|

市場調査レポート

商品コード

1693565

日本の航空:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Japan Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本の航空:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 233 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

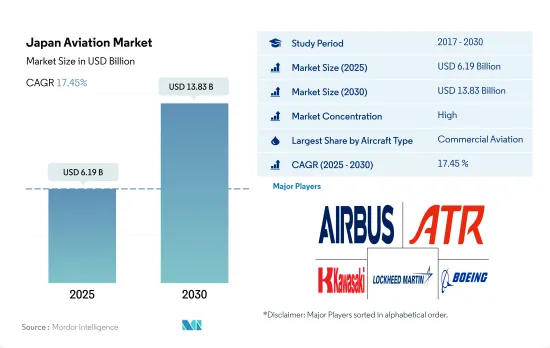

日本の航空市場規模は2025年に61億9,000万米ドルと推定され、2030年には138億3,000万米ドルに達し、予測期間(2025~2030年)のCAGRは17.45%で成長すると予測されます。

日本では、航空需要の高まりにより民間航空セグメントが市場を独占すると予想されます。

- 航空会社とそのサプライチェーンで構成される民間航空産業は、予測期間中、日本のGDPに721億米ドル寄与すると推定・予測されます。加えて、航空輸送部門へのインプットと、航空支援で来日する外国人観光客は、日本のGDPの2.4%に貢献すると予想されます。

- 日本は、COVID-19の大流行がこの地域の民間航空産業に影響を与えているにもかかわらず、世界で力強く成長している民間航空市場の1つです。旅客輸送量の回復は、日本の民間航空産業の復活を助長すると予想されます。2021年の日本の航空旅客輸送量は139%増加しました。旅客輸送量の増加は、国境規制の緩和に起因しています。

- 富裕層の増加、訓練校の増加、ビジネスジェットインフラの開発に対する政府の注力、規制緩和活動といった要因が、予測期間中、日本における一般航空の成長を促進すると予想されます。日本では、定期便以外のビジネス旅行のニーズが高まっているため、チャーター便運航会社が絶えず航路を拡大し、新しい航空機を保有機に加えつつあります。これが日本におけるビジネスジェット機とターボプロップ機の需要を支えています。他方、軽スポーツ機や練習機の需要は引き続き高く、一般航空機材の成長に寄与しています。

- 日本の防衛省は2021年初頭に、2022年度予算として493億米ドル超を提案したが、これは記録的なものであり、GDPの1%という長年の上限を上回る可能性があります。2027年までには、日本は米国と中国に次ぐ世界第3位の防衛支出国になる可能性があります。

日本の航空市場動向

規制緩和と旅客旅行の増加が需要を牽引。

- アジア太平洋における日本の戦略的立地は、国際旅行・観光の人気目的地となっています。所得の増加、観光客の増加、世界のビジネス交流といった要因に後押しされ、日本国内と海外の目的地への航空旅行の需要は伸び続けています。2022年には、2020年の5,100万人に対し、1億2,200万人の航空旅客が日本を通過します。2022年と2020年の間の伸びは139%でした。2022~2021年にかけての伸びは変わらなかりました。

- 2019年、日本の37の空港が国際路線を有していました。しかし2022年には、この数はわずか17に減少しました。日本政府がCOVID-19パンデミックの間、ごく少数の空港から日本への国際アクセスを許可するという決定を下した結果、また、日本の地方空港から運航されていた国際路線の多くが、パンデミック以前の運航にはまだ戻っていない中国や韓国の地方市場に就航していたこともあり、国際線トラフィックはより少数の空港に集中するようになりました。

- 旅行需要の落ち込みと、それに関連して大手航空会社が直面した損失は、航空会社が予定していた航空機の納入を延期し、数機種の航空機を早期に退役させることによって既存の航空機を再編成する結果となりました。例えば、日本の航空のナショナル・キャリアは、旧式のBoeing社製737型短距離路線用航空機を、最新の燃費効率の良い機種に置き換えることを検討しています。同航空会社が保有するBoeing737型機は45機で、平均機齢は約12.5年です。同航空は、老朽化した機材を置き換えるために、737 MaxシリーズとAirbusSEのライバル機A320neoのどちらかを選択し、30機と50機のナローボディ機を発注する見込みです。

地政学的脅威が日本の防衛費増額の原動力となっています。

- 日本の総合軍事力は米国、ロシア、中国、インドに次いで世界第6位です。日本の防衛予算は、2022年の140カ国中10位でした。2022年、日本は軍事費として460億米ドルを計上し、2021年から5.9%増加しました。これまで軍事費の上限をGDPの1.0%としていた日本は、施策を大きく転換している最中です。日本の2022年国家安全保障戦略は、軍事費を含む安全保障への支出を2027年までにGDPの2.0%まで増やすことを目標としています。この増額は、中国、北朝鮮、ロシアからの脅威が増大しているという日本の認識への対応が主要理由です。2022年のGDP比1.1%で、日本の軍事負担は3年連続で1.0%を超え、1960年以来の高水準となりました。

- 中国の侵略が強まる中、また、南シナ海と東シナ海に関わるほぼすべての紛争における利害関係者として、日本が軍用機を調達する必要性は著しく高まっています。この点に関して、固定翼機セグメントでは、日本はLockheed Martin社に対し、F-XまたはF-3として一般に知られる第6世代ステルス戦闘機プログラムのF-35A 63機とF-35B 42機を含むF-35戦闘機105機について、231億1,000万米ドルの大量調達契約を発注しました。さらに同国は、軍用回転翼機部門でベル・ヘリコプターズに150機のベルと412機のUH-X輸送ヘリコプターを発注しました。2021年までに3機のヘリコプターが納入され、残りの機体は2039年までに納入される予定です。これらの多目的ヘリコプターは、日本の陸上自衛隊(JGSDF)が現在保有するUH-1J機の代替機として発注されます。

日本の航空産業概要

日本の航空市場はかなり統合されており、上位5社で89.11%を占めています。この市場の主要企業は、Airbus SE、ATR、Kawasaki Heavy Industries、Ltd.、Lockheed Martin Corporation、The Boeing Companyなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 航空旅客輸送量

- 航空貨物輸送量

- 国内総生産

- 収入旅客キロ(rpk)

- インフレ率

- アクティブフリートデータ

- 国防支出

- 個人富裕層(hnwi)

- 規制の枠組み

- バリューチェーン分析

第5章 市場セグメンテーション

- 航空機タイプ

- 民間航空機

- サブ航空機タイプ別

- 貨物機

- 旅客機

- ボディタイプ別

- ナローボディ機

- ワイドボディ機

- 一般旅客機

- サブ航空機タイプ別

- ビジネスジェット

- ボディタイプ別

- 大型ジェット機

- 小型ジェット機

- 中型ジェット機

- ピストン固定翼機

- その他

- 軍用機

- サブ航空機タイプ別

- 固定翼機

- ボディタイプ別

- 多用途航空機

- 輸送機

- その他

- 回転翼機

- 機体タイプ別

- マルチミッションヘリコプター

- 輸送用ヘリコプター

- その他

- 民間航空機

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Airbus SE

- ATR

- Bombardier Inc.

- Kawasaki Heavy Industries, Ltd.

- Lockheed Martin Corporation

- Textron Inc.

- The Boeing Company

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92659

The Japan Aviation Market size is estimated at 6.19 billion USD in 2025, and is expected to reach 13.83 billion USD by 2030, growing at a CAGR of 17.45% during the forecast period (2025-2030).

The commercial aviation segment is expected to dominate the market in Japan due to rising demand for air travel

- The commercial aviation industry, comprising airlines and their supply chains, is estimated to contribute USD 72.1 billion to Japan's GDP during the forecast period. In addition, inputs to the air transport sector and foreign tourists coming by air support are expected to contribute 2.4% of the country's GDP.

- Japan is one of the world's strongly growing commercial aviation markets, despite the COVID-19 pandemic impacting the region's commercial airline industry. The recovery of passenger traffic is anticipated to aid in the revival of Japan's commercial aviation industry. Japan witnessed a total increase of 139% in air passenger traffic in 2021. The rise in passenger traffic is attributed to ease in border restrictions.

- Factors such as the increasing number of high-net-worth individuals, training schools, the government's focus on developing business jet infrastructure, and deregulation activities are expected to drive the growth of general aviation in Japan during the forecast period. Charter operators in the country are constantly expanding their routes and are adding new aircraft to their fleets, driven by the growing need for non-scheduled business travel. This has helped the demand for business jets and turboprops in Japan. On the other hand, the demand for light sport and trainer aircraft remained high, contributing to the growth of the general aviation fleet.

- Japan's Defense Ministry proposed a budget for fiscal 2022 of more than USD 49.3 billion at the beginning of 2021, which is a record and potentially exceeds the long-standing cap of 1% of GDP. By 2027, Japan might be the world's third-largest defense spender, after only the United States and China.

Japan Aviation Market Trends

Ease of restrictions and rising passenger travel driving demand

- The strategic location of Japan in the Asia-Pacific region makes it a popular destination for international travel and tourism. The demand for air travel within Japan and to international destinations continues to grow, driven by factors such as rising incomes, increased tourism, and global business interactions. In 2022, 122 million air passengers traveled through Japan, compared to 51 million in 2020. The growth between 2022 and 2020 was 139%. The growth remained the same between 2022 and 2021.

- In 2019, 37 Japanese airports had international routes. However, in 2022, this number fell to just 17. International traffic has also become more concentrated in fewer airports, partly as a result of the Japanese government's decision to allow international access to Japan through just a small number of airports during the COVID-19 pandemic and partly because many of the international routes that operated from regional airports in Japan served regional markets in China and South Korea, which are not yet back to pre-pandemic operations.

- The drop in travel demand and the associated losses faced by major airlines resulted in airlines deferring their expected aircraft deliveries and restructuring their existing fleet by retiring a few aircraft models early. For instance, Japan Airlines Co.'s national Carrier is looking to replace its older Boeing Co. 737 short-haul fleet with modern and fuel-efficient aircraft models. The airline has a fleet of 45 Boeing 737 jets with an average age of about 12.5 years. The airline is expected to choose between the 737 Max range and Airbus SE's rival A320neo to replace the aging fleet, with an expected order of 30 and 50 narrow-body jets.

Geopolitical threats is driving the growth of defense expenditure in Japan

- Japan is ranked sixth globally in overall military power after the United States, Russia, China, and India. The country's defense budget ranked tenth in the 2022 ranking of 140 countries. In 2022, Japan allocated USD 46.0 billion to its military, up by 5.9% from 2021. The country is in the middle of a significant shift in policy, which had previously capped military spending at 1.0% of GDP. Japan's 2022 National Security Strategy aims to increase spending on security, which includes funding for the military, to up to 2.0% of GDP by 2027. The planned increase is largely in response to Japan's perception of growing threats from China, North Korea, and Russia. At 1.1% of GDP in 2022, Japan's military burden surpassed 1.0% for the third consecutive year and was at its highest level since 1960.

- In the face of rising Chinese aggression, and as a stakeholder in almost all disputes involving the South and East China seas, the need for Japan to procure military aircraft has increased significantly. On this note, in the fixed-wing aircraft segment, Japan ordered a mass procurement contract worth USD 23.11 billion with Lockheed Martin for 105 F-35 combat aircraft, which includes 63 F-35A and 42 F-35B under the sixth-generation stealth fight aircraft program, popularly known as F-X or F-3. In addition, the country placed an order with Bell Helicopters for 150 Bell and 412 UH-X transport helicopters in the military rotorcraft segment. Till 2021, three helicopters were delivered, and the remaining aircraft are expected to be delivered by 2039. These multi-purpose helicopters are ordered to replace Japan's Ground Self-Defense Force's (JGSDF) current fleet of UH-1J aircraft.

Japan Aviation Industry Overview

The Japan Aviation Market is fairly consolidated, with the top five companies occupying 89.11%. The major players in this market are Airbus SE, ATR, Kawasaki Heavy Industries, Ltd., Lockheed Martin Corporation and The Boeing Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 Air Transport Freight

- 4.3 Gross Domestic Product

- 4.4 Revenue Passenger Kilometers (rpk)

- 4.5 Inflation Rate

- 4.6 Active Fleet Data

- 4.7 Defense Spending

- 4.8 High-net-worth Individual (hnwi)

- 4.9 Regulatory Framework

- 4.10 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Aircraft Type

- 5.1.1 Commercial Aviation

- 5.1.1.1 By Sub Aircraft Type

- 5.1.1.1.1 Freighter Aircraft

- 5.1.1.1.2 Passenger Aircraft

- 5.1.1.1.2.1 By Body Type

- 5.1.1.1.2.1.1 Narrowbody Aircraft

- 5.1.1.1.2.1.2 Widebody Aircraft

- 5.1.2 General Aviation

- 5.1.2.1 By Sub Aircraft Type

- 5.1.2.1.1 Business Jets

- 5.1.2.1.1.1 By Body Type

- 5.1.2.1.1.1.1 Large Jet

- 5.1.2.1.1.1.2 Light Jet

- 5.1.2.1.1.1.3 Mid-Size Jet

- 5.1.2.1.2 Piston Fixed-Wing Aircraft

- 5.1.2.1.3 Others

- 5.1.3 Military Aviation

- 5.1.3.1 By Sub Aircraft Type

- 5.1.3.1.1 Fixed-Wing Aircraft

- 5.1.3.1.1.1 By Body Type

- 5.1.3.1.1.1.1 Multi-Role Aircraft

- 5.1.3.1.1.1.2 Transport Aircraft

- 5.1.3.1.1.1.3 Others

- 5.1.3.1.2 Rotorcraft

- 5.1.3.1.2.1 By Body Type

- 5.1.3.1.2.1.1 Multi-Mission Helicopter

- 5.1.3.1.2.1.2 Transport Helicopter

- 5.1.3.1.2.1.3 Others

- 5.1.1 Commercial Aviation

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 ATR

- 6.4.3 Bombardier Inc.

- 6.4.4 Kawasaki Heavy Industries, Ltd.

- 6.4.5 Lockheed Martin Corporation

- 6.4.6 Textron Inc.

- 6.4.7 The Boeing Company

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms