南米の航空燃料:市場シェア分析、産業動向、成長予測(2025~2030年)

South America Aviation Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690765

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

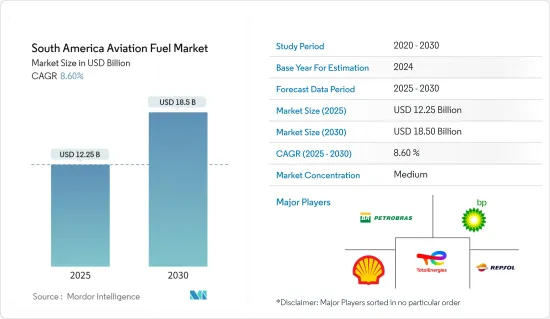

南米の航空燃料市場規模は2025年に122億5,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは8.6%で、2030年には185億米ドルに達すると予測されます。

主要ハイライト

- 中期的には、最近の航空運賃の安さによる航空旅客数の回復、より堅調な経済状況、可処分所得の増加などが市場の主要な促進要因のひとつです。

- その一方で、南米諸国では化石燃料をベースとする航空燃料のシェアが高く、環境悪化の原因となっているため、市場は今後数年間でハードルに直面する可能性があります。

- 南米はバイオ燃料の主要地域のひとつです。航空用バイオ燃料へのシフトが進む中、近い将来大きなビジネス機会が生まれる可能性が高いです。

- ブラジルは南米最大の航空燃料消費国であり、同地域における優位性をもたらしています。市場の成長により、ブラジルは予測期間中もその優位性を維持すると予想されます。

南米の航空燃料市場動向

商業セクタが著しい成長を遂げる

- 民間航空は、定期便と非定期便の航空機を運航し、旅客や貨物の商業航空輸送を促進します。このセグメントでは、民間部門が航空燃料の主要消費者の一つとして際立っており、航空会社の総運航支出の約4分の1を占めています。

- ラテンアメリカ・カリブ海地域(LAC)における2022年12月の総輸送旅客数は3,230万人でした。一方、LATAM地域の航空会社グループによる搭乗者総数は53,861人でした。

- ブラジル、パラグアイ、ペルーといった国々で進行中の空港民営化は、空港インフラの開拓と収容能力の増加に寄与し、それによって同地域の調査対象市場の下支えとなると予想されます。

- 逆に、同地域では短距離便の割合が顕著に増加しており、航空輸送量の割合が増加しています。ラテンアメリカでは、格安航空会社(LCC)と超低価格航空会社(ULCC)の動きが大きな勢いを見せています。現在、同地域の格安航空会社は、これまで以上に加速度的な成長を遂げており、レガシー航空会社をしのぐ勢いを見せています。

- さらに2023年8月、Air bpはLABACE 2023で発表したように、ブラジルのサンパウロ州に位置するパウリニアに航空機燃料供給ハブを設立する計画を明らかにしました。この施設は2023年に操業を開始する予定で、1,000万米ドルを超える同社の戦略的投資の一環です。この構想は、物流の柔軟性を高め、航空機運航会社への燃料供給オプションを改善することを目的としています。

- さらに、Air bpはサンパウロコンゴーニャス空港で新たな燃料タンクファームの開発を進めており、2024年の稼働を目指しています。これら2つの今後の施設は重要な投資を意味し、航空部門におけるインフラとサービスの強化に対するエアbpのコミットメントを示すものです。

- このように、上記の要因は、予測期間中に商業セグメントの成長を促進すると予想されます。

市場を独占するブラジル

- 南米では、ブラジルが航空燃料の最大消費国です。同国の航空機用指定製品には、航空灯油(QAV)、航空ガソリン、代替航空灯油(代替QAV)が含まれます。

- ブラジルの民間航空市場は規模が大きく、ANACの報告によると、2022年には前年比39%増の83万1,000便が記録されました。Anuario do Transporte Aereo 2022によると、このうち国内便は73万1,000便で、33.7%の大幅増となったが、国際便は10万便で、89%の大幅増となりました。

- ブラジルにおける航空燃料の販売は、Petrobrasが特定のロットの化学品検査結果を理由に輸入航空燃料の供給を停止した影響に直面しました。この開発により、BR DistribuidoraやRaizenなどの大手燃料販売会社も同製品の販売を一時的に停止しました。しかし、状況は改善し、航空燃料の販売はその影響から回復しました。

- さらに2023年10月、Boeingはブラジルにエンジニアリング技術センターを正式に開設し、最先端の技術開発を通じて航空宇宙イノベーションを推進する世界15のBoeingのエンジニアリング拠点に加わりました。また、カンピーナス州立大学(Unicamp)との協力により、Boeingは持続可能性に関する協力関係を拡大するための財政支援も発表しました。この拡大は、ブラジルの特定地域におけるサステイナブル航空燃料(SAF)生産のための最も有望な投入物の実行可能性を理解することを目的とした、SAFMapsデータベースの第3段階の開発を含みます。

- 全体として、ブラジルの航空燃料市場は、市場のさらなる成長を後押しすると思われる政府のイニシアティブにより、予測期間中にまずまずの成長を記録すると予想されます。

南米の航空燃料産業概要

南米の航空燃料市場は細分化されています。主要企業(順不同)は、Petroleo Brasileiro SA、BP PLC、Shell PLC、TotalEnergies SE、Repsol SAなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 牽引役

- 最近の航空運賃の安さによる航空旅客数の回復

- 人口の可処分所得の増加

- 抑制要因

- 南米諸国における化石燃料ベースの航空燃料の高いシェア

- 牽引役

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 燃料タイプ

- エアタービン燃料(ATF)

- 航空バイオ燃料

- アブガス

- 用途

- 業務用

- 防衛

- 一般航空

- 地域

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Petroleo Brasileiro SA

- Repsol SA

- BP PLC

- Shell PLC

- TotalEnergies SE

- Pan American Energy SL

- Exxon Mobil Corporation

- Allied Aviation Services Inc.

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 航空バイオ燃料へのシフトの高まり

目次

Product Code: 71500

The South America Aviation Fuel Market size is estimated at USD 12.25 billion in 2025, and is expected to reach USD 18.50 billion by 2030, at a CAGR of 8.6% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the recovering number of air passengers, on account of cheaper airfare in recent times, more robust economic conditions, and increasing disposable income are among the major driving factors for the market.

- On the other hand, the market can face hurdles in the coming years due to the high share of fossil-fuel-based aviation fuels in South American countries, which are responsible for the degradation of the environment.

- Nevertheless, South America is one of the leading regions in biofuels. With an increasing shift towards aviation biofuels, significant opportunities are likely to be created in the near future.

- Brazil is the largest consumer of aviation fuels in South America, resulting in its dominance in the region. With the growing market, the nation is expected to continue its dominance during the forecast period.

South America Aviation Fuel Market Trends

The Commercial Sector to Witness a Significant Growth

- Commercial aviation involves the operation of both scheduled and non-scheduled aircraft, facilitating the commercial air transportation of passengers or cargo. Within this sector, the commercial segment stands out as one of the leading consumers of aviation fuel, constituting approximately a quarter of the total operating expenditure for airline operators.

- The total number of passengers transported in Latin America and the Caribbean (LAC) was 32.3 million in December 2022, which is the highest number of passengers. Meanwhile, the LATAM region had a total number of 53,861 passengers boarded by the airline group.

- The ongoing privatization of airports in countries like Brazil, Paraguay, and Peru is anticipated to contribute to the development of airport infrastructure and an increase in capacity, thereby providing support to the studied market in the region.

- Conversely, there has been a notable rise in the share of short-haul flights within the region, leading to an increased proportion of air traffic. In Latin America, the low-cost (LCC) and ultra-low-cost (ULCC) movements are experiencing significant momentum. Currently, more than ever, low-cost carriers in the region are witnessing accelerated growth, outpacing legacy airlines in their ascent.

- Moreover, in August 2023, Air bp has revealed plans to establish an aircraft fuel supply hub in Paulinia, located in Brazil's Sao Paulo state, as announced during LABACE 2023. The facility, anticipated to commence operations in 2023, is part of the company's strategic investment exceeding USD 10 million. This initiative aims to enhance logistical flexibility and provide improved fuel supply options for aircraft operators.

- Additionally, Air bp is in the process of developing a new fuel tank farm at Sao Paulo Congonhas Airport, set to become operational in 2024. These two upcoming facilities signify a significant investment, demonstrating Air bp's commitment to bolstering infrastructure and services in the aviation sector.

- Thus, the factors mentioned above are expected to drive growth in the commercial segment during the forecast period.

Brazil to Dominate the Market

- In South America, Brazil holds the distinction of being the largest consumer of aviation fuels. The designated products for aircraft use in the country encompass aviation kerosene (QAV), aviation gasoline, and alternative aviation kerosene (alternative QAV).

- The commercial aviation market in Brazil is substantial, with 831,000 flights recorded in 2022, marking a notable 39% increase compared to the previous year, as reported by ANAC. Within this total, 731,000 flights were domestic, reflecting a significant uptick of 33.7%, while international flights accounted for 100,000, showcasing a remarkable 89% increase, according to the Anuario do Transporte Aereo 2022.

- The sales of aviation fuel in Brazil faced an impact from Petrobras' suspension of the supply of imported aviation fuel due to chemical test results from a specific batch, which raised potential concerns. This development also prompted major fuel distributors, including BR Distribuidora and Raizen, to temporarily halt the sale of the product. However, the situation has improved and sales of aviation fuel has recovered from that impact.

- Moreover, In October 2023, Boeing officially inaugurated its Engineering and Technology Center in Brazil, joining the roster of 15 Boeing engineering sites worldwide dedicated to advancing aerospace innovation through cutting-edge technology development. In collaboration with the State University of Campinas (Unicamp), Boeing has also disclosed financial support to expand their sustainability collaboration. This extension involves the development of the third phase of the SAFMaps database, aimed at comprehending the viability of the most promising inputs for Sustainable Aviation Fuel (SAF) production in specific regions of Brazil.

- Overall, the aviation fuel market for Brazil is expected to register decent growth during the forecast period, owing to the supporting government initiatives, which are likely to aid the market's growth further.

South America Aviation Fuel Industry Overview

The South American aviation fuel market is semi-fragmented. Some of the major companies (in no particular order) are Petroleo Brasileiro SA, BP PLC, Shell PLC, TotalEnergies SE, and Repsol SA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Recovering Number of Air Passengers, on Account of the Cheaper Airfare in Recent Times

- 4.5.1.2 Increasing Disposable Income of Population

- 4.5.2 Restraints

- 4.5.2.1 High Share of Fossil-Fuel-Based Aviation Fuels in South American Countries

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 Air Turbine Fuel (ATF)

- 5.1.2 Aviation Biofuel

- 5.1.3 AVGAS

- 5.2 Application

- 5.2.1 Commercial

- 5.2.2 Defense

- 5.2.3 General Aviation

- 5.3 Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Colombia

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Petroleo Brasileiro SA

- 6.3.2 Repsol SA

- 6.3.3 BP PLC

- 6.3.4 Shell PLC

- 6.3.5 TotalEnergies SE

- 6.3.6 Pan American Energy SL

- 6.3.7 Exxon Mobil Corporation

- 6.3.8 Allied Aviation Services Inc.

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Shift Towards Aviation Biofuels

南米の航空燃料:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日