|

市場調査レポート

商品コード

1693512

ベトナムの特殊肥料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Vietnam Specialty Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ベトナムの特殊肥料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 177 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

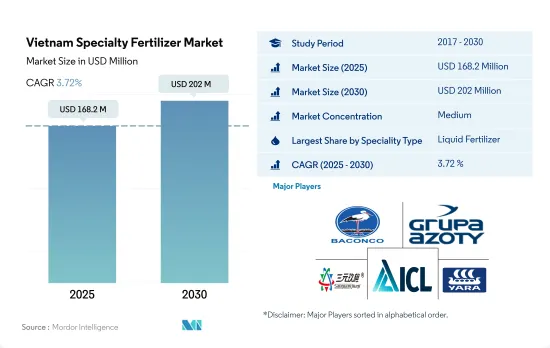

ベトナムの特殊肥料市場規模は2025年に1億6,820万米ドルと推定され、2030年には2億200万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは3.72%で成長する見込みです。

高効率肥料への需要の高まりが特殊肥料の需要を促進

- ベトナムの特殊肥料市場では、水溶性肥料が2022年に6,590万米ドルに達することが確認されています。水溶性肥料は、農家が植物の成長サイクルに合わせて栄養素の濃度を調整できる柔軟性を提供します。植物の根の近くに可溶性肥料を施用することで、農家は生育期全体にわたって広い面積に集中的に施肥するよりもコストを節約できます。こうした利点がベトナムにおける水溶性肥料の需要を後押ししています。

- 2020年のベトナム特殊肥料の市場規模は1,510万米ドル減少したが、これは主にCOVID-19の封鎖による国際貿易の混乱が原因です。この減少は前年の動向に続くものでした。さらに、市場は気温の変動、不規則な降雨、干ばつなどの課題に直面しました。

- ベトナムの特殊肥料市場は液体肥料が支配的です。作物の品質向上、輸出規格への適合、精密農業の採用が重視されるようになり、この分野の園芸作物の金額は2023年から2030年にかけてCAGR 4.6%を記録すると予測されます。

- コントロール・リリース肥料(CRF)とスロー・リリース肥料(SRF)は、一定のペースで徐々に栄養素を放出し、土壌条件の影響を受けながらシーズンを通して作物のニーズに応えます。CRFとSRFのこのユニークな特徴は、肥料使用量と環境悪化を減らすだけでなく、農家に経済的利益をもたらします。その結果、これらの肥料の市場は2023年から2030年にかけて大きく成長する見込みです。

ベトナムの特殊肥料市場動向

ベトナム政府は生産コストを削減する政策を推進しており、これにより畑作物の栽培面積が増加すると予想されます。

- ベトナムは畑作物に多くの土地を割り当てており、米、トウモロコシ(トウモロコシ)、その他の主食が主な対象です。多様な気候と地形により、ベトナムでは様々な作物を栽培することができます。しかし、調査期間中に畑作物の栽培面積は6.6%減少しました。

- 米は主食であることから、ベトナムの主要な畑作物の中心を占めています。総栽培面積の81.8%を占め、トウモロコシが10.2%で続きます。2022年、ベトナムのコメ生産量は約4,390万トンに達し、世界有数の輸出国としての地位を固めました。

- ベトナムは、冬から春(早場)、夏から秋(中盤)、秋から冬(長い雨季)の3つの明確な作期を経験します。ベトナムの主要な農業拠点は、紅河デルタ、メコン河デルタ、南部テラスです。米は3地域すべてで主要作物となっており、メコンデルタだけでベトナムの米輸出の半分を占めています。

- ベトナム政府は、生産コストの削減を目的とした政策を実施しています。これらの施策には、肥料や農薬の使用量の削減、地元産肥料の普及、畑作物の生産性、品質、収益性の向上における肥料の役割の強調などが含まれます。栄養不足による不作が増加していることや、植物の矮小化に対抗するために高効率肥料が必要とされていることも、ベトナムの肥料市場を強化している要因です。

窒素は様々な畑作物に必要不可欠な栄養素であり、その施用量は顕著に増加しています。

- 2022年、ベトナムの畑作物の一次養分の平均施用量は1ヘクタール当たり123.94kgでした。この分野では、穀物・穀類が肥料の最大消費者に浮上しました。特に、米、小麦、トウモロコシはベトナムの穀物作物の中でトップであり、同年の一次養分の平均施用量はそれぞれ155.49 kg/ha、228.90 kg/ha、148.49 kg/haでした。

- 一次養分の中では窒素がトップで、畑作物の平均施用量は221.43kg/ヘクタールでした。このように窒素が重視されるのは、耕起、葉面積の開発、粒の形成、充填、タンパク質の合成など、作物の成長のさまざまな側面を強化する役割に由来します。窒素はまた、収量と品質の両方に好影響を与えます。小麦が492.06kg/haで最も高い窒素施用量の栄冠に輝き、次いで米が328.04kg/haでした。

- ベトナムのVinh Phuc省では、土壌のかなりの部分が劣化に苦しんでおり、有機物が少なく、全利用可能窒素が0.08%以下、全リンが0.04%以下、全カリウムが1.0%以下であることが特徴です。さらに、利用可能リンは10ppmを下回っています。こうした欠乏がベトナムの肥料消費量を急増させ、1969年の49.2kg/haから2018年には415.3kg/haに増加し、CAGRは6.71%となっています。

- ベトナムの人口の43%が農業に従事しているにもかかわらず、同部門のGDPへの貢献はわずかで、約12.36%にすぎないです。しかし、国家が農業の安定を目指す中、肥料の需要は増加の一途をたどっており、2023年から2030年にかけてのベトナムの肥料市場の成長を後押ししています。

ベトナムの特殊肥料産業の概要

ベトナムの特殊肥料市場は適度に統合されており、上位5社で60.32%を占めています。この市場の主要企業は以下の通り。 Baconco, Grupa Azoty S.A.(Compo Expert), Hebei Sanyuanjiuqi Fertilizer, ICL Group Ltd and Yara International ASA(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 主要作物の作付面積

- 畑作物

- 園芸作物

- 平均養分施用率

- 微量栄養素

- 畑作物

- 園芸作物

- 一次栄養素

- 畑作物

- 園芸作物

- 二次多量栄養素

- 畑作物

- 園芸作物

- 微量栄養素

- 灌漑農地

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- スペシャリティタイプ

- CRF

- ポリマーコート

- ポリマー硫黄コーティング

- その他

- 液体肥料

- SRF

- 水溶性

- CRF

- 施肥モード

- 施肥

- 葉面散布

- 土壌

- 作物タイプ

- 畑作物

- 園芸作物

- 芝・観賞用

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Baconco

- Grupa Azoty S.A.(Compo Expert)

- Haifa Group

- Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- ICL Group Ltd

- Yara International ASA

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Vietnam Specialty Fertilizer Market size is estimated at 168.2 million USD in 2025, and is expected to reach 202 million USD by 2030, growing at a CAGR of 3.72% during the forecast period (2025-2030).

The rising demand for highly efficient fertilizers is driving the demand for specialty fertilizers

- The Vietnamese specialized fertilizer market witnessed water-soluble fertilizers reaching a value of USD 65.9 million in 2022. These fertilizers offer farmers the flexibility to adjust nutrient concentrations as per the evolving needs of plants during their growth cycle. By applying soluble fertilizers near the plant's root zone, farmers can save costs compared to intensive fertilization across a large area for the entire growing season. These advantages are fueling the demand for water-soluble fertilizers in Vietnam.

- The year 2020 saw the Vietnam specialty fertilizer market value decline by USD 15.1 million, primarily due to disruptions in international trade caused by the COVID-19 lockdown. This decline followed a trend from the previous year. Additionally, the market faced challenges from temperature fluctuations, erratic rainfall, and droughts.

- Liquid fertilizers dominate the specialty fertilizer market in Vietnam. With a growing emphasis on improving crop quality, meeting export standards, and adopting precision farming, the value of horticulture crops in this segment is projected to register a CAGR of 4.6% from 2023 to 2030.

- Control-release fertilizers (CRFs) and slow-release fertilizers (SRFs) gradually release nutrients at a consistent pace, catering to crop needs throughout the season, influenced by soil conditions. This unique feature of CRFs and SRFs not only reduces fertilizer usage and environmental degradation but also brings economic benefits to farmers. Consequently, the market for these fertilizers is poised for significant growth during 2023-2030.

Vietnam Specialty Fertilizer Market Trends

The Vietnamese government has been promoting policies to reduce production costs, which is expected to increase the cultivation area under field crops

- Vietnam allocates significant land to field crops, with major focuses on rice, maize (corn), and other staples. Owing to its diverse climate and topography, Vietnam can cultivate a wide array of crops. However, the country witnessed a 6.6% decline in the area dedicated to field crop cultivation during the study period.

- Rice takes center stage as Vietnam's primary field crop, given its status as a staple food. It dominates the cultivation landscape, accounting for 81.8% of the total area, followed by corn at 10.2%. In 2022, Vietnam's rice production reached around 43.9 million metric tons, solidifying its position as a leading global exporter.

- Vietnam experiences three distinct cropping seasons: winter-spring (early season), summer-autumn (midseason), and autumn-winter (longer rainy season). Key agricultural hubs in the country encompass the Red River Delta, Mekong River Delta, and Southern Terrace. Rice stands as the primary crop across all three regions, with the Mekong Delta alone contributing to half of Vietnam's rice exports.

- The Vietnamese government has implemented policies aimed at reducing production costs. These measures include cutting back on fertilizer and pesticide usage, promoting locally-sourced fertilizers, and emphasizing their role in enhancing field crop productivity, quality, and profitability. The increase in crop failures due to nutrient deficiencies and the need for high-efficiency fertilizers to combat plant dwarfism are additional factors bolstering Vietnam's fertilizers market.

Nitrogen is a vital nutrient required for a range of field crops, and its application is notably higher

- In 2022, field crops in Vietnam saw an average application rate of 123.94 kg per hectare for primary nutrients. Within this segment, grains and cereals emerged as the largest consumers of fertilizers. Notably, rice, wheat, and maize stood out as the top cereal crops in Vietnam, with average primary nutrient application rates of 155.49 kg/ha, 228.90 kg/ha, and 148.49 kg/ha, respectively, in the same year.

- Among the primary nutrients, nitrogen took the lead, with an average application rate of 221.43 kg/hectare for field crops. This emphasis on nitrogen stems from its role in bolstering various aspects of crop growth, such as tillering, leaf area development, grain formation, filling, and protein synthesis. It also positively impacts both yield and quality. Wheat took the crown for the highest nitrogen application rate at 492.06 kg/ha, followed by rice at 328.04 kg/ha.

- In Vietnam's Vinh Phuc province, significant portions of soil suffer from degradation, characterized by low organic matter, total available nitrogen below 0.08%, total phosphorus below 0.04%, and total potassium below 1.0%. Additionally, available phosphorus falls below 10 ppm. These deficiencies have contributed to a surge in fertilizer consumption in Vietnam, rising from 49.2 kg/ha in 1969 to 415.3 kg/ha by 2018, marking an average annual growth rate of 6.71%.

- Despite 43% of Vietnam's population being involved in agriculture, the sector's contribution to the country's GDP remains modest, accounting for only about 12.36%. However, as the nation strives for agricultural stability, the demand for fertilizers continues to rise, propelling the growth of Vietnam's fertilizers market during 2023-2030.

Vietnam Specialty Fertilizer Industry Overview

The Vietnam Specialty Fertilizer Market is moderately consolidated, with the top five companies occupying 60.32%. The major players in this market are Baconco, Grupa Azoty S.A. (Compo Expert), Hebei Sanyuanjiuqi Fertilizer Co., Ltd., ICL Group Ltd and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Speciality Type

- 5.1.1 CRF

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 SRF

- 5.1.4 Water Soluble

- 5.1.1 CRF

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Baconco

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Haifa Group

- 6.4.4 Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- 6.4.5 ICL Group Ltd

- 6.4.6 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms