|

市場調査レポート

商品コード

1438277

食用フィルムおよびコーティング:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Edible Films and Coating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 食用フィルムおよびコーティング:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

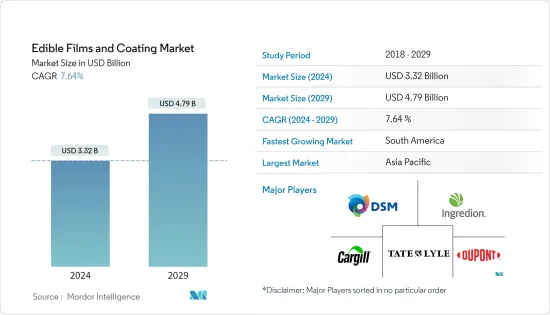

食用フィルムおよびコーティング市場規模は、2024年に33億2,000万米ドルと推定され、2029年までに47億9,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に7.64%のCAGRで成長します。

主なハイライト

- 食品に食用コーティングを使用する利点は、二酸化炭素、脂質、水分、酸素、香りに対するバリアとして機能することです。食品の品質を向上させ、製品の保存期間を延ばします。可食フィルムおよびコーティングを使用する主な利点の1つは、いくつかの有効成分をポリマーマトリックスに組み込んで食品と一緒に摂取できるため、安全性が向上し、さらには栄養特性や感覚特性も向上することです。食用コーティングは、大豆タンパク質、小麦グルテン、ホエー、ゼラチンなどから作ることができます。

- 植物由来の食品は、その利点と健康志向により、消費者の間で需要が高まっています。食品メーカーは、微生物の安全性を確保し、外部要因の影響から食品を保存するために、賞味期限を延ばし、既存の包装技術を改善する取り組みを強化しています。技術機関や研究者は、さまざまな成分を使用して可食フィルムを開発するための新しい技術を革新しています。

- たとえば、2022年 9月、インド工科大学グワーハーティー校は、果物や野菜の保存期間を延長するための食用コーティングを開発しました。コーティングは微細藻類抽出物と多糖類の混合物から作られています。抗酸化特性で知られる海洋微細藻類Dunaliella tertiolectaは、カロテノイド、タンパク質、多糖類などのさまざまな生理活性化合物として使用されています。したがって、メーカーによる新製品の革新は、食用フィルムおよびコーティング市場の市場成長に貢献すると予想されます。

食用フィルムおよびコーティング市場動向

天然資源からの食用包装材の需要の増加

- 従来の食品包装材料には、環境への影響、汚染、製造要件、廃棄などの多くの欠点があります。代替の包装材料と包装形式の必要性が大幅に増加しています。

- 持続可能性、倫理、食品の安全性、食品の品質、製品コストに関する問題はすべて、現代の消費者にとって食品購入時にますます重要な要素となっており、食品包装の法規制によってこれらの問題の多くが強制されています。これらすべての要因が、食品包装業界における可食性フィルムおよびコーティングの需要の増加に大きく寄与しています。これらの可食フィルムは、天然および有機製品から抽出されています。

- たとえば、小麦グルテン、ホエータンパク質、コーンゼイン、ワックス、セルロース誘導体、ペクチンなどは、果物、ナッツ、穀物、野菜を使用して製造される食用フィルムです。さらに、メーカーはさまざまなタンパク質の形態を使用することにより、食用包装分野でも革新を進めています。

- たとえば、2022年 6月に、ベネデットマレリという科学者は、シルクタンパク質を使用するために、Moriというバイオテクノロジーのスタートアップを立ち上げました。これらのタンパク質は、庭の野菜、柔らかくしたステーキ、新鮮な鶏肉、その他の生鮮食品や包装食品のコーティングに使用されます。

アジア太平洋が世界市場を独占し続ける

- 中国と日本は、この地域の食用フィルムおよびコーティング市場の主要消費者です。中国では、キサンタンガムは食品に最も一般的に使用される食用コーティングの1つであり、多糖類ベースのフィルムおよびコーティングに対する高い需要が生じています。

- しかし、この地域では食用コーティングの他の供給源を発見する調査が行われており、これにより製品の賞味期限が延長され、鮮度が長持ちすると期待されています。さらに、インドのような国での意識の高まりにより、予測期間中に非常に有望な市場シナリオがもたらされると予測されています。

- 2021年4月、BASFは香港でJoncryl HPB(ハイパフォーマンスバリア)を発売しました。同社によれば、この特定の製品は、最新の包装動向と天然資源の保護において重要な役割を果たす水ベースの液体バリアコーティングであるといいます。この新たな立ち上げの背後にある戦略は、会社のビジネスを拡大することでした。

食用フィルムおよびコーティング業界の概要

食用フィルムおよびコーティング市場は、世界および地域の市場企業によって細分化されています。食用フィルムおよびコーティング市場で事業を展開している主要企業には、DuPont de Nemours Inc、Tate &Lyle、Cargill, Incorporated、Koninklijke DSM NV、およびIngredion Incorporatedが含まれます。食用フィルムおよびコーティングは、包装分野の成長市場であり、消費者が通常の消耗品からそのようなオプションを求めるため、需要は拡大すると予想されます。市場は今後数年間でさらに多くのイノベーションをし、業界は合併や買収を予想する可能性があります。最近新しいブランドが登場し、その提供内容に基づいて大きな注目を集めています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 成分の種類

- タンパク質

- 多糖類

- 脂質

- 複合材料

- 応用

- 乳製品

- ベーカリー・菓子類

- 果物と野菜

- 肉、鶏肉、魚介類

- その他の用途

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 北米のその他の地域

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- 南アフリカ

- サウジアラビア

- その他中東およびアフリカ

- 北米

第6章 競合情勢

- 市場シェア分析

- 最も採用されている戦略

- 企業プロファイル

- Tate &Lyle PLC

- DuPont de Nemours Inc.

- DOHler Group Se

- Koninklijke DSM NV

- Cargill, Incorporated

- Ingredion Incorporated

- RPM International, Inc.(Mantrose-Haeuser Co. Inc.)

- Nagase &Co Ltd

- Sumitomo Chemical Co. Ltd

- Sufresca

- Pace International, LLC

- AgroFresh Solutions, Inc.

- Akorn Technology, Inc.

第7章 市場機会と将来の動向

The Edible Films and Coating Market size is estimated at USD 3.32 billion in 2024, and is expected to reach USD 4.79 billion by 2029, growing at a CAGR of 7.64% during the forecast period (2024-2029).

Key Highlights

- The benefit of using edible coating on food products is that it acts as a barrier for carbon dioxide, lipids, moisture, oxygen, and aromas. It improves food quality and extends the shelf life of products. One major advantage of using edible films and coatings is that several active ingredients can be incorporated into the polymer matrix and consumed with food, thus, enhancing safety or even nutritional and sensory attributes. The edible coatings can be made from soybean protein, wheat gluten, whey, gelatin, and many more.

- Demand for plant-based food products is increasing among consumers because of their benefits and health consciousness. The food product manufacturers have increased their efforts to increase the shelf life and improve the existing packaging technology, ensuring the microbial safety and preservation of food from the influence of external factors. Technological institutes and researchers are innovating new technologies to develop edible films with the use of different components.

- For instance, in September 2022, the Indian Institute of Technology, Guwahati, developed an edible coating to extend the shelf life of fruits and vegetables. The coating is made from a mix of microalgae extract and polysaccharides. The marine microalgae Dunaliella tertiolecta, known for its antioxidant properties, is used for its various bioactive compounds such as carotenoids, proteins, and polysaccharides. Thus, new product innovations from manufacturers are expected to contribute to the market growth of the edible films and coatings market.

Edible Films & Coatings Market Trends

Increasing Demand for Edible Packaging from Natural Resources

- Traditional food packaging materials have many shortcomings like environmental effects, pollution, manufacturing requirements, and wastage. The need for alternative packaging materials and packaging formats has increased at a significant level.

- Issues about sustainability, ethics, food safety, food quality, and product costs are all becoming increasingly important factors for modern-day consumers at the time of purchasing food products, and food packaging legislative regulations enforce a number of these issues. All these factors have largely contributed to the rising demand for edible films and coatings in the food packaging industry. These edible films are extracted from natural and organic products.

- For instance, wheat gluten, whey protein, corn zein, waxes, cellulose derivatives, and pectins are some edible films manufactured using fruits, nuts, grains, and vegetables. Additionally, manufacturers are innovating in the edible packaging space by using various protein forms.

- For instance, in June 2022, a scientist named Benedetto Marelli launched a biotech startup called Mori to use silk proteins. These proteins are used to coat garden vegetables, tenderized steaks, fresh poultry, and other perishable and packaged foods.

Asia-Pacific Continues to Dominate the Global Market

- China and Japan are the major consumers of the region's edible films and coatings market. In China, xanthan gum is one of the most commonly used edible coatings in food products, giving rise to the high demand for polysaccharide-based films and coatings.

- However, research to discover other sources of edible coatings is being conducted in the region, which is expected to extend the shelf life and prolong the freshness of products. Moreover, the rising awareness in countries like India is projected to lead to a very promising market scenario in the forecast period.

- In April 2021, BASF launched Joncryl HPB (High-Performance Barrier) in Hong Kong. According to the firm, this specific product is a water-based liquid barrier coating that plays an important role in the latest packaging trends and the conservation of natural resources. The strategy behind this new launch was to expand the company's business.

Edible Films & Coatings Industry Overview

The edible films and coating market is fragmented with global and regional market players. The major players operating in the edible films and coatings market include DuPont de Nemours Inc, Tate & Lyle, Cargill, Incorporated, Koninklijke DSM N.V., and Ingredion Incorporated. Edible film and coatings are a growing market within the packaging segment, where the demand is expected to upscale as consumers seek such options from their regular consumables. The market is poised to witness more innovations over the coming years, and the industry may expect mergers and acquisitions. New brands have emerged recently and have gained significant traction based on their offerings.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Ingredient Type

- 5.1.1 Protein

- 5.1.2 Polysaccharides

- 5.1.3 Lipids

- 5.1.4 Composites

- 5.2 Application

- 5.2.1 Dairy products

- 5.2.2 Bakery and Confectionery

- 5.2.3 Fruits and Vegetables

- 5.2.4 Meat, Poultry, and Seafood

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Most Adopted Strategies

- 6.3 Company Profiles

- 6.3.1 Tate & Lyle PLC

- 6.3.2 DuPont de Nemours Inc.

- 6.3.3 DOHler Group Se

- 6.3.4 Koninklijke DSM N.V.

- 6.3.5 Cargill, Incorporated

- 6.3.6 Ingredion Incorporated

- 6.3.7 RPM International, Inc. (Mantrose-Haeuser Co. Inc.)

- 6.3.8 Nagase & Co Ltd

- 6.3.9 Sumitomo Chemical Co. Ltd

- 6.3.10 Sufresca

- 6.3.11 Pace International, LLC

- 6.3.12 AgroFresh Solutions, Inc.

- 6.3.13 Akorn Technology, Inc.