|

|

市場調査レポート

商品コード

1458434

宇宙用推進剤タンクの世界市場:プラットフォーム別、エンドユーザー別、材質別、製造プロセス別、推進剤タンク別、国別 - 分析と予測 (2023-2033年)Global Space-Qualified Propellant Tank Market: Focus on Platform, End User, Material, Manufacturing Process, Propellant Tank and Country - Analysis and Forecast, 2023-2033 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 宇宙用推進剤タンクの世界市場:プラットフォーム別、エンドユーザー別、材質別、製造プロセス別、推進剤タンク別、国別 - 分析と予測 (2023-2033年) |

|

出版日: 2024年04月02日

発行: BIS Research

ページ情報: 英文

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

宇宙用推進剤タンクは、宇宙ミッションの厳しい要件を満たすように設計された、航空宇宙工学の分野で重要なコンポーネントです。

これらのタンクは、宇宙船の推進に必要な推進剤を貯蔵し、軌道調整、軌道離脱、深宇宙探査などの操作を可能にします。宇宙仕様の推進剤タンクの設計と製造には、宇宙の過酷な環境における信頼性、安全性、効率を確保するための高度な材料と技術が必要です。

長年にわたる材料科学と工学の進歩により、極端な温度や圧力、さまざまな推進剤の腐食性に耐えるタンクが開発されてきました。Benchmark Space Systemsなどのメーカーやukasiewicz Institute of Aviationなどの機関は、宇宙ミッションが環境に与える影響の軽減を目指し、高試験過酸化物 (HTP) やその他のグリーン推進剤を利用する推進システムの技術革新の最前線に立ってきました。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2023-2033年 |

| 2023年の評価額 | 17億5,450万米ドル |

| 2033年予測 | 34億3,180万米ドル |

| CAGR | 6.94% |

プラットフォーム別では、打上げロケット部門

宇宙用推進剤タンク市場では、いくつかの促進要因により打上げロケット部門が主導権を握っています。衛星打ち上げ数の増加と、通信、地球観測、ナビゲーション、追跡などさまざまな目的の衛星コンステレーションの開発が、この動向に大きく寄与しています。打ち上げロケットには、ロケットステージ用の燃料や酸化剤を貯蔵するための特殊な推進剤タンクが必要であり、これらの打ち上げロケットの性能を高めるために、軽量で効率的な推進剤タンクの需要が増加しています。

材料別では、炭素繊維複合材料の部門が市場を独占:

炭素繊維複合材料の部門が2022年に最大の市場普及率を示しています。炭素繊維複合材料部門の収益規模は、2022年の4億2,360万米ドルから、予測期間中は7.06%のCAGRで成長すると予測されています。

地域別では、北米が世界市場をリードしています。これには、堅調な航空宇宙産業などいくつかの主な理由があります。この地域は、宇宙探査と衛星技術に対する政府機関および商業機関からの大規模な投資から利益を得ています。NASAのArtemisなど、人類を月に、そして最終的には火星に帰還させることを目的としたプログラムは、この分野の資金調達と開発を推進する野心的な目標を裏付けています。このようなレベルの投資は、宇宙用推進剤タンクや関連技術の進歩を促進します。北米は、軽量で高性能な推進剤タンクの開発など、航空宇宙分野における技術革新の最前線にあります。電気推進、化学推進、ハイブリッド推進システムの進歩に重点を置くことで、この地域の主導的地位はさらに強固なものとなっています。ライナーレス複合極低温推進剤タンクの開発などの革新は、技術的進歩を例証するものです。

当レポートでは、世界の宇宙用推進剤タンクの市場を調査し、市場概要、主要動向、エコシステム、進行中のプログラム、法規制環境、市場影響因子および市場機会の分析、市場規模の推移・予測、各種区分・地域別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

目次

エグゼクティブサマリー

第1章 市場

- 動向:現在および将来の影響評価

- 持続可能性への注目の高まり

- 軌道上整備および燃料補給技術

- 規制状況 (国別)

- 米国

- 英国

- フランス

- ドイツ

- インド

- 中国

- ロシア

- エコシステム/進行中のプログラム

- 宇宙用燃料タンクの製造業者と規格

- 新たな宇宙ビジネスシナリオ:宇宙用推進剤タンク市場における新たな機会

- 小型衛星市場の成長

- 小型ロケット市場の成長

- スタートアップと投資情勢

- 市場力学の概要

- 市場促進要因

- 市場抑制要因

- 市場機会

- サプライチェーンの概要

第2章 用途

- 用途の分類

- 用途の概要

- 宇宙用推進剤タンクの世界市場

- 市場概要

- 世界の宇宙用推進剤タンク市場:プラットフォーム別

- 衛星

- 打上げロケット

- 世界の宇宙用推進剤タンク市場:エンドユーザー別

- 政府・軍

- 商用

第3章 製品

- 製品の分類

- 製品概要

- 宇宙用推進剤タンクの世界市場

- 市場概要

- 世界の宇宙用推進剤タンク市場:材質別

- 炭素繊維複合材料

- アルミニウムおよびチタン合金

- 熱硬化性および熱可塑性複合材料

- ナノマテリアル

- その他

- 世界の宇宙用推進剤タンク市場:製造プロセス別

- 自動ファイバー配置

- 圧縮成形

- 付加製造

- 従来型製造

- その他

- 世界の宇宙用推進剤タンク市場:推進剤タンク別

- ダイヤフラムタンク

- 推進剤管理デバイスタンク

- ヘリウム、窒素、キセノンタンク

- アルミニウム合金タンク

- ヒドラジンタンク

- 高濃度過酸化水素タンク

第4章 地域

- 地域概要

- 北米

- 欧州

- アジア太平洋

- その他の地域

第5章 市場:競合ベンチマーキング・企業プロファイル

- 次なるフロンティア

- 地理的評価

- Airbus S.A.S.

- AdamWorks LLC

- Ariane Group

- Busek Co. Inc.

- Infinite Composite Technologies

- IHI Aerospace Co., Ltd.

- Lockheed Martin Corporation

- Microcosm, Inc.

- Moog Inc.

- OHB SE

- Northrop Grumman Corporation

- Nammo AS

- Peak Technology

- Phase Four

- Stelia Aerospace North America Inc.

第6章 調査手法

List of Figures

- Figure 1: Global Space-Qualified Propellant Tank Market (by Region), $Million, 2022, 2023, and 2033

- Figure 2: Global Space-Qualified Propellant Tank Market (by Platform, $Million, 2022 and 2033

- Figure 3: Global Space-Qualified Propellant Tank Market (by End User), $Million, 2022 and 2033

- Figure 4: Global Space-Qualified Propellant Tank Market (by Material), $Million, 2022 and 2033

- Figure 5: Global Space-Qualified Propellant Tank Market (by Manufacturing Process), $Million, 2022 and 2033

- Figure 6: Global Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022 and 2033

- Figure 7: Space-Qualified Propellant Tank, Recent Developments

- Figure 8: Small Satellite Market Scenarios (101-2,200 Kg), 2022-2033

- Figure 9: Global Small Launch Vehicle Scenarios, 2022-2026

- Figure 10: Impact Analysis of Market Navigating Factors, 2022-2033

- Figure 11: Upcoming Deep Space Missions

- Figure 12: Supply Chain and Risks within the Supply Chain

- Figure 13: U.S. Space-Qualified Propellant Tank Market, $Million, 2022-2033

- Figure 14: Canada Space-Qualified Propellant Tank Market, $Million, 2022-2033

- Figure 15: France Space-Qualified Propellant Tank Market, $Million, 2022-2033

- Figure 16: Germany Space-Qualified Propellant Tank Market, $Million, 2022-2033

- Figure 17: U.K. Space-Qualified Propellant Tank Market, $Million, 2022-2033

- Figure 18: Russia Space-Qualified Propellant Tank Market, $Million, 2022-2033ple

- Figure 19: Rest-of-Europe Space-Qualified Propellant Tank Market, $Million, 2022-2033

- Figure 20: China Space-Qualified Propellant Tank Market, $Million, 2022-2033

- Figure 21: India Space-Qualified Propellant Tank Market, $Million, 2022-2033

- Figure 22: Japan Space-Qualified Propellant Tank Market, $Million, 2022-2033

- Figure 23: Rest-of-Asia-Pacific Space-Qualified Propellant Tank Market, $Million, 2022-2033

- Figure 24: Latin America Space-Qualified Propellant Tank Market, $Million, 2022-2033

- Figure 25: Middle East and Africa Space-Qualified Propellant Tank Market, $Million, 2022-2033

- Figure 26: Strategic Initiatives, 2020-2023

- Figure 27: Share of Strategic Initiatives, 2020-2023

- Figure 28: Data Triangulation

- Figure 29: Top-Down and Bottom-Up Approach

- Figure 30: Assumptions and Limitations

List of Tables

- Table 1: Market Snapshot

- Table 2: Global Space-Qualified Propellant Tank Market Opportunities across Regions

- Table 3: Other Sections Under the Regulations for Propulsion Systems

- Table 4: Chinese National Standard Code for Space Propulsions

- Table 5: List of Certification

- Table 6: Funding and Investment Scenario, January 2019-January 2024

- Table 7: Global Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 8: Global Space-Qualified Propellant Tank Market (by Platform), Units, 2022-2033

- Table 9: Global Space-Qualified Propellant Tank Market (by Satellite), $Million, 2022-2033

- Table 10: Global Space-Qualified Propellant Tank Market (by Satellite), Units, 2022-2033

- Table 11: Global Space-Qualified Propellant Tank Market (by Launch Vehicle), $Million, 2022-2033

- Table 12: Global Space-Qualified Propellant Tank Market (by Launch Vehicle), Units, 2022-2033

- Table 13: Global Space-Qualified Propellant Tank Market (by End User), $Million, 2022-2033

- Table 14: Global Space-Qualified Propellant Tank Market (by Material), $Million, 2022-2033

- Table 15: Global Space-Qualified Propellant Tank Market (by Manufacturing Process), $Million, 2022-2033

- Table 16: Global Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 17: Global Space-Qualified Propellant Tank Market (by Region), $Million, 2022-2033

- Table 18: North America Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 19: North America Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 20: U.S. Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 21: U.S. Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 22: Canada Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 23: Canada Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 24: Europe Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 25: Europe Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 26: France Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 27: France Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 28: Germany Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 29: Germany Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 30: U.K. Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 31: U.K. Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 32: Russia Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 33: Russia Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 34: Rest-of-Europe Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 35: Rest-of-Europe Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 36: Asia-Pacific Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 37: Asia-Pacific Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 38: China Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 39: China Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 40: India Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 41: India Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 42: Japan Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 43: Japan Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 44: Rest-of-Asia-Pacific Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 45: Rest-of-Asia-Pacific Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 46: Rest-of-the-World Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 47: Rest-of-the-World Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 48: Latin America Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 49: Latin America Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 50: Middle East and Africa Space-Qualified Propellant Tank Market (by Platform), $Million, 2022-2033

- Table 51: Middle East and Africa Space-Qualified Propellant Tank Market (by Propellant Tank), $Million, 2022-2033

- Table 52: Market Share

Introduction of Space-Qualified Propellant Tank

Space-qualified propellant tanks are critical components in the field of aerospace engineering, designed to meet the stringent requirements of space missions. These tanks store the propellant necessary for spacecraft propulsion, enabling maneuvers such as orbit adjustment, deorbiting, and deep space exploration. The design and manufacturing of space-qualified propellant tanks involve advanced materials and technologies to ensure reliability, safety, and efficiency in the harsh environment of space.

Over the years, advancements in materials science and engineering have led to the development of tanks that can withstand extreme temperatures, pressures, and the corrosive nature of various propellants. Manufacturers such as Benchmark Space Systems and institutions such as the ?ukasiewicz Institute of Aviation have been at the forefront of innovating propulsion systems that utilize high-test peroxide (HTP) and other green propellants, aiming to reduce the environmental impact of space missions.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2023 - 2033 |

| 2023 Evaluation | $1,754.5 Million |

| 2033 Forecast | $3,431.8 Million |

| CAGR | 6.94% |

Moreover, the successful deployment of these tanks in space missions underscores the importance of reliable propellant storage solutions in the expanding landscape of satellite technology and interplanetary exploration. The design considerations for these tanks, including material selection and structural integrity, play a pivotal role in the mission's success, highlighting the critical balance between performance, cost, and manufacturability (DocsLib). As the space industry continues to evolve, with an increasing focus on sustainability and efficiency, space-qualified propellant tanks will remain indispensable in powering the next generation of spacecraft, further enabling humanity's exploration and utilization of outer space.

Market Introduction

The space-qualified propellant tank market is a highly specialized sector within the aerospace industry, focusing on the production and supply of propellant storage solutions for spacecraft and satellite operations. This market caters to a wide range of applications, from commercial satellite constellations and government space missions to deep space exploration ventures. It is driven by the critical need for reliable, efficient, and safe storage of propellants that power the thrusters and engines essential for maneuvering and operating spacecraft in the vacuum of space.

As the global space economy continues to expand, with increasing numbers of large satellite launches and ambitious exploration missions to the Moon, Mars, and beyond, the demand for space-qualified propellant tanks is experiencing significant growth. This growth is further amplified by the emergence of new space-faring nations and private space companies, each contributing to a more crowded and competitive arena both in Low Earth Orbit (LEO) and in deeper space.

The market encompasses a variety of propellant tank types designed to store both traditional and green propellants. Traditional propellants include hydrazine and nitrogen tetroxide, while green propellants such as Hydroxylammonium Nitrate Fuel Blend (AF-M315E) and LMP-103S offer the promise of reduced environmental impact and enhanced safety for ground operations. The choice of propellant influences the design, material selection, and manufacturing processes of the tanks, with each option presenting its own set of challenges and benefits. Innovation and technological advancements play a crucial role in this market. Manufacturers are constantly seeking new materials and design approaches to create tanks that are lighter, more durable, and capable of withstanding the extreme conditions of space. These innovations not only improve the performance and reliability of space missions but also contribute to reducing the overall cost of access to space.

Furthermore, the push toward in-space manufacturing and refueling stations, along with the development of reusable spacecraft, is creating new opportunities and challenges for the space-qualified propellant tank market. The ability to refuel spacecraft in orbit or on other celestial bodies could dramatically change the logistics and economics of space exploration, requiring tanks that are not only reliable over longer missions but also compatible with in-space propellant transfer technologies.

Industrial Impact

The industrial impact of the space-qualified propellant tank market is profound and multifaceted, resonating across the aerospace industry and its ancillary sectors. As the backbone of spacecraft propulsion systems, these tanks are pivotal in enhancing the reliability, efficiency, and safety of space missions. The market's evolution is spurring innovation in materials science and propulsion technologies, pushing manufacturers to develop lighter, more durable tanks capable of withstanding the rigors of space. This, in turn, demands a skilled workforce and fosters job creation in high-tech engineering and manufacturing domains. Moreover, the drive toward greener propellants and the need for space sustainability are shaping environmental standards and practices within the industry. As commercial space activities burgeon, the demand for space-qualified propellant tanks is set to rise, highlighting the market's crucial role in the broader space economy and its contribution to technological advancement, economic growth, and environmental stewardship in the era of space exploration.

Market Segmentation:

Segmentation 1: by Platform

- Satellite

- 0-500 kg

- 501-1,000 kg

- 1,001 kg and Above

- Launch Vehicle

- Small Lift Launch Vehicle (0-2,200 kg)

- Medium and Heavy Lift Launch Vehicle (2,201 kg and Above)

Launch Vehicle Segment to Dominate the Global Space-Qualified Propellant Tank Market (by Platform)

The launch vehicle segment in the space-qualified propellant tank market is leading due to several driving factors. The increasing number of satellite launches and the development of satellite constellations for various purposes, including communication, Earth observation, navigation, and tracking, are major contributors to this trend. Launch vehicles require specialized propellant tanks to store fuel or oxidizer for rocket stages, and the demand for lightweight, efficient propellant tanks is on the rise to enhance the performance of these vehicles.

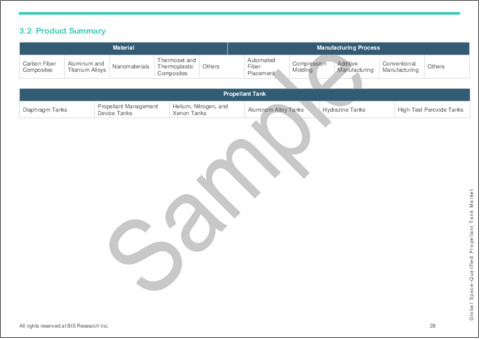

Segmentation 2: by Material

- Carbon Fiber Composites

- Aluminum and Titanium Alloys

- Nanomaterials

- Thermoset and Thermoplastic Composites

- Others

Carbon Fiber Composites Segment to Dominate the Global Space-Qualified Propellant Tank Market (by Material)

The carbon fiber composites segment had the highest market penetration in 2022. The carbon fiber composites reported revenue of $423.6 million in 2022 and is expected to grow at a CAGR of 7.06% during the forecast period 2023-2033.

Segmentation 3: by End User

- Government and Military

- Commercial

Segmentation 4: by Manufacturing Process

- Automated Fiber Placement

- Compression Molding

- Additive Manufacturing

- Conventional Manufacturing

- Others

Segmentation 5: by Propellant Tank

- Diaphragm Tanks

- Propellant Management Devices

- Helium, Nitrogen and Xenon Tanks

- Aluminum Alloy Tanks

- Hydrazine Tanks

- HTP Tanks

Segmentation 6: by Region

- North America - U.S. and Canada

- Europe - U.K., Germany, France, Russia, and Rest-of-the-Europe

- Asia-Pacific - China, India, Japan, and Rest-of-Asia-Pacific

- Rest-of-the-World - Latin America and Middle East and Africa

North America leads the global space-qualified propellant tank market for several key reasons, including its robust aerospace industry. The region benefits from substantial investments by both government and commercial organizations in space exploration and satellite technologies. Programs such as NASA's Artemis, aimed at returning humans to the Moon and eventually Mars, underscore the ambitious goals that drive funding and development in the sector. This level of investment facilitates advancements in space-qualified propellant tanks and related technologies. North America is at the forefront of technological innovation in aerospace, including the development of lightweight and high-performance propellant tanks. The focus on advancing electric, chemical, and hybrid propulsion systems further solidifies the region's leadership position. Innovations, such as the development of linerless composite cryogenic propellant tanks, exemplify the technological strides being made.

Recent Developments in the Global Space-Qualified Propellant Tank Market

- In March 2023, China achieved a significant milestone in its pursuit of developing a super heavy-lift launch vehicle by successfully producing a 33-foot-wide (10-meter) class propellant tank. This remarkable accomplishment was announced by the China Academy of Launch Vehicle Technology (CALT). The manufacturing of this sizable tank showcases technological breakthroughs, enabling the creation of a propellant storage tank that is both robust and lightweight, crucial for rocket launches.

- In July 2022, Lockheed Martin, in partnership with Australian company Omni Tanker and the University of New South Wales (UNSW) Sydney, embarked on a groundbreaking project to create and bring to market advanced composite tank technologies. This initiative, supported by a grant from the Australian Government's Advanced Manufacturing Growth Centre (AMGC), focuses on the development of innovative solutions for the storage and transport of liquid hydrogen. The project, valued at $0.91 million, aimed to overcome the challenges associated with using composite materials for cryogenic liquid fuel storage, catering to various applications, including terrestrial, aerial, underwater, and space environments.

- In August 2021, Firefly Aerospace Inc. announced a new business line for supplying rocket engines and spaceflight components, including carbon fiber-reinforced composite structures.

How can this report add value to an organization?

Product/Innovation Strategy: The product segment helps the reader understand the different types of products available for deployment globally. Moreover, the study provides the reader with a detailed understanding of the global space-qualified propellant tank market based on platform (satellite and launch vehicle) and end user (government and military and commercial). The global space-qualified propellant tank market is segmented into the material (carbon fiber composite, aluminum and titanium alloys, nanomaterials, thermoset and thermoplastic composites, and others), manufacturing process (automated fiber placement, compression molding, additive manufacturing, conventional manufacturing, and others) and propellant tank (diaphragm tanks, propellant management devices, helium, nitrogen, and xenon tanks, aluminum alloy tanks, hydrazine tanks, and high-test peroxide tanks).

Growth/Marketing Strategy: The global space-qualified propellant tank market has seen major development by key players operating in the market, such as business expansion, partnership, collaboration, and joint venture. The company's favored strategy has been partnerships and contracts to strengthen its position in the global space-qualified propellant tank market. For instance, Airbus selected MT Aerospace AG to provide tanks for the spacecraft's chemical propulsion system. The contract, worth $3.06 million, was signed in May 2021. These tanks, part of the E3000 tank series initially designed for telecommunications satellites, are utilized to minimize development complexity and effort. Each tank has a capacity of 225 liters and is designed to release the required propellant and oxidizer in zero gravity using capillary action via a complex assembly known as the propellant management device.

Methodology: The research methodology design adopted for this specific study includes a mix of data collected from primary and secondary data sources. Both primary resources (key players, market leaders, and in-house experts) and secondary research (a host of paid and unpaid databases), along with analytical tools, are employed to build the predictive and forecast models.

Data and validation have been taken into consideration from both primary sources as well as secondary sources.

Key Considerations and Assumptions in Market Engineering and Validation

Detailed secondary research has been done to ensure maximum coverage of manufacturers/suppliers operational in a country.

Based on the classification, the average selling price (ASP) has been calculated using the weighted average method.

The currency conversion rate has been taken from the historical exchange rate of Oanda and/or other relevant websites.

Any economic downturn in the future has not been taken into consideration for the market estimation and forecast.

The base currency considered for the market analysis is US$. Currencies other than the US$ have been converted to the US$ for all statistical calculations, considering the average conversion rate for that particular year.

The term "product" in this document may refer to "propellant tank" as and where relevant.

The term "manufacturers/suppliers" may refer to "systems providers" or "technology providers" as and where relevant.

Primary Research

The primary sources involve industry experts from the aerospace and defense industry, including propellant tank manufacturers and component manufacturers. Respondents such as CEOs, vice presidents, marketing directors, and technology and innovation directors have been interviewed to obtain and verify both qualitative and quantitative aspects of this research study.

Secondary Research

This study involves the usage of extensive secondary research, company websites, directories, and annual reports. It also makes use of databases, such as Spacenews, Businessweek, and others, to collect effective and useful information for a market-oriented, technical, commercial, and extensive study of the global market. In addition to the data sources, the study has been undertaken with the help of other data sources and websites, such as www.nasa.gov.

Secondary research was done to obtain critical information about the industry's value chain, the market's monetary chain, revenue models, the total pool of key players, and the current and potential use cases and applications.

Key Market Players and Competition Synopsis

The companies that are profiled have been selected based on thorough secondary research, which includes analyzing company coverage, product portfolio, market penetration, and insights gathered from primary experts.

The global space-qualified propellant tank market comprises key players who have established themselves thoroughly and have the proper understanding of the market, accompanied by start-ups who are looking forward to establishing themselves in this highly competitive market. In 2022, the global space-qualified propellant tank market was dominated by established players, accounting for 71% of the market share, whereas start-ups managed to capture 29% of the market.

Some prominent names established in this market are:

- Airbus S.A.S.

- Adam Works.

- Ariane Group

- Busek Co. Inc.

- Infinite Composite Technologies

- IHI Aerospace Co.

- Lockheed Martin Corporation

- Microcosm, Inc.

- Moog Inc.

- OHB SE

- Northrop Grumman Corporation

- Nammo AS

- Peak Technology

- Phase Four

- Stelia Aerospace North America Inc.

Table of Contents

Executive Summary

Scope and Definition

1 Markets

- 1.1 Trends: Current and Future Impact Assessment

- 1.1.1 Increasing Focus on Sustainability

- 1.1.2 On-Orbit Servicing and Refueling Technologies

- 1.2 Regulatory Landscape (by Country)

- 1.2.1 U.S.

- 1.2.2 U.K.

- 1.2.3 France

- 1.2.4 Germany

- 1.2.5 India

- 1.2.6 China

- 1.2.7 Russia

- 1.3 Ecosystem/Ongoing Programs

- 1.3.1 The ASTRIS Mission

- 1.3.2 SpaceTank Project

- 1.4 Space-Qualified Propellant Tank Manufacturers and Standards

- 1.5 New Space Business Scenario: An Emerging Opportunity for the Space-Qualified Propellant Tank Market

- 1.5.1 Growth in Small Satellite Market

- 1.5.2 Growth in Small Launch Vehicle Market

- 1.6 Start-Ups and Investment Landscape

- 1.7 Market Dynamics Overview

- 1.7.1 Market Drivers

- 1.7.1.1 Advancements in Materials and Manufacturing Processes

- 1.7.1.2 Increasing Deployment of Satellite Constellation

- 1.7.2 Market Restraints

- 1.7.2.1 Risk of Orbital Debris Colliding with Propellant Tanks

- 1.7.3 Market Opportunities

- 1.7.3.1 Modular and Reusable Propellant Tank Systems

- 1.7.3.2 Increasing Deep Space Mission

- 1.7.1 Market Drivers

- 1.8 Supply Chain Overview

2 Application

- 2.1 Application Segmentation

- 2.2 Application Summary

- 2.3 Global Space-Qualified Propellant Tank Market

- 2.3.1 Market Overview

- 2.4 Global Space-Qualified Propellant Tank Market (by Platform)

- 2.4.1 Satellite

- 2.4.1.1 0-500 Kg

- 2.4.1.2 501-1,000 Kg

- 2.4.1.3 1,001 Kg and Above

- 2.4.2 Launch Vehicle

- 2.4.2.1 Small Lift Launch Vehicle (0-2,200 Kg)

- 2.4.2.2 Medium and Heavy Lift Launch Vehicle (2,201 Kg and Above)

- 2.4.1 Satellite

- 2.5 Global Space-Qualified Propellant Tank Market (by End User)

- 2.5.1 Government and Military

- 2.5.2 Commercial

3 Products

- 3.1 Product Segmentation

- 3.2 Product Summary

- 3.3 Global Space-Qualified Propellant Tank Market

- 3.3.1 Market Overview

- 3.4 Global Space-Qualified Propellant Tank Market (by Material)

- 3.4.1 Carbon Fiber Composites

- 3.4.2 Aluminum and Titanium Alloys

- 3.4.3 Thermoset and Thermoplastic Composites

- 3.4.4 Nanomaterials

- 3.4.5 Others

- 3.5 Global Space-Qualified Propellant Tank Market (by Manufacturing Process)

- 3.5.1 Automated Fiber Placement

- 3.5.2 Compression Molding

- 3.5.3 Additive Manufacturing

- 3.5.4 Conventional Manufacturing

- 3.5.5 Others

- 3.6 Global Space-Qualified Propellant Tank Market (by Propellant Tank)

- 3.6.1 Diaphragm Tanks

- 3.6.2 Propellant Management Device Tanks

- 3.6.3 Helium, Nitrogen, and Xenon Tanks

- 3.6.4 Aluminum Alloy Tanks

- 3.6.5 Hydrazine Tanks

- 3.6.6 High-Test Peroxide Tanks

4 Regions

- 4.1 Regional Summary

- 4.2 North America

- 4.2.1 Regional Overview

- 4.2.2 Driving Factors for Market Growth

- 4.2.3 Factors Challenging the Market

- 4.2.4 Application (by Platform)

- 4.2.5 Product (by Propellant Tank)

- 4.2.6 U.S.

- 4.2.6.1 Application (by Platform)

- 4.2.6.2 Product (by Propellant Tank)

- 4.2.7 Canada

- 4.2.7.1 Application (by Platform)

- 4.2.7.2 Product (by Propellant Tank)

- 4.3 Europe

- 4.3.1 Regional Overview

- 4.3.2 Driving Factors for Market Growth

- 4.3.3 Factors Challenging the Market

- 4.3.4 Application (by Platform)

- 4.3.5 Product (by Propellant Tank)

- 4.3.6 France

- 4.3.6.1 Application (by Platform)

- 4.3.6.2 Product (by Propellant Tank)

- 4.3.7 Germany

- 4.3.7.1 Application (by Platform)

- 4.3.7.2 Product (by Propellant Tank)

- 4.3.8 U.K.

- 4.3.8.1 Application (by Platform)

- 4.3.8.2 Product (by Propellant Tank)

- 4.3.9 Russia

- 4.3.9.1 Application (by Platform)

- 4.3.9.2 Product (by Propellant Tank)

- 4.3.10 Rest-of-Europe

- 4.3.10.1 Application (by Platform)

- 4.3.10.2 Product (by Propellant Tank)

- 4.4 Asia-Pacific

- 4.4.1 Regional Overview

- 4.4.2 Driving Factors for Market Growth

- 4.4.3 Factors Challenging the Market

- 4.4.4 Application (by Platform)

- 4.4.5 Product (by Propellant Tank)

- 4.4.6 China

- 4.4.6.1 Application (by Platform)

- 4.4.6.2 Product (by Propellant Tank)

- 4.4.7 India

- 4.4.7.1 Application (by Platform)

- 4.4.7.2 Product (by Propellant Tank)

- 4.4.8 Japan

- 4.4.8.1 Application (by Platform)

- 4.4.8.2 Product (by Propellant Tank)

- 4.4.9 Rest-of-Asia-Pacific

- 4.4.9.1 Application (by Platform)

- 4.4.9.2 Product (by Propellant Tank)

- 4.5 Rest-of-the-World

- 4.5.1 Regional Overview

- 4.5.2 Driving Factors for Market Growth

- 4.5.3 Factors Challenging the Market

- 4.5.4 Application (by Platform)

- 4.5.5 Product (by Propellant Tank)

- 4.5.6 Latin America

- 4.5.7 Regional Overview

- 4.5.7.1 Application (by Platform)

- 4.5.7.2 Product (by Propellant Tank)

- 4.5.8 Middle East and Africa

- 4.5.9 Regional Overview

- 4.5.9.1 Application (by Platform)

- 4.5.9.2 Product (by Propellant Tank)

5 Markets - Competitive Benchmarking & Company Profiles

- 5.1 Next Frontiers

- 5.2 Geographic Assessment

- 5.2.1 Airbus S.A.S.

- 5.2.1.1 Overview

- 5.2.1.2 Top Products/Product Portfolio

- 5.2.1.3 Top Competitors

- 5.2.1.4 Target Customers

- 5.2.1.5 Key Personnel

- 5.2.1.6 Analyst View

- 5.2.1.7 Market Share, 2022

- 5.2.2 AdamWorks LLC

- 5.2.2.1 Overview

- 5.2.2.2 Top Products/Product Portfolio

- 5.2.2.3 Top Competitors

- 5.2.2.4 Target Customers

- 5.2.2.5 Key Personnel

- 5.2.2.6 Analyst View

- 5.2.2.7 Market Share, 2022

- 5.2.3 Ariane Group

- 5.2.3.1 Overview

- 5.2.3.2 Top Products/Product Portfolio

- 5.2.3.3 Top Competitors

- 5.2.3.4 Target Customers

- 5.2.3.5 Key Personnel

- 5.2.3.6 Analyst View

- 5.2.3.7 Market Share, 2022

- 5.2.4 Busek Co. Inc.

- 5.2.4.1 Overview

- 5.2.4.2 Top Products/Product Portfolio

- 5.2.4.3 Top Competitors

- 5.2.4.4 Target Customers

- 5.2.4.5 Key Personnel

- 5.2.4.6 Analyst View

- 5.2.4.7 Market Share, 2022

- 5.2.5 Infinite Composite Technologies

- 5.2.5.1 Overview

- 5.2.5.2 Top Products/Product Portfolio

- 5.2.5.3 Top Competitors

- 5.2.5.4 Target Customers

- 5.2.5.5 Key Personnel

- 5.2.5.6 Analyst View

- 5.2.5.7 Market Share, 2022

- 5.2.6 IHI Aerospace Co., Ltd.

- 5.2.6.1 Overview

- 5.2.6.2 Top Products/Product Portfolio

- 5.2.6.3 Top Competitors

- 5.2.6.4 Target Customers

- 5.2.6.5 Key Personnel

- 5.2.6.6 Analyst View

- 5.2.6.7 Market Share, 2022

- 5.2.7 Lockheed Martin Corporation

- 5.2.7.1 Overview

- 5.2.7.2 Top Products/Product Portfolio

- 5.2.7.3 Top Competitors

- 5.2.7.4 Target Customers

- 5.2.7.5 Key Personnel

- 5.2.7.6 Analyst View

- 5.2.7.7 Market Share, 2022

- 5.2.8 Microcosm, Inc.

- 5.2.8.1 Overview

- 5.2.8.2 Top Products/Product Portfolio

- 5.2.8.3 Top Competitors

- 5.2.8.4 Target Customers

- 5.2.8.5 Key Personnel

- 5.2.8.6 Analyst View

- 5.2.8.7 Market Share, 2022

- 5.2.9 Moog Inc.

- 5.2.9.1 Overview

- 5.2.9.2 Top Products/Product Portfolio

- 5.2.9.3 Top Competitors

- 5.2.9.4 Target Customers

- 5.2.9.5 Key Personnel

- 5.2.9.6 Analyst View

- 5.2.9.7 Market Share, 2022

- 5.2.10 OHB SE

- 5.2.10.1 Overview

- 5.2.10.2 Top Products/Product Portfolio

- 5.2.10.3 Top Competitors

- 5.2.10.4 Target Customers

- 5.2.10.5 Key Personnel

- 5.2.10.6 Analyst View

- 5.2.10.7 Market Share, 2022

- 5.2.11 Northrop Grumman Corporation

- 5.2.11.1 Overview

- 5.2.11.2 Top Products/Product Portfolio

- 5.2.11.3 Top Competitors

- 5.2.11.4 Target Customers

- 5.2.11.5 Key Personnel

- 5.2.11.6 Analyst View

- 5.2.11.7 Market Share, 2022

- 5.2.12 Nammo AS

- 5.2.12.1 Overview

- 5.2.12.2 Top Products/Product Portfolio

- 5.2.12.3 Top Competitors

- 5.2.12.4 Target Customers

- 5.2.12.5 Key Personnel

- 5.2.12.6 Analyst View

- 5.2.12.7 Market Share, 2022

- 5.2.13 Peak Technology

- 5.2.13.1 Overview

- 5.2.13.2 Top Products/Product Portfolio

- 5.2.13.3 Top Competitors

- 5.2.13.4 Target Customers

- 5.2.13.5 Key Personnel

- 5.2.13.6 Analyst View

- 5.2.13.7 Market Share, 2022

- 5.2.14 Phase Four

- 5.2.14.1 Overview

- 5.2.14.2 Top Products/Product Portfolio

- 5.2.14.3 Top Competitors

- 5.2.14.4 Target Customers

- 5.2.14.5 Key Personnel

- 5.2.14.6 Analyst View

- 5.2.14.7 Market Share, 2022

- 5.2.15 Stelia Aerospace North America Inc.

- 5.2.15.1 Overview

- 5.2.15.2 Top Products/Product Portfolio

- 5.2.15.3 Top Competitors

- 5.2.15.4 Target Customers

- 5.2.15.5 Key Personnel

- 5.2.15.6 Analyst View

- 5.2.15.7 Market Share, 2022

- 5.2.1 Airbus S.A.S.

6 Research Methodology

- 6.1 Data Sources

- 6.1.1 Primary Data Sources

- 6.1.2 Secondary Data Sources

- 6.1.3 Data Triangulation

- 6.2 Market Estimation and Forecast