|

市場調査レポート

商品コード

1693711

欧州の民間航空機用機内エンターテイメントシステム- 市場シェア分析、産業動向、成長予測(2025年~2030年)Europe Commercial Aircraft In-Flight Entertainment System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の民間航空機用機内エンターテイメントシステム- 市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 118 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

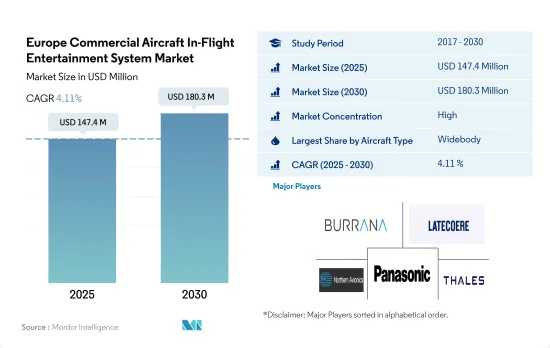

欧州の民間航空機用機内エンターテイメントシステム市場規模は、2025年に1億4,740万米ドルと推定され、2030年には1億8,030万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは4.11%で成長すると予測されます。

欧州の航空会社は長距離便にナローボディ機を使用することが増えており、ナローボディ機のIFEシステムの使用が容易になっています。

- 機内エンターテイメントは客室のインテリアに不可欠であり、乗客のフライト体験全体を決定づける。欧州の航空会社による長距離路線へのナローボディ機の採用が増加し、ナローボディ機へのIFEシステムの導入を後押ししています。ルフトハンザやエールフランスなどの航空会社は、ビジネスクラスの座席を改善し、IFEシステムを通じて顧客体験を向上させることに注力しています。

- この地域では、パナソニックは、Astrova、NEXT、Xシリーズなど、多くのバージョンのIFEシステムを提供する主要OEMの1つです。欧州の様々な航空会社は、客室クラスに応じて、LED、QLED、4K HDRスクリーンなど、異なる構成の12インチから18インチのスクリーンを使用しています。エア・欧州、ターキッシュ・エアラインズ、TUIエアウェイズは、2017~2022年にナローボディ機でIFEシステムを提供した地域の主要航空会社です。対照的に、エールフランスやブリティッシュ・エアウェイズなどの他の主要航空会社の一部は、9~12インチのスクリーンサイズを持つワイドボディ機にもIFEシステムを提供しています。同地域の未開拓市場における新規路線の追加による航空機調達数の急増は、欧州における民間航空機とそれに関連するIFEシステムの需要を押し上げると予想されます。

- 2017~2022年にかけて、ナローボディ機が納入機数の大半を占め、納入機数全体の82%を占めました。国内需要の拡大に伴い、ナローボディ市場の成長率はワイドボディ市場を上回ると予想されます。2022年、同地域の新造航空機の調達は、2019年比でパンデミック前の水準を38%上回りました。

欧州では機内接続性強化の需要が高まる見込みで、旅客体験全般を優先する航空会社に恩恵をもたらす

- 機内エンターテイメントは機内インテリアの不可欠な一部であり、乗客の完全なフライト体験を定義する上で近年ますます重要な役割を果たしています。IFEは機内インテリアの不可欠な一部であり、乗客の完全なフライト体験を決定づける重要な役割を果たしています。観測されているように、航空会社は航空機全体の重量を減らすために、より軽量なIFEシステムに切り替えつつあります。キャビンクラス、エコノミークラス、プレミアムエコノミークラスで見ると、2022年にはキャビンクラスがシートバックの機内エンターテイメント・スクリーン全体の約90%を占めます。

- 欧州の航空会社は、主要国での航空旅客輸送量の増加に対応するため、機体拡大計画を実施しています。IFEシステムの重要性が航空会社にとって単なる付加的なアメニティではなく必需品となっていることから、同地域のIFEシステムの需要を後押しすることが予想されます。

- タレス、サフラン、パナソニックは、欧州市場でIFEシステムを提供している主要企業です。ブリティッシュ・エアウェイズ、エールフランス、ルフトハンザなど、この地域の主要航空会社は、4KスクリーンとOLEDディスプレイの採用を重視し、エコノミークラスでのIFEシステムの可用性を高めることで、新規顧客の注目を集め、既存のサービスを向上させています。

- 民間航空機製造の主要OEMであるBoeingとAirbusは、欧州で多くの航空機を納入する見込みです。例えば、2023~2030年にかけて、この地域では2,300機以上のナローボディ機と290機以上のワイドボディ機が納入される見込みです。このように、新しい航空機の納入の増加に伴い、欧州の民間航空機用機内エンターテイメントシステム市場は予測期間中に高い成長を達成する見込みです。

欧州の民間航空機用機内エンターテイメントシステム市場動向

市場成長の主要理由は、欧州における航空機保有数の拡大と旅客航空需要の増加

- 欧州は2022年に航空旅客輸送量が最も多い第2位の地域となりました。欧州の航空旅客輸送量は2022年に10億5,000万人に達し、2017年から11%増加しました。航空会社は、航空需要の増加に対応するため、機材の大型化に注力しており、その結果、欧州では新造航空機の需要が大幅に増加する可能性があります。

- 2017~2022年の間に、合計1,206機の新造航空機が欧州に納入され、2023~2030年の間にさらに2,647機の新造ジェット機が納入されると予想されています。この過去に、欧州で新たに納入されたジェット機は、世界の民間航空機納入数の約25%に達しました。予測期間中の納入機数の増加には、旅客の搭乗率を高め、競合コストを削減し、限られた予算の旅行者の需要を満たす組織構造を構築する一方で、明確で手頃な市場機会を創出するLCCの事業革新など、多くの要因が寄与している可能性があります。この間、合計1,206機のジェット機が納入され、そのうち990機がナローボディ機でした。

- 2023年6月現在、この地域では約3,000機以上のAirbus機が納入されており、ナローボディセグメントではA320ceo、A320neo、A321ceo、A321neo、ワイドボディセグメントではA330-300、A350-900が主要納入機となっています。ライアンエアー、ルフトハンザ、ウィズエアー、アエロフロート・グループ、エールフランス-KLM、イージージェットなど、欧州の大手航空会社数社は、ナローボディとワイドボディの混合機を含め、1,600機以上の航空機の受注残を抱えています。こうした要因が、民間航空機の客室内装品市場の今後の成長を後押しすると予想されます。

航空旅客輸送量の伸びは、国内と国際航空旅行の需要増加によって支えられると予想されます。

- 2022年に欧州各国の渡航制限が徐々に緩和されたことで、欧州大陸内の移動はCOVID-19の流行時よりもはるかに容易になりました。この動向により、国際線需要が急増し、封鎖期間中に旅行できなかった旅客は、国内で休暇を取る代わりに再び海外へ飛びたがりました。2022年、欧州全体の航空旅客数は13億人に達し、2021年比で8%の伸びを示しました。英国、ドイツ、スペインは、欧州の航空旅客輸送量全体の36%を占めており、したがって、今後数年間は、他の欧州諸国と比較して、新型航空機に対するより多くの需要を生み出す可能性があります。また、欧州の航空会社は、世界の国際航空旅客数の40%近くを輸送しています。

- 2022年1~6月期の欧州の空港利用者数は2021年比で247%増加し、その結果、欧州大陸全体で6億6,000万人の旅客が増加しました。英国、オランダ、トルコ、ドイツは、最も利用者の多い空港を擁し、2022年上半期の旅客数は大幅な伸びを記録しました。2022年8月、欧州の上位5空港の旅客輸送量は68.1%増加したが、主にアジアで旅行制限が続いたため、流行前の2019年8月の水準を17.5%下回る水準にとどまりました。その他の欧州の空港でも、2022年8月に同様の航空旅客輸送量の増加が見られました。ウクライナの空港からは商業航空輸送量が減少し、ベラルーシとロシアの空港でもロシア・ウクライナ戦争が始まって以来、旅客数の減少が記録されました。2023~2030年には、国内・国際航空需要の増加により、航空旅客輸送量は31%急増すると予想されます。

欧州の民間航空機用機内エンターテイメントシステム産業概要

欧州の民間航空機用機内エンターテイメントシステム市場はかなり統合されており、上位5社で89.88%を占めています。この市場の主要企業は、Burrana、Latecoere、Northern Avionics srl、Panasonic Avionics Corporation、Thales Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 航空旅客輸送量

- 新規航空機納入数

- 一人当たりGDP(現行価格)

- 航空機メーカーの売上高

- 航空機受注残

- 受注総額

- 空港建設支出(継続中)

- 航空会社の燃料費

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 航空機タイプ

- ナローボディ

- ワイドボディ

- 国名

- フランス

- ドイツ

- スペイン

- トルコ

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Burrana

- Donica Aviation Engineering Co., Ltd

- IMAGIK International Corp.

- Latecoere

- Northern Avionics srl

- Panasonic Avionics Corporation

- Thales Group

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The Europe Commercial Aircraft In-Flight Entertainment System Market size is estimated at 147.4 million USD in 2025, and is expected to reach 180.3 million USD by 2030, growing at a CAGR of 4.11% during the forecast period (2025-2030).

European airlines increasingly use narrowbody aircraft for long-haul flights, making it easier for them to use IFE systems on narrowbody aircraft

- In-flight entertainment is integral to cabin interiors and defines a passenger's entire flight experience. The adoption of narrowbody aircraft in long-haul routes by European airlines has increased, aiding the deployment of IFE systems in narrowbody aircraft. Airlines such as Lufthansa and Air France focus on improving their business-class seats and enhancing the customer experience through IFE systems.

- In the region, Panasonic is one of the major OEMs that offers many versions of the IFE system, including Astrova, NEXT, and X Series. Various airlines in Europe use screens ranging from 12 inches to 18 inches with different configurations, such as LED, QLED, and 4K HDR screens, according to cabin class. Air Europa, Turkish Airlines, and TUI Airways are the major airlines in the region that offered IFE systems in their narrowbody fleet during 2017-2022. In contrast, some of the other major carriers, such as Air France and British Airways, also offered IFE systems in their widebody fleet with a screen size ranging from 9 to 12 inches. The surge in aircraft procurement numbers due to the addition of new routes in the underserved markets of the region is expected to boost the demand for commercial aircraft and its associated IFE systems in Europe.

- During 2017-2022, narrowbody aircraft accounted for the majority of deliveries, which accounted for 82% of the total aircraft delivered. As domestic demand has grown, the narrowbody market is expected to grow at a faster rate than the widebody market. In 2022, the procurement of new aircraft in the region has exceeded the pre-pandemic levels by 38% compared to 2019.

The demand for enhanced in-flight connectivity is expected to increase in Europe, benefiting airlines that prioritize the overall passenger experience

- In-flight entertainment is an integral part of the cabin interior, playing an increasingly important role in defining the complete passenger flight experience in recent years. The IFE is an integral part of the cabin interior, playing a vital role in defining a passenger's complete flight experience. As observed, airlines are switching to lighter IFE systems to reduce the aircraft's overall weight. In terms of cabin class, economy, and premium economy, cabin class accounted for around 90% of the overall seatback in-flight entertainment screens in 2022.

- Airline companies in Europe are implementing fleet expansion plans to cater to the growing air passenger traffic in the major countries. This is expected to aid the demand for IFE systems in the region, with the importance of the IFE systems making it a necessity for airlines rather than just an additional amenity.

- Thales, Safran, and Panasonic are the major players that provide IFE systems in the European market. The major airlines in the region, such as British Airways, Air France, and Lufthansa, emphasize the adoption of 4K screens and OLED displays and increase the availability of IFE systems in their economy class to attract the attention of new customers and improve their existing services.

- The major commercial aircraft manufacturing OEMs, Boeing and Airbus, are expected to deliver many aircraft in the European region. For instance, over 2300 narrowbody aircraft and 290+ widebody aircraft are expected to be delivered in the region during 2023-2030. Thus, with the increase in deliveries of new aircraft, the European commercial aircraft in-flight entertainment systems market is expected to achieve higher growth during the forecast period.

Europe Commercial Aircraft In-Flight Entertainment System Market Trends

The main reasons for market growth are the expansion of the fleet and the increased demand for passenger air travel in Europe

- Europe was the second-largest region with the highest air passenger traffic in 2022. Air passenger traffic in Europe reached 1.05 billion in 2022, up by 11% from 2017. Airlines are concentrating on growing their fleet sizes to meet the rising demand for air travel, which may result in a significant increase in the demand for new aircraft in Europe.

- Between 2017 and 2022, a total of 1,206 new aircraft were delivered to Europe, and another 2,647 new jets are anticipated to be delivered between 2023 and 2030. During the historic period, new jet deliveries in Europe amounted to around 25% of global commercial aircraft deliveries. A number of factors may contribute to the increasing number of deliveries during the forecast period, such as LCC's business innovation to increase passenger load factors, reduce competitive costs, and create an organizational structure that satisfies the demand for travelers with a limited budget while creating distinctly affordable market opportunities. On this note, a total of 1,206 jets were delivered during this period, of which 990 were narrowbody aircraft.

- As of June 2023, around 3,000+ Airbus aircraft were delivered in the region, with major deliveries by A320ceo, A320neo, A321ceo, and A321neo aircraft in the narrowbody segment, and A330-300 and A350-900 in the widebody segment. Several major airlines in Europe, such as Ryanair, Lufthansa, Wizz Air, Aeroflot Group, Air France-KLM, and EasyJet, have a backlog of over 1,600 aircraft, including a mix of narrowbody and widebody jets. Such factors are expected to aid the growth of the commercial aircraft cabin interior market in the future.

The growth in air passenger traffic is expected to be supported by the increasing demand for domestic and international air travel

- The gradual relaxation of travel restrictions in various European countries in 2022 made travel within the continent much easier than during the COVID-19 pandemic. Due to this trend, international demand soared, with passengers unable to travel during the lockdowns eager to fly abroad once again instead of taking domestic vacations. In 2022, air passenger traffic in the whole of Europe reached 1.3 billion, a growth of 8% compared to 2021. The United Kingdom, Germany, and Spain accounted for 36% of the total air passenger traffic in Europe and, hence, may generate more demand for new aircraft compared to other European countries over the coming years. European airlines have also been responsible for carrying almost 40% of global international air passengers.

- European airport traffic grew by 247% in the first six months of 2022 compared to 2021, resulting in an additional 660 million passengers handled across the continent. The United Kingdom, the Netherlands, Turkey, and Germany, which have some of the countries with the busiest airports, recorded a significant rise in passenger traffic in H1 2022. In August 2022, passenger traffic in the top five European airports increased by 68.1% but remained -17.5% below pre-pandemic August 2019 levels, mainly due to continued travel restrictions in Asia. A similar increase in air passenger traffic was observed at airports in the Rest of Europe in August 2022. Commercial air traffic declined from Ukrainian airports, and airports in Belarus and Russia recorded declining passenger volumes as well since the beginning of the Russia-Ukraine War. The air passenger traffic is expected to surge by 31% during 2023-2030, with increased demand in domestic and international aviation.

Europe Commercial Aircraft In-Flight Entertainment System Industry Overview

The Europe Commercial Aircraft In-Flight Entertainment System Market is fairly consolidated, with the top five companies occupying 89.88%. The major players in this market are Burrana, Latecoere, Northern Avionics srl, Panasonic Avionics Corporation and Thales Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 New Aircraft Deliveries

- 4.3 GDP Per Capita (current Price)

- 4.4 Revenue Of Aircraft Manufacturers

- 4.5 Aircraft Backlog

- 4.6 Gross Orders

- 4.7 Expenditure On Airport Construction Projects (ongoing)

- 4.8 Expenditure Of Airlines On Fuel

- 4.9 Regulatory Framework

- 4.10 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Aircraft Type

- 5.1.1 Narrowbody

- 5.1.2 Widebody

- 5.2 Country

- 5.2.1 France

- 5.2.2 Germany

- 5.2.3 Spain

- 5.2.4 Turkey

- 5.2.5 United Kingdom

- 5.2.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Burrana

- 6.4.2 Donica Aviation Engineering Co., Ltd

- 6.4.3 IMAGIK International Corp.

- 6.4.4 Latecoere

- 6.4.5 Northern Avionics srl

- 6.4.6 Panasonic Avionics Corporation

- 6.4.7 Thales Group

7 KEY STRATEGIC QUESTIONS FOR COMMERCIAL AIRCRAFT CABIN INTERIOR CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms