|

市場調査レポート

商品コード

1693567

米国の軍用機:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)US Military Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の軍用機:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 164 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

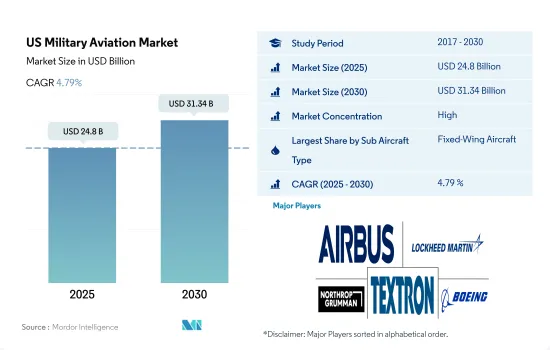

米国の軍用機市場規模は2025年に248億米ドルと推定・予測され、2030年には313億4,000万米ドルに達し、予測期間(2025-2030年)のCAGRは4.79%で成長すると予測されています。

国防予算の増加と巨額の航空機調達が市場を牽引

- 中国と米国は、将来の戦争に備えるために新技術の研究開発にますます力を入れており、両国の技術競争は加速しています。2022年には、米国が世界の国防軍事支出の39%を占め、8,770億米ドル(0.7%)増加します。この合計には、199億米ドルと推定されるウクライナへの軍事援助が含まれています。2022年、同国は空軍省予算を発表し、2023年度の予算要求を約1,940億米ドルと概算しました。

- 防衛予算の大部分は、F-35ジェット機、B-21レイダー爆撃機、KC-46Aペガサスタンカー、その他のヘリコプターに割り当てられています。これらの新型機の一部は、50年以上運用されてきた既存の航空機を置き換えることになります。2022年、空軍はC-130航空機の総フリートを削減し、約92機のC-130航空機をアップグレードする計画でした。米国空軍は、新型機C-130Jのために旧型機を退役させる計画です。2022年末までに米国は47機のF-35を受領し、予測期間中に1,943機の未納機が予想されます。

- 2023年から2029年にかけて、現在進行中および将来のいくつかの調達計画が、同国の軍用ヘリコプター市場を牽引すると予想されます。2023年3月、ボーイングは、米国陸軍が4年契約で19億5,000万米ドルを発注し、AH-64Eアパッチ・ガーディアン攻撃ヘリコプターを新たに製造すると発表しました。2018年9月、米国空軍(USAF)はUH-1Nヒューイヘリコプターの後継機としてMH-139を選定しました。2022年12月現在、9機のヘリコプターが納入され、残りの納入は予測期間中に予定されています。予測期間中、同国は合計2,330機を調達する見込みです。

米国軍用機市場の動向

国防費の増加は、米国が直面する様々な地政学的脅威に起因します。

- 2022年、米国は世界の国防費軍事費の39%を占め、2022年には8,770億米ドル(0.7%)増加しました。2022年、米国は空軍省予算を発表し、その概要によると、2023年度の予算要求は約1,940億米ドルで、2022年度の要求から202億米ドル(11.7%)増加しました。米国国防総省は、2023年度の取得資金(調達と研究開発・試験・評価(RDT&E))として2,760億米ドルを提案しており、内訳は調達が1,459億米ドル、RDT&Eが1,301億米ドルとなっています。予算で要求された資金は、国家防衛戦略の提言を実施するためのバランスの取れたポートフォリオ・アプローチです。

- 要求額2,760億米ドルのうち、565億米ドル(研究開発費168億米ドル、調達費396億米ドル)は、航空機の研究開発、航空機の取得、初期予備品、航空機支援装備品などの航空機および関連システムに充てられます。最も高額な防衛計画である第5世代F-35統合打撃戦闘機(JSF)は、海軍(F-35C)、海兵隊(F-35B&C)、空軍(F-35A)用の61機に対して110億米ドルの要求があります。2023年度の予算には、24機のF-15EX、79機の兵站支援機、119機の回転翼航空機、12機のUAV/UASの購入も含まれています。

- 米国陸軍の2022年度予算要求は1,730億米ドル、海軍は2,120億米ドル、空軍は2,130億米ドルでした。航空機および関連システム部門には、以下のサブグループが含まれる:戦闘機(230億米ドル)、貨物機(50億米ドル)、支援機(16億米ドル)で、残りはUAS、航空機支援、技術開発、航空機改造の予算です。

艦隊の近代化と近代戦の拡大が、同国の現役艦隊強化の原動力となっています。

- 米国空軍(USAF)は、現代戦の要求に応えるため、次世代航空機の開発と調達を続けています。新型機の投入により、保有機体の老朽化が遅れています。米国空軍は、現在の兵力規模を維持するのに十分な数の新型機を購入していないです。今後、保有機数のさらなる減少が予想されます。数少ない航空機の平均機齢は、爆撃機が45年、タンカーが49年、ヘリコプターが32年、練習機が32年、戦闘機/攻撃機が29年と高いです。海軍と陸軍も、航空機の老朽化と保有機体の維持という課題に直面しています。しかし、空軍は老朽化と代替機の取得の遅れの点ではるかに悪い状況にあります。2022年12月現在、米国は世界最大の軍用機保有国であり、合計13,300機が運用されています。この艦隊のかなりの部分が戦闘ヘリコプター(42%)と戦闘機(21%)で占められています。一方、訓練機とヘリコプターは20%を占め、輸送機はわずか7%にすぎないです。一方、タンカーと特殊任務機はそれぞれ5%を占めています。

- 2023年度について米国空軍は、A-10 21機、F-22 33機、E-8 8機、E-3セントリー15機、C-130Hハーキュリーズ10機、T-1ジェイホーク50機、KC-135タンカー13機を含む最大150機を退役させる許可を議会に求めました。米空軍はまた、次世代航空優勢(NGAD)を開発し、F-15EXを展開するための資金を確保するため、F-35Aの購入を削減しました。米空軍は2023年に33機のF-35Aを購入する計画で、2022年度に米空軍が要求した48機よりも少ないです。現代戦のダイナミックな性質に伴い、米国は効果的な航空機の小規模な艦隊を維持することを目指しており、予測期間中に艦隊全体の規模が大幅に縮小する可能性があります。

米国の軍用機産業の概要

米国の軍用機市場はかなり統合されており、上位5社で98.65%を占めています。この市場の主要企業は以下の通り。 Airbus SE, Lockheed Martin Corporation, Northrop Grumman Corporation, Textron Inc. and The Boeing Company(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 国内総生産

- アクティブフリートデータ

- 国防支出

- 規制の枠組み

- バリューチェーン分析

第5章 市場セグメンテーション

- サブ航空機タイプ

- 固定翼機

- マルチロール航空機

- 訓練用航空機

- 輸送機

- その他

- 回転翼機

- マルチミッションヘリコプター

- 輸送用ヘリコプター

- その他

- 固定翼機

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Airbus SE

- Leonardo S.p.A

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Textron Inc.

- The Boeing Company

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92661

The US Military Aviation Market size is estimated at 24.8 billion USD in 2025, and is expected to reach 31.34 billion USD by 2030, growing at a CAGR of 4.79% during the forecast period (2025-2030).

Rising defense budgets and huge aircraft procurement are driving the market

- Competition in technology between China and the United States is accelerating as both countries are increasingly focused on the R&D of emerging technologies to prepare for future warfare. In 2022, the United States accounted for 39% of global defense military spending, which increased by USD 877 billion in 2022, or 0.7%. The total includes military assistance to Ukraine, estimated at USD 19.9 billion. In 2022, the country released the Department of the Air Force budget, which outlined the budget request for FY 2023 at approximately USD 194.0 billion.

- A significant portion of the defense budget is allocated for F-35 jets, B-21 Raider bombers, KC-46A Pegasus tankers, and other helicopters. Some of these new aircraft will replace the existing fleet that has been operational for over 50 years. In 2022, the Air Force planned to cut down the total fleet of C-130 aircraft and upgrade about 92 C-130 aircraft. The US Air Force plans to retire the older models for the new C-130J aircraft fleet. By the end of 2022, the United States received 47 F-35s, with outstanding deliveries for 1,943 aircraft expected during the forecast period.

- Several ongoing and future procurement programs of the country are expected to drive its military helicopter market during 2023-2029. In March 2023, Boeing announced that the US Army had awarded a contract to build new AH-64E Apache Guardian attack helicopters under a USD 1.95 billion four-year order. In September 2018, the US Air Force (USAF) selected the MH-139 to replace its fleet of UH-1N Huey helicopters. As of December 2022, nine helicopters were delivered, with the rest of the deliveries expected during the forecast period. During the forecast period, a total of 2,330 aircraft are expected to be procured by the country.

US Military Aviation Market Trends

The increase in defense spending can be attributed to the various geopolitical threats faced by the US

- In 2022, the US accounted for 39% of global defense spending military spending, which increased by USD 877 billion in 2022, or 0.7%. In 2022, the US released the Department of the Air Force budget, which outlined that for FY 2023, the budget request was approximately USD 194.0 billion, a USD 20.2 billion or 11.7% increase from the FY 2022 request. The US DoD proposed USD 276.0 billion in acquisition funds for FY2023 (Procurement and Research, Development, Test, and Evaluation (RDT&E)), which comprised USD 145.9 billion for Procurement and USD 130.1 billion for RDT&E. The financing requested in the budget is a balanced portfolio approach to implementing the National Defense Strategy recommendations.

- Of the USD 276 billion in the request, USD 56.5 billion (USD 16.8 billion for RDT&E and USD 39.6 billion for Procurement) will finance aircraft and related systems, including money for aircraft R&D, aircraft acquisition, initial spares, and aircraft support equipment. The single most expensive defense program, the fifth generation F-35 Joint Strike Fighter (JSF), has USD 11.0 billion in requests for 61 aircraft for the Navy (F-35C), Marine Corps (F-35B & C), and Air Force (F-35A). Funding for FY 2023 also included the purchase of 24 F-15EX, 79 logistics and support aircraft, 119 rotary wing aircraft, and 12 UAV/UAS.

- The US Army's budget request for FY 2022 was USD 173 billion, the Navy's was USD 212 billion, and the Air Force's request was USD 213 billion. The aircraft and related systems category includes the following subgroups: Combat Aircraft (USD 23.0 billion), Cargo Aircraft (USD 5.0 billion), Support Aircraft (USD 1.6 billion), with the remaining budget for UAS, aircraft support, technology development, and aircraft modifications.

Fleet modernization and growing modern warfare are the driving factors for the country's active fleet enhancement

- The US Air Force (USAF) continues to develop and procure next-generation aircraft to meet the demands of modern warfare. Fielding of new aircraft has slowed the increase in fleet age. The US Air Force is not buying enough new aircraft to sustain its force structure at its current size. A further decrease in fleet size is likely to be witnessed in the future. The average age of a few aircraft is high, at 45 years for bombers, 49 years for tankers, 32 years for helicopters, 32 years for trainers, and 29 years for fighter/attack aircraft. The Navy and the Army also face challenges with aging aircraft and maintaining their fleets. However, the Air Force is in far worse shape in terms of aging and the slow acquisition of replacements. As of December 2022, the United States had the biggest fleet of military aircraft in the world, with a total of 13,300 operational planes. A considerable chunk of this fleet is made up of combat helicopters (42%) and combat planes (21%). In contrast, training planes and helicopters account for 20%, while transport planes make up only 7%. Meanwhile, tankers and special mission aircraft each represent 5% of the fleet.

- For FY2023, the US Air Force asked for permission from Congress to retire up to 150 aircraft, including 21 A-10, 33 F-22, 8 E-8, 15 E-3 Sentries, 10 C-130H Hercules, 50 T-1 Jayhawks, and 13 KC-135 tankers. The USAF also trimmed its F-35A purchases to free up funds to develop Next Generation Air Dominance (NGAD) and roll out the F-15EX. The USAF plans to buy 33 F-35As in 2023, fewer than the 48 the service asked for in FY2022. With the dynamic nature of modern warfare, the United States aims to maintain a smaller fleet of effective aircraft, which may significantly reduce the overall fleet size during the forecast period.

US Military Aviation Industry Overview

The US Military Aviation Market is fairly consolidated, with the top five companies occupying 98.65%. The major players in this market are Airbus SE, Lockheed Martin Corporation, Northrop Grumman Corporation, Textron Inc. and The Boeing Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Gross Domestic Product

- 4.2 Active Fleet Data

- 4.3 Defense Spending

- 4.4 Regulatory Framework

- 4.5 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Aircraft Type

- 5.1.1 Fixed-Wing Aircraft

- 5.1.1.1 Multi-Role Aircraft

- 5.1.1.2 Training Aircraft

- 5.1.1.3 Transport Aircraft

- 5.1.1.4 Others

- 5.1.2 Rotorcraft

- 5.1.2.1 Multi-Mission Helicopter

- 5.1.2.2 Transport Helicopter

- 5.1.2.3 Others

- 5.1.1 Fixed-Wing Aircraft

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Airbus SE

- 6.4.2 Leonardo S.p.A

- 6.4.3 Lockheed Martin Corporation

- 6.4.4 Northrop Grumman Corporation

- 6.4.5 Textron Inc.

- 6.4.6 The Boeing Company

7 KEY STRATEGIC QUESTIONS FOR AVIATION CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms