|

市場調査レポート

商品コード

1693820

インドのエンジニアリングプラスチック市場:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)India Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのエンジニアリングプラスチック市場:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 259 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

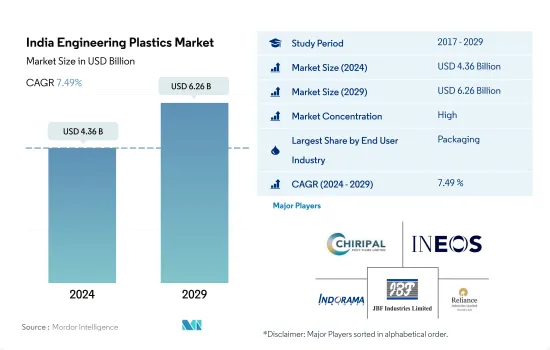

インドのエンジニアリングプラスチック市場規模は2024年に43億6,000万米ドルと推定・予測され、2029年には62億6,000万米ドルに達し、予測期間中(2024~2029年)のCAGRは7.49%で成長すると予測されます。

予測期間中も包装産業が優位を保つ

- エンジニアリングプラスチックの用途は、航空宇宙の内装壁パネルやドアから硬質包装や軟質包装に至るまで幅広いです。インドのエンジニアリングプラスチック市場は、包装、電気・電子、自動車といった産業が牽引しています。2022年の市場売上高シェアは、包装が27.58%、電気・電子が21.10%と最も高いです。

- インドのエンジニアリングプラスチック市場では、包装が最大のシェアを占めています。インドの包装産業は、新製品を発売する際のプラスチック包装の需要により、第二級都市で盛んになっています。国内外の企業が合弁や提携といった戦略を採用し、市場成長にプラスの影響を与えています。また、主に樹脂の低コストと柔軟性によって成長が促進され、環境への二酸化炭素排出量も低く抑えられています。インドのプラスチック包装の生産量は、2021年の400万トンから2022年には416万トンとなり、数量ベースで前年比3.97%の伸びを示しました。

- 電気・電子産業はインドで最も急速に拡大しているセグメントであり、2021年の同国のGDPに約3.4%寄与しています。政府は、今後数年間で、スマートフォン、半導体、デザイン、ITソフトウェアハードウェア部品の4つのPLI(生産連動型インセンティブ)スキームを通じて、エレクトロニクス産業を振興し、その価値を170億米ドルにまで高める戦略を概説しています。インドの電子製品輸出は2022年9月に20億907万米ドルとなり、前年同月比71.99%増加しました。これらの要因によって、エレクトロニクス産業におけるエンジニアリングプラスチックの成長が促進され、インドの予測期間中のCAGRは金額ベースで9.42%を記録すると予想されます。

インドのエンジニアリングプラスチック市場動向

政府による規制支援が産業の成長に重要な役割を果たす

- インドでは、2020~2021年にかけて電気・電子機器の売上が19.6%増加しました。エレクトロニクス製造業の生産額は2015~16年の371億米ドルから2020~2021年には673億米ドルに増加します。しかし、COVID-19関連の混乱が2020~2021年の成長軌道に影響を与え、生産高の減少につながりました。

- インドの電子製品輸出は2022年9月に20億907万米ドルとなり、前年比71.99%増加しました。携帯電話、ITハードウェア(ノートパソコン、タブレット)、民生用電子機器(テレビ、オーディオ)、産業用電子機器、自動車用電子機器がこのセグメントの主要輸出品目です。電子・IT省は、インドのエレクトロニクス産業の輸出額は2026年までに1,200億米ドルに達すると予測しています。米国はインドの電子機器輸出の最大の輸入国であり、次いでアラブ首長国連邦がそれぞれ輸出全体の18%と17%を占めています。インドからの携帯電話輸出は、南アジア、アフリカ、中東に大きな市場を見出し、これらの製品の主要輸入地域となっています。

- 電子製品へのニーズの高まりを受けて、政府は同国の電子製品産業を促進するため、生産連動型奨励金(PLI)、電子部品・半導体製造(SPECS)、改良型電子製造クラスター(EMC 2.0)などを打ち出しました。インドのエレクトロニクス産業は、2020~2021年の750億米ドルから2025~26年には3,000億米ドルに達すると予想されています。インドのエレクトロニクス部門は、インドのビジネスプロセスアウトソーシング(BPO)産業の市場開拓とシェア拡大により、今後3~5年でインドのトップ輸出部門のひとつになる可能性を秘めています。

インドのエンジニアリングプラスチック産業概要

インドのエンジニアリングプラスチック市場はかなり統合されており、上位5社で85.39%を占めています。この市場の主要企業は、Chiripal Poly Film、INEOS、IVL Dhunseri Petrochem Industries Private Limited(IDPIPL)、JBF Industries Ltd、Reliance Industries Limitedなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 包装

- 輸出入動向

- 価格動向

- リサイクル概要

- ポリアミド(PA)のリサイクル動向

- ポリカーボネート(PC)のリサイクル動向

- ポリエチレンテレフタレート(PET)のリサイクル動向

- スチレン系共重合体(ABS、SAN)のリサイクル動向

- 規制の枠組み

- インド

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 工業・機械

- 包装

- その他

- 樹脂タイプ

- フッ素樹脂

- サブタイプ別

- エチレンテトラフルオロエチレン(ETFE)

- フッ素化エチレンプロピレン(FEP)

- ポリテトラフルオロエチレン(PTFE)

- ポリフッ化ビニル(PVF)

- ポリフッ化ビニリデン(PVDF)

- その他のサブレジンタイプ

- 液晶ポリマー(LCP)

- ポリアミド(PA)

- サブレジンタイプ別

- アラミド

- ポリアミド(PA)6

- ポリアミド(PA)66

- ポリフタルアミド

- ポリブチレンテレフタレート(PBT)

- ポリカーボネート(PC)

- ポリエーテルエーテルケトン(PEEK)

- ポリエチレンテレフタレート(PET)

- ポリイミド(PI)

- ポリメチルメタクリレート(PMMA)

- ポリオキシメチレン(POM)

- スチレン共重合体(ABSとSAN)

- フッ素樹脂

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Bhansali Engineering Polymers Limited

- Chiripal Poly Film

- DuPont

- Ester Industries Limited

- Gujarat Fluorochemicals Limited(GFL)

- Gujarat State Fertilizers & Chemicals Limited(GSFC)

- Hindustan Fluorocarbons Limited.

- INEOS

- IVL Dhunseri Petrochem Industries Private Limited(IDPIPL)

- JBF Industries Ltd

- LANXESS

- Mitsubishi Chemical Corporation

- Polyplex

- Reliance Industries Limited

- Solvay

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The India Engineering Plastics Market size is estimated at 4.36 billion USD in 2024, and is expected to reach 6.26 billion USD by 2029, growing at a CAGR of 7.49% during the forecast period (2024-2029).

Packaging industry to remain dominant during the forecast period

- Engineering plastics have applications ranging from interior wall panels and doors in aerospace to rigid and flexible packaging. The engineering plastics market in India is led by industries such as packaging, electrical and electronics, and automotive. Packaging and electrical and electronics accounted for the highest market revenue shares of 27.58% and 21.10%, respectively, in 2022.

- Packaging holds the largest share of India's engineering plastics market. The packaging industry in India is flourishing in second-tier cities due to the demand for plastic packaging in launching new products. Domestic and foreign firms are adopting strategies such as joint ventures and partnerships that positively impact market growth. The growth is also primarily driven by the low cost and flexibility of the resins, which also maintain a low-carbon footprint on the environment. India's plastic packaging production had a volume of 4.16 million tons in 2022 from 4 million tons in 2021, at a Y-o-Y growth of 3.97% by volume.

- The electrical and electronics industry is India's most rapidly expanding sector, with the electronics segment contributing approximately 3.4% to the country's GDP in 2021. The government has outlined a strategy to promote the electronics industry and increase its value to USD 17 billion through four PLI (production-linked incentive) schemes for smartphones, semiconductors, design, and IT software and hardware components over the next few years. India's export of electronic goods stood at USD 2,009.07 million in September 2022, with an increase of 71.99% Y-o-Y. These factors are expected to impetus the growth of engineering plastics in the electronics industry, registering a CAGR of 9.42%, by value, over the forecast period in India.

India Engineering Plastics Market Trends

Regulatory support by the government to play key role in industry growth

- India witnessed an increase in electrical and electronics revenue by 19.6% from 2020 to 2021. The electronics manufacturing industry's production grew from a value of USD 37.1 billion in 2015-16 to USD 67.3 billion in 2020-21. However, COVID-19-related disruptions impacted the growth trajectory in 2020-21 and led to a decline in output.

- India's export of electronic goods stood at USD 2,009.07 million in September 2022, an increase of 71.99% Y-o-Y. Mobile phones, IT hardware (laptops, tablets), consumer electronics (TV and audio), industrial electronics, and auto electronics are key export products in this sector. The Ministry of Electronics & IT estimates that India's electronics industry exports are expected to reach a value of USD 120 billion by 2026. The United States is the largest importer of India's electronic exports, followed by the United Arab Emirates, accounting for 18% and 17% of the overall exports, respectively. Mobile phone exports from India find significant markets in South Asia, Africa, and the Middle East, making them key importing regions for these products.

- With the growing need for electronic goods, the government launched production-linked incentives (PLI), Manufacturing of Electronic Components and Semiconductors (SPECS), Modified Electronic Manufacturing Clusters (EMC 2.0), etc., to promote the country's electronic goods industry. The country's electronics industry is expected to reach a value of USD 300 billion by 2025-26 from USD 75 billion in 2020-21. India's electronics sector has the potential to become one of the top exporting sectors of India in the next 3-5 years due to the development and increase in the market share of the Indian business process outsourcing (BPO) industry.

India Engineering Plastics Industry Overview

The India Engineering Plastics Market is fairly consolidated, with the top five companies occupying 85.39%. The major players in this market are Chiripal Poly Film, INEOS, IVL Dhunseri Petrochem Industries Private Limited (IDPIPL), JBF Industries Ltd and Reliance Industries Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.3 Price Trends

- 4.4 Recycling Overview

- 4.4.1 Polyamide (PA) Recycling Trends

- 4.4.2 Polycarbonate (PC) Recycling Trends

- 4.4.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.4.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.5 Regulatory Framework

- 4.5.1 India

- 4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Resin Type

- 5.2.1 Fluoropolymer

- 5.2.1.1 By Sub Resin Type

- 5.2.1.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.1.1.3 Polytetrafluoroethylene (PTFE)

- 5.2.1.1.4 Polyvinylfluoride (PVF)

- 5.2.1.1.5 Polyvinylidene Fluoride (PVDF)

- 5.2.1.1.6 Other Sub Resin Types

- 5.2.2 Liquid Crystal Polymer (LCP)

- 5.2.3 Polyamide (PA)

- 5.2.3.1 By Sub Resin Type

- 5.2.3.1.1 Aramid

- 5.2.3.1.2 Polyamide (PA) 6

- 5.2.3.1.3 Polyamide (PA) 66

- 5.2.3.1.4 Polyphthalamide

- 5.2.4 Polybutylene Terephthalate (PBT)

- 5.2.5 Polycarbonate (PC)

- 5.2.6 Polyether Ether Ketone (PEEK)

- 5.2.7 Polyethylene Terephthalate (PET)

- 5.2.8 Polyimide (PI)

- 5.2.9 Polymethyl Methacrylate (PMMA)

- 5.2.10 Polyoxymethylene (POM)

- 5.2.11 Styrene Copolymers (ABS and SAN)

- 5.2.1 Fluoropolymer

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Bhansali Engineering Polymers Limited

- 6.4.2 Chiripal Poly Film

- 6.4.3 DuPont

- 6.4.4 Ester Industries Limited

- 6.4.5 Gujarat Fluorochemicals Limited (GFL)

- 6.4.6 Gujarat State Fertilizers & Chemicals Limited (GSFC)

- 6.4.7 Hindustan Fluorocarbons Limited.

- 6.4.8 INEOS

- 6.4.9 IVL Dhunseri Petrochem Industries Private Limited (IDPIPL)

- 6.4.10 JBF Industries Ltd

- 6.4.11 LANXESS

- 6.4.12 Mitsubishi Chemical Corporation

- 6.4.13 Polyplex

- 6.4.14 Reliance Industries Limited

- 6.4.15 Solvay

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms