|

市場調査レポート

商品コード

1685843

北米のエンジニアリングプラスチック:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)North America Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のエンジニアリングプラスチック:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 306 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

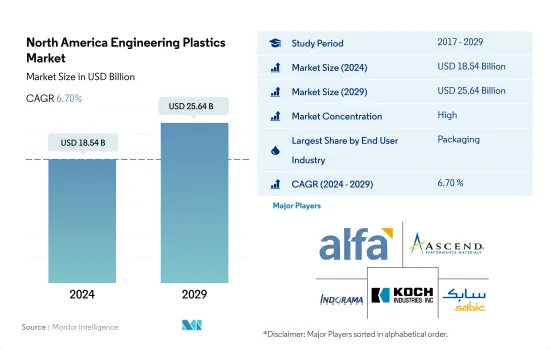

北米のエンジニアリングプラスチック市場規模は2024年に185億4,000万米ドルと推定・予測され、2029年には256億4,000万米ドルに達し、予測期間中(2024-2029年)のCAGRは6.70%で成長すると予測されます。

包装業界は電気・電子業界に数量シェアを奪われる

- エンジニアリングプラスチックの用途は、航空宇宙の内装壁パネルやドアから硬質・軟質パッケージングまで多岐にわたる。北米のエンジニアリングプラスチック市場は、包装、電気・電子、自動車といった産業が牽引しています。2022年のエンジニアリングプラスチック市場の売上高は、包装が約31.35%、電気・電子が約17.43%を占めています。

- 世界的に家族の人数が少なくなり、都市化と家族の人口動態が大きく変化しているため、この地域では包装が最大のエンドユーザー産業となっています。こうした要因により、機能的で包装済みの便利な食品の需要が高まっています。北米の2022年のプラスチック包装生産量は2,240万トンで、世界全体の16.6%を占めました。この地域のエンジニアリングプラスチックの需要は、包装食品や飲食品に対する消費者需要の増加により増加しています。

- 電気・電子部門はこの地域で2番目に大きく、特に米国で大きいです。同部門はGDPの1.6%を占めています。2022年には同地域で5,761億米ドルの売上高を計上し、電気・電子機器に対する需要を増大させるとともに、電気自動車、自律型ロボット、極秘防衛技術の登場を後押しし、エンジニアリングプラスチックの需要を押し上げています。

- 電気・電子産業は、様々な電気・電子用途におけるプラスチック複合材料の必要性からエンジニアリングプラスチックの用途が増加しているため、収益と予測期間(2023~2029年)のCAGRは8.54%と予測され、この地域で最も急成長しています。

技術革新と相まって、進化する消費者動向と産業動向がエンジニアリングプラスチックの需要を押し上げる可能性があります。

- 2022年のエンジニアリングプラスチックの世界消費シェアは、北米が15%を占めました。エンジニアリングプラスチックは汎用性の高い特性を示すため、自動車、包装、電気・電子産業で用途が見出されています。

- 米国は2022年に金額ベースで前年比7.14%の成長を記録したが、これは包装産業と電気・電子産業によるもので、それぞれ金額ベースで市場シェアの27%と24%を占めました。すぐに食べられるコンビニエンス・フードの需要が増加し、外出の多いライフスタイルの動向が台頭しているため、包装資材の消費量が増加しており、同地域のエンジニアリングプラスチックの販売動向を後押ししています。企業が在宅勤務モデルを採用し、人々がホームオフィスを構えるようになったことで、電子機器の需要も増加しました。技術革新もまた、電子機器に対する安定した需要を毎年生み出しています。

- メキシコは最も急成長している市場であり、2022年には金額ベースで2021年比10.53%の成長を記録し、産業機械・設備産業が牽引しています。メキシコは、高速道路の整備、港湾の近代化、農場の機械化による拡大を目指しており、建設機械と農業機械の需要を押し上げています。

- 北米のエンジニアリングプラスチック市場は、予測期間中にCAGR 6.62%を記録すると予想され、中でも電気・電子産業は金額ベースでCAGR 8.54%と最も高いCAGRを記録します。先端材料、有機エレクトロニクス、小型化、AIやIoTのような破壊的技術の使用も、スマートな製造方法の採用を後押しし、業界の成長を促進する可能性があります。

北米のエンジニアリングプラスチック市場動向

技術革新の力強い成長が業界全体の成長を後押し

- 北米の電気・電子機器生産は、スマートテレビ、冷蔵庫、エアコンなどの家電製品需要の増加と相まって、技術の進歩により2017年から2019年にかけてCAGRが1.4%を超えました。電子技術革新の急速なペースは、より新しくより高速な電子製品への需要を促進しています。その結果、この地域の電気・電子機器生産も増加しています。

- 北米の電子機器売上高は、生産施設の操業停止、サプライチェーンの混乱、その他様々な制約のため、COVID-19の影響により、2020年には2019年比で約9%減少しました。その結果、同地域の電気・電子機器生産による収益は2020年に前年比4.7%減少しました。

- 2021年には、同地域の消費者向け電子機器の売上高は約1,130億米ドルに達し、2020年より4%増加しました。その結果、北米の電気・電子機器生産は2021年に前年比13.8%増となりました。

- 2027年には、北米は電気・電子機器生産で第3位の地域となり、世界市場の約10.5%のシェアを占めると予測されています。効率性と低コストを実現するために、バーチャルリアリティ、IoTソリューション、ロボット工学などの先進技術が家電製品に登場したことが、家電産業に大きなメリットをもたらしています。同地域の家電産業は、2023年の1,276億米ドルから2027年には約1,618億米ドルの市場規模に達すると予測されています。その結果、同地域の電気・電子製品に対する需要は増加すると予測されます。

北米のエンジニアリングプラスチックス産業の概要

北米のエンジニアリングプラスチックス市場はかなり統合されており、上位5社で68.68%を占めています。この市場の主要企業は以下の通りです。 Alfa S.A.B. de C.V., Ascend Performance Materials, Indorama Ventures Public Company Limited, Koch Industries, Inc. and SABIC(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 包装

- 輸出入動向

- フッ素樹脂貿易

- ポリアミド(PA)貿易

- ポリカーボネート(PC)貿易

- ポリエチレンテレフタレート(PET)の貿易

- ポリメチルメタクリレート(PMMA)の貿易

- ポリオキシメチレン(POM)貿易

- スチレン共重合体(ABSとSAN)の貿易

- 価格動向

- リサイクルの概要

- ポリアミド(PA)のリサイクル動向

- ポリカーボネート(PC)のリサイクル動向

- ポリエチレンテレフタレート(PET)のリサイクル動向

- スチレン系共重合体(ABS、SAN)のリサイクル動向

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 工業・機械

- 包装

- その他エンドユーザー産業

- 樹脂タイプ

- フッ素樹脂

- サブタイプ別

- エチレンテトラフルオロエチレン(ETFE)

- フッ素化エチレンプロピレン(FEP)

- ポリテトラフルオロエチレン(PTFE)

- ポリフッ化ビニル(PVF)

- ポリフッ化ビニリデン(PVDF)

- その他のサブレジンタイプ

- 液晶ポリマー(LCP)

- ポリアミド(PA)

- サブレジンタイプ別

- アラミド

- ポリアミド(PA)6

- ポリアミド(PA)66

- ポリフタルアミド

- ポリブチレンテレフタレート(PBT)

- ポリカーボネート(PC)

- ポリエーテルエーテルケトン(PEEK)

- ポリエチレンテレフタレート(PET)

- ポリイミド(PI)

- ポリメチルメタクリレート(PMMA)

- ポリオキシメチレン(POM)

- スチレン共重合体(ABSおよびSAN)

- フッ素樹脂

- 国

- カナダ

- メキシコ

- 米国

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Alfa S.A.B. de C.V.

- Arkema

- Ascend Performance Materials

- BASF SE

- Celanese Corporation

- Covestro AG

- DuPont

- Eastman Chemical Company

- Formosa Plastics Group

- Indorama Ventures Public Company Limited

- INEOS

- Koch Industries, Inc.

- SABIC

- Solvay

- Trinseo

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The North America Engineering Plastics Market size is estimated at 18.54 billion USD in 2024, and is expected to reach 25.64 billion USD by 2029, growing at a CAGR of 6.70% during the forecast period (2024-2029).

Packaging industry to lose some of its volume share to electrical and electronics industry

- Engineering plastics have applications ranging from interior wall panels and doors in aerospace to rigid and flexible packaging. The North American engineering plastics market is led by industries such as packaging, electrical and electronics, and automotive. Packaging and electrical and electronics accounted for around 31.35% and 17.43%, respectively, of the engineering plastics market in terms of revenue in 2022.

- Packaging is the largest end-user industry in the region due to families worldwide becoming smaller and significant changes in urbanization and family demographics. These factors increase the demand for functional, prepackaged, and convenient food products. Plastic packaging production in North America had a volume of 22.4 million tons in 2022, which was 16.6% globally. The demand for engineering plastics in the region is increasing due to the increasing consumer demand for packaged food and beverages.

- The electrical and electronics sector is the second largest in the region and especially in the United States. The sector accounted for 1.6% of the GDP. It generated a revenue of USD 576.1 billion in 2022 in the region, thus increasing the demand for electrical and electronics and empowering the onset of electric vehicles, autonomous robots, and top-secret defense technologies, thereby boosting the demand for engineering plastics.

- The electrical and electronics industry is the fastest-growing in the region by revenue, with an expected CAGR of 8.54% during the forecast period (2023-2029), due to increasing applications of engineering plastics for the need of plastic composites in various electrical and electronics applications.

Evolving consumer and industrial trends, coupled with technological innovations, may boost the demand for engineering plastics

- North America accounted for a 15% consumption share of engineering plastics globally in 2022. Engineering plastics exhibit versatile properties, thus finding applications in the automotive, packaging, and electrical and electronics industries.

- The United States recorded a growth of 7.14% by value in 2022 compared to the previous year, attributed to the packaging and electrical and electronics industries, which held 27% and 24% of the market shares, respectively, by value. With an increase in the demand for ready-to-eat convenience food products and the emerging trend of an on-the-go lifestyle, the consumption of packaging materials has increased, thus boosting the sales of engineering plastics in the region. With companies adopting work-from-home models and people setting up home offices, the demand for electronic devices also increased. Technological innovations are also creating consistent demand for electronic gadgets every year.

- Mexico is the fastest-growing market, recording a growth of 10.53% in terms of value in 2022 compared to 2021, led by the industrial machinery and equipment industry. Mexico aims to improve its highways, modernize its ports, and expand its farms by making them more mechanized, thus boosting the demand for construction and farming machinery.

- The North American engineering plastics market is expected to register a CAGR of 6.62% during the forecast period, with the electrical and electronics industry recording the highest CAGR of 8.54% by value. The use of advanced materials, organic electronics, miniaturization, and disruptive technologies like AI and the IoT may also boost the adoption of smart manufacturing practices, thus driving the industry's growth.

North America Engineering Plastics Market Trends

Strong growth of technological innovations to augment the overall growth of the industry

- Electrical and electronics production in North America witnessed a CAGR of over 1.4% between 2017 and 2019 owing to the advancement of technology, coupled with the increasing demand for consumer electronics products, such as smart TVs, refrigerators, air conditioners, and other products. The rapid pace of electronic technological innovation is driving the demand for newer and faster electronic products. As a result, it has also increased the electrical and electronics production in the region.

- Electronic device sales in North America fell by around 9% in 2020 compared to 2019, owing to the COVID-19 impact, because of the production facility shutdowns, supply chain disruptions, and various other constraints. As a result, revenue from electrical and electronics production in the region decreased by 4.7% in 2020 compared to the previous year.

- In 2021, the sales of consumer electronics in the region reached around USD 113 billion, 4% higher than in 2020. As a result, North America's electrical and electronics production grew by 13.8% in 2021 in terms of revenue compared to the previous year.

- By 2027, North America is projected to be the third-largest region for electrical and electronics production and account for a share of around 10.5% of the global market. The emergence of advanced technologies such as virtual reality, IoT solutions, and robotics into consumer electronic products to achieve efficiency and low cost has provided a significant advantage to the consumer electronics industry. The consumer electronics industry in the region is projected to reach a market volume of around USD 161.8 billion by 2027 from USD 127.6 billion in 2023. As a result, the demand for electrical and electronic products in the region is projected to increase.

North America Engineering Plastics Industry Overview

The North America Engineering Plastics Market is fairly consolidated, with the top five companies occupying 68.68%. The major players in this market are Alfa S.A.B. de C.V., Ascend Performance Materials, Indorama Ventures Public Company Limited, Koch Industries, Inc. and SABIC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Fluoropolymer Trade

- 4.2.2 Polyamide (PA) Trade

- 4.2.3 Polycarbonate (PC) Trade

- 4.2.4 Polyethylene Terephthalate (PET) Trade

- 4.2.5 Polymethyl Methacrylate (PMMA) Trade

- 4.2.6 Polyoxymethylene (POM) Trade

- 4.2.7 Styrene Copolymers (ABS and SAN) Trade

- 4.3 Price Trends

- 4.4 Recycling Overview

- 4.4.1 Polyamide (PA) Recycling Trends

- 4.4.2 Polycarbonate (PC) Recycling Trends

- 4.4.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.4.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.5 Regulatory Framework

- 4.5.1 Canada

- 4.5.2 Mexico

- 4.5.3 United States

- 4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Resin Type

- 5.2.1 Fluoropolymer

- 5.2.1.1 By Sub Resin Type

- 5.2.1.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.1.1.3 Polytetrafluoroethylene (PTFE)

- 5.2.1.1.4 Polyvinylfluoride (PVF)

- 5.2.1.1.5 Polyvinylidene Fluoride (PVDF)

- 5.2.1.1.6 Other Sub Resin Types

- 5.2.2 Liquid Crystal Polymer (LCP)

- 5.2.3 Polyamide (PA)

- 5.2.3.1 By Sub Resin Type

- 5.2.3.1.1 Aramid

- 5.2.3.1.2 Polyamide (PA) 6

- 5.2.3.1.3 Polyamide (PA) 66

- 5.2.3.1.4 Polyphthalamide

- 5.2.4 Polybutylene Terephthalate (PBT)

- 5.2.5 Polycarbonate (PC)

- 5.2.6 Polyether Ether Ketone (PEEK)

- 5.2.7 Polyethylene Terephthalate (PET)

- 5.2.8 Polyimide (PI)

- 5.2.9 Polymethyl Methacrylate (PMMA)

- 5.2.10 Polyoxymethylene (POM)

- 5.2.11 Styrene Copolymers (ABS and SAN)

- 5.2.1 Fluoropolymer

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Alfa S.A.B. de C.V.

- 6.4.2 Arkema

- 6.4.3 Ascend Performance Materials

- 6.4.4 BASF SE

- 6.4.5 Celanese Corporation

- 6.4.6 Covestro AG

- 6.4.7 DuPont

- 6.4.8 Eastman Chemical Company

- 6.4.9 Formosa Plastics Group

- 6.4.10 Indorama Ventures Public Company Limited

- 6.4.11 INEOS

- 6.4.12 Koch Industries, Inc.

- 6.4.13 SABIC

- 6.4.14 Solvay

- 6.4.15 Trinseo

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms