|

市場調査レポート

商品コード

1432931

軍用機近代化およびレトロフィット:市場シェア分析、産業動向、成長予測(2024年~2029年)Military Aircraft Modernization And Retrofit - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 軍用機近代化およびレトロフィット:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

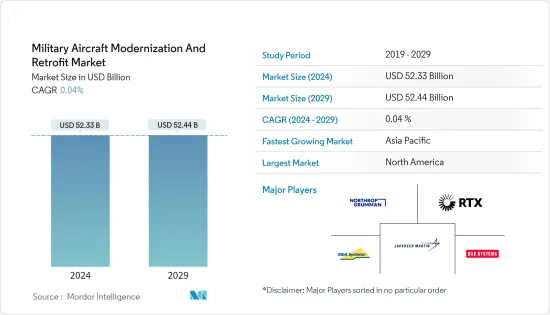

軍用機近代化およびレトロフィット市場規模は2024年に523億3,000万米ドルと推定され、2029年には524億4,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは0.04%で成長する見込みです。

主なハイライト

- 軍用航空部門は、パンデミック時に軽度の課題に直面しています。エアバスやボーイングなどの大手防衛関連企業は、従業員の安全への懸念や政府による操業停止により生産を停止しました。地元企業はサプライチェーンの問題と部品不足に直面し、パンデミック期間中の市場成長を阻害しました。パンデミック後の市場は、軍事近代化計画の増加と最新鋭軍用機の調達増加により力強い回復を見せた。

- 新興国の軍事費の増加は、老朽化した航空機の既存装備の近代化、主に新鋭装備への投資を促進しています。これが予測期間中の軍用機近代化・改修市場の成長を促進すると予想されます。先端材料、アビオニクス、ミッションシステムなど、軍用機の技術の進化は市場の成長に寄与しています。航空機が高度化するにつれて、これらの複雑なシステムを効率的に保守・修理するためには、専門的な知識と高度な診断ツールが必要となります。ステルス機能やサイバーセキュリティ対策などの先端技術の取り込みは、MROプロバイダーに新たな課題と機会をもたらし、これらの進化する要件に対応するための専門的なサービスや専門知識の必要性を促しています。継続的な技術の進歩と革新も、軍用機市場の成長を後押ししています。

軍用機近代化およびレトロフィット市場の動向

固定翼機セグメントが市場で最も高いシェアを占める

- 現在、固定翼機セグメントが市場を独占しており、予測期間中もその支配が続くと予想されます。成長の背景には、空軍能力向上のための戦闘機調達の増加や、軍用機近代化計画の増加があります。各軍の旧式で老朽化した航空機には、F-16ファイティングファルコン、F-15イーグル、ノースロップF-5、スホーイSu-27、L-100ハーキュリーズ、アントノフAn-24などがあります。軍用装備品や軍用機に搭載される航空機の開発、寿命延長プログラムのニーズの高まりが、予測期間中の同セグメントの成長を後押ししています。

- 例えば、2023年3月、Leonardo S.p.Aとイタリア国防省の空軍軍備・耐空性総局であるArmaereoは、イタリア空軍のC-27J Spartanフリートをアップグレードする契約を締結しました。この契約には、C-27J用の新しいアビオニクス構成の開発、統合、資格認定、認証、自己保護システムのアップグレード、航空機の一般的なシステムの交換、フライトシミュレータが含まれています。また、この構成の最初の航空機の引き渡しと、残りの11機の改修も含まれます。このような発展と近代化契約は、予測期間中の市場の成長を促進します。

アジア太平洋地域は予測期間中に目覚ましい成長を見せるだろう

- アジア太平洋地域は予測期間中に最も高い成長を記録すると予測されています。同地域では、軍事費の増加と現在進行中の政治的緊張が、老朽化した軍用機の近代化計画を後押ししています。ストックホルム国際平和研究所(SIPRI)の報告書(2022年版)によると、中国とインドは世界第2位と第4位の国防支出国であり、国防予算はそれぞれ2,930億米ドルと814億米ドルでした。アジア諸国は、状況認識を強化するため、既存の戦闘機群をアップグレードしています。

- 例えば、2023年2月、近代化活動で大きな経験を持つクラウン・グループは、インド海軍のMiG 29Kや、国際的な重要なOEM提携関係にあるMiG 29、ミラージュ2000、スホーイなど、インドの既存の戦闘機隊に対して、フルメンテナンス、交換、アビオニクス・サポートを提供すると発表しました。さらに、当グループはAtmanirbhar Bharatイニシアチブも支援しています。防衛航空宇宙MROとアビオニクス修理に対応する、軍と産業界からの訓練を受けた専門家のコア・チームによって管理される2つの最新鋭施設を設立しました。このように、軍用機近代化およびレトロフィットプログラムへの投資の増加と軍用機フリートの増加が、地域全体の市場の成長を促進しています。

軍用機近代化およびレトロフィット産業の概要

軍用機近代化およびレトロフィット市場は細分化された市場であり、多様な製品ポートフォリオとともに、さまざまな航空機プログラムをサポートする多くのプレーヤーが存在します。この市場で著名なプレーヤーには、ロッキード・マーチン社、ノースロップ・グラマン社、レイセオン・テクノロジーズ社、エルビット・システムズ社、BAEシステムズ社などがあります。

コックピット技術、兵器システム、構造アップグレードの進歩は、軍用機近代化およびレトロフィット市場の成長を促進する要因の一部です。

近代化需要の高まりは、メーカーに新たな市場機会をもたらし、既存の航空機装備の近代化に関する様々な国からの契約は、今後数年間、企業が世界の存在感を高めるだけでなく、売上にも貢献すると期待されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 航空機タイプ

- 固定翼

- 回転翼

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 日本

- 韓国

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Raytheon Technologies Corporation

- L3Harris Technologies, Inc.

- BAE Systems plc

- Elbit Systems Ltd.

- Honeywell International Inc.

- Israel Aerospace Industries Ltd.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Leonardo S.p.A

- Safran

- General Dynamics Corporation

- THALES

- The Boeing Company

第7章 市場機会と今後の動向

The Military Aircraft Modernization And Retrofit Market size is estimated at USD 52.33 billion in 2024, and is expected to reach USD 52.44 billion by 2029, growing at a CAGR of 0.04% during the forecast period (2024-2029).

Key Highlights

- The military aviation sector has faced mild challenges during the pandemic. Major defense contractors such as Airbus and Boeing halted production due to employee safety concerns and lockdowns imposed by governments. Local players faced supply chain issues and a shortage of components which hindered market growth during the pandemic period. The market showcased a strong recovery post covid due to the increasing number of military modernization programs and rising procurement of advanced military aircraft.

- The increasing military expenditure of emerging economies is propelling investments in the modernization of the existing equipment in aging aircraft, mainly with new and advanced equipment. This is expected to drive the growth of the military aircraft modernization and retrofit market during the forecast period. The evolution of technology in military aircraft, such as advanced materials, avionics, and mission systems, contributes to the growth of the market. As aircraft become more sophisticated, specialized expertise and advanced diagnostics tools are required to maintain and repair these complex systems effectively. The incorporation of advanced technologies, including stealth capabilities and cybersecurity measures, presents new challenges and opportunities for MRO providers, driving the need for specialized services and expertise to address these evolving requirements. Continuous technological advancements and innovations also drive market growth in military aviation.

Military Aircraft Modernization And Retrofit Market Trends

Fixed-Wing Aircraft Segment Holds Highest Shares in the Market

- The fixed-wing aircraft segment currently dominates the market, and it is expected to continue its dominance during the forecast period. The growth is attributed to the increasing procurement of fighter jets to improve air force capabilities and the rising number of military aircraft modernization programs. The old and aging aircraft fleet of various armed forces includes F-16 Fighting Falcon, F-15 Eagle, Northrop F-5, Sukhoi Su-27, L-100 Hercules, Antonov An-24, and Antonov An-24, among others. Developments in military equipment and onboard military aircraft, as well as the growth in the need for life extension programs, are bolstering the growth of the segment during the forecast period.

- For instance, in March 2023, Leonardo S.p.A and Armaereo, the Italian Defence Ministry's Air Force Armament and Airworthiness Directorate, signed a contract to upgrade Italian Air Force's C-27J Spartan fleet. The contract includes the development, integration, qualification, and certification of a new avionics configuration for the C-27J, the upgradation of the self-protection system, the replacement of general systems on the aircraft, and the flight simulator. It also includes the delivery of the first aircraft in this configuration and retrofitting of the remaining 11 aircraft. Such developments and modernization contracts drive the growth of the market during the forecast period.

Asia-Pacific Will Showcase Remarkable Growth During the Forecast Period

- The Asia-Pacific region is anticipated to register the highest growth during the forecast period. The increasing military spending and current ongoing political tensions in the region are propelling the modernization plans of the aging military aircraft fleet in the region. According to the 2022 edition of the Stockholm International Peace Research Institute (SIPRI) report, China and India were the second and fourth largest defense spenders in the world, with a defense budget of USD 293 billion and USD 81.4 billion, respectively. The Asian countries are upgrading their existing fleet of fighter aircraft to enhance their situational awareness.

- For instance, in February 2023, the Crown Group, which has a significant experience in modernization activities, announced that they would be providing full maintenance, replacement, and avionics support to the existing fleet of Indian fighter jets, such as the MiG 29K of the Indian Navy and the MiG 29, Mirage 2000 and Sukhoi under its significant international OEM tie up. Moreover, the Group is also supporting the Atmanirbhar Bharat initiative. It has set up two state-of-the-art facilities, managed by a core team of trained professionals from the military and industry catering to Defense Aerospace MRO and Avionics Repairs. Thus, increasing investment in military aircraft modernization and retrofitting programs and growing military aircraft fleets drive the growth of the market across the region.

Military Aircraft Modernization And Retrofit Industry Overview

The military aircraft modernization and retrofit market is a fragmented market, with many players supporting various aircraft programs, along with a diversified product portfolio. Some of the prominent players in this market are Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, Elbit Systems Ltd., and BAE Systems plc, among others.

Advancements in cockpit technologies, weapon systems, and structural upgrades are some of the factors driving the growth of the military aircraft upgrade and retrofit market as several countries look to modernize their existing fleet and enhance their aerial combat and surveillance capabilities.

The growing demand for modernization will open new market opportunities for manufacturers and the contracts from various countries for the modernization of existing aircraft equipment are expected to help the companies enhance their global presence as well as sales in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Aircraft Type

- 5.1.1 Fixed-Wing

- 5.1.2 Rotary-Wing

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Turkey

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Raytheon Technologies Corporation

- 6.2.2 L3Harris Technologies, Inc.

- 6.2.3 BAE Systems plc

- 6.2.4 Elbit Systems Ltd.

- 6.2.5 Honeywell International Inc.

- 6.2.6 Israel Aerospace Industries Ltd.

- 6.2.7 Lockheed Martin Corporation

- 6.2.8 Northrop Grumman Corporation

- 6.2.9 Leonardo S.p.A

- 6.2.10 Safran

- 6.2.11 General Dynamics Corporation

- 6.2.12 THALES

- 6.2.13 The Boeing Company