|

市場調査レポート

商品コード

1693718

北米の民間航空機用機内エンターテインメントシステム- 市場シェア分析、産業動向、成長予測(2025~2030年)North America Commercial Aircraft In-Flight Entertainment System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の民間航空機用機内エンターテインメントシステム- 市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 111 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

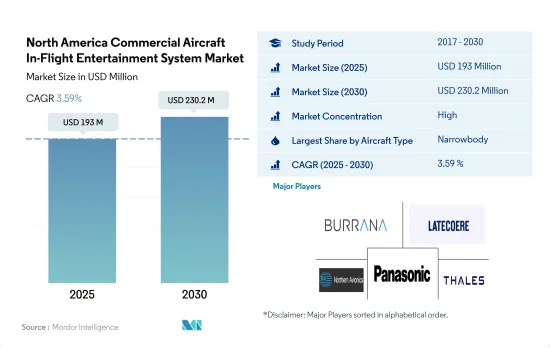

北米の民間航空機用機内エンターテインメントシステム市場規模は、2025年には1億9,300万米ドルと推定され、2030年には2億3,020万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは3.59%で成長する見込みです。

ナローボディ機への需要の高まりと、乗客の全体的な体験を重視する航空会社が、北米のIFE需要を促進すると予想される要因の一部です。

- 機内エンターテインメントは客室のインテリアに不可欠であり、乗客のフライト体験全体を決定づけるものです。米国では、ユナイテッド航空、アメリカン航空、サウスウエスト航空、デルタ航空が、現役の民間航空機に機内エンターテインメントシステムを導入しています。同様に、カナダではエア・カナダ、ウェストジェット、エア・トランザットも民間航空機に機内エンターテインメントシステムを導入しています。

- この地域では、パナソニックが、Astrova、NEXT、Xシリーズなど、多くのバージョンのIFEシステムを提供している主要OEMの1つです。北米のさまざまな航空会社は、客室クラスに応じて、LED、QLED、4K HDRスクリーンなど、さまざまな構成の12インチから18インチまでのスクリーンを使用しています。

- 国内航空需要の増加に伴い、ナローボディ機の市場はワイドボディ機よりも早く回復すると予想されています。また、737 MAXが2020年後半に運航を再開することも、ナローボディ機セグメントの成長を後押しする可能性があります。

- 納入機数では、2017~2022年にかけて、合計2,049機がこの地域の様々な航空会社によって調達されました。これら2,049機のうち、ナローボディ機が92%、ワイドボディ機が8%をそれぞれ占めました。新型民間旅客機の発注機数が増加していることが、市場の成長を後押ししています。例えば、2021年7月にユナイテッド航空はBoeing737マックスとAirbusA320を270機発注したと発表し、デルタ航空はBoeing737-10を100機発注し、さらに30機のオプションを付けた。このような発注は、北米の航空機客室市場におけるIFE需要を生み出し、2023~2030年の間に、合計2,885機の航空機が納入される見込みです。

ナローボディ機の台頭と、個別化された旅行体験を提供するために乗客を重視する航空会社が促進要因に

- 民間航空機部門は、主にナローボディ機の需要と北米における航空旅客数の増加に牽引され、大きな成長が見込まれます。航空会社の機体開発、燃費効率の高い航空機に対する需要の増加、航空産業によるゼロエミッション2050年目標の検討が民間航空機の需要を促進しています。2023年8月現在、この地域には1,474機のBoeing機と986機のAirbus機の供給残があります。これらの航空機のうち、米国だけで2,405機の受注残があります。したがって、米国は予測期間中により大きな成長を遂げることが予想されます。

- さらに、IFEシステムの需要は、個人化された旅行体験を求める乗客によって牽引されています。そのため、航空会社は強化されたIFEシステムに投資することで対応しています。IFEシステム市場は、新型航空機の調達や航空旅客数の増加に加え、燃料消費量やメンテナンスコストを削減し、航空会社の収益性を高めるために、従来の有線IFEシステムを無線IFEシステムに置き換える必要性によっても牽引されています。パナソニックやタレスなどのOEMは、従来のIFEシステムよりも重量の軽い座席内ディスプレイや客室内ディスプレイを開発しています。

- さらに、米国では、アラスカ航空、フロンティア航空、サウスウエスト航空、スピリット航空などの航空会社がIFEシステムを提供していないことが確認されました。これらの航空会社は、機内Wi-Fiを使用するために多少の追加料金を支払って、乗客自身のデバイスでエンターテインメントをストリーミングするオプションを選択しているからです。このような市場の開拓により、市場は2023~2030年にかけて1.92%の成長が見込まれます。

北米の民間航空機用機内エンターテインメントシステム市場動向

航空会社は燃費の良い新型機を大量発注しており、LCCの拡大が市場成長に寄与

- 2022年の北米における航空旅客輸送量は、米国が全体の80%を占めます。そのため、予測期間中、米国は他の北米諸国に比べて新型航空機の納入需要が最も高くなると予想されます。航空会社は増大する航空需要に対応するため機体規模の拡大を図っており、北米では新造航空機に対する大きな需要が発生する可能性があります。

- 北米では2017~2022年にかけて合計1,903機の新造旅客機が納入され、2023~2030年にかけてはさらに2,885機の新造ジェット機が納入される見込みです。納入された1,903機のジェット機のうち、1,748機がナローボディ機、155機がワイドボディ機でした。格安航空会社の拡大により、短距離路線での運航コストの低さや燃費の良さといった利点を持つ新世代のナローボディ機への需要が大きく伸びています。予測期間中に納入されるジェット機のうち、約2,678機がナローボディ機になると予想されます。これは、経済的で小型の航空機が好まれること、格安航空会社の成功、長距離ナローボディ機の導入など、いくつかの要因によるものです。北米の大手航空会社には、アメリカン航空、デルタ航空、ユナイテッド航空、サウスウエスト航空、エア・カナダ、アラスカ航空があります。これらの航空会社は合計で2,460機以上の航空機を保有し、その中にはナローボディ機とワイドボディ機の両方が含まれています。COVID-19パンデミックの間、ほとんどの大手航空会社は、古い機種の一部を退役させ、採算を維持するために燃費効率の良い新型機を調達しました。航空会社はより若い機体を維持しようとしているため、予測期間中は新型機の大量発注が予想されます。

経済成長、観光産業の増加、規制の緩和が北米の安定した航空旅客輸送量増加の原動力となっています。

- 広大な国土と多様な目的地を持つ北米は、国内線と国際線を利用する数百万人の旅客にとって人気の高い国です。経済の成長、航空券の値ごろ感、中産階級の台頭といった要因が、航空旅客数の大幅な増加に寄与しています。米国の2022年の航空旅客数は10億4,000万人に達し、2021年比で7%、2019年比で12%増加しました。2022年の1月から12月までに米国の航空会社が運んだ旅客数は8億5,300万人で、2021年の6億5,800万人、2020年の3億8,800万人を上回りました。カナダの航空会社が運んだ旅客数は2022年に1億700万人に達し、2021年の水準を6%上回りました。2022年のメキシコの航空旅客数は1億人で、2021年の水準と比較して7%の伸びを示しました。北米は、他の多くの国や地域よりも渡航制限が少なく、その期間も短いという恩恵を受けています。これは、大規模な自国市場の国内旅行と海外旅行を後押ししています。同地域の純利益は、2022年の99億米ドルから2023年には114億米ドルに増加すると予想されます。

- 航空旅客輸送量による需要に対応するため、この地域のさまざまな航空会社が新しい航空機の調達を計画しています。例えば、2023年に納入される世界の航空機の約3分の1は北米の航空会社が受領すると予想されています。同地域の航空機納入数は2022年にはすでに2019年の水準を上回っていたが、2023年にはさらに72機の増加が見込まれています。全体として、安定した航空旅行により、同地域の航空旅客輸送量は、2022年に記録された12億人に比べ、2030年には17億人増加すると予想されます。

北米の民間航空機用機内エンターテインメントシステム産業概要

北米の民間航空機用機内エンターテインメントシステム市場はかなり統合されており、上位5社で71.42%を占めています。この市場の主要企業は、Burrana、Latecoere、Northern Avionics srl、Panasonic Avionics Corporation、Thales Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 航空旅客輸送量

- 新規航空機納入数

- 一人当たりGDP(現行価格)

- 航空機メーカーの売上高

- 航空機受注残

- 受注総額

- 空港建設支出(継続中)

- 航空会社の燃料費

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 航空機タイプ

- ナローボディ

- ワイドボディ

- 国名

- カナダ

- 米国

- その他の北米地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Burrana

- Donica Aviation Engineering Co., Ltd

- IMAGIK International Corp.

- Latecoere

- Northern Avionics srl

- Panasonic Avionics Corporation

- Thales Group

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The North America Commercial Aircraft In-Flight Entertainment System Market size is estimated at 193 million USD in 2025, and is expected to reach 230.2 million USD by 2030, growing at a CAGR of 3.59% during the forecast period (2025-2030).

Rising demand for narrowbody aircraft and airlines focusing on passenger's overall experience are some of the factors that expected to drive the demand for IFE in North America

- In-flight entertainment is integral to cabin interiors and defines a passenger's entire flight experience. In the United States, United Airlines, American Airlines, Southwest Airlines, and Delta Air Lines have in-flight entertainment systems in their active fleet of commercial aircraft. Similarly, Air Canada, WestJet, and Air Transat operating in Canada also have in-flight entertainment systems in their active fleet of commercial aircraft.

- In the region, Panasonic is one of the major OEMs that offers many versions of the IFE system, including Astrova, NEXT, and X Series. Various airlines in North America use screens ranging from 12 inches to 18 inches with different configurations, such as LED, QLED, and 4K HDR screens, according to cabin class.

- As the demand for domestic aviation has increased, the market for narrowbody aircraft is anticipated to rebound faster than widebody aircraft. The 737 MAX's return to service in late 2020 may also boost the growth of the narrowbody aircraft segment.

- In terms of deliveries, during 2017-2022, a total of 2,049 aircraft were procured by various airlines in the region. Out of these 2,049 aircraft, narrowbody aircraft accounted for 92%, and widebody aircraft accounted for 8%, respectively. The rising number of aircraft orders of new commercial passenger aircraft has positively driven the growth of the market. For instance, in July 2021, United Airlines announced that it placed a 270-plane order for Boeing 737 Max and Airbus A320s, and Delta Airlines placed orders for 100 Boeing 737-10 aircraft, with an option for 30 more. Such orders are expected to generate demand for IFE in North America's aircraft cabin market, and during 2023-2030, a total of 2,885 aircraft are expected to be delivered.

Rise of narrowbody aircraft, and airlines focusing on passengers to provide personalized travel experiences are the driving factors

- The commercial aircraft segment is expected to experience significant growth, primarily driven by the demand for narrowbody aircraft and the growing number of air passengers in North America. Fleet development of the airlines, increase in demand for fuel-efficient aircraft, and the airline industry's consideration of the zero-emission 2050 goal fuel the demand for commercial aircraft. As of August 2023, the region has a backlog of 1,474 Boeing aircraft and 986 Airbus aircraft. Of these total aircraft, the US alone has 2,405 aircraft in backlog. Hence, the country is expected to witness larger growth during the forecast period.

- Additionally, the demand for IFE systems is driven by passengers as they seek personalized travel experiences. So, airlines are responding by investing in enhanced IFE systems. Besides the procurement of new aircraft and increasing air passenger traffic, the IFE system market is also driven by the need to replace conventional wired IFE systems with wireless IFE systems to reduce fuel consumption and maintenance costs and increase airline profitability. OEMs, such as Panasonic, Thales, and others, are developing in-seat and cabin displays that weigh less than the conventional IFE system.

- Furthermore, it was observed that in the US, airlines such as Alaska Airlines, Frontier Airlines, Southwest Airlines, and Spirit Airlines are not providing any IFE system because these airlines have opted for the option of streaming entertainment on the passenger's own device with some additional cost to use their in-flight Wi-Fi. Overall, with such developments, the market is expected to grow by 1.92% from 2023 to 2030.

North America Commercial Aircraft In-Flight Entertainment System Market Trends

Airlines are placing huge orders for new fuel-efficient aircraft, and the expansion of LCCs is contributing to the growth of the market

- The United States accounted for 80% of the total air passenger traffic in North America in 2022. Therefore, the United States is expected to generate the highest demand for new aircraft deliveries compared to other North American countries over the forecast period. Airlines are looking to expand their fleet size to cater to the growing demand for air travel, which may generate significant demand for new aircraft in North America.

- A total of 1,903 new passenger aircraft were delivered in North America between 2017 and 2022, and a further 2,885 new jets are expected to be delivered to the region during 2023-2030. Of the 1,903 jets delivered, 1,748 were narrowbody aircraft, and 155 were widebody aircraft. The expansion of low-cost carriers has resulted in huge demand for newer generation narrowbody aircraft, which offer advantages such as low operation costs and fuel efficiency in short-haul routes. It is expected that out of all the jets that will be delivered during the forecast period, around 2,678 of them will be narrowbody aircraft. This is due to several factors, including the preference for economical and smaller aircraft, the success of low-cost carriers, and the introduction of long-range narrowbody aircraft. Some of the major airlines in North America are American Airlines, Delta Air Lines, United Airlines, Southwest Airlines, Air Canada, and Alaska Airlines. These airlines together have a backlog of over 2,460 aircraft, including a mix of both narrowbody and widebody aircraft. During the COVID-19 pandemic, most major airlines retired some of their old aircraft models and procured new fuel-efficient aircraft to remain profitable. As the airlines try to maintain a younger fleet, large orders for new aircraft are expected during the forecast period.

Rising economy, increase in tourism industry and ease of restrictions are the driving factors for a consistent air passenger traffic growth in North America

- North America's vast landmass and diverse destinations make it a popular choice for millions of passengers who choose to fly both domestically and internationally. Factors such as a growing economy, increased affordability of air travel, and a rising middle class have contributed to a significant uptick in air passenger traffic. Air passenger traffic in the United States reached 1.04 billion in 2022, up by 7% compared to 2021 and 12% compared to 2019. In 2022, from January through December, US airlines carried 853 million passengers, up from 658 million in 2021 and 388 million in 2020. The total number of passengers carried by airlines in Canada reached 107 million in 2022, surpassing the levels in 2021 by 6%. In 2022, Mexico had 100 million air passenger traffic, representing a 7% growth compared to its 2021 traffic levels. North America has benefitted from fewer and shorter-lasting travel restrictions than many other countries and regions. This has boosted domestic travel in the large home market, as well as international travel. Net profits in the region are expected to rise from USD 9.9 billion in 2022 to USD 11.4 billion in 2023.

- To cater to the demand driven by air passenger traffic, various airlines in the region are planning to procure new aircraft. For instance, around one-third of global aircraft deliveries in 2023 were anticipated to be received by various carriers in North America. Although the region's aircraft deliveries were already above 2019 levels in 2022, they were expected to grow by an additional 72 units in 2023. Overall, with consistent air travel, the region's air passenger traffic is expected to increase by 1.7 billion in 2030 compared to 1.2 billion recorded in 2022.

North America Commercial Aircraft In-Flight Entertainment System Industry Overview

The North America Commercial Aircraft In-Flight Entertainment System Market is fairly consolidated, with the top five companies occupying 71.42%. The major players in this market are Burrana, Latecoere, Northern Avionics srl, Panasonic Avionics Corporation and Thales Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 New Aircraft Deliveries

- 4.3 GDP Per Capita (current Price)

- 4.4 Revenue Of Aircraft Manufacturers

- 4.5 Aircraft Backlog

- 4.6 Gross Orders

- 4.7 Expenditure On Airport Construction Projects (ongoing)

- 4.8 Expenditure Of Airlines On Fuel

- 4.9 Regulatory Framework

- 4.10 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Aircraft Type

- 5.1.1 Narrowbody

- 5.1.2 Widebody

- 5.2 Country

- 5.2.1 Canada

- 5.2.2 United States

- 5.2.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Burrana

- 6.4.2 Donica Aviation Engineering Co., Ltd

- 6.4.3 IMAGIK International Corp.

- 6.4.4 Latecoere

- 6.4.5 Northern Avionics srl

- 6.4.6 Panasonic Avionics Corporation

- 6.4.7 Thales Group

7 KEY STRATEGIC QUESTIONS FOR COMMERCIAL AIRCRAFT CABIN INTERIOR CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms