|

|

市場調査レポート

商品コード

1510646

アジア太平洋のヘルスケアCRM市場予測(~2030年):地域別分析 - 展開形態、製品タイプ、用途、エンドユーザー別Asia Pacific Healthcare CRM Market Forecast to 2030 - Regional Analysis - by Deployment Mode, Product Type, Application, and End User |

||||||

|

|||||||

|

|||||||

| アジア太平洋のヘルスケアCRM市場予測(~2030年):地域別分析 - 展開形態、製品タイプ、用途、エンドユーザー別 |

|

出版日: 2024年05月07日

発行: The Insight Partners

ページ情報: 英文 139 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

アジア太平洋のヘルスケアCRMの市場規模は、2022年には11億6,617万米ドルに達し、2030年には27億4,550万米ドルに達すると予測され、2022年~2030年のCAGRは11.3%と推定されます。

モノのインターネットと人工知能に関する知識の増加がアジア太平洋のヘルスケアCRM市場を後押し

データ主導の洞察、分析、集団健康管理に対する需要は、ヘルスケア産業の発展を著しく促進しており、これがヘルスケアCRMの需要を促進しています。このような需要の増加は、バリュー・ベースのケアを重視する傾向が強まり、ヘルスケア組織が患者の転帰を改善し、コストを削減し、全体的なケアの質を向上させることが求められていることと関連しています。データ主導の洞察分析は、組織が大量の患者データを調査・評価し、動向、パターン、相関関係を特定することを可能にするため、ヘルスケアCRMにおいて非常に重要です。これにより、ヘルスケア担当者は患者集団をよりよく理解することができ、治療計画、介入、リソース配分についてより正確な意思決定を行うことができます。ヘルスケア組織はまた、データ主導型アナリティクスを採用することで、リスクの高い患者を特定し、将来の病気を予測し、悪い結果を防ぐために積極的に介入することができます。同様に、ポピュレーションヘルス管理も、アジア太平洋のヘルスケアCRM市場におけるデータ主導型の洞察とアナリティクスに対する需要拡大の重要な要因の一つです。集団全体の健康アウトカムの改善に焦点を当てた集団健康管理では、ヘルスケア組織が患者集団とその健康に影響を与える要因を幅広く理解する必要があります。データ主導のインサイト分析により、ヘルスケア専門家は人口統計、臨床的問題、リスク要因などの基準に基づいて患者集団をセグメント化することができます。これにより、医療サービスや治療計画を患者グループの個別要件に合わせてパーソナライズすることができます。

さらに、ヘルスケアCRMの開発者は、高度なアナリティクスと集団健康管理機能をヘルスケアCRMプラットフォームに迅速に統合しています。これらの機能により、ヘルスケア組織はデータを利用して臨床とオペレーションのアウトカムを向上させ、より良い患者ケアとコスト削減を実現することができます。このように、データ主導の洞察、分析、集団健康管理に対する需要の高まりは、患者の転帰を改善し、コストを削減し、全体的なケアの質を高めるヘルスケアCRMの需要を促進し、アジア太平洋のヘルスケアCRM市場の成長を後押ししています。

アジア太平洋のヘルスケアCRM市場概要

中国のヘルスケアCRM市場は、ヘルスケア分野でのデジタル技術の採用増加により、今後数年間で大きな成長が見込まれています。中国政府は、ヘルスケアサービスの質とアクセシビリティを向上させるため、デジタルヘルスソリューションを推進しています。ヘルシー・チャイナ2030」計画の下、中国は今後数年間、医療技術革新の推進に多額の投資を行う計画です。この投資は、技術の進歩とヘルスケアシステムの改善を通じて、中国国内における健康の公平性を確保することを目的としています。

さらに、中国は世界で最も人口密度の高い国のひとつです。現在の人口は14億1,000万人です。2020年10月に発表された世界疾病負担(GBD)調査によると、中国の人々は感染症、慢性疾患、急性疾患にかかりやすいです。中国では、脳卒中、がん、アルツハイマー病、糖尿病など多くの疾患の発生が報告されています。患者数の増加とより良いヘルスケアサービスに対する需要の高まりが、中国におけるアジア太平洋のヘルスケアCRM市場の成長を後押ししています。さらに、Future Health Indexのデータによると、中国の医療従事者の94%がデジタルヘルス技術やモバイルヘルスアプリを利用しています。現地の主要企業の存在感の高まりが、中国のヘルスケアCRM市場の成長を後押ししています。メーカー各社は、戦略的なグローバルプレゼンスと独自の技術力を持つ専門知識の拡大に注力しており、中国市場の成長を牽引しています。高齢化社会は、身体的ストレスのためにいつでも病院を受診することができないため、受診のための適切なスケジュールや在宅ケアのためのデジタル予約を必要とするため、ヘルスケアCRMソフトウェアの需要増加の主な要因の1つとなっています。2019年、中国の人口の12.6%が65歳以上です。また、WHOによれば、2040年までに4億200万人(すなわち総人口の28%)が60歳以上になるとされています。このように、中国は高齢化の圧力と、がん、アルツハイマー病、糖尿病などの疾病の有病率の絶え間ない上昇に直面しています。その結果、病院受診やオンライン予約の需要は増加し続け、中国のヘルスケアCRMソフトウェアに対する新たな要件が設定されるでしょう。

アジア太平洋のヘルスケアCRM市場の収益と2030年までの予測(金額)

アジア太平洋のヘルスケアCRM市場のセグメンテーション

アジア太平洋のヘルスケアCRM市場は、展開形態、製品タイプ、用途、エンドユーザー、国別に分類されます。

展開形態別では、アジア太平洋のヘルスケアCRM市場はクラウドベースとオンプレミスに二分されます。2022年にはクラウドベースのセグメントがより大きな市場シェアを占めています。

製品タイプ別では、アジア太平洋のヘルスケアCRM市場は、運用型CRM、分析型CRM、連携型CRMに分類されます。2022年には、運用型CRMセグメントがより大きな市場シェアを占めています。

用途別では、アジア太平洋のヘルスケアCRM市場は、リレーションシップ管理、ケース管理、ケースコーディネーション、コミュニティアウトリーチ、その他に分類されます。リレーションシップ管理セグメントが2022年に最も大きな市場シェアを占めました。ケース管理セグメントはさらに疾病管理と臨床試験リレーションシップ管理に細分化されます。ケースコーディネーションセグメントは、さらに患者情報管理、事前承認/適格性などに細分化されます。コミュニティアウトリーチセグメントは、さらにアウトリーチ/プロモーションとコミュニティヘルス教育に細分化されます。

エンドユーザー別では、アジア太平洋のヘルスケアCRM市場は提供者、支払者、その他に区分されます。2022年には提供者セグメントが最大の市場シェアを占めました。

国別では、アジア太平洋のヘルスケアCRM市場は、中国、日本、インド、オーストラリア、韓国、その他アジア太平洋に区分されます。2022年のアジア太平洋のヘルスケアCRM市場シェアは中国が独占しました。

International Business Machines Corp、IQVIA Holdings Inc、Microsoft Corp、Oracle Corp、Pegasystems Inc、Sage Group Plc、Salesforce Inc、SAP SE、SugarCRM Inc、Veeva Systems Inc、Zendesk Incは、アジア太平洋のヘルスケアCRM市場で事業を展開している主要企業です。

目次

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 アジア太平洋のヘルスケアCRM市場- 主要産業力学

- アジア太平洋のヘルスケアCRM市場- 主要産業力学

- 市場促進要因

- 患者中心のヘルスケア提供の重視の高まり

- データ主導の洞察、分析、集団健康管理に対する需要の高まり

- 市場抑制要因

- データセキュリティの欠如と患者情報のプライバシーに関する懸念

- 市場機会

- モノのインターネットと人工知能に関する知識の増加

- 今後の動向

- デジタルヘルスとモバイルCRMソリューションの受け入れ拡大

- 促進要因と抑制要因の影響

第5章 ヘルスケアCRM市場:アジア太平洋市場分析

- アジア太平洋のヘルスケアCRM市場収益(2022年~2030年)

- アジア太平洋のヘルスケアCRM市場の予測と分析

第6章 アジア太平洋のヘルスケアCRM市場分析:展開形態別

- クラウドベース

- オンプレミス

第7章 アジア太平洋のヘルスケアCRM市場分析:製品タイプ別

- 運用型CRM

- 分析型CRM

- 連携型CRM

第8章 アジア太平洋のヘルスケアCRM市場分析:用途別

- リレーションシップ管理

- ケース管理

- ケースコーディネーション

- コミュニティアウトリーチ

- その他

第9章 アジア太平洋のヘルスケアCRM市場分析:エンドユーザー別

- 提供者

- 支払者

- その他

第10章 アジア太平洋のヘルスケアCRM市場:国別分析

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

第11章 ヘルスケアCRM市場の業界情勢

第12章 企業プロファイル

- Pegasystems Inc

- Sage Group Plc

- IQVIA Holdings Inc

- Zendesk Inc

- SugarCRM Inc

- SAP SE

- Veeva Systems Inc

- Oracle Corp

- Microsoft Corp

- Salesforce Inc

- International Business Machines Corp

第13章 付録

List Of Tables

- Table 1. Asia Pacific Healthcare CRM Market Segmentation

- Table 2. Largest Healthcare Data Breaches (2009-2022) as per the HIPAA Journal

- Table 3. Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Million)

- Table 4. Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Million) - By Deployment Mode

- Table 5. Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030(US$ Million) - By Product Type

- Table 6. Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030(US$ Million) - By Application

- Table 7. Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Million) - By End User

- Table 8. China: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Deployment Mode

- Table 9. China: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Product Type

- Table 10. China: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Application

- Table 11. China: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Case Management

- Table 12. China: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Community Outreach

- Table 13. China: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Case Coordination

- Table 14. China: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By End User

- Table 15. Japan: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Deployment Mode

- Table 16. Japan: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Product Type

- Table 17. Japan: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Application

- Table 18. Japan: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Case Management

- Table 19. Japan: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Community Outreach

- Table 20. Japan: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Case Coordination

- Table 21. Japan: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By End User

- Table 22. India: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Deployment Mode

- Table 23. India: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Product Type

- Table 24. India: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Application

- Table 25. India: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Case Management

- Table 26. India: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Community Outreach

- Table 27. India: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Case Coordination

- Table 28. India: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By End User

- Table 29. Australia: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Deployment Mode

- Table 30. Australia: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Product Type

- Table 31. Australia: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Application

- Table 32. Australia: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Case Management

- Table 33. Australia: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Community Outreach

- Table 34. Australia: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Case Coordination

- Table 35. Australia: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By End User

- Table 36. South Korea: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Deployment Mode

- Table 37. South Korea: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Product Type

- Table 38. South Korea: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Application

- Table 39. South Korea: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Case Management

- Table 40. South Korea: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Community Outreach

- Table 41. South Korea: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Case Coordination

- Table 42. South Korea: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By End User

- Table 43. Rest of Asia Pacific: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Deployment Mode

- Table 44. Rest of Asia Pacific: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Product Type

- Table 45. Rest of Asia Pacific: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Application

- Table 46. Rest of Asia Pacific: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Case Management

- Table 47. Rest of Asia Pacific: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Community Outreach

- Table 48. Rest of Asia Pacific: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By Case Coordination

- Table 49. Rest of Asia Pacific: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn) - By End User

- Table 50. Recent Growth Strategies in the Healthcare CRM Market

- Table 51. Glossary of Terms, Healthcare CRM Market

List Of Figures

- Figure 1. Asia Pacific Healthcare CRM Market Segmentation, By Country

- Figure 2. Impact Analysis of Drivers and Restraints

- Figure 3. Asia Pacific Healthcare CRM Market Revenue (US$ Million), 2022 - 2030

- Figure 4. Asia Pacific Healthcare CRM Market Share (%) - By Deployment Mode, 2022 and 2030

- Figure 5. Cloud Based Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 6. On-premise Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 7. Asia Pacific Healthcare CRM Market Share (%) - By Product Type, 2022 and 2030

- Figure 8. Operational CRM Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 9. Analytical CRM Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 10. Collaborative CRM Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 11. Asia Pacific Healthcare CRM Market Share (%) - By Application, 2022 and 2030

- Figure 12. Relationship Management Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 13. Case Management Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 14. Case Coordination Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 15. Community Outreach Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 16. Others Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 17. Asia Pacific Healthcare CRM Market Share (%) - By End User, 2022 and 2030

- Figure 18. Providers Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 19. Payers Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 20. Others Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 21. Asia Pacific Healthcare CRM Market Breakdown by Key Countries - Revenue (2022) (US$ Million)

- Figure 22. Asia Pacific Healthcare CRM Market Breakdown by Key Countries, 2022 and 2030 (%)

- Figure 23. China: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn)

- Figure 24. Japan: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn)

- Figure 25. India: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn)

- Figure 26. Australia: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn)

- Figure 27. South Korea: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn)

- Figure 28. Rest of Asia Pacific: Asia Pacific Healthcare CRM Market - Revenue and Forecast to 2030 (US$ Mn)

The Asia Pacific healthcare CRM market was valued at US$ 1,166.17 million in 2022 and is expected to reach US$ 2,745.50 million by 2030; it is estimated to register a CAGR of 11.3% from 2022 to 2030.

Increasing Knowledge About Internet of Things and Artificial Intelligence Boosts Asia Pacific Healthcare CRM Market

The demand for data-driven insights, analytics, and population health management is significantly promoting the development of the healthcare industry, which, in turn, propels the demand for healthcare CRM. This increase in demand can be related to the growing emphasis on value-based care and the demand for healthcare organizations to improve patient outcomes, lower costs, and improve overall care quality. Data-driven insights analytics are critical in healthcare CRM since they allow organizations to examine and evaluate large volumes of patient data to identify trends, patterns, and correlations. This enables healthcare practitioners to understand their patient population better, allowing them to make more accurate decisions about treatment plans, interventions, and resource allocation. Healthcare organizations may also identify high-risk patients, forecast prospective illnesses, and intervene proactively to prevent negative outcomes by employing data-driven analytics. Similarly, population health management is another significant driver of the growing demand for data-driven insights and analytics in the Asia Pacific healthcare CRM market. Population health management, focusing on improving the health outcomes of entire populations, necessitates healthcare organizations having an extensive understanding of their patient population and the factors that impact their health. Data-driven insights analytics allow healthcare professionals to segment their patient population based on criteria including demographics, clinical problems, and risk factors. This allows them to personalize medical services and treatment plans to the individual requirements of distinct patient groups.

Furthermore, healthcare CRM developers rapidly integrate advanced analytics and population health management capabilities into healthcare CRM platforms. These capabilities enable healthcare organizations to use data to enhance clinical and operational outcomes, resulting in better patient care and lower costs. Thus, the increasing demand for data-driven insights, analytics, and population health management propels the demand for healthcare CRM to improve patient outcomes, reduce costs, and enhance the overall quality of care, which fuels the growth of the Asia Pacific healthcare CRM market.

Asia Pacific Healthcare CRM Market Overview

The market for healthcare CRM in China is expected to witness significant growth in the coming years due to the increasing adoption of digital technologies in the healthcare sector. The Chinese government is promoting digital health solutions to improve the quality and accessibility of healthcare services. Under the Healthy China 2030 plan, China plans to invest significantly in advancing its healthcare technology innovation in the coming years. This expenditure is intended to ensure health equity within China through technological advancements and improvements to the healthcare system.

Additionally, China is among the most densely populated countries across the world. The current population is ~1.41 billion. According to the Global Burden of Disease (GBD) study published in October 2020, the population in the country is prone to infectious, chronic, and acute diseases. China reports the incidence of many diseases such as stroke, cancer, Alzheimer's, and diabetes. The rising number of patients and the increasing demand for better healthcare services boost the Asia Pacific healthcare CRM market growth in China. Furthermore, according to data from the Future Health Index, 94% of Chinese healthcare professionals used digital health technology or mobile health apps. The growing presence of local key players is boosting the China healthcare CRM market growth. Manufacturers are focusing on expanding their strategic global presence and specialized expertise with exclusive technological capabilities, leading to the market growth in China. Aging population has become one of the major contributors to the increased demand for healthcare CRM software as they are unable to visit the hospital anytime due to physical stress and thus require a proper schedule for medical visits and a digital appointment for home care settings. In 2019, 12.6% of China's population was over 65. Also, as per WHO, by 2040, ~402 million people (i.e., 28% of the total population) will be over 60. Thus, China is facing pressures of an aging population and constant rise in the prevalence of diseases such as cancer, Alzheimer's disease, and diabetes. As a result, demand for hospital visits and online appointments will continue to rise, setting new requirements for healthcare CRM software in China.

Asia Pacific Healthcare CRM Market Revenue and Forecast to 2030 (US$ Million)

Asia Pacific Healthcare CRM Market Segmentation

The Asia Pacific healthcare CRM market is categorized into deployment mode, product type, application, and end user, and country.

Based on deployment mode, the Asia Pacific healthcare CRM market is bifurcated cloud based and on-premise. The cloud based segment held a larger market share in 2022.

In terms of product type, the Asia Pacific healthcare CRM market is categorized into operational CRM, analytical CRM, and collaborative CRM. The operational CRM segment held a larger market share in 2022.

By application, the Asia Pacific healthcare CRM market is segmented into relationship management, case management, case coordination, community outreach, and others. The relationship management segment held the largest market share in 2022. The case management segment is further subsegmented into disease management and clinical trials relationship management. The case coordination segment is further subsegmented into patient information management and pre-authorizations / eligibility. The community outreach segment is further services outreach/promotion and community health education.

By end user, the Asia Pacific healthcare CRM market is segmented into providers, payers, and others. The providers segment held the largest market share in 2022.

By country, the Asia Pacific healthcare CRM market is segmented into China, Japan, India, Australia, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific healthcare CRM market share in 2022.

International Business Machines Corp, IQVIA Holdings Inc, Microsoft Corp, Oracle Corp, Pegasystems Inc, Sage Group Plc, Salesforce Inc, SAP SE, SugarCRM Inc, Veeva Systems Inc, and Zendesk Inc are among the leading companies operating in the Asia Pacific healthcare CRM market.

Table Of Contents

Table of Content

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

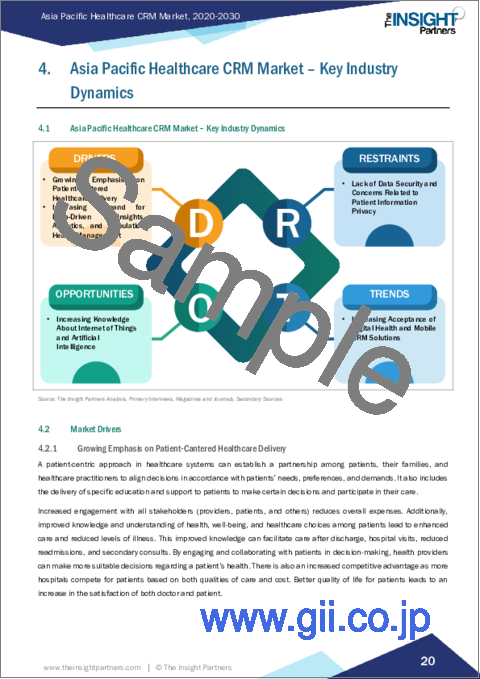

4. Asia Pacific Healthcare CRM Market - Key Industry Dynamics

- 4.1 Asia Pacific Healthcare CRM Market - Key Industry Dynamics

- 4.2 Market Drivers

- 4.2.1 Growing Emphasis on Patient-Cantered Healthcare Delivery

- 4.2.2 Increasing Demand for Data-Driven Insights, Analytics, and Population Health Management

- 4.3 Market Restraints

- 4.3.1 Lack of Data Security and Concerns Related to Patient Information Privacy

- 4.4 Market Opportunities

- 4.4.1 Increasing Knowledge About Internet of Things and Artificial Intelligence

- 4.5 Future Trends

- 4.5.1 Increasing Acceptance of Digital Health and Mobile CRM Solutions

- 4.6 Impact of Drivers and Restraints:

5. Healthcare CRM Market - Asia Pacific Market Analysis

- 5.1 Asia Pacific Healthcare CRM Market Revenue (US$ Million), 2022 - 2030

- 5.2 Asia Pacific Healthcare CRM Market Forecast and Analysis

6. Asia Pacific Healthcare CRM Market Analysis - By Deployment Mode

- 6.1 Cloud Based

- 6.1.1 Overview

- 6.1.2 Cloud Based Market, Revenue and Forecast to 2030 (US$ Million)

- 6.2 On-premise

- 6.2.1 Overview

- 6.2.2 On-premise Market, Revenue and Forecast to 2030 (US$ Million)

7. Asia Pacific Healthcare CRM Market Analysis - By Product Type

- 7.1 Operational CRM

- 7.1.1 Overview

- 7.1.2 Operational CRM Market, Revenue and Forecast to 2030 (US$ Million)

- 7.2 Analytical CRM

- 7.2.1 Overview

- 7.2.2 Analytical CRM Market, Revenue and Forecast to 2030 (US$ Million)

- 7.3 Collaborative CRM

- 7.3.1 Overview

- 7.3.2 Collaborative CRM Market, Revenue and Forecast to 2030 (US$ Million)

8. Asia Pacific Healthcare CRM Market Analysis - By Application

- 8.1 Relationship Management

- 8.1.1 Overview

- 8.1.2 Relationship Management Market, Revenue and Forecast to 2030 (US$ Million)

- 8.2 Case Management

- 8.2.1 Overview

- 8.2.2 Case Management Market, Revenue and Forecast to 2030 (US$ Million)

- 8.3 Case Coordination

- 8.3.1 Overview

- 8.3.2 Case Coordination Market, Revenue and Forecast to 2030 (US$ Million)

- 8.4 Community Outreach

- 8.4.1 Overview

- 8.4.2 Community Outreach Market, Revenue and Forecast to 2030 (US$ Million)

- 8.5 Others

- 8.5.1 Overview

- 8.5.2 Others Market, Revenue and Forecast to 2030 (US$ Million)

9. Asia Pacific Healthcare CRM Market Analysis - By End User

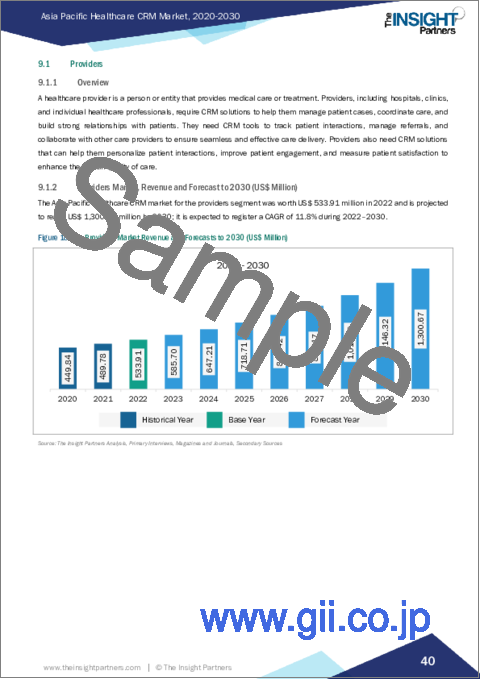

- 9.1 Providers

- 9.1.1 Overview

- 9.1.2 Providers Market, Revenue and Forecast to 2030 (US$ Million)

- 9.2 Payers

- 9.2.1 Overview

- 9.2.2 Payers Market, Revenue and Forecast to 2030 (US$ Million)

- 9.3 Others

- 9.3.1 Overview

- 9.3.2 Others Market, Revenue and Forecast to 2030 (US$ Million)

10. Asia Pacific Healthcare CRM Market - Country Analysis

- 10.1 Asia Pacific Healthcare CRM Market Revenue and Forecast and Analysis - By Country

- 10.1.1 Asia Pacific Healthcare CRM Market Revenue and Forecast and Analysis - By Country

- 10.1.1.1 China: Asia Pacific Healthcare CRM Market Revenue and Forecast to 2030 (US$ Mn)

- 10.1.1.1.1 China: Asia Pacific Healthcare CRM Market Breakdown by Deployment Mode

- 10.1.1.1.2 China: Asia Pacific Healthcare CRM Market Breakdown by Product Type

- 10.1.1.1.3 China: Asia Pacific Healthcare CRM Market Breakdown by Application

- 10.1.1.1.3.1 China: Asia Pacific Healthcare CRM Market Breakdown by Case Management

- 10.1.1.1.3.2 China: Asia Pacific Healthcare CRM Market Breakdown by Community Outreach

- 10.1.1.1.3.3 China: Asia Pacific Healthcare CRM Market Breakdown by Case Coordination

- 10.1.1.1.4 China: Asia Pacific Healthcare CRM Market Breakdown by End User

- 10.1.1.2 Japan: Asia Pacific Healthcare CRM Market Revenue and Forecast to 2030 (US$ Mn)

- 10.1.1.2.1 Japan: Asia Pacific Healthcare CRM Market Breakdown by Deployment Mode

- 10.1.1.2.2 Japan: Asia Pacific Healthcare CRM Market Breakdown by Product Type

- 10.1.1.2.3 Japan: Asia Pacific Healthcare CRM Market Breakdown by Application

- 10.1.1.2.3.1 Japan: Asia Pacific Healthcare CRM Market Breakdown by Case Management

- 10.1.1.2.3.2 Japan: Asia Pacific Healthcare CRM Market Breakdown by Community Outreach

- 10.1.1.2.3.3 Japan: Asia Pacific Healthcare CRM Market Breakdown by Case Coordination

- 10.1.1.2.4 Japan: Asia Pacific Healthcare CRM Market Breakdown by End User

- 10.1.1.3 India: Asia Pacific Healthcare CRM Market Revenue and Forecast to 2030 (US$ Mn)

- 10.1.1.3.1 India: Asia Pacific Healthcare CRM Market Breakdown by Deployment Mode

- 10.1.1.3.2 India: Asia Pacific Healthcare CRM Market Breakdown by Product Type

- 10.1.1.3.3 India: Asia Pacific Healthcare CRM Market Breakdown by Application

- 10.1.1.3.3.1 India: Asia Pacific Healthcare CRM Market Breakdown by Case Management

- 10.1.1.3.3.2 India: Asia Pacific Healthcare CRM Market Breakdown by Community Outreach

- 10.1.1.3.3.3 India: Asia Pacific Healthcare CRM Market Breakdown by Case Coordination

- 10.1.1.3.4 India: Asia Pacific Healthcare CRM Market Breakdown by End User

- 10.1.1.4 Australia: Asia Pacific Healthcare CRM Market Revenue and Forecast to 2030 (US$ Mn)

- 10.1.1.4.1 Australia: Asia Pacific Healthcare CRM Market Breakdown by Deployment Mode

- 10.1.1.4.2 Australia: Asia Pacific Healthcare CRM Market Breakdown by Product Type

- 10.1.1.4.3 Australia: Asia Pacific Healthcare CRM Market Breakdown by Application

- 10.1.1.4.3.1 Australia: Asia Pacific Healthcare CRM Market Breakdown by Case Management

- 10.1.1.4.3.2 Australia: Asia Pacific Healthcare CRM Market Breakdown by Community Outreach

- 10.1.1.4.3.3 Australia: Asia Pacific Healthcare CRM Market Breakdown by Case Coordination

- 10.1.1.4.4 Australia: Asia Pacific Healthcare CRM Market Breakdown by End User

- 10.1.1.5 South Korea: Asia Pacific Healthcare CRM Market Revenue and Forecast to 2030 (US$ Mn)

- 10.1.1.5.1 South Korea: Asia Pacific Healthcare CRM Market Breakdown by Deployment Mode

- 10.1.1.5.2 South Korea: Asia Pacific Healthcare CRM Market Breakdown by Product Type

- 10.1.1.5.3 South Korea: Asia Pacific Healthcare CRM Market Breakdown by Application

- 10.1.1.5.3.1 South Korea: Asia Pacific Healthcare CRM Market Breakdown by Case Management

- 10.1.1.5.3.2 South Korea: Asia Pacific Healthcare CRM Market Breakdown by Community Outreach

- 10.1.1.5.3.3 South Korea: Asia Pacific Healthcare CRM Market Breakdown by Case Coordination

- 10.1.1.5.4 South Korea: Asia Pacific Healthcare CRM Market Breakdown by End User

- 10.1.1.6 Rest of Asia Pacific: Asia Pacific Healthcare CRM Market Revenue and Forecast to 2030 (US$ Mn)

- 10.1.1.6.1 Rest of Asia Pacific: Asia Pacific Healthcare CRM Market Breakdown by Deployment Mode

- 10.1.1.6.2 Rest of Asia Pacific: Asia Pacific Healthcare CRM Market Breakdown by Product Type

- 10.1.1.6.3 Rest of Asia Pacific: Asia Pacific Healthcare CRM Market Breakdown by Application

- 10.1.1.6.3.1 Rest of Asia Pacific: Asia Pacific Healthcare CRM Market Breakdown by Case Management

- 10.1.1.6.3.2 Rest of Asia Pacific: Asia Pacific Healthcare CRM Market Breakdown by Community Outreach

- 10.1.1.6.3.3 Rest of Asia Pacific: Asia Pacific Healthcare CRM Market Breakdown by Case Coordination

- 10.1.1.6.4 Rest of Asia Pacific: Asia Pacific Healthcare CRM Market Breakdown by End User

- 10.1.1.1 China: Asia Pacific Healthcare CRM Market Revenue and Forecast to 2030 (US$ Mn)

- 10.1.1 Asia Pacific Healthcare CRM Market Revenue and Forecast and Analysis - By Country

11. Healthcare CRM Market Industry Landscape

- 11.1 Overview

12. Company Profiles

- 12.1 Pegasystems Inc

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Sage Group Plc

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 IQVIA Holdings Inc

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Zendesk Inc

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 SugarCRM Inc

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 SAP SE

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 Veeva Systems Inc

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 Oracle Corp

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 Microsoft Corp

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

- 12.10 Salesforce Inc

- 12.10.1 Key Facts

- 12.10.2 Business Description

- 12.10.3 Products and Services

- 12.10.4 Financial Overview

- 12.10.5 SWOT Analysis

- 12.10.6 Key Developments

- 12.11 International Business Machines Corp

- 12.11.1 Key Facts

- 12.11.2 Business Description

- 12.11.3 Products and Services

- 12.11.4 Financial Overview

- 12.11.5 SWOT Analysis

- 12.11.6 Key Developments

13. Appendix

- 13.1 About The Insight Partners

- 13.2 Glossary of Terms