのサービスの採用が増加していることから、予測期間中に欧州のMVNO(Mobile Virtual Network Operator)の需要が高まるとみられています。

- ネットワークとクラウド技術の進歩は、eSIMの採用とともに、MVNOの状況を再形成し、それを民主化し、アクセスを拡大しています。この変化により、通信事業者だけでなく、ブランドや個人も市場に参入できるようになっています。MNOの小売収入が急増し、5G投資を活用する必要性が高まる中、MVNOはより受容的なネットワーク・パートナー環境を見出しつつあります。さらに、マルチテナント型MVNE(モバイル・バーチャル・ネットワーク・イネーブラー)プラットフォームの台頭により、ホストMNOが同地域のMVNOテナントを管理する作業が大幅に簡素化されています。

- 費用対効果の高い価格設定、ニーズに合わせたサービス提供、飽和状態のモバイル市場が、欧州のMVNO市場の成長を後押ししています。また、4Gの登場と現在進行中の5G展開により、サービス品質が向上しています。既存の小売ブランドやメディアブランドは、MVNOを活用して市場への浸透と消費者の信頼を強化しています。優れた顧客サービス、革新的なビジネスモデル、消費者の認知度向上に注力することで、MVNOの魅力はさらに強固なものとなり、ニッチ市場や多様な顧客の需要に効果的に対応できるようになります。

- e-SIM技術の成長は力学を加速させ、欧州の消費者に利便性と柔軟性の向上を記載しています。物理的なSIMカードの物流上のハードルをなくすことで、デジタル専用MVNOはより迅速かつ大幅なコスト削減でサービスを開始できるようになりました。この進歩により、消費者はシームレスにプロバイダーを切り替えることができ、高額なローミング料金を回避したり、プランの上限に達した際に余分な分数やデータを得ることができます。その結果、MVNOは革新的なサービスを導入し、新たな顧客を獲得する機会が広がっています。

- 市場の主要企業は積極的にパートナーシップを結び、革新的な製品をさまざまな市場で展開し、市場シェアを拡大しています。2023年9月、fliggs MobileはTモバイルと提携し、先駆的なオールデジタルWeb3 MVNOを発表しました。この戦略的な動きは、TelcoとWeb3を融合させただけでなく、fliggs MobileをWeb3の普及を推進する極めて重要な参入企業として位置づけた。

- 非親告罪のウォレットをモバイルアプリに直接組み込むことで、fliggs Mobileは、インターネットの未来であるWeb3へのシームレスで安全なエントリーポイントを顧客に提供しました。分散型ID(DID)を提供する重要なMVNOであるfliggs Mobileは、Web3とFinTechサービスへの普遍的なアクセスをユーザーに記載しています。これにより、顧客は先進的データコントロールが可能になり、デジタルトランザクションにおけるプライバシーが強化されます。さらに、このウォレットは暗号通貨決済を合理化し、キャッシュバック・ロイヤリティ・プログラムを導入し、慈善寄付を支援しています。

- しかし、欧州のMVNO市場では激しい競合が価格競争を引き起こし、利益率は最小限に抑えられています。MVNOは、特にMNO(移動体通信事業者)からのネットワークリース料などの運営コストが高いため、収益性のハードルに直面しています。ホストMNOへの依存度が高まることは大きな懸念材料であり、予測期間中の市場の成長をさらに制限する可能性があります。

欧州の仮想移動体通信事業者(MVNO)市場動向

モバイルネットワーク加入者とモバイルデバイスの普及が増加

- モバイルネットワーク加入者の急増に伴い、欧州のMVNO市場は、手頃な価格で多様なモバイルサービスに対する需要の高まりに牽引されて成長を遂げています。MVNOは、競合価格設定、柔軟なプラン、ニッチ市場に特化したサービスを提供することで、この機会を捉えています。加入者基盤が拡大するにつれ、MVNOはその機敏なオペレーションと顧客中心主義的戦略により、従来のMNOから不満を持つユーザーを引きつける傾向が強まっています。

- さらに、加入者ベースの拡大は、MNOがMVNOにより多くのネットワーク容量を割り当てることを促し、競合価格設定とイノベーションの促進につながっています。このエコシステムは市場競争を激化させるだけでなく、サービス水準を高め、MVNOの魅力をさらに高めています。

- このようなデバイス所有の急増は、多様で費用対効果の高いモバイルサービスへの需要に拍車をかけています。スマートフォンやタブレットがユビキタス化する中、消費者は魅力的で柔軟なプランを提供するMVNOにますます注目しています。これらのプロバイダーは、従来のMNOプランよりもパーソナライズされたサービスを重視する、技術に精通し、予算に敏感な顧客を引き込み、この動向を活用しています。消費者基盤の拡大により、MNOはMVNOにより多くのネットワーク容量を割り当てざるを得なくなり、競合価格設定とサービス強化につながっています。

- 2023年6月、Vodafone Group PLCとCK Hutchison Holdings Limitedの子会社であるCK Hutchison Group Telecom Holdings Limitedは、英国の通信事業体であるVodafone UKとThree UKを合併することに合意しました。この契約では、ボーダフォンが「MergeCo」と呼ばれる新会社の株式51%を確保し、CK Hutchison Group Telecom Holdings Limitedが残りの49%を取得しました。この合併は、英国の通信セグメントに第3の大手参入企業を導入し、同国を支配するコンバージド・オペレーターに対する競争を強化するものと期待されています。さらに、すでに競合英国のMVNOにとっては、卸売りパートナーの選択肢が広がることで、選択肢が多様化することが期待されます。2030年までに、統一された事業体は、固定無線アクセス(モバイル・ホーム・ブロードバンド)を英国の家庭の82%に拡大することを目指しており、すでに国内で最も広範なフルファイバーネットワークを包含している既存のリーチを強化します。

予測期間中に著しい市場成長が見込まれる英国

- 英国は、5G、コネクテッドモバイルデバイス、スマートフォン普及率の高さなど、さまざまな先進技術の導入で常にリードしており、かなりの市場シェアを占めています。

- 英国のMVNO市場は、競合価格設定、カスタマイズ型サービス、技術に精通した消費者層に後押しされて拡大しています。モバイル市場は飽和状態に達しており、革新的な参入企業にとって有利な環境が整っています。さらに、4Gと5G技術の普及がサービス水準を高めています。Ofcomによる規制の後押しも、この競合情勢をさらに後押ししています。

- GSMA Intelligenceによると、欧州のモバイル契約普及率は2030年までに93%に達し、2023年から2%上昇すると予測されています。2023年時点では4Gが優勢であったが、2030年には5Gが欧州のモバイル技術をリードすることになります。市場は、既存参入企業と新興参入企業の混在による競争企業間の激しい敵対関係を目の当たりにしています。これらの市場参入企業は、競合を強化し市場成長を促進するために、有機的・無機的な戦略を展開しています。

- 2023年9月、カスタマー・エクスペリエンス、データ収益化、クラウドコミュニケーションソリューションの世界のプロバイダーであるComvivaは、英国を拠点とする通信サービス・プロバイダーのレバラと提携しました。この提携は、ComvivaのクラウドベースのマルチテナントSMSCプラットフォーム「UNO」を通じて、Lebaraのメッセージングサービスを刷新することを目的としています。Lebaraは戦略的な動きとして、ComvivaのUNOプラットフォームを複数のMVNOに導入しました。この決定は、メッセージングサービスのプロビジョニング、制御、管理を合理化するという目標、特に多様な地理的ロケーションにまたがるという目標によって行われました。ライバラはこの展開を活用することで、クラウドリソースを最適化し、ソフトウェア・ライセンスの効率を最大化することができます。その結果、通信プロバイダーは企業のオンボーディング時間を大幅に短縮できると見込んでいます。

- 2023年7月、企業向けに固定回線の音声、インターネット、広域ネットワークサービスを提供するSpitfire Network Services Ltd(Spitfire)は、BT Wholesaleと包括的なMVNO契約を締結しました。この契約では、Spitfireの先進的コアネットワークがBTグループのEE 4Gと5G無線アクセスネットワークとシームレスに統合されました。エンハンスト・モバイルによって、スピットファイアは新たに「スピットファイア・ユニファイド・ネットワーク」と名付けられ、接続性に革命を起こそうとしています。固定網とモバイル網のギャップを埋め、強化されたセキュリティ、柔軟な課金、英国全土の中小企業、企業、IoT顧客向けに調整された革新的なプランを約束します。

欧州の仮想移動体通信事業者(MVNO)産業概要

同市場は、Virgin Mobile、Tesco Mobile、Lebara Group、ASDA Mobileなどの参入企業が存在し、競争は中程度です。市場参入企業は、戦略的提携や買収を通じて製品ポートフォリオを強化し、持続的な競合を確保しています。

- 2024年2月フランスの通信事業者Bouygues Telecomは、La Posteグループと独占契約を結び、フランスで重要なMVNOであるLa Poste Telecomの子会社を100%取得しました。この戦略的な動きは、Bouygues Telecomに所有権を与えただけでなく、La Posteの広範な販売網へのアクセスも可能にしました。この取引により、Bouygues TelecomはLa Posteの販売網を利用し、信頼と近接性という価値観で強く認知されているとされるLa Posteのブランドを活用することができます。

- 2024年1月Virgin Media O2とTesco Mobileの親会社であるTesco PLCは、50:50の合弁事業の10年延長に調印しました。20年前に設立されたTesco Mobileは現在、英国で重要なMVNOとしての地位を固めており、550万人を超える顧客基盤を誇っています。この新たなパートナーシップは、大手携帯電話会社にとって好ましいネットワークとしてのVirgin Media O2の地位を確固たるものにしただけでなく、Tesco Mobileの顧客がVirgin Media O2が提供する広範なモバイル通信を引き続き享受できることを保証するものでもあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

- 調査の枠組み

- 2次調査

- 1次調査

- データの三角測量と洞察の生成

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- マクロ経済シナリオの分析(景気後退、ロシア・ウクライナ戦争など)

第5章 市場力学

- 市場促進要因

- モバイルネットワーク加入者の増加とモバイル機器の普及拡大

- 5G技術の普及に伴う効率的なセルラーネットワークに対する需要の高まり

- 市場課題

- ホスト・モバイル・ネットワーク・オペレーター(MNO)への依存

- 市場機会

- ネットワーク・スライシングを利用したイノベーションと競合との差別化能力

- 欧州主要国別の加入者ベースと小売店/実店舗(該当する場合)を有するMVNO概要

- 英国、ドイツ、フランス、スペインなどを含む

- MVNOの主要用途(指標となるシェア)

- BFSI

- バーチャルアシスタント

- エンターテインメント

- バーチャル・ヘルス

- 小売

- 割引ソリューション

- バンドルソリューション

- M2Mコネクティビティ

- その他

第6章 市場セグメンテーション

- タイプ別

- コンシューマー(若者、農村部、都市部)

- 企業(ビジネス)

- 国別

- 英国

- フランス

- ドイツ

- デンマーク

- イタリア

- スペイン

第7章 競合情勢

- 企業プロファイル

- Virgin Mobile

- Tesco Mobile

- Lebara Group

- Lycamobile UK Limited

- Postemobile SPA

- ASDA Mobile

- Giffgaff limited

- 1&1 Drillisch AG

- Voiceworks GmbH

- Afone Mobile

第8章 投資分析

第9章 市場の将来

目次

The Europe Mobile Virtual Network Operator Market size is estimated at USD 34.40 billion in 2024, and is expected to reach USD 47.26 billion by 2029, growing at a CAGR of 6.56% during the forecast period (2024-2029).

The total number of mobile virtual network operators (MVNOs) in Europe has increased, and they have significantly strengthened their presence. This growth has been mainly driven by the emergence of non-telco brand-led MVNOs entering the mobile service provider space, which boosted market growth opportunities.

Key Highlights

- Enabled by 5G network slicing, European businesses are poised to witness a surge of MVNOs targeting specific verticals. These MVNOs are focused on building solutions that cater to specialized connectivity needs and integrate cloud services and AI/big data solutions. These emerging MVNOs empower small businesses and entrepreneurs by harnessing AI, big data, and cloud services.

- According to Ericsson, Western Europe's 5G subscribers are estimated to reach 443 million by 2028. Also, the rising adoption of services like cloud computing, machine-to-machine (M2M) transactions, and mobile money is set to boost the demand for mobile virtual network operators (MVNOs) in Europe during the forecast period.

- Advancements in network and cloud technologies, alongside the adoption of eSIMs, are reshaping the MVNO landscape, democratizing it, and broadening access. This shift is enabling not just telcos but also brands and individuals to enter the market. As MNO retail revenues surge and the imperative to capitalize on 5G investments intensifies, MVNOs are finding a more receptive network partner environment. Additionally, the rise of multi-tenant MVNE (mobile virtual network enabler) platforms is significantly simplifying the task for host MNOs in managing their MVNO tenants in the region.

- Cost-effective pricing, tailored service offerings, and a saturated mobile market propel the growth of Europe's MVNO market. Also, the advent of 4G and the ongoing 5G deployment are enhancing service quality. Established retail and media brands are leveraging MVNOs to strengthen market penetration and consumer trust. Focusing on superior customer service, innovative business models, and increased consumer awareness further solidifies MVNOs' appeal, allowing them to effectively cater to niche markets and diverse customer demands.

- Growth in e-SIM technology accelerates changing dynamics, offering European consumers enhanced convenience and flexibility. By eliminating the logistical hurdles of physical SIM cards, digital-only MVNOs can now launch faster and at significantly reduced costs. This advancement allows consumers to seamlessly switch providers, avoiding high roaming charges or gaining extra minutes and data when reaching plan limits. Consequently, MVNOs have a broader opportunity to introduce innovative offerings and attract new clientele.

- Key market players are actively forming partnerships to expand the overall reach of their innovative products across various markets, bolstering their market share. In September 2023, fliggs Mobile partnered with T-Mobile, unveiling the pioneering all-digital Web3 MVNO. This strategic move not only merged Telco and Web3 but also positioned fliggs Mobile as a pivotal player in driving widespread Web3 adoption.

- By embedding a non-custodial wallet directly into its mobile app, fliggs Mobile has provided its clientele with a seamless and safe entry point into Web3, the future of the Internet. fliggs Mobile, the significant MVNO offering a decentralized ID (DID), empowers users with universal access to Web3 and FinTech services. This grants customer heightened data control and bolsters privacy in their digital transactions. Moreover, the wallet streamlines cryptocurrency payments, introduces cashback loyalty programs, and supports charitable donations.

- However, the intense competition in Europe's MVNO market has led to price wars and minimized profit margins. MVNOs face hurdles in profitability due to steep operational costs, notably network leasing fees from MNOs (Mobile Network Operators). The increasing dependency on host MNOs can be a significant concern, further restricting the market's growth over the forecast period.

Europe Mobile Virtual Network Operator (MVNO) Market Trends

Mobile Network Subscribers and the Penetration of Mobile Devices are Increasing

- With a surge in mobile network subscribers, the MVNO market in Europe is witnessing growth, driven by the rising demand for affordable and diverse mobile services. MVNOs are seizing this opportunity by providing competitive pricing, flexible plans, and specialized services aimed at niche markets. As the subscriber base widens, MVNOs are increasingly attracting dissatisfied users from traditional MNOs due to their nimble operations and customer-centric strategies.

- Moreover, the growing subscriber base is pushing MNOs to allocate more network capacity to MVNOs, leading to competitive pricing and fostering innovation. This ecosystem not only intensifies market competition but also elevates service standards, making MVNOs even more appealing.

- This surge in device ownership is fueling the demand for diverse and cost-effective mobile services. With smartphones and tablets becoming ubiquitous, consumers are increasingly turning to MVNOs for their attractive and flexible plans. These providers are capitalizing on the trend, drawing in tech-savvy and budget-conscious customers who value personalized offerings over traditional MNO plans. The expanding consumer base is compelling MNOs to allocate more network capacity to MVNOs, leading to competitive pricing and service enhancements.

- In June 2023, Vodafone Group PLC and CK Hutchison Group Telecom Holdings Limited, a subsidiary of CK Hutchison Holdings Limited, inked binding agreements to merge their UK telecommunication entities - Vodafone UK and Three UK. In this deal, Vodafone secured a 51% stake in the newly formed entity, dubbed "MergeCo," while CK Hutchison Group Telecom Holdings Limited got the remaining 49%. This merger is expected to introduce a third major player into the UK telecom arena, enhancing competition against the nation's dominant converged operators. Moreover, it promises to diversify options for the UK's already competitive MVNOs by broadening their wholesale partner choices. By 2030, the unified entity aims to extend fixed wireless access (mobile home broadband) to 82% of UK households, bolstering its existing reach, which already encompasses the nation's most extensive full-fiber network.

The United Kingdom Expected to Register Significant Market Growth During the Forecast Period

- The United Kingdom holds a considerable market share, consistently leading in the adoption of various advanced technologies such as 5G, connected mobile devices, and high smartphone penetration.

- The UK MVNO market is expanding, propelled by competitive pricing, customized services, and a tech-savvy consumer base. With the mobile market reaching saturation, there is a favorable environment for innovative players. Moreover, the prevalence of 4G and 5G technologies is elevating service standards. Regulatory backing from Ofcom further bolsters this competitive landscape.

- According to GSMA Intelligence, Europe's mobile subscription penetration rate is forecasted to hit 93% by 2030, marking a 2% rise from 2023. While 4G held sway in 2023, 5G is poised to take the lead in Europe's mobile technology landscape by 2030. The market witnesses intense competitive rivalry driven by a mix of established and emerging players. These industry participants are deploying a range of strategies, both organic and inorganic, to enhance their competitive edge and fuel market growth.

- In September 2023, Comviva, a global provider of customer experience, data monetization, and cloud communication solutions, partnered with Lebara, a UK-based telecom service provider. The collaboration aims to revamp Lebara's messaging services through Comviva's cloud-based multi-tenant SMSC platform, UNO. Lebara, in its strategic move, deployed Comviva's UNO platform for several MVNOs. This decision was driven by the goal of streamlining the provisioning, control, and management of messaging services, especially across diverse geographical locations. By leveraging this deployment, Lebara stands to optimize its cloud resources and maximize the efficiency of its software licenses. Consequently, the telecom provider anticipates significantly reducing the onboarding time for enterprises.

- In July 2023, Spitfire Network Services Ltd (Spitfire), a provider of fixed line voice, Internet, and wide area network services to businesses, inked a comprehensive MVNO agreement with BT Wholesale. This deal involved Spitfire's advanced core network seamlessly integrating with BT Group's EE 4G and 5G radio access network. With 'Enhanced Mobile,' Spitfire's newly labeled 'Spitfire Unified Network' is set to revolutionize connectivity. It promises enhanced security, flexible billing, and innovative plans tailored for SMEs, enterprises, and IoT clientele across the UK, bridging the gap between fixed and mobile networks.

Europe Mobile Virtual Network Operator (MVNO) Industry Overview

The market is moderately competitive with players like Virgin Mobile, Tesco Mobile, Lebara Group, ASDA Mobile, etc. Market players are bolstering their product portfolios and securing lasting competitive edges through strategic partnerships and acquisitions.

- February 2024: Bouygues Telecom, a French operator, secured an exclusive deal with La Poste group, acquiring 100% ownership of its subsidiary, La Poste Telecom, the significant MVNO in France. This strategic move not only granted Bouygues Telecom ownership but also opened up access to La Poste's extensive distribution network. The deal allows Bouygues Telecom to draw on La Poste's distribution network and tap into its brand, which is described as strong and recognized for its values of trust and proximity.

- January 2024: Virgin Media O2 and Tesco PLC, the parent company of Tesco Mobile, have signed a 10-year extension to their 50:50 joint venture. Established two decades ago, Tesco Mobile has now solidified its position as a significant MVNO in the UK, boasting a customer base exceeding 5.5 million. This renewed partnership not only cemented Virgin Media O2's status as the preferred network for major mobile players but also guaranteed that Tesco Mobile's clientele will continue to enjoy the extensive mobile coverage provided by Virgin Media O2.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation & Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Analysis of Macro-economics Scenarios (Recension, Russia-Ukraine war, etc.)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Mobile Network Subscribers and the Growing Penetration of Mobile Devices

- 5.1.2 Rising Demand for Efficient Cellular Networks owing to increasing Penetration of 5G Technology

- 5.2 Market Challenges

- 5.2.1 Dependency on Host Mobile Network Operators (MNO)

- 5.3 Market Opportunities

- 5.3.1 Capability to Innovate and Differentiate From Competitors by Using the Network Slicing

- 5.4 Overview of MVNOs with subscriber base and retail presence/physical stores (if any), by major countries in Europe

- 5.4.1 Includes UK, Germany, France, Spain, etc.

- 5.5 Key applications of MVNO (Indicative share)

- 5.5.1 BFSI

- 5.5.2 Virtual Assistants

- 5.5.3 Entertainment

- 5.5.4 Virtual Health

- 5.5.5 Retail

- 5.5.6 Discount Solutions

- 5.5.7 Bundled Solutions

- 5.5.8 M2M connectivity

- 5.5.9 Others

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Consumer (Youth, Rural, and Urban)

- 6.1.2 Enterprise (Business)

- 6.2 By Country

- 6.2.1 United Kingdom

- 6.2.2 France

- 6.2.3 Germany

- 6.2.4 Denmark

- 6.2.5 Italy

- 6.2.6 Spain

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Virgin Mobile

- 7.1.2 Tesco Mobile

- 7.1.3 Lebara Group

- 7.1.4 Lycamobile UK Limited

- 7.1.5 Postemobile SPA

- 7.1.6 ASDA Mobile

- 7.1.7 Giffgaff limited

- 7.1.8 1&1 Drillisch AG

- 7.1.9 Voiceworks GmbH

- 7.1.10 Afone Mobile

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日