ヨーグルト:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Yogurt - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 365 Pages

- 納期

- 2~3営業日

- 商品コード

- 1938980

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

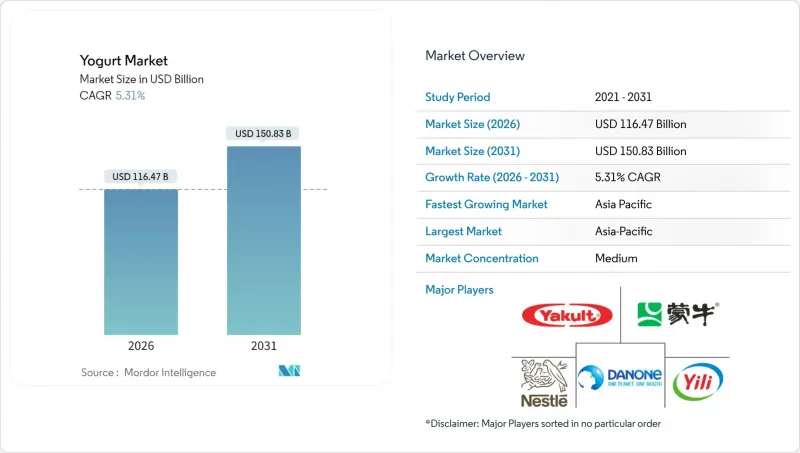

2026年のヨーグルト市場規模は1,164億7,000万米ドルと推定され、2025年の1,106億米ドルから成長を続けています。

2031年には1,508億3,000万米ドルに達する見込みで、2026年から2031年にかけてCAGR5.31%で拡大すると予測されています。

ヨーグルト市場は、臨床的に検証されたプロバイオティクス菌株と腸内健康への測定可能な効果との確かな関連性から引き続き恩恵を受けており、プレミアム化の促進とカテゴリーの着実な回復力強化につながっております。メーカー各社は、消化過程でも有益な細菌を生存させる先進的な発酵技術を採用し、機能性食品としてのポジショニングを強化するとともに、消費者のグレードアップ志向を持続させております。新興経済国における可処分所得の堅調な伸びと免疫サポートへの関心の高まりが需要をさらに後押しする一方、デジタルコマースは製品発見と定期購入型補充を加速させています。特にカフェやコンビニエンスストアにおける外食産業への浸透拡大が利用機会を広げ、常温保存可能包装の技術的進歩はコールドチェーンインフラが未整備な市場への進出を可能にしています。

世界のヨーグルト市場の動向と洞察

腸内環境・プロバイオティクス・免疫機能への消費者関心の高まり

プロバイオティクス菌株は、ヨーグルトの役割を単なる嗜好品から治療的栄養選択肢へと再定義しています。臨床研究により、ラクトバチルス・アシドフィルスやビフィドバクテリウム・ラクティスなどの特定細菌培養物が免疫機能と消化器健康を向上させる効果が確認されています。国立生物工学情報センター(NCBI)の報告によれば、これらの菌株は呼吸器感染症の期間を最大2日間短縮し、腸管バリア機能を強化することが示唆されています。こうした科学的裏付けにより、メーカーはプロバイオティクス強化製品のプレミアム価格設定を正当化できると同時に、実証済みの健康効果を通じて消費者の信頼を築けます。世界の医療費の増加に伴い、機能性ヨーグルトは具体的な健康効果をもたらす予防栄養食品として注目を集めています。さらに、規制当局が特定のプロバイオティクス菌株に対する健康強調表示を承認するケースが増加しており、臨床調査と菌株の革新を優先する企業に競争上の優位性をもたらしています。

栄養強化機能性ヨーグルトの開発

ヨーグルトはウェルネス製品として再定義されつつあり、メーカーは消費者の食事における特定の栄養不足を補うため、タンパク質分離物、オメガ3脂肪酸、ビタミン、ミネラルを添加しています。先進的なマイクロカプセル化技術により、発酵や保存過程で敏感な栄養素が保護され、プロバイオティクスやビタミンなどの熱に弱い成分の安定供給が実現されています。これは米国食品医薬品局(FDA)も認める事実です。こうした進歩を活かし、単品用ヨーグルト製品は現在、20~25グラムのタンパク質と完全なビタミンプロファイルを提供し、従来のサプリメントと直接競合しています。この戦略は、栄養不足が確認されている地域で特に効果的であり、強化ヨーグルトを必須栄養素の入手しやすい供給源として位置づけています。強化に関する主張の規制承認プロセスは参入障壁を生み、規制順守と臨床検証の専門知識を持つ確立されたメーカーに有利に働きます。

牛乳価格の変動と供給不安定性

牛乳価格の変動は利益率を圧迫し、サプライチェーンを混乱させます。これにより製造業者は、競争の激しい小売市場における消費者の価格感応度に対応しつつ、動的な価格戦略の実施を迫られています。米国農務省(USDA)の予測によれば、2025年まで牛乳価格は100重量ポンドあたり22~24米ドルで推移し、15~20%の変動幅がヨーグルト生産コストに直接影響します。天候関連の供給障害、飼料コストの上昇、乳牛群の統合により牛乳の安定供給が困難となり、生産計画と在庫管理が複雑化しています。小規模なヨーグルト生産者は、乳製品供給業者との交渉力が限られていること、金融商品による商品価格リスクの軽減能力が低いことから、より大きな課題に直面しています。さらに、乳製品生産が特定の地域に地理的に集中しているため、局所的な供給障害の影響を受けやすく、世界のヨーグルト製造ネットワークに影響を及ぼしています。

セグメント分析

2025年現在、スプーンで食べるタイプのヨーグルトは、消費者の強い嗜好と朝食・間食・デザートなど多様な消費シーンでの汎用性を背景に、67.42%という圧倒的な市場シェアを占めております。その成功は主に、分量の調整が容易である点と、混ぜ込みトッピングや多彩なフレーバーによるカスタマイズ性によって、製品の感覚的魅力と認知価値を向上させていることに起因しております。一方、飲用ヨーグルトは市場で最も急速な成長を遂げており、2031年までCAGR6.86%が見込まれています。この成長は主に、現代消費者の忙しいライフスタイルに合致する、手軽で移動中に摂取できる栄養ソリューションへの需要増加に起因しています。

革新的な包装技術は、プロバイオティクスの生存性を確保しつつ保存期間を延長することで、飲用ヨーグルトの成長に重要な役割を果たしてきました。これにより流通網の拡大が促進されています。また、カフェやコンビニエンスストアが液体形態を好む傾向が強まる中、飲用ヨーグルトセグメントは外食産業チャネルの拡大からも大きな恩恵を受けています。これらの形態は既存の飲料業務に容易に統合でき、最小限の準備で済むため、事業者にとって魅力的な選択肢となっています。さらに、FDA(米国食品医薬品局)はスプーンで食べるタイプと飲むタイプの両ヨーグルト形式の健康表示を支持していますが、飲むタイプは特に糖分含有量や栄養表示に関してより厳しい監視に直面しています。この規制上の焦点は製品処方の戦略に影響を与え、メーカーに革新を促し、進化する消費者と規制当局の期待に応えるよう求めています。

2025年現在、乳製品ベースのセグメントは53.95%という大きな市場シェアを占めております。これは伝統的な製造ノウハウと強固なサプライチェーンに支えられた結果です。これらの強みが、世界市場における安定した品質と競争力のある価格設定を可能にしております。消費者が乳製品に親しんでいること、そして天然の完全タンパク質を含むことが、健康面でのポジショニングを高め、栄養表示を裏付けています。一方、植物由来の代替品は著しい成長を見せており、2031年までCAGR7.78%が見込まれています。この成長は、乳糖不耐症への認識の高まり、環境持続可能性への懸念の増大、食習慣の変化といった要因によるもので、これらが相まって潜在市場規模を拡大していると、国立生物工学情報センター(NCBI)は指摘しています。

植物性タンパク質の分離技術や発酵技術の進歩により、非乳製品ヨーグルトは従来の乳製品と同等の食感や風味を実現しつつ、同様のプロバイオティクス効果を提供できるようになりました。アーモンド、オーツ、ココナッツをベースとした製品は、それぞれ異なる栄養プロファイルと風味特性を有し、多様な消費者層や使用シーンに訴求しています。しかしながら、植物由来セグメントは、特にタンパク質含有量の表示やプロバイオティクス菌株の生存率に関する規制上の課題に直面しています。これらの課題は専門的な製造プロセスと厳格な品質管理を必要とし、小規模生産者にとって大きな参入障壁となっています。

ヨーグルト市場は、製品タイプ別(フレーバーヨーグルト、プレーンヨーグルト)、流通チャネル別(小売流通、外食流通)、地域別(アフリカ、アジア太平洋、欧州、中東、北米、南米)に分類されます。市場規模は米ドルベースの金額と数量の両方で提示されます。主要なデータポイントとして、一人当たり消費量、人口、乳製品生産量が観察されています。

地域別分析

2025年時点でアジア太平洋地域は55.78%という圧倒的な市場シェアを占め、2031年まで11.9%という高い成長率が予測されています。この成長は、同地域における伝統的な発酵食品の習慣と、様々な経済段階における西洋式ヨーグルトの急速な普及が相まって生み出されています。中国とインドにおける都市化は可処分所得の増加と健康意識の高まりを促進し、地域の拡大を後押ししています。一方、日本や韓国などの成熟市場では、プレミアムなプロバイオティクス技術革新や機能性栄養食品に注力しています。同地域の乳製品生産能力と植物由来代替品の台頭は、多様な食習慣ニーズや乳糖不耐症の広範な普及に対応しています。ただし、アジア太平洋地域の規制枠組みは国によって大きく異なり、厳格なプロバイオティクス菌株要件を課す国もあれば、より柔軟な健康強調表示基準を採用する国もあり、製品開発戦略に影響を与えています。

欧州は成熟市場ながら、ヨーグルト産業において戦略的に重要な位置を占め続けております。同地域の消費者は有機栽培、プレミアム、職人の技を活かしたヨーグルト製品を好んでおり、これらは高価格帯で取引されることが多く、カテゴリー内のイノベーションを牽引しております。欧州の確立された乳製品インフラと厳格な食品安全規制は、現地生産者に競争優位性をもたらすと同時に、世界の品質基準を設定しています。ドイツ、フランス、オランダなどの国々は一人当たり消費量でトップクラスを維持し、強力な輸出能力を有しています。さらに、欧州の消費者は持続可能な包装や環境に配慮した生産方法をますます重視しており、サプライチェーンの決定やブランド戦略に影響を与えています。

北米は依然として重要な市場存在感を維持しており、機能性栄養、高タンパク製品、地域の移動中の消費習慣に対応した便利な包装形態に関するイノベーションで主導的立場にあります。米国とカナダは、先進的な小売・電子商取引インフラの恩恵を受け、迅速な製品投入と消費者教育活動が可能であり、プレミアムブランドのポジショニングを支えています。健康強調表示やプロバイオティクスの効能に関する規制面の支援が、機能性ヨーグルト製品の開発を促進しています。外食産業チャネルとの確立された関係が、特にレストランやコンビニエンスストアにおける需要をさらに牽引しています。この地域におけるタンパク質とフィットネス文化への注目は、栄養価の高さで知られるギリシャヨーグルトやアイスランドヨーグルトの人気を強く後押ししています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 消費者の腸内環境・プロバイオティクス・免疫機能への関心の高まり

- 栄養素を添加した機能性・強化ヨーグルトの開発

- カフェ、クイックサービスレストラン(QSR)、コンビニエンスストアでの利用拡大

- 電子商取引の拡大

- 高度な発酵技術と常温保存可能な包装技術の革新

- 高タンパクのギリシャ風・アイスランド風製品ラインが使用機会を拡大

- 市場抑制要因

- 牛乳価格の変動と供給の不安定さ、

- 地域の食品安全、表示、健康強調表示に関する規制への遵守

- 原材料およびエネルギー価格の上昇が生産コストを押し上げております

- アーモンドミルクやオートミルクなどの非乳製品代替品との競合

- 規制の見通し

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- タイプ

- 飲むヨーグルト

- スプーナブルヨーグルト

- 原料

- 乳製品ベース

- 非乳製品ベース

- フレーバー

- フレーバー付き

- フレーバーなし

- 流通チャネル

- オントレード

- オフトレード

- コンビニエンスストア

- 専門小売店

- スーパーマーケットおよびハイパーマーケット

- オンライン小売

- その他(倉庫型会員制店、ガソリンスタンドなど)

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- インドネシア

- タイ

- マレーシア

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- チリ

- ペルー

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- モロッコ

- ナイジェリア

- エジプト

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場ランキング分析

- 企業プロファイル

- China Mengniu Dairy Co Ltd

- Inner Mongolia Yili Industrial Group Co Ltd

- Nestle SA

- Yakult Honsha Co Ltd

- General Mills Inc.(Yoplait)

- Chobani Global Holdings LLC

- Lactalis Group

- Fonterra Co-operative Group Ltd

- Arla Foods am-ba

- Saputo Inc.

- Gujarat Co-operative Milk Marketing Federation(Amul)

- Meiji Holdings Co Ltd

- Bright Dairy & Food Co Ltd

- Grupo Lala S.A.B. de C.V.

- Ultima Foods Inc.

- Valio Oy

- Lifeway Foods Inc.

- Morinaga Milk Industry Co Ltd

- The Hain Celestial Group Inc.

- Yoso Brands

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 365 Pages

- 納期

- 2~3営業日