|

市場調査レポート

商品コード

1693961

米国の産業用センサ:市場シェア分析、産業動向、成長予測(2025~2030年)United States (US) Industrial Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の産業用センサ:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 192 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

米国の産業用センサ市場規模は、2025年に176億6,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは6.93%で、2030年には246億9,000万米ドルに達すると予測されています。

産業用センサは、ファクトリーオートメーションとインダストリー4.0に不可欠な要素です。モーション、環境、振動センサなどのセンサは、直線や角度の位置決め、傾き検知、水平、衝撃、落下検知など、機器の健全性をモニタリングするために使用されます。米国産業は、経済的にも人口統計学的にも事業を強化する立場にあり、国内の利益と輸出の可能性の両方に貢献しています。

主要ハイライト

- 産業用センサシステムの電源はDC24Vであることが多く、3Vや5Vで駆動する民生用システムのセンサとは大きく異なります。その結果、産業用センサシステムは、センサを効果的に駆動するために追加の電源管理を必要とします。これらのシステムでは、IO-Linkのようなデジタル出力をマイクロコントローラや無線トランシーバに直接使用します。

- 米国でIoTの採用が増加しているのは、急速なデジタル化、技術の進歩、政府の取り組み、施策、デジタル変革やインダストリー4.0の促進を目的とした投資などの要因によるものと考えられます。インダストリー4.0とIoTの受け入れにより、製造業における大規模なシフトは、自動化で人間労働を補完・拡大し、プロセスの失敗による産業事故を減らす技術で生産を前進させるために、俊敏でよりスマートで革新的な方法を採用することを企業に要求しています。コネクテッドデバイスやセンサの高い普及率とM2M通信の実現により、製造業で生成されるデータポイントが増加しています。

- 世界の自動車セクタは過去2年間に不況に見舞われたが、その動向は米国にも反映されました。同部門ではセンサとセンサ部品の数が増加しました。MEMS圧力センサは、ここ数年、スマート自動車セグメントで大きな採用実績を上げています。このため、Asystomは自律性の向上を特徴とするマルチセンサIIoTデバイスの製品群を発売しました。

- マルチセンサ機能は、幅広い産業機器の予知保全ニーズに対応し、その場で分析を行う新しいオンボード、コネクテッド、省エネエレクトロニクスを統合しています。性能の向上だけでなく、これらの革新的な製品は環境に優しく、100%アップグレードが可能です。

- センサの統合は産業オートメーションレベルを向上させるが、追加コストが発生するため、コスト重視の用途での使用は制限されます。さらに、新製品を製造するための研究開発活動に伴う高い開発コストは、主に資金不足の中小センサメーカーにとって重大な課題となっています。ここ数年、コスト格差は縮小傾向にあるが、それでもまだコストは高いです。しかし、いくつかの産業環境では生産性が極めて重要であるため、これらのセンサは地域全体の複数の組織で広く採用されています。しかし、初期投資の高さは依然として市場成長の大きな課題となっています。

米国産業用センサ市場動向

センシングコンポーネント需要につながるIoTの採用拡大が市場を牽引

- モノのインターネット(IoT)はインダストリー4.0の重要な要素です。製造業やサービス業における生産システムのモニタリングに幅広く応用されています。この技術は、より高いパフォーマンスを促進することで、製造業に新たな革新的可能性をもたらします。モノのインターネットの導入と利用は、産業の運営、通信、データ活用の方法を一変させ、その成長はとどまるところを知らないです。

- 産業用モノのインターネットによって、産業はビジネスモデルを再考し、IIoTデバイスから実用的な情報や知識を生み出すことができるようになりました。データ共有のエコシステムは、新たな収益源とパートナーシップを構築し始めました。

- 一方、センサから集約されたリアルタイムのデータは、IIoTが「意思決定」デバイスの原動力となることで、これらの内蔵機能により特定の行動をとることができるロボットの開発につながりました。これは倉庫において、Internet of Robotic Things(IoRT)として起こりました。デジタルトランスフォーメーションの本質的な側面として、IoT技術は製造業でますます重要になっています。

- センサの安定した信頼性の高い性能は、重工業業務の資産を日々の重要な指標を推進することにつながっています。製造業者は、生産ラインに沿った資産の稼働時間を常にモニタリングしています。IIoTは、さまざまな使用事例、役割、用途に対応するIIoTプラットフォームと産業用接続性を介して、これらの複雑な産業で一般的なレガシー機械を統合します。

- IIoTは、スマートセンサを使用して、産業プロセスや機器をモニタリングし、改善します。これらのセンサは、機械、コンポーネント、技術に関するデータをリアルタイムで取得・分析し、そのデータを保存、さらなる分析、または技術者やオペレーターに異常が発生していることを通知するために送信します。Global System for Mobile Communications Associationによると、2025年までに北米の消費者向けと産業向けのモノのインターネット(IoT)接続総数は54億に増加すると予測されています。

- さらに、さまざまなメーカーがIoT機器にセンサを配備し、性能を高めています。例えば、2023年5月、モノのインターネット(IoT)ソリューションのプロバイダである米国のiMatrix Systemsは、食品・農産物の保管、輸送モニタリング、製薬、農業の用途向けに設計された一連の温度・湿度センサを発売しました。NEOシリーズのセンサは、温度と湿度の変化を迅速かつ正確に測定できるため、冷蔵倉庫や冷蔵輸送のような動的な冷蔵環境での使用に最適です。

大きな市場シェアを占める圧力センサ

- 圧力センサは、多くのプロセス用途や油圧・空圧機器において、相対的なシステム圧力をモニタリングするために利用されています。これらのセンサは、航空宇宙、自動車、医療、消費財など、さまざまな産業で用途が拡大しているため、長年にわたって大きな成長を遂げています。実験室での用途からプラントや機械工学に至るまで、圧力・レベル測定装置は、測定技術の進化により、その用途セグメントと同様に多様なものとなっています。

- ここ数年、クロスカントリーカーやオフロードカーに革新的なタイヤ空気圧制御システムが搭載されるようになりました。例えば、メルセデスのG63 AMG 6X6では、ドライバーはフロントとリアアクスルのタイヤ空気圧を別々にチェックし、変化させることができます。報告によると、このシステムはタイヤ空気圧を0.5バールから1.8バールまで上げるのに20秒もかからないです。このような用途は、タイヤ空気圧モニタリングシステム(TMPS)の需要増加と相まって、予測期間中、タイヤ空気圧用途の圧力センサの必要性を支配すると予想されます。

- 圧抵抗センサと静電容量式センサは、自動車、医療、石油化学、石油・ガス産業での使用が増加しているため、圧力センサ市場を独占しています。光学式センサと共振式ソリッドステートセンサは、危険な環境での用途のため、予測期間中に成長が拡大すると予測されています。

- 例えば、2023年9月、エネルギー技術企業であるBaker Hughesは、水素ドラック水素定格圧力センサの最新製品の発売を発表しました。長期安定性を提供し、過酷な環境に耐えるように設計された水素圧力センサは、ガスタービン、水素製造電解、水素充填ステーションなど、さまざまな用途で使用できます。

- 医療産業も、高齢者の増加、医療支出の増加、人口の慢性疾患の増加により、大きな成長機会を見出しています。米国は、世界のどの国よりも一人当たりの医療支出額が多いです。米国には医療制度の財源を賄う明確な方法があり、費用の大半は民間保険で賄われています。2023会計年度には、民間保険が医療費全体の約3分の1をカバーします。

米国産業用センサ市場概要

米国の産業用センサ市場は非常にセグメント化されており、TE Connectivity Ltd.、Omega Engineering Inc.、Honeywell International Inc.、Rockwell Automation Inc.、Siemens AGなどの大手企業が存在します。市場参入企業は、製品ラインナップを強化し、サステイナブル競争優位性を獲得するため、提携や買収などの戦略を採用しています。

- 2023年6月-STMicroelectronicsは、産業市場向けに10年の長寿命プログラムを宣言した初のMEMS防水/防液絶対圧センサを発表しました。最新の防水圧力センサは、顧客のMEMS設計を保護するために必要な長期的可用性を備え、デジタル変革に必要な環境堅牢性を記載しています。

- 2023年1月-Quadricとamsオスラムは、最先端の可視光・赤外光用CMOSセンサMiraファミリーとQuadricの先進的なChimera GPNPUプロセッサを組み合わせた統合センシングモジュールを開発するため、協業パートナーシップを締結。統合された超低消費電力モジュールにより、ウェアラブル技術で新しいタイプのスマートセンシングを使用できるようになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 産業バリューチェーン分析

第5章 市場力学

- 市場の促進要因

- センシングコンポーネントの需要につながるIoTの採用拡大

- 予知保全と遠隔モニタリングの重視の高まり

- 市場課題/抑制要因

- 高コストと運用上の懸念

第6章 市場セグメンテーション

- 接続性別

- 有線ソリューション

- 無線ソリューション

- タイプ別

- フローセンサ

- 市場概要

- エンドユーザー産業

- 温度センサ

- 市場概要

- エンドユーザー産業

- レベルセンサ

- 市場概要

- エンドユーザー産業

- 圧力センサ

- 市場概要

- エンドユーザー産業

- ガスセンサ

- 市場概要

- エンドユーザー産業

- その他のセンサ

- フローセンサ

第7章 競合情勢

- 企業プロファイル

- Texas Instruments Incorporated

- TE Connectivity Ltd

- Omega Engineering Inc.

- Honeywell International Inc.

- Rockwell Automation Inc.

- Siemens AG

- Stmicroelectronics Inc.

- Ams-osram AG

- NXP Semiconductors N.V.

- Bosch Sensortec GMBH(Bosch Internationals)

- Sick AG

- ABB Ltd

- Omron Corporation

- Emerson Electric Co.

- Endress+Hauser AG

- The Krohne Group

- Yokogawa Electric Corporation

- Meggitt Sensing Systems

- Vega Grieshaber KG

- Analog Devices, Inc.

- Sensata Technologies Inc.

- Infineon Technologies AG

第8章 市場展望

- 現在の地政学的シナリオが市場に与える影響

- 予想される景気減速/後退の影響

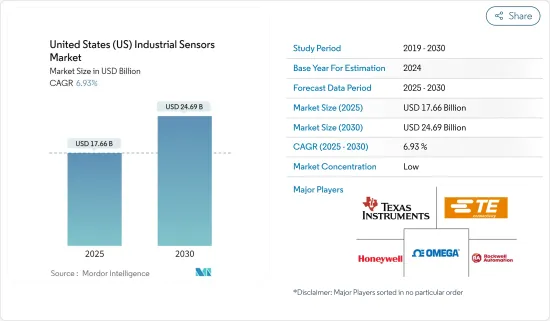

The United States Industrial Sensors Market size is estimated at USD 17.66 billion in 2025, and is expected to reach USD 24.69 billion by 2030, at a CAGR of 6.93% during the forecast period (2025-2030).

Industrial sensors are a crucial part of factory automation and Industry 4.0. Sensors such as motion, environmental, and vibration sensors are used to monitor equipment health, from linear or angular positioning, tilt sensing, leveling, shock, or fall detection. United States industries are positioned to augment their operations economically and demographically, serving both domestic interests and export possibilities, which will rise soon.

Key Highlights

- An industrial sensor system is often powered by a 24V DC source, which is very different from a sensor in a consumer system that is powered by a 3V or 5V source. As a result, industrial sensor systems require additional power management to drive the sensors effectively. These use digital outputs such as IO-Link directly to a microcontroller or the wireless transceiver.

- The increasing adoption of IoT in the United States can be attributed to factors like rapid digitalization, technological advancements, government initiatives, policies, and investments aimed at promoting digital transformation and Industry 4.0. Due to Industry 4.0 and the acceptance of IoT, massive shifts in manufacturing require enterprises to adopt agile, smarter, and innovative ways to advance production with technologies that complement and augment human labor with automation and reduce industrial accidents caused by process failure. With the high adoption rate of connected devices and sensors and the enabling of M2M communication, there has been an increase in the data points generated in the manufacturing industry.

- Although the global automotive sector witnessed a recession in the past two years, the trend was also reflected in the United States. The number of sensors and sensor components increased in the sector. MEMS pressure sensors have witnessed significant adoption in the smart automotive sector in the last few years. For the same, Asystom launched a range of multi-sensor IIoT devices featuring increased autonomy.

- The multi-sensor capability has addressed the predictive maintenance needs of a wide array of industrial equipment, integrating new on-board, connected, energy-saving electronics performing in situ analysis. Apart from increased performance, these innovative products are eco-responsible and 100% upgradeable.

- Although the integration of sensors increases the industrial automation level, it incurs an additional cost, which limits the use in cost-sensitive applications. Additionally, high development costs involved in the research and development activities to manufacture new products act as a critical challenge, mainly for the cash-deficient small and medium-sized sensor manufacturers. While the cost disparity has been declining in the past few years, they still cost more. However, as productivity is crucial in several industrial settings, these sensors have been widely adopted by multiple organizations across the region. However, higher initial investment still poses a significant challenge to the market's growth.

United States (US) Industrial Sensors Market Trends

Growing Adoption of IoT Leading to Demand for Sensing Components Drives the Market

- The Internet of Things (IoT) is a critical component of Industry 4.0. It has extensive applications in the monitoring of production systems in manufacturing and services. This technology opens up new and innovative possibilities in manufacturing by facilitating higher performance. The implementation and use of the Internet of Things transformed how industries operate, communicate, and utilize data, and it is only continuing to grow.

- The Industrial Internet of Things enabled industries to rethink business models, generating actionable information and knowledge from IIoT devices. A data-sharing ecosystem started to build new revenue streams and partnerships.

- On the other hand, aggregated and real-time data from sensors led to the development of robots that can take specific actions because of these built-in capabilities, whereby IIoT becomes a driver of 'decision-making' devices. This happened in warehouses as the Internet of Robotic Things (IoRT). As an essential aspect of digital transformation, IoT technology is becoming increasingly important in the manufacturing industry.

- The consistent and reliable performance of sensors has led the assets in heavy industrial operations to drive critical daily metrics. Manufacturers are constantly monitoring the uptime of assets along their production lines. IIoT integrates legacy machinery commonplace within these complex industries via industrial connectivity with IIoT platforms for different use cases, roles, and applications.

- IIoT uses smart sensors to monitor and improve industrial processes and equipment. These sensors capture and analyze data about machines, components, and techniques in real time and then transmit that data for storage, further analysis, or to notify a technician or operator that something is going wrong. According to the Global System for Mobile Communications Association, by 2025, North America's total number of consumer and industrial Internet of Things (IoT) connections is forecast to grow to 5.4 billion.

- Moreover, various manufacturers are deploying sensors in IoT devices to boost their performance. For instance, in May 2023, iMatrix Systems, a US-based provider of Internet of Things (IoT) solutions, launched a range of temperature and humidity sensors designed for use in food and produce storage, transport monitoring, pharmaceutical, and agriculture applications. The NEO series sensors can quickly and accurately measure changes in temperature and humidity, making them ideal for use in dynamic refrigeration environments like cold storage and refrigerated transportation.

Pressure Sensors to Hold Significant Market Share

- Pressure sensors are utilized to monitor relative system pressure in many process applications, as well as hydraulics and pneumatics. These sensors have witnessed significant growth over the years owing to the increasing applications across various industries, such as aerospace, automotive, healthcare, consumer goods, etc. Ranging from laboratory applications to plant and mechanical engineering, pressure and level measuring devices have become as diverse as their areas of application, thanks to the evolution of measurement technologies.

- In the past few years, exclusive cross-country and off-road cars have been installed with an innovative tire pressure control system. For instance, the G63 AMG 6X6 from the Mercedes enables the driver to check and vary the tire pressure of both the front and rear axles separately. Reportedly, the system takes less than 20 seconds to raise the tire pressure from 0.5 bar to 1.8 bar. Such applications, coupled with increasing demand for Tire Pressure Monitoring Systems (TMPS), are expected to govern the need for pressure sensors in tire pressure applications over the forecast period.

- Piezoresistive and capacitive sensors dominate the pressure sensors market as they are increasingly used in the automotive, medical, petrochemical, oil, and gas industries. Optical and resonant solid-state sensors are anticipated to exhibit increased growth over the forecast period due to their applications in hazardous environments.

- For instance, in September 2023, Baker Hughes, an energy technology company, announced the launch of its latest product for hydrogen-druck hydrogen-rated pressure sensors. Designed to offer longer-term stability and withstand harsh environments, the hydrogen pressure sensors can be used in various applications, including gas turbines, hydrogen production electrolysis, and hydrogen filling stations.

- The medical industry is also observing significant growth opportunities owing to rising geriatric populations, increasing healthcare expenditures, and growing chronic diseases among the considerable population. The USA spends more money on healthcare per person than any other country in the world. Nevertheless, the United States has a distinct method of funding their healthcare system, with most of the costs being covered by private insurance. In the fiscal year 2023, private insurance covers approximately one third of total health spending.

United States (US) Industrial Sensors Market Overview

The United States Industrial Sensors Market is highly fragmented, with the presence of major players like TE Connectivity Ltd, Omega Engineering Inc., Honeywell International Inc., Rockwell Automation Inc., and Siemens AG. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- June 2023 - STMicroelectronics introduced the first MEMS water/liquid-proof absolute pressure sensor with a declared 10-year longevity program for the industrial market. The latest waterproof pressure sensors provide the environmental robustness needed to power digital transformation with the long-term availability necessary to protect customers' MEMS designs.

- January 2023 - Quadric and ams OSRAM established a collaborative partnership to create integrated sensing modules that combine the cutting-edge Mira Family of CMOS sensors for visible and infrared light with Quadric's advanced Chimera GPNPU processors. The integrated ultra-low power modules will allow wearable technology to use new types of smart sensing.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of IoT Leading to Demand for Sensing Components

- 5.1.2 Growing Emphasis on the Use of Predictive Maintenance and Remote Monitoring

- 5.2 Market Challenges/Restraints

- 5.2.1 High Cost and Operational Concern

6 MARKET SEGMENTATION

- 6.1 By Connectivity

- 6.1.1 Wired Solutions

- 6.1.2 Wireless Solutions

- 6.2 By Type

- 6.2.1 Flow Sensors

- 6.2.1.1 Market Overview

- 6.2.1.2 End-user Industry

- 6.2.2 Temperature Sensors

- 6.2.2.1 Market Overview

- 6.2.2.2 End-user Industry

- 6.2.3 Level Sensors

- 6.2.3.1 Market Overview

- 6.2.3.2 End-user Industry

- 6.2.4 Pressure Sensors

- 6.2.4.1 Market Overview

- 6.2.4.2 End-user Industry

- 6.2.5 Gas Sensors

- 6.2.5.1 Market Overview

- 6.2.5.2 End-user Industry

- 6.2.6 Other Sensors

- 6.2.1 Flow Sensors

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Texas Instruments Incorporated

- 7.1.2 TE Connectivity Ltd

- 7.1.3 Omega Engineering Inc.

- 7.1.4 Honeywell International Inc.

- 7.1.5 Rockwell Automation Inc.

- 7.1.6 Siemens AG

- 7.1.7 Stmicroelectronics Inc.

- 7.1.8 Ams-osram AG

- 7.1.9 NXP Semiconductors N.V.

- 7.1.10 Bosch Sensortec GMBH (Bosch Internationals)

- 7.1.11 Sick AG

- 7.1.12 ABB Ltd

- 7.1.13 Omron Corporation

- 7.1.14 Emerson Electric Co.

- 7.1.15 Endress + Hauser AG

- 7.1.16 The Krohne Group

- 7.1.17 Yokogawa Electric Corporation

- 7.1.18 Meggitt Sensing Systems

- 7.1.19 Vega Grieshaber KG

- 7.1.20 Analog Devices, Inc.

- 7.1.21 Sensata Technologies Inc.

- 7.1.22 Infineon Technologies AG

8 MARKET OUTLOOK

- 8.1 Impact of Current Geopolitical Scenarios on the Market

- 8.2 Impact of Anticipated Economic Slowdown/Recession