|

市場調査レポート

商品コード

1437615

NATO軍用機の近代化と改修:市場シェア分析、業界動向と統計、成長予測(2024~2029年)NATO Military Aircraft Modernization And Retrofit - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| NATO軍用機の近代化と改修:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

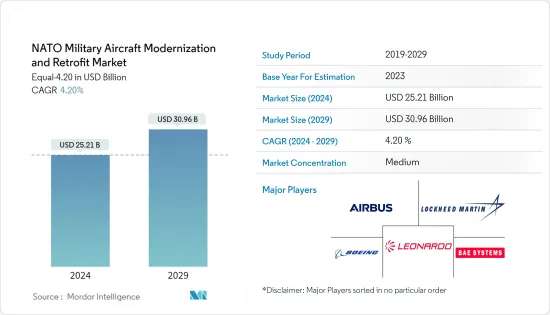

NATO軍用機の近代化と改修市場規模は、2024年に252億1,000万米ドルと推定され、2029年までに309億6,000万米ドルに達すると予想されており、予測期間(2024年から2029年)中に4.20%のCAGRで成長します。

NATO諸国は、経済的に手頃な価格のクロスカントリー防衛シンクタンクとしてそれを達成するために、現在の艦隊に新しくて先進的な技術を統合することに取り組んでいます。したがって、多くの近代化およびアップグレードプログラムが現在進行中であるか、予測期間中に開始される予定です。

適切な代替機が目前にない老朽化した航空機を背景に、各国は有効寿命を延ばし、航空機の老朽化を防ぐために既存世代の航空機を近代化する必要に迫られています。したがって、米国とそのNATO同盟国は、急速に台頭する技術戦場での生存性を高めるために、新しいブロック兵器とシステムを備えた戦闘機および多用途航空機隊をアップグレードすることに資源を集中しています。ステルス技術と精密航空兵器の進歩により、予測期間中に市場参加者にいくつかの機会が生まれると予想されます。

NATO軍用機の近代化と改修市場の動向

固定翼セグメントは予測期間中も優位性を維持

NATO諸国は固定翼航空機の熱心なユーザーです。この分野の需要は、米国、カナダ、英国、フランス、ドイツ、イタリアなどの主要なNATO諸国の国防支出の増加によって牽引されています。例えば、これらの国々の国防支出は、2022年に1兆1,100億米ドルを占めました。これらの著名なNATO加盟国は、毎年一貫して世界の防衛支出額が最も高い国の一つにランクされており、先進兵器の研究開発と高度な軍事資産の調達に多額の投資が行われていることを意味しています。

たとえば、2023年 3月、フランス政府は4年間の開発を経て最新鋭のラファール戦闘機を受け取り、重要なマイルストーンを達成しました。 F4規格は、2021年4月にフランスのDGAによる飛行試験を受け、2025年までに完全に実用化される予定です。F4は、タレス・スコーピオンのヘルメット搭載ディスプレイ、MBDAのMICA NG空対空ミサイル、サフランのAASMなどの新機能を誇る。 1,000キログラムのバージョンを備えたハンマー精密誘導弾。同様に、2023年6月に英国は、英国空軍(RAF)と英国海軍(RN)の要員の訓練に使用されていたビーチクラフト・キング・エア350ERの保有機群をアップグレードすると発表しました。この艦隊は大幅な機能アップグレードが行われる予定で、更新された航空機は2023年から2033年まで運用できるようになる予定です。アップグレードには、アクティブ電子走査アレイレーダー、電気光学カメラ、客室エリアとミッションコンソールの再構成が含まれます。 1億5,500万米ドルの後部乗組員維持契約の一環として。このような発展は、予測期間中に調査された市場の成長見通しを推進すると想定されています。

予測期間米国が市場を独占

2022年には、他のNATO諸国と比較して数倍となる巨額の国防費により、米国が最大の市場シェアを占めました。米国の国防費は前年比9%増加し、2022年には8,770億米ドルに達しました。米国における軍用機の近代化と改修市場の需要は主に国防費の増加と、特に中国とロシアの間の地政学的な緊張の高まりによって引き起こされています。それが軍用機の調達を促進します。

米国国防総省(DoD)は、2024年度に、F-22、F-35、F-22、F-35、F-22などの戦闘機を中心とした致死的な空軍の開発、近代化、調達を目的とした611億米ドルの国防予算を要求しました。 15EX、B-21爆撃機、KC-46A、その他の航空機。これに合わせて、2023年11月、米国空軍はボーイングに対し、空中給油と貨物輸送能力を強化するためKC-46ペガサス空中給油機15機を納入する23億米ドルの契約を締結しました。新しい航空機の調達とは別に、米国は軍用機の即応性を維持するために軍用機部隊をアップグレードするために多額の投資も行っています。たとえば、2023年11月、米国陸軍はボーイングと陸軍のアパッチヘリコプター群をアップグレードする契約を締結しました。契約に基づき、陸軍は新しいエンジンを購入し、Apache用の最新ソフトウェアバージョンをインストールすることを決定しました。このような契約と開発は、予測期間中に米国の需要を促進すると予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 航空機の種類

- 固定翼

- 回転翼

- 地域

- 米国

- カナダ

- 英国

- フランス

- ドイツ

- イタリア

- その他のNATO諸国

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- RTX Corporation

- L3Harris Technologies Inc.

- BAE Systems PLC

- Lockheed Martin Corporation

- Elbit Systems Ltd

- Honeywell International Inc.

- Northrop Grumman Corporation

- Safran SA

- General Dynamics Corporation

- Leonardo SpA

- The Boeing Company

- Airbus SE

第7章 市場機会と将来の動向

The NATO Military Aircraft Modernization And Retrofit Market size is estimated at USD 25.21 billion in 2024, and is expected to reach USD 30.96 billion by 2029, growing at a CAGR of 4.20% during the forecast period (2024-2029).

The NATO countries are committed to integrating new and advanced technologies in their current fleet to accomplish it as an economically affordable cross-country defense think tank. Thus, many modernization and upgrade programs are currently underway or envisioned to be initiated during the forecast period.

The aging fleet with no plausible replacement on the horizon has driven the countries to modernize the existing generation of aircraft to extend their effective life and prevent the fleet from becoming obsolete. Therefore, the United States and its NATO allies are focusing their resources on upgrading their combat and multirole aircraft fleet with new block weaponry and systems to enhance their survivability in a rapidly emerging technological battlefield. The advancements in stealth technology and precision aerial weaponry are expected to create several opportunities for the market players during the forecast period.

NATO Military Aircraft Modernization And Retrofit Market Trends

Fixed-wing Segment to Continue its Dominance During the Forecast Period

The NATO countries are avid users of fixed-wing aircraft. The demand for this segment is driven by the rising defense expenditures of major NATO countries such as the United States, Canada, the United Kingdom, France, Germany, and Italy. For instance, these countries' defense expenditures accounted for USD 1.11 trillion in 2022. These prominent NATO member countries have consistently ranked amongst the highest global defense spending nations each year, signifying substantial investments toward the R&D of advanced weaponry and procurement of sophisticated military assets.

For instance, in March 2023, the French government achieved a significant milestone when they received their most advanced Rafale fighter jets after four years of development. The F4 standard underwent flight tests by France's DGA in April 2021 and is expected to be fully available by 2025. The F4 boasts new features such as the Thales Scorpion helmet-mounted display, MBDA's MICA NG air-to-air missile, and Safran's AASM hammer precision-guided munition with a 1,000-kilogram variant. Similarly, in June 2023, the United Kingdom announced that it is upgrading its fleet of Beechcraft King Air 350ERs that was used to train personnel for the Royal Air Force (RAF) and Royal Navy (RN). The fleet is expected to undergo a major capability upgrade, with the updated aircraft to be capable of serving from 2023 to 2033. The upgrades include an active electronically scanned array radar, an electro-optical camera, and reconfiguration of the cabin area and mission consoles as part of a USD 155 million rear crew sustainment deal. Such developments are envisioned to drive the growth prospects of the market studied during the forecast period.

United States Dominates the Market During the Forecast Period

In 2022, the United States accounted for the largest market share due to its gigantic defense spending, which is multifold compared to other NATO countries. The US defense expenditure witnessed a 9% YoY growth, accounting for USD 877 billion in 2022. The demand for military aircraft modernization and retrofit market in the United States is primarily driven by the rising defense expenditure and increasing geopolitical tensions, especially between China and Russia over the years, which in turn drives military aircraft procurement.

In FY2024, the US Department of Defense (DoD) has requested a defense budget of USD 61.1 billion aimed at developing, modernizing, and procuring lethal air forces, including a focus on fighters, such as F-22, F-35, F-15EX, B-21 bomber, KC-46A, and other aircraft. In line with this, in November 2023, the US Air Force awarded Boeing a USD 2.3 billion contract to deliver 15 KC-46 Pegasus tanker aircraft to bolster its aerial refueling and cargo transport capacities. Apart from new aircraft procurements, the United States is also making significant investments to upgrade its military aircraft fleet to maintain its fleet readiness. For instance, in November 2023, the US Army awarded Boeing a contract to upgrade the Army's fleet of Apache helicopters. Under the contract, the Army decided to buy new engines and install the latest software version for the Apache. Such contracts and developments are expected to drive the demand in the US during the forecast period.

NATO Military Aircraft Modernization And Retrofit Industry Overview

The NATO military aircraft modernization and retrofit market is semi-consolidated, with major players, such as Lockheed Martin Corporation, Leonardo SpA, BAE Systems PLC, The Boeing Company, and Airbus SE dominating the market. The stringent safety and regulatory policies in the defense segment are expected to restrict the entry of new players. However, a trend of strategic collaboration has been observed in the market wherein the market players enter into a mutual partnership to develop advanced aircraft and associated subsystems as per the specifications of the end-users.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Aircraft Type

- 5.1.1 Fixed-wing

- 5.1.2 Rotary-wing

- 5.2 Geography

- 5.2.1 United States

- 5.2.2 Canada

- 5.2.3 United Kingdom

- 5.2.4 France

- 5.2.5 Germany

- 5.2.6 Italy

- 5.2.7 Rest of NATO Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 RTX Corporation

- 6.2.2 L3Harris Technologies Inc.

- 6.2.3 BAE Systems PLC

- 6.2.4 Lockheed Martin Corporation

- 6.2.5 Elbit Systems Ltd

- 6.2.6 Honeywell International Inc.

- 6.2.7 Northrop Grumman Corporation

- 6.2.8 Safran SA

- 6.2.9 General Dynamics Corporation

- 6.2.10 Leonardo SpA

- 6.2.11 The Boeing Company

- 6.2.12 Airbus SE