中国の特殊肥料の市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

China Specialty Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 191 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693508

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

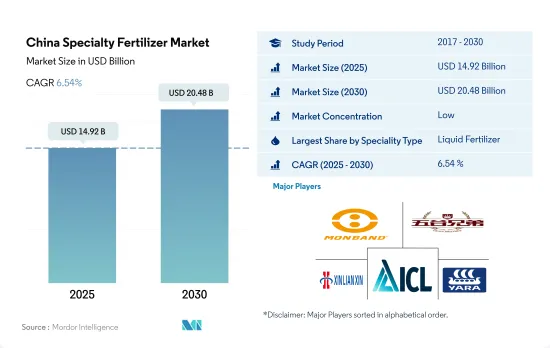

中国の特殊肥料市場規模は2025年に149億2,000万米ドルと推定・予測され、2030年には204億8,000万米ドルに達し、予測期間中(2025~2030年)のCAGRは6.54%で成長すると予測されます。

特定の栄養素を効率的に供給し、施肥回数を減らすことが市場を牽引する可能性

- 特殊肥料市場は、2022年の中国肥料市場の市場規模の約3.8%を占めています。特殊肥料の市場シェアがわずかなのは、効率に関する農業従事者の認識が低いことと、従来の特殊肥料に比べてコストが高いことが主要原因です。

- 水溶性肥料は2022年の中国の特殊肥料市場規模の51.0%を占めました。水溶性肥料が優勢なのは、灌漑農業の普及と灌漑設備の技術進歩によるところが大きいです。灌漑は、同国の小規模灌漑システムで最も普及している施用方法です。これが2023~2030年の水溶性肥料市場を牽引すると考えられます。

- 液体肥料は2022年の中国の特殊肥料市場規模の48.8%を占めます。液体肥料は植物に吸収されやすく、灌漑や散布と併用することで人件費を削減できます。葉面散布は液体肥料で最もよく使われる方法です。

- 放出制御肥料は中国の特殊肥料市場数量で次に大きな市場シェアを占め、2022年には0.1%を占めます。放出制御肥料の市場シェアは主に、最大6ヶ月間養分を供給できる可能性があることによる。栄養素の損失も非常に少ないです。しかし、農業従事者の意識の高まりは、予測期間中に放出制御肥料の市場シェアを高める可能性があります。

- 最近の動向では、中国の水溶性肥料産業は、肥料の使用量、水、労働力、コストを削減し、収量と品質を向上させるという利点があるため、近代農業開発のための有利な施策と多額の投資を伴って活況を呈しています。

中国の特殊肥料の市場動向

栽培面積の拡大は、食糧需要の増加と主食の自給自足を目指す国の目標が原動力となっています。

- 中国の畑作物の栽培面積は、2018年の1億2,660万ヘクタールから2022年には1億2,780万ヘクタールへとわずかに拡大し、全国の総耕作地の70.8%を占めます。2022年には、トウモロコシが34.2%で最大のシェアを占め、コメが23.6%、小麦が18.3%でこれに続きます。このような耕作面積の増加は、国内の肥料需要を押し上げると予測されます。

- 中国は通常、畑作物の生産を春夏(4月~9月)と冬の2つの季節に分ける。春作には早生トウモロコシ、早生コメ、早生小麦、綿花が含まれ、冬作は冬小麦と菜種が中心です。しかし、米とトウモロコシは中国の農業の中で優先され、中国の穀物生産量の3分の1を占めています。世界有数のコメ生産国である中国は、2022年には3,000万ヘクタールを稲作に充て、2億1,000万トンの豊作を見込んでいます。主要な米生産地域は、黒龍江省、湖南省、江西省、湖北省、江蘇省、四川省、広西チワン族自治区、広東省、クラウド南省にまたがっています。2022~23年の中国のトウモロコシ生産量は、豊作に支えられ、前年比460万トン増の2億7,720万トンに達すると予測されています。トウモロコシの主産地は東北部の黒龍江省、吉林省、内モンゴル自治区です。

- 中国の作付けは春が中心だが、6月と7月の暑い時期にはいくつかの課題に直面します。米は何百万人もの人々の主食であるため、この地域の高温と限られた降雨量は土壌のミネラル枯渇を悪化させ、肥料の施用量を増やす必要があります。このような乾燥状態は、作物の収量も低下させています。

世界の農地からの亜酸化窒素排出量の約28%は、中国の農地から排出されています。

- 一次栄養素は、植物の酵素活性などの生化学的プロセスを改善し、植物細胞の成長を促進します。一次栄養素の欠乏は、植物の健康、開発、作物生産高に影響を与える可能性があります。2022年の畑作物における窒素、カリウム、リンの平均施用量は159.9kg/ヘクタールでした。畑作物における一次養分の平均施用量は、窒素65.23%、リン28.07%、カリウム6.68%でした。

- 窒素は植物の代謝に不可欠であり、葉緑素やアミノ酸の構成成分であるため、一次養分では第一位です。窒素の平均施用量は279.65kg/ヘクタールでした。次いでカリが105.3kg/ヘクタール、リンが94.9kg/ヘクタールであった(2022年)。窒素とリンによる地表水と地下水の汚染は、肥料散布量に関する農業従事者への不適切なアドバイスの結果と考えられています。世界の農地からの亜酸化窒素排出量の約28%は、中国の農地からのものです。

- 2022年、平均養分施用率が最も高い作物は、綿(255.41kg/ヘクタール)、小麦(232.25kg/ヘクタール)、トウモロコシ(198.44kg/ヘクタール)、米(157.76kg/ヘクタール)です。2022年の綿花生産量は640万トンで、中国は世界最大の綿花生産国、消費国、輸入国となっています。世界で消費される綿花の約20%が中国で生産され、その84%が新疆ウイグル自治区で生産されています。

- 人口増加の需要を満たすには、農作物生産の拡大が不可欠であり、その結果、畑作物への一次栄養素の施用は2023~2030年にかけて増加すると予想されます。

中国の特殊肥料産業概要

中国の特殊肥料市場はセグメント化されており、上位5社で5.01%を占めています。この市場の主要企業は、Hebei Monband Water Soluble Fertilizer、Hebei Woze Wufeng Biological Technology、Henan XinlianXin Chemicals Group Company Limited、ICL Group Ltd、Yara International ASAなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 主要作物の作付面積

- 畑作物

- 園芸作物

- 平均養分施用率

- 微量栄養素

- 畑作物

- 園芸作物

- 一次栄養素

- 畑作物

- 園芸作物

- 二次多量栄養素

- 畑作物

- 園芸作物

- 微量栄養素

- 灌漑農地

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- スペシャリティタイプ

- CRF

- ポリマーコート

- ポリマー硫黄コーティング

- その他

- 液体肥料

- SRF

- 水溶性

- CRF

- 施肥モード

- 施肥

- 葉面散布

- 土壌

- 作物タイプ

- 畑作物

- 園芸作物

- 芝・観賞用

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Grupa Azoty S.A.(Compo Expert)

- Haifa Group

- Hebei Monband Water Soluble Fertilizer Co. Ltd

- Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- Hebei Woze Wufeng Biological Technology Co., Ltd

- Henan XinlianXin Chemicals Group Company Limited

- ICL Group Ltd

- Sociedad Quimica y Minera de Chile SA

- Yara International ASA

- Zouping Hongyun BIoTechnology Co., Ltd.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

The China Specialty Fertilizer Market size is estimated at 14.92 billion USD in 2025, and is expected to reach 20.48 billion USD by 2030, growing at a CAGR of 6.54% during the forecast period (2025-2030).

Efficiency in providing particular nutrients and reducing the number of fertilizations may drive the market

- The specialty fertilizer market accounted for about 3.8% of the market volume of the Chinese fertilizer market in 2022. The minimal market share of the specialty fertilizers market is majorly attributed to the less awareness among farmers regarding efficiency and higher cost compared to conventional specialty fertilizers.

- Water-soluble fertilizers accounted for 51.0% of the Chinese specialty fertilizer market volume in 2022. The dominance of water-soluble fertilizers is majorly due to the growing adoption of irrigation agriculture and technical advancements in irrigation equipment. Fertigation is the most popular application mode used in the country's micro irrigation systems. This will drive the soluble fertilizers market during 2023-2030

- Liquid fertilizers accounted for 48.8% of the Chinese specialty fertilizer market volume in 2022. Liquid fertilizers are more easily absorbed by plants and can be used with irrigation or spraying by reducing labor costs. Foliar is the most popular method used by the liquid fertilizer application.

- Controlled-release fertilizers accounted for the next largest market share in the Chinese specialty fertilizer market volume, accounting for 0.1% in 2022. The market share of controlled-release fertilizers is mainly due to their potential to provide nutrients for up to six months. The loss of nutrients is also very low. However, rising awareness among farmers can increase the market share of controlled-release fertilizers in the forecast period.

- In recent years, the soluble fertilizer industry in China has boomed because of its advantages in reducing fertilizer usage, water, labor, and cost, and increasing yield and quality, accompanied by favorable policies for modern agriculture development and substantial investment.

China Specialty Fertilizer Market Trends

The expansion of the cultivation area is driven by increasing demand for food and the country's goal to achieve self-sufficiency in staple food

- China's cultivation area for field crops expanded marginally from 126.6 million hectares in 2018 to 127.8 million hectares in 2022, representing 70.8% of the nation's total cultivated land. In 2022, corn claimed the largest share at 34.2%, trailed by rice and wheat at 23.6% and 18.3% respectively. This uptick in cultivation area is projected to drive up fertilizer demand in the country.

- China typically divides its field crop production into two seasons: spring/summer (April-September) and winter. Spring crops encompass early corn, early rice, early wheat, and cotton, while winter crops focus on winter wheat and rapeseed. Rice and corn, however, take precedence in China's agricultural landscape, accounting for a third of the nation's grain output. As the world's leading rice producer, China dedicated 30 million hectares to rice farming in 2022, yielding a bountiful 210 million tonnes. Key rice-growing regions span Heilongjiang, Hunan, Jiangxi, Hubei, Jiangsu, Sichuan, Guangxi, Guangdong, and Yunnan. China's corn production for 2022-23 was projected to hit 277.2 million tonnes, a 4.6 million-tonne increase from the previous year, buoyed by a successful harvest. The primary corn belts lie in the northeastern provinces of Heilongjiang, Jilin, and Inner Mongolia.

- While spring dominates China's cropping calendar, it faces some challenges during the hotter months of June and July. Given rice's status as a dietary staple for millions, the region's high temperatures and limited rainfall exacerbate mineral depletion in the soil, necessitating higher fertilizer application. These arid conditions can also curtail crop yields.

About 28% of global nitrous oxide emissions from croplands are from China's agricultural lands

- Primary nutrients improve biochemical processes like enzyme activity in plants and promote plant cell growth. Primary nutrient deficiencies can impact plant health, development, and crop production output. The average application rate of nitrogen, potassium, and phosphorus collectively in field crops was 159.9 kg/hectare in 2022. The average primary nutrient application in field crops included 65.23% nitrogen, 28.07% phosphorous, and 6.68% potassium.

- Nitrogen ranks first in primary nutrients, as it is essential for plant metabolism and is a component of chlorophyll and amino acids. Nitrogen had an average application rate of 279.65 kg/hectare. This was followed by potash at 105.3 kg/hectare and phosphorous at 94.9 kg/hectare in 2022. The contamination of surface and groundwater with nitrogen and phosphorus has been considered a result of inadequate advice given to farmers regarding fertilizer application rates. About 28% of global nitrous oxide emissions from croplands are from China's agricultural lands.

- In 2022, the crops with the highest average nutrient application rates were cotton (255.41 kg/hectare), wheat (232.25 kg/hectare), corn (198.44 kg/hectare), and rice (157.76 kg/hectare). In 2022, cotton production amounted to 6.4 million metric tons, making China the world's largest producer, consumer, and importer of cotton. Around 20% of the cotton consumed worldwide is produced in China, and 84% of that production comes from Xinjiang.

- To meet the demands of a growing population, boosting crop production is essential; as a result, the application of primary nutrients in field crops is expected to grow from 2023 to 2030.

China Specialty Fertilizer Industry Overview

The China Specialty Fertilizer Market is fragmented, with the top five companies occupying 5.01%. The major players in this market are Hebei Monband Water Soluble Fertilizer Co. Ltd, Hebei Woze Wufeng Biological Technology Co., Ltd, Henan XinlianXin Chemicals Group Company Limited, ICL Group Ltd and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Speciality Type

- 5.1.1 CRF

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 SRF

- 5.1.4 Water Soluble

- 5.1.1 CRF

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Grupa Azoty S.A. (Compo Expert)

- 6.4.2 Haifa Group

- 6.4.3 Hebei Monband Water Soluble Fertilizer Co. Ltd

- 6.4.4 Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- 6.4.5 Hebei Woze Wufeng Biological Technology Co., Ltd

- 6.4.6 Henan XinlianXin Chemicals Group Company Limited

- 6.4.7 ICL Group Ltd

- 6.4.8 Sociedad Quimica y Minera de Chile SA

- 6.4.9 Yara International ASA

- 6.4.10 Zouping Hongyun Biotechnology Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 191 Pages

- 納期

- 2~3営業日