|

市場調査レポート

商品コード

1693968

アドテク- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Ad Tech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アドテク- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 164 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

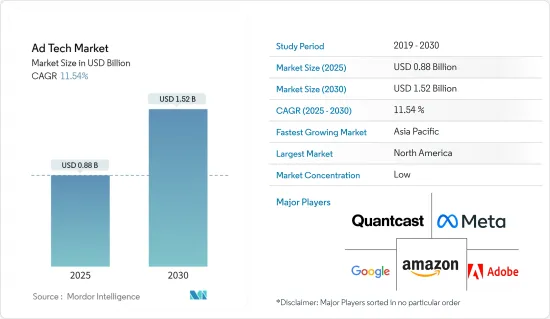

アドテク市場規模は2025年に8億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは11.54%で、2030年には15億2,000万米ドルに達すると予測されます。

アドテク市場は、デジタル機器とインターネットの利用拡大に牽引され、過去数年間で大きな成長を遂げてきました。スマートフォンやソーシャルメディアプラットフォームの普及に伴い、デジタル広告は世界中の企業のマーケティング計画に欠かせないものとなっています。

主要ハイライト

- 従来型広告からオンライン広告への継続的なシフトが、市場成長の主要原動力となっています。インターネットの普及とインターネットユーザーの増加により、デジタル広告を通じてより多くのオーディエンスにリーチすることが可能になりました。人々は仕事、娯楽、社交のためにより多くの時間をオンラインで過ごすようになり、広告主はオンラインで彼らにリーチできるようになりました。

- 5G技術は、低遅延、高速ダウンロード、ネットワーク効率の改善を提供し、アドテク需要の成長に大きな影響を与えると予想されます。このような進歩は、アドテク企業にとって、ユーザー体験を向上させる対象を絞った革新的なデータ主導型広告ソリューションを提供する新たな機会をもたらします。

- オンラインeコマースサービス部門も、パンデミックの間に大きく成長しました。より多くの人々がオンラインショッピングなどのデジタルサービスを利用するようになり、これらの産業の企業は潜在的な視聴者にリーチするために広告費を増やしました。このため、特に検索エンジンやソーシャルメディアプラットフォームでのオンライン広告の需要が高まりました。

- しかし、アドテクのプラクティスに対する一般市民の認識不足が、規制上の懸念の増大につながっています。消費者保護機関は、広告活動のためにデータが使用・収集されることへの懸念を強めており、アドテク産業の成長を脅かす厳しい規制につながっています。

- COVID-19の流行は広告産業に大きな変革をもたらし、これらの変革のいくつかは広告産業に長期的な影響を及ぼすと予想されます。個人消費の減少や景気の先行き不透明感から、多くのブランドが広告予算の削減を選択し、広告費全体の減少につながっています。この落ち込みは、ラジオ、テレビ、印刷メディアといった伝統的メディアプラットフォームで特に顕著で、広告収入が激減しています。一方、人々が自宅で過ごす時間が長くなり、デジタルメディアを利用するようになったため、デジタル広告費は大幅に増加しています。この増加傾向は、パンデミックが沈静化した後も、eコマースやデジタルチャネルに親しむ個人が増えるにつれて続くと予測されています。全体として、パンデミックは、産業のデータ主導型アプローチとデジタル広告チャネルへの移行を促進し、このセグメントの将来に長期的な影響を及ぼしています。

アドテク市場の動向

モバイルデバイスとスマートフォンが大幅な成長を遂げる

- モバイルデバイス上の広告は、企業が対象とするオーディエンスとつながり、交流するための重要なツールとして機能します。ビジネスセクタの小規模企業は、このセクタの視覚的な側面を利用して、自社の提供物や特徴的なブランドID確認を強調する魅力的な広告をモバイルデバイス上で作成することができます。

- さらに、画像テキスト広告やバナー広告、クリック・ツー・コール広告、クリック・ツー・メッセージ広告、クリック・ツー・ダウンロード広告など、モバイル機器向けの広告にはいくつかの形態があります。さらに、そのモビリティと容易さのために、人々は最終的にラップトップやデスクトップよりもスマートフォン端末を選択します。また、似たようなタスクをこなす前者の能力により、モバイルプラットフォームはますます利益を生むようになると予測されています。

- 企業に力を与え、第4次産業革命に参入させる最新のマーケティング戦略には、デジタル広告とモバイルマーケティングが含まれます。近い将来、オンライン販売に移行する中小企業の数が大幅に増加し、スマートフォンの使用率が上昇し、地上でのイベントや展示会が不足することを考えると、やがて不可欠な広告チャネルを供給し、オンライン広告市場に良い影響をもたらすことが証明されると考えられます。

- Ericssonによると、世界のスマートフォンモバイルネットワーク契約総数は近年約64億件に達し、予測期間中には77億件を突破すると予測されています。スマートフォンのモバイルネットワーク契約数が最も多い国は中国、インド、米国です。したがって、スマートフォンのモバイルネットワーク契約数が世界的に増加していることから、同市場は同セグメントで成長する十分な機会を目の当たりにすることになると予想されます。

- したがって、より多くの顧客が物事を探索し、購入するためにモバイルデバイスを使用するように、モバイル広告は、ファッションビジネスにとってより重要になってきています。対象オーディエンスにリーチし、交流するために、企業はモバイル広告への投資を大幅に増やしています。

大きな成長が期待されるアジア太平洋

- 中国の経済成長と技術に精通した人口の増加により、近年、インターネット消費とモバイル機器の普及率が高まっています。ソーシャルメディアの普及に伴い、同国ではアドテク産業が急成長しています。中国には百度(Baidu)、騰訊(Tencent)、阿里巴巴(Alibaba)といったハイテク大手があります。動画ベースのプラットフォームへの傾斜が高まっていることも、この地域における様々な広告フォーマットの需要を高めています。

- デジタル革命とインターネット普及率の上昇がインドのアドテク市場を牽引しています。オンラインショッピングやその他のデジタルサービスの台頭、検索エンジンやソーシャルメディアプラットフォームを中心としたデジタル広告への需要の高まりにより、インドのアドテク産業の企業は広告支出を増やす必要に迫られています。

- 日本のアドテク市場は、データ、自動化、人工知能、プログラマティック広告への投資の増加により成長が見込まれています。新たな市場参入企業の出現とイノベーションは、日本のアドテクエコシステムにおいて重要な役割を果たしています。日本ではモバイルアプリのエコシステムが拡大しており、アドテク企業にとって大きなビジネス機会となっているため、予測期間中にモバイル広告費は増加すると予測されます。また、動画広告配信プラットフォームの日本市場への参入も増加しています。

- オーストラリアではデジタルとインターネットの普及が進んでおり、この地域のアドテク市場の成長を後押ししています。人工知能(AI)、機械学習(ML)、仮想現実(VR)、拡張現実(AR)技術の採用が増加しており、広告技術企業にとって有利な成長機会がもたらされると期待されています。ソーシャルメディアアプリの利用拡大やゲーム産業の台頭も、オーストラリアにおけるアドテク市場成長のための選択肢を数多く生み出しています。

- 韓国では、投資の増加、官民パートナーシップ、成長し続けるデジタルゲーム市場により、マーケターが高度にインタラクティブなアウトオブホーム(OOH)環境でオーディエンスを魅了する絶好の機会がもたらされると予測されます。プログラマティックデジタルアウト・オブ・ホーム広告は、メディアオーナーに新たな収益源を開き、さらなる収益をもたらします。

- クリエイティブな革新、技術的な採用、倫理的な広告への献身が組み合わさることで、世界のアドテク市場におけるニュージーランドの地位が決まる。市場の拡大が予測され、地域性や法令遵守が重視されるニュージーランドは、デジタル広告の変化に大きな影響を与える立場にあります。

アドテク産業概要

アドテク市場は細分化されており、大企業と中小企業の間で高い競争が繰り広げられています。参入企業には、Adobe、Google LLC、Amazon.com Inc.、Meta Platform Inc.、Quantcastなどがあります。同市場の参入企業は、製品提供を強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年10月-Metaは広告主向けに初の生成AI機能を発表し、広告主はAIを使用して背景を作成したり、画像を拡大したり、元のコピーに基づいて複数バージョンの広告テキストを生成したりできるようになりました。新機能のうち最初のものは、広告主が複数の異なる背景を生成して商品画像の見た目を変えることで、クリエイティブ資産をカスタマイズすることを可能にします。もう一つの機能である画像拡大は、広告主がフィードやリールのような様々な製品で必要とされる異なるアスペクト比に合わせてアセットを調整することを可能にします。

- 2023年7月-オムニコムはGoogleと提携し、Googleの生成AIモデルを自社のアドテクプラットフォームに統合しました。この統合は、パーソナライズされた効果的な広告機会を提供しながら、オムニコムのアドテックプラットフォームの機能を向上させることを目的としています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- COVID-19が産業に与える影響の評価

- マクロ経済動向の影響

第5章 市場力学

- 市場の促進要因

- スマートフォンとソーシャルメディアの普及率上昇

- デジタル広告の高精度、効果、コスト効率

- 市場抑制要因

- 認知度が低い中でのクリックボットやインストール型ハイジャックの増加

- 広告のデジタル化

- パブリッシャーによる顧客データへのアクセスの増加

- 新たな収益ストリームの創出

- レコメンデーションエンジンを通じたパーソナライゼーションによる視聴体験の向上

- ロケーションベース広告

- 消費パターンに役立つ顧客行動分析

- 技術企業とのパートナーシップとコラボレーションの増加

第6章 市場セグメンテーション

- プラットフォーム別

- サプライサイドプラットフォーム(SSP)

- デマンドサイドプラットフォーム(DSP)

- アドエクスチェンジ

- データマネジメント

- 広告フォーマット別

- 動画広告

- ソーシャルメディア

- 検索広告

- メール

- その他の広告フォーマット

- デバイスプラットフォーム別

- デスクトップ

- モバイルスマートフォン

- その他のデバイスプラットフォーム

- エンドユーザー産業別

- 小売・eコマース

- 医療

- BFSI

- サービス(ホスピタリティ、観光、法律サービス)

- 通信産業

- その他

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ニュージーランド

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ナイジェリア

- エジプト

- その他の中東・アフリカ

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- その他のラテンアメリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Google LLC

- Amazon.com, Inc.

- Meta Platform, Inc.

- Quantcast

- Adobe

- Adform A/S

- MediaMath

- Microsoft Corporation

- Zeta Global Holdings Corp.

- Mediaocean

第8章 投資分析

The Ad Tech Market size is estimated at USD 0.88 billion in 2025, and is expected to reach USD 1.52 billion by 2030, at a CAGR of 11.54% during the forecast period (2025-2030).

The ad tech market has witnessed considerable growth over the past few years, driven by the growing use of digital devices and the Internet. With the increasing adoption of smartphones and social media platforms, digital advertising has become essential to marketing plans for businesses worldwide.

Key Highlights

- The continuous shift from traditional to online advertising is the main driving force behind the market's growth. The proliferation of the Internet and the increase in the number of Internet users has made it possible to reach a larger audience through digital ads. People spend more time online for work, entertainment, and socializing, and advertisers can now reach them online.

- 5G technology is expected to significantly impact ad tech demand growth, offering lower latency, faster download speeds, and improved network efficiency. These advances introduce new opportunities for ad tech companies to provide targeted, innovative, data-driven advertising solutions to enhance user experience.

- The online and e-commerce services sector also significantly boosted during the pandemic. As more people turn to digital services such as online shopping, companies in these industries have increased their advertising spending to reach potential audiences. This has increased the demand for online advertising, especially on search engines and social media platforms.

- However, a lack of public awareness of ad tech practices has led to augmented regulatory concerns. Consumer protection agencies are becoming increasingly concerned about data being used and collected for advertising efforts, leading to strict regulations that threaten the growth of the ad tech industry.

- The COVID-19 pandemic has brought about significant transformations in the advertising industry, and several of these changes are expected to have a long-lasting impact on the sector. With reduced consumer spending and economic uncertainty, many brands have opted to decrease their advertising budgets, leading to an overall decrease in ad spending. This decline has been particularly noticeable in traditional media platforms such as radio, television, and print media, which have experienced a sharp decrease in advertising revenues. On the other hand, as people spend more time at home and engage with digital media, there has been a substantial increase in digital ad spending. This upward trend is predicted to persist even after the pandemic subsides as more individuals become acquainted with e-commerce and digital channels. Overall, the pandemic has augmented the industry's shift to a more data-driven approach and digital advertising channels, with long-term effects for the sector's future.

Ad Tech Market Trends

Mobile Devices and Smartphones to Witness Significant Growth

- Advertising on mobile devices acts as a significant tool for firms to connect with and interact with their target audience. Small firms in the business sector may make use of the visual aspect of the sector to create engaging advertising on mobile devices that highlights their offerings and distinctive brand identities.

- Furthermore, there are several forms of advertising for mobile devices, such as image text and banner ads, click-to-call ads, click-to-message ads, and click-to-download ads. Additionally, due to their mobility and ease, people ultimately choose smartphone devices over laptops or desktops. Also, due to the former's ability to undertake similar tasks, mobile platforms are predicted to become increasingly profitable.

- Modern marketing strategies that would empower firms and bring them into the fourth industrial revolution include digital advertising and mobile marketing. In due course, it would supply the essential advertising channels and prove to produce a good influence on the online advertising market, given the significant number of SMEs transitioning to online sales, rising smartphone usage, and the lack of on-ground events or exhibits in the near future.

- According to Ericsson, the total number of smartphone mobile network subscriptions worldwide reached around 6.4 billion in the recent years and is forecasted to surpass 7.7 billion during the forecast period. China, India, and the United States are the countries with the most significant number of smartphone mobile network subscriptions. Hence, with the rise in the overall number of smartphone mobile network subscriptions worldwide, the market is expected to witness ample opportunities to grow within the market sector.

- Therefore, as more customers use their mobile devices to explore and buy things, mobile advertising is becoming more crucial for the fashion business. In order to reach and interact with their target audience, firms are increasing their investment in mobile advertising significantly.

Asia-Pacific Expected to Witness Major Growth

- China's economic growth and a rising tech-savvy population have resulted in higher penetration of internet consumption and mobile device penetration in recent years. Due to the increased proliferation of social media, the ad tech industry is growing rapidly in the country. China hosts several tech giants such as Baidu, Tencent, and Alibaba. The rising inclination toward video-based platforms has also increased the demand for various advertising formats in the region.

- The digital revolution and growing internet penetration are driving the ad tech market in India. The rise of online shopping and other digital services, as well as increasing demand for digital advertising, especially on search engines and social media platforms, have compelled businesses in the Indian ad tech industry to increase their advertisement spending.

- The ad tech market in Japan is anticipated to grow due to increasing investment in data, automation, artificial intelligence, and programmatic advertising. The emergence of new market players and innovation plays a critical role in the ad tech ecosystem in Japan. Mobile ad spending is projected to increase in Japan during the forecast period, attributed to the country's expanding mobile app ecosystem, representing a massive opportunity for ad tech companies. Japan also has an increased influx of video advertising serving platforms entering the Japanese market.

- The rising digital and internet penetration in Australia is bolstering the growth of the regional ad tech market. The rising adoption of artificial intelligence (AI), machine learning (ML), Virtual reality (VR), and augmented reality (AR) technologies is expected to provide lucrative growth opportunities for advertising technology players. The growing use of social media apps and the rising gaming industry also create numerous options for the ad tech market growth in Australia.

- Increased investments, public-private partnerships, and the ever-growing digital gaming market are projected to provide tremendous opportunities for marketers to attract audiences in highly interactive out-of-home (OOH) environments in South Korea. Programmatic Digital out-of-home advertising is opening up new revenue streams for media owners to drive additional revenues.

- A combination of creative innovation, technical adoption, and a dedication to ethical advertising define New Zealand's position in the global ad tech market. Because of the market's projected expansion and emphasis on regional specifics and legal compliance, New Zealand is positioned to have a significant impact on the changing face of digital advertising.

Ad Tech Industry Overview

The Ad tech market is fragmented, with high competition among large and small companies. Some of the players include Adobe, Google LLC, Amazon.com Inc., Meta Platform Inc., and Quantcast. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- October 2023 - Meta launched its first generative AI features for advertisers, allowing them to use AI to create backgrounds, expand images, and generate multiple versions of ad text based on their original copy. The first among the trio of new features allows an advertiser to customize their creative assets by generating multiple different backgrounds to change the look of their product images. Another feature, image expansion, allows advertisers to adjust their assets to fit different aspect ratios required across various products, like Feed or Reels.

- July 2023 - Omnicom has partnered with Google to integrate the latter's generative AI models into its Adtech platform. The integration aims to improve the capabilities of Omnicom's Adtech platform while providing personalized and effective advertising opportunities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 An Assessment of the Impact of COVID-19 on the Industry

- 4.3 Impact of Macroeconomic Trends

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in the Adoption of Smartphones and Social Media

- 5.1.2 High Precision, Effectiveness, and Cost Efficiency of Digital Advertising

- 5.2 Market Restraint

- 5.2.1 Rise of Click Bots and Install Hijacks Amid Low Public Awareness

- 5.3 Digital Transformation in Advertising

- 5.3.1 Increased Access of Customer Data for Publishers

- 5.3.2 Generation of New Revenue Streams

- 5.3.3 Better Viewer Experience Through Personalization Through Recommendation Engines

- 5.3.4 Location-Based Advertising

- 5.3.5 Customer Behavior Analytics Helping with Spending Pattern

- 5.3.6 Increasing Partnerships and Collaboration with Technology Companies

6 MARKET SEGMENTATION

- 6.1 By Platform

- 6.1.1 Supply Side Platform (SSP)

- 6.1.2 Demand Side Platform (DSP)

- 6.1.3 Ad Exchange

- 6.1.4 Data Management

- 6.2 By Ad Format

- 6.2.1 Video Advertising

- 6.2.2 Social Media

- 6.2.3 Search Advertising

- 6.2.4 Email

- 6.2.5 Other Ad Formats

- 6.3 By Device Platforms

- 6.3.1 Desktop

- 6.3.2 Mobile Devices and Smartphones

- 6.3.3 Other Device Platforms

- 6.4 By End-user Industry

- 6.4.1 Retail and E-Commerce

- 6.4.2 Healthcare

- 6.4.3 BFSI

- 6.4.4 Services (Hospitality, Tourism, Legal Services)

- 6.4.5 Telecommunications

- 6.4.6 Other End-user Industries

- 6.5 By Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.2 Europe

- 6.5.2.1 United Kingdom

- 6.5.2.2 Germany

- 6.5.2.3 France

- 6.5.2.4 Spain

- 6.5.2.5 Italy

- 6.5.2.6 Rest of Europe

- 6.5.3 Asia-Pacific

- 6.5.3.1 China

- 6.5.3.2 India

- 6.5.3.3 Japan

- 6.5.3.4 Australia

- 6.5.3.5 South Korea

- 6.5.3.6 New Zealand

- 6.5.3.7 Rest of Asia-Pacific

- 6.5.4 Middle-East and Africa

- 6.5.4.1 Saudi Arabia

- 6.5.4.2 United Arab Emirates

- 6.5.4.3 South Africa

- 6.5.4.4 Nigeria

- 6.5.4.5 Egypt

- 6.5.4.6 Rest of Middle East and Africa

- 6.5.5 Latin America

- 6.5.5.1 Brazil

- 6.5.5.2 Mexico

- 6.5.5.3 Argentina

- 6.5.5.4 Colombia

- 6.5.5.5 Rest of Latin America

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Google LLC

- 7.1.2 Amazon.com, Inc.

- 7.1.3 Meta Platform, Inc.

- 7.1.4 Quantcast

- 7.1.5 Adobe

- 7.1.6 Adform A/S

- 7.1.7 MediaMath

- 7.1.8 Microsoft Corporation

- 7.1.9 Zeta Global Holdings Corp.

- 7.1.10 Mediaocean