航空燃料:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Aviation Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687253

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

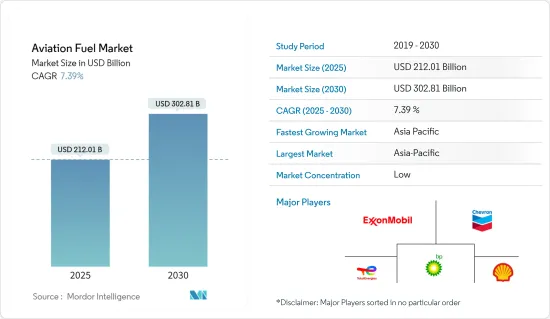

航空燃料市場規模は2025年に2,120億1,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは7.39%で、2030年には3,028億1,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、航空需要の増加と航空機保有数の増加が予測期間中の市場を牽引するとみられます。

- 一方、大気汚染に対する環境問題の高まりは、予測期間中の市場成長の妨げになると予想されます。

- サステイナブル航空燃料技術の進歩が進むことで、航空燃料市場に大きなビジネス機会が生まれると期待されています。

- アジア太平洋は、同地域における航空旅行と航空機保有台数の増加により、航空燃料市場の支配的な地域となることが予想されます。

航空燃料市場の動向

航空タービン燃料が市場を独占する見込み

- 一般にジェット燃料として知られる航空タービン燃料(ATF)は、灯油に似た組成を持つ石油由来の燃料です。ジェットA、ジェットA-1、ジェットBなど、世界的にさまざまなグレードがあり、ジェットA-1が最も一般的に利用されています。ジェットA-1は、さまざまな航空機のタービンエンジンに適合します。最低引火点は摂氏38度(100°F)、最高凍結点は摂氏-47度です。

- 航空タービン燃料は、民間旅客機、軍用機、ビジネスジェット機など、さまざまな航空機に使用されています。現在就航しているほとんどの航空機、特に大型の民間航空機は、一次エネルギー源としてジェット燃料に依存しています。様々なタイプの航空機でジェット燃料が広く使用されていることが、市場におけるジェット燃料の優位性に寄与しています。

- さらに、民間航空や軍用航空に普及しているジェットエンジンは、効率的に作動するために航空タービン燃料を必要とします。これらのエンジンは、ジェット燃料のエネルギー含有量と燃焼特性を利用するように設計されています。ジェットエンジンが航空産業において支配的な推進技術であり続ける限り、航空タービン燃料の需要は引き続き大きいです。

- 例えば、米国エネルギー情報局によると、米国におけるジェット燃料の消費量は2022~2021年の間に14%近く増加しており、これは航空機の運航と燃料消費の増加を示しています。

- 航空タービン燃料は、ピストンエンジン機に使用されるアベガスなどの他の燃料よりもエネルギー密度が高いです。これは、ジェット燃料が単位体積当たりにより多くのエネルギーを供給できることを意味し、長距離フライトや大型航空機にとって極めて重要です。航空タービン燃料の高いエネルギー密度は、ジェットエンジンの動力源として理想的であり、効率的で長時間の飛行を可能にします。

- 2023年1月、Indian Oil Corp(IOC)は、小型航空機や無人航空機(UAV)の要求に応える航空燃料の輸出を開始しました。この動きにより、インドは石油輸出に乗り出すことで、約27億米ドルと評価される世界市場に参入することができます。Jawaharlal Nehru Port Trust(JNPT)は、パプアニューギニアへの80バレルの航空燃料からなる最初の委託品の出荷を促進しました。1バレルの容量は16キロリットルで、かなりの量の航空ガスを輸送することができます。

- 従って、議論されているように、航空タービン燃料は予測期間中に市場を縮小させることが予想されます。

アジア太平洋が市場を独占する見込み

- アジア太平洋は著しい経済成長を遂げており、中国、インド、東南アジア諸国などがこの拡大を牽引しています。経済成長に伴って航空需要が増加し、航空燃料消費量の増加に直結します。この地域の力強い経済成長は、航空燃料市場の優位性を高めています。

- アジア太平洋は航空産業が盛んで、数多くの航空会社が存在し、航空機の保有台数も増加しています。同地域の航空会社は継続的に事業を拡大し、新規路線を増やし、飛行頻度を増やしています。このような拡大が航空燃料の需要を高め、同地域における航空燃料市場の優位性に寄与しています。

- さらに、アジア太平洋における急速な都市化と中流階級の人口の増加が、航空旅行の急増につながっています。同地域で航空輸送を利用する人が増えるにつれ、航空燃料の需要も伸びています。都市化の進展と中間層の急増が、アジア太平洋における市場の優位性を高める主要因となっています。

- さらに、アジア太平洋では格安航空会社(LCC)の出現と成長が見られます。これらの航空会社は手頃な航空運賃を提供し、より多くの人口層を惹きつけ、航空需要を刺激しています。LCCは通常、高い搭乗率で運航するため、燃料消費量の増加につながり、その結果、この地域における航空燃料市場の優位性を高めています。

- さらに、アジア太平洋の多くの国々が空港インフラ開発に多額の投資を行っています。新しい空港が建設され、既存の空港も拡大と近代化が進められています。こうしたインフラ投資は、航空交通量と燃料消費量の増加に有利な条件を生み出し、航空燃料市場における同地域の優位性をさらに高めています。

- 例えば、2023年5月、Indian Oil Corp.は、脱炭素目標を達成するために航空会社が必要とする世界の供給が大幅に不足しているため、1億2,200万米ドルのサステイナブル航空燃料(SAF)プラントを建設する予定です。この計画施設は、年間8万8,000トンのSAFを製造する能力を持っています。

- 以上のことから、予測期間中はアジア太平洋が市場を独占すると予想されます。

航空燃料産業概要

航空燃料市場はセグメント化されています。市場の主要企業(順不同)には、ExxonMobil、Chevron Corporation、Shell Plc.、TotalEnergies SE、BPなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 航空需要の増加

- 航空機材の拡大

- 抑制要因

- 不安定な原油価格

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 燃料タイプ

- エアタービン燃料

- ジェットA-1

- ジェットA

- ジェットB

- 航空バイオ燃料

- AVGAS

- エアタービン燃料

- エンドユーザー

- 商業

- 防衛

- 一般航空

- 市場分析:地域別、2028年までの市場規模と需要予測(地域別)

- 北米

- 米国

- カナダ

- その他の北米地域

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Exxon Mobil Corporation

- Chevron Corporation

- Shell Plc.

- TotalEnergies SE

- BP Plc

- Gazprom Neft'PAO

- Neste Oyj

- Swedish Biofuels AB

- Red Rock Biofuels LLC

- Abu Dhabi National Oil Company

- Bharat Petroleum Corp. Ltd.

- Indian Oil Corporation Ltd.

- Emirates National Oil Company

- Valero Energy Corporation

- Allied Aviation Services Inc.

第7章 市場機会と今後の動向

- バイオ燃料とサステイナブル代替燃料

目次

Product Code: 57160

The Aviation Fuel Market size is estimated at USD 212.01 billion in 2025, and is expected to reach USD 302.81 billion by 2030, at a CAGR of 7.39% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the increasing demand for air travel and an increasing fleet of aircraft is expected to drive the market during the forecasted period.

- On the other hand, the increasing environmental concerns for air pollution are expected to hinder the growth of the market during the forecasted period.

- Nevertheless, the increasing advancements in sustainable aviation fuel technology are expected to create huge opportunities for the aviation fuel market.

- Asia-Pacific is expected to be a dominant aviation fuel market region due to the increasing air travel and aircraft fleets in the region.

Aviation Fuel Market Trends

Aviation Turbine Fuels Expected to Dominate the Market

- Aviation Turbine Fuel (ATF), commonly known as jet fuel, is a petroleum-derived fuel with a composition resembling kerosene. It is available in different grades globally, including Jet A, Jet A-1, and Jet B, with Jet A-1 being the most commonly utilized. Jet A-1 is compatible with a wide range of aircraft turbine engines. It exhibits a minimum flash point of 38 degrees Celsius (100°F) and a maximum freeze point of -47 degrees Celsius.

- Aviation turbine fuels are used in various aircraft, including commercial airliners, military, and business jets. Most aircraft in service today, especially larger commercial aircraft, rely on jet fuel as their primary energy source. The widespread usage of jet fuel in various aircraft types contributes to its dominance in the market.

- Moreover, jet engines, prevalent in commercial and military aviation, require aviation turbine fuels to operate efficiently. These engines are designed to utilize jet fuel's energy content and combustion properties. As long as jet engines remain the dominant propulsion technology in the aviation industry, the demand for aviation turbine fuels will continue to be significant.

- For instance, according to the United States Energy Information Administration, the consumption of jet fuel in the United States increased by almost 14% between 2022 and 2021, signifying the increasing air ravels and fuel consumption.

- Aviation turbine fuels have a higher energy density than other fuels, such as avgas used in piston-engine aircraft. This means that jet fuel can provide more energy per unit of volume, which is crucial for long-haul flights and larger aircraft. The high energy density of aviation turbine fuels makes them ideal for powering jet engines and allows for efficient and extended flight operations.

- In January 2023, The Indian Oil Corporation (IOC) initiated the export of aviation fuel, catering to the requirements of small aircraft and unmanned aerial vehicles (UAVs). This move allows India to enter the global market, valued at approximately USD 2.7 billion, by venturing into petroleum exports. The Jawaharlal Nehru Port Trust (JNPT) facilitated the shipment of the first consignment comprising 80 barrels of aviation fuel to Papua New Guinea. Each barrel has a capacity of 16 kiloliters, enabling the transport of a significant quantity of aviation gas.

- Therefore as per the points discussed, aviation turbine fuel is expected to diminish the market during the forecasted period.

Asia-Pacific Expected to Dominate the Market

- The Asia-Pacific region is experiencing significant economic growth, with countries like China, India, and Southeast Asian nations driving this expansion. As economies grow, there is a corresponding increase in air travel demand, directly translating to higher aviation fuel consumption. The region's robust economic growth fuels the dominance of the aviation fuel market.

- The Asia-Pacific region has a flourishing airline industry with numerous carriers and a growing fleet of aircraft. Airlines in the region continuously expand their operations, adding new routes and increasing flight frequencies. This expansion necessitates a higher demand for aviation fuel, contributing to the dominance of the market in the region.

- Moreover, rapid urbanization in the Asia-Pacific region and the rise of the middle-class population has led to a surge in air travel. As more people in the region access air transportation, the demand for aviation fuel grows. The increasing urbanization and a burgeoning middle-class population are key factors driving the dominance of the market in the Asia-Pacific region.

- Furthermore, Asia-Pacific region has witnessed the emergence and growth of low-cost carriers (LCCs). These airlines offer affordable airfares, attracting a larger segment of the population and stimulating air travel demand. LCCs typically operate with higher load factors, leading to increased fuel consumption and subsequently driving the aviation fuel market's dominance in the region.

- Additionally, many countries in the Asia-Pacific region are investing heavily in airport infrastructure development. New airports are being built, and existing ones are undergoing expansion and modernization. These infrastructure investments create favorable conditions for increased air traffic and fuel consumption, further contributing to the region's dominance in the aviation fuel market.

- For instance, in May 2023, Indian Oil Corp. intends to construct a sustainable aviation fuel (SAF) plant worth USD 122 million due to the substantial shortfall in global supplies required by airlines to achieve decarbonization targets. The planned facility will have the capability to manufacture 88,000 tons of SAF annually.

- Therefore as per the above-mentioned points the Asia-Pacific region is expected to dominate the market during the forecasted period.

Aviation Fuel Industry Overview

The Aviation fuel market is fragmented. Some of the major players in the market (in no particular order) include ExxonMobil Corporation, Chevron Corporation, Shell Plc., TotalEnergies SE, and BP Plc. among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Air Travel Demand

- 4.5.1.2 Expanding Airline Fleet

- 4.5.2 Restraints

- 4.5.2.1 Volatile Crude Oil Prices

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 Air Turbine Fuel

- 5.1.1.1 Jet A-1

- 5.1.1.2 Jet A

- 5.1.1.3 Jet B

- 5.1.2 Aviation Biofuel

- 5.1.3 AVGAS

- 5.1.1 Air Turbine Fuel

- 5.2 End-User

- 5.2.1 Commercial

- 5.2.2 Defence

- 5.2.3 General Aviation

- 5.3 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Chile

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Egypt

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Exxon Mobil Corporation

- 6.3.2 Chevron Corporation

- 6.3.3 Shell Plc.

- 6.3.4 TotalEnergies SE

- 6.3.5 BP Plc

- 6.3.6 Gazprom Neft' PAO

- 6.3.7 Neste Oyj

- 6.3.8 Swedish Biofuels AB

- 6.3.9 Red Rock Biofuels LLC

- 6.3.10 Abu Dhabi National Oil Company

- 6.3.11 Bharat Petroleum Corp. Ltd.

- 6.3.12 Indian Oil Corporation Ltd.

- 6.3.13 Emirates National Oil Company

- 6.3.14 Valero Energy Corporation

- 6.3.15 Allied Aviation Services Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Biofuels and Sustainable Alternatives

航空燃料:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日