アフリカの特殊肥料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Africa Specialty Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 197 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693539

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

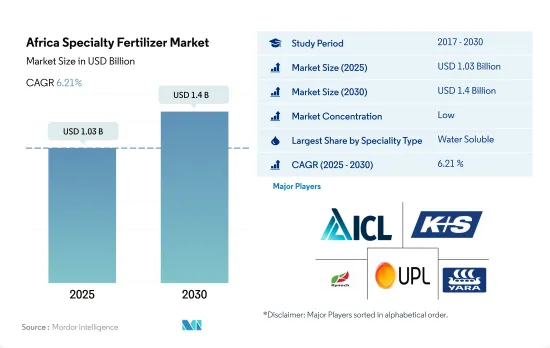

アフリカの特殊肥料市場規模は2025年に10億3,000万米ドルと推定され、2030年には14億米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは6.21%で成長する見込みです。

従来の肥料よりも特殊肥料を使用した方が様々な利点があるため、市場の成長が促進されると予想されます。

- 2022年には、放出制御肥料(CRF)が特殊肥料市場で7.4%のシェアを占めていました。CRFの着実な成長は、従来の肥料に対する明確な優位性と、効率的な農法に対する意識の高まりに起因しています。CRFは長期間にわたって徐々に養分を放出するため、植物への安定した養分供給を保証します。このため、養分の浪費が抑えられるだけでなく、従来の肥料にありがちな溶出や蒸発のリスクも最小限に抑えられます。

- 水溶性肥料の市場シェアは47.8%で、2022年の特殊肥料市場で第2位となりました。水溶性肥料の使用は、健全な植物の栽培に必要な水と肥料の両方を削減する可能性を示しています。

- 液体肥料市場は、灌漑システムの進歩や、水耕栽培やアクアポニックスのような高度な栽培技術の採用の高まりに後押しされ、成長を遂げようとしています。液体肥料の市場価値は、2023年から2030年の間にCAGR 5.8%になると予測されています。

- 緩効性肥料の採用は、農家に経済的なメリットだけでなく、節水、窒素の揮発・溶出の防止、肥料取り扱いの労力軽減といった環境面でのメリットももたらします。こうした要因により、2023~20230年の間に緩効性肥料の市場価値は5.4%成長すると予想されます。

- 正確な栄養分の放出、施肥量の削減、農家にとっての経済的メリットなど、特殊肥料の利点を考えると、特殊肥料市場は今後数年間で成長する態勢を整えています。

政府の取り組みと生産性向上に注力する農家が市場の成長を後押しする見込み

- 2022年、ナイジェリアはアフリカの特殊肥料市場で27.0%の圧倒的な金額シェアを占めました。同国の農業部門は、複雑な土地所有権の問題、不十分な灌漑インフラ、気候変動の悪影響、最先端の農業技術の段階的導入といった課題に直面しながらも、政府のイニシアティブに支えられて市場の成長を遂げてきました。これらには、農業振興政策(APP)、ナイジェリア・アフリカ貿易投資促進プログラム、国家農業技術・イノベーション計画(NATIP)、アンカー借入人プログラム(ABP)などがあり、いずれも農業生産性の向上に役立っています。

- 南アフリカは、大陸で最も先進的で生産性が高く、多様性に富んだ農業地域です。2022年には、その堅調な農業部門がアフリカの特殊肥料市場全体の37.0%という大きなシェアを占めていました。同市場は予測期間中にCAGR 6.7%を記録すると予想されます。このような成長が予想されるのは、より効率的な肥料ソリューションを採用することで、長引く干ばつや猛暑などの気候関連リスクの影響を軽減する必要性が高まっていることが主な要因です。

- アフリカの特殊肥料市場は、人口の急増、耕地の減少、既存の農地での収量向上が急務であること、地域全体で農業生産性を向上させる取り組みが行われていることなどが背景にあり、拡大が見込まれています。このため、2023年から2030年までのCAGRは6.0%になると予測されます。

アフリカの特殊肥料市場の動向

国内需要の高まりにより、近い将来、農業生産は倍増すると思われます。

- アフリカの農業生態系ゾーンは、年2回の降雨がある密生した熱帯雨林から、降雨量の少ない乾燥した砂漠まで多岐にわたる。この地域の主要な畑作作物には、トウモロコシ、ソルガム、小麦、米などがあります。2022年には、これらの作物の栽培面積は2億2,480万ヘクタールに達し、この地域の農地の95%以上を占めています。価格抑制につながるトウモロコシの余剰在庫を受けて、南アフリカのトウモロコシ農家は2018-19年シーズンに作付けを10%縮小し、210万ヘクタールとしました。その結果、同国のトウモロコシ生産量は1,300万トンから1,200万トンに11%減少し、輸出量は250万トンから100万トンに減少しました。このシフトにより、生産者は油糧作物、特に大豆により多くの畑を割り当てるようになり、その結果2018-2019年のアフリカ全体のトウモロコシ栽培は減少しました。

- ナイジェリアがアフリカ最大のソルガム生産国としてトップに立ち、僅差でエチオピアが続きます。ソルガムは全穀物生産量の50%を占め、ナイジェリアの穀物作付面積の約45%を占めています。ソルガムきびは干ばつと湛水耐性で知られ、多様な土壌条件で生育します。こうした特性から、ソルガムきびはアフリカの乾燥地帯における主食作物として位置づけられており、食糧安全保障と所得保障の両方が確保されています。

- ケニア、ソマリア、エチオピアの大部分は、深刻な食糧不足の危機と闘っています。過去10年間で、アフリカの農業と耕作地が拡大し続けているにもかかわらず、食料輸入への支出は3倍近くになっています。

菜種は窒素消費量が最も多い作物

- 菜種はカリウムとリンの施用率が最も高く、それぞれ162.4kg/ヘクタールと281.7kg/ヘクタールを占める。一方、アフリカの畑作物の平均窒素施用量は364.9kg/ヘクタールです。2022年には、アフリカの畑作物は一次養分消費量全体の87.1%を占め、55万6,100トンに達しました。この優位性は、畑作物専用の広大な土地面積に起因しています。具体的には、これらの作物における窒素、リン、カリウムの平均養分施用量は、それぞれ223.2 kg/ha、125.3 kg/ha、155.3 kg/haでした。

- ナイジェリアのギニアサバンナは、トウモロコシ生産に適した環境条件を提供しています。しかし、このような可能性があるにもかかわらず、この地域の農家は低い収量に苦しんでいます。主な原因は、土地利用の激化による土壌の劣化と養分の枯渇(主に窒素)です。畑作物は、耕起、葉面積の拡大、穀粒の形成、充填、タンパク質合成の促進など、窒素には複数の利点があるため、窒素施用が優先されます。窒素はまた、穀物の収量と品質の向上にも重要な役割を果たしています。

- 一次栄養素は作物の生育に不可欠であり、土壌の枯渇や窒素の溶出が懸念されることから、一次栄養素の施用率は今後数年間で大きく伸びると予想されます。

アフリカの特殊肥料産業の概要

アフリカの特殊肥料市場は断片化されており、上位5社で29.76%を占めています。この市場の主要企業は以下の通りです。 ICL Group Ltd, K+S Aktiengesellschaft, Kynoch Fertilizer, UPL Limited and Yara International ASA(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 主要作物の作付面積

- 畑作物

- 園芸作物

- 平均養分施用率

- 微量栄養素

- 畑作物

- 園芸作物

- 一次栄養素

- 畑作物

- 園芸作物

- 二次多量栄養素

- 畑作物

- 園芸作物

- 微量栄養素

- 灌漑農地

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- スペシャリティタイプ

- CRF

- ポリマーコート

- ポリマー硫黄コーティング

- その他

- 液体肥料

- SRF

- 水溶性

- CRF

- 施肥モード

- 施肥

- 葉面散布

- 土壌

- 作物タイプ

- 畑作物

- 園芸作物

- 芝・観賞用

- 生産国

- ナイジェリア

- 南アフリカ

- その他のアフリカ

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Gavilon South Africa(MacroSource, LLC)

- Haifa Group

- ICL Group Ltd

- K+S Aktiengesellschaft

- Kynoch Fertilizer

- UPL Limited

- Yara International ASA

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92604

The Africa Specialty Fertilizer Market size is estimated at 1.03 billion USD in 2025, and is expected to reach 1.4 billion USD by 2030, growing at a CAGR of 6.21% during the forecast period (2025-2030).

The various advantages of using specialty fertilizers over conventional fertilizers is expected to bolster the growth of the market

- In 2022, controlled-release fertilizers (CRFs) held a 7.4% share of the specialty fertilizer market. The steady growth of CRFs can be attributed to their distinct advantages over traditional fertilizers and the increasing awareness of efficient agricultural practices. CRFs gradually release nutrients over an extended period, ensuring a consistent nutrient supply to plants. This not only reduces nutrient wastage but also minimizes the risk of leaching or evaporation, which is common with conventional fertilizers.

- Water-soluble fertilizers, with a 47.8% market share, ranked second in the specialty fertilizer market in 2022. The use of water-soluble fertilizers has shown potential in reducing both water and fertilizer requirements for cultivating healthy plants.

- The liquid fertilizer market is poised for growth, propelled by advancements in irrigation systems and the rising adoption of advanced cultivation techniques such as hydroponics and aquaponics. The market value of liquid fertilizers is projected to witness a CAGR of 5.8% during 2023-2030.

- The adoption of slow-release fertilizers offers farmers not only economic benefits but also environmental advantages, such as water conservation, prevention of nitrogen volatilization and leaching, and reduced labor in fertilizer handling. These factors are expected to drive a 5.4% growth in the market value of slow-release fertilizers during 2023-20230.

- Given the benefits of specialty fertilizers, including precise nutrient release, reduced application rates, and economic advantages for farmers, the specialty fertilizer market is poised for growth in the coming years.

Government initiatives and farmers' focus on increasing productivity are expected to bolster the growth of the market

- In 2022, Nigeria held a commanding 27.0% value share in the African specialty fertilizer market. The country's agricultural sector, while facing challenges such as complex land tenure issues, inadequate irrigation infrastructure, the adverse effects of climate change, and the gradual adoption of cutting-edge agricultural technologies, has seen growth in the market supported by government initiatives. These include the Agriculture Promotion Policy (APP), the Nigeria-Africa Trade and Investment Promotion Programme, the National Agricultural Technology and Innovation Plan (NATIP), and the Anchor Borrowers Program (ABP), all of which have been instrumental in enhancing agricultural productivity.

- South Africa distinguishes itself as the continent's most advanced, productive, and diverse agricultural region. In 2022, its robust agricultural sector held a substantial 37.0% share of the total African specialty fertilizer market. The market is expected to record a CAGR of 6.7% during forecast period. This anticipated growth is largely due to the increasing need to mitigate the effects of climate-related risks, such as prolonged droughts and intense heat waves, by adopting more efficient fertilizer solutions.

- The African specialty fertilizer market is set to expand, driven by a rapidly growing population, the diminishing availability of arable land, the urgent necessity to improve yields on existing farmland, and concerted efforts to enhance agricultural productivity across the region. Thus, the market is forecasted to witness a CAGR of 6.0% from 2023 to 2030.

Africa Specialty Fertilizer Market Trends

The rising domestic demand will lead to double the agricultural production in the near future

- The agro-ecological zones in Africa span from dense rainforests with bi-annual rainfall to arid deserts with minimal precipitation. Key field crops in the region include corn, sorghum, wheat, and rice. In 2022, the cultivation area for these crops reached 224.8 million hectares, accounting for over 95% of the region's agricultural land. In response to a surplus of corn stocks leading to price suppression, South African corn farmers scaled back their planting by 10% to 2.1 million hectares in the 2018-19 season. Consequently, corn production in the country dipped by 11% from 13 million to 12 million tonnes, and exports fell from 2.5 million to 1 million tonnes. This shift prompted producers to allocate more of their fields to oilseed crops, particularly soybeans, resulting in an overall decline in corn cultivation across Africa in 2018-2019.

- Nigeria takes the lead as the largest sorghum producer in Africa, closely followed by Ethiopia. Sorghum, accounting for 50% of the total cereal output, dominates about 45% of Nigeria's cereal crop land. Known for its drought and waterlogging tolerance, sorghum thrives in diverse soil conditions. These attributes position sorghum as the go-to staple crop in Africa's drier regions, ensuring both food and income security.

- Kenya, Somalia, and significant parts of Ethiopia are grappling with the looming specter of severe food shortages. Over the past decade, Africa's spending on food imports has nearly tripled, even as its agricultural industry and cultivated land have continued to expand.

Rapeseed is the highest nitrogen consuming crop

- Rapeseed crops have the highest potassium and phosphorous application rates, accounting for 162.4 kg/hectare and 281.7 kg/hectare, respectively. Meanwhile, the average nitrogen application rate for field crops in Africa stands at 364.9 kg/hectare. In 2022, field crops in Africa accounted for 87.1% of the total primary nutrient consumption, which amounted to 556.1 thousand metric tons. This dominance can be attributed to the extensive land area dedicated to field crops. Specifically, the average nutrient application rates for nitrogen, phosphorous, and potassium in these crops were 223.2 kg/ha, 125.3 kg/ha, and 155.3 kg/ha, respectively.

- The Guinea savannas in Nigeria offer favorable environmental conditions for maize production. However, despite this potential, farmers in the region struggle with low yields. The primary culprits are soil degradation and nutrient depletion, primarily nitrogen, resulting from intensified land use. Field crops prioritize nitrogen application due to its multiple benefits, including promoting tillering, leaf area development, grain formation, filling, and protein synthesis. Nitrogen also plays a crucial role in enhancing both grain yield and quality.

- Given that primary nutrients are vital for crop growth and with concerns over soil depletion and nitrogen leaching, the application rates for primary nutrients are expected to witness significant growth in the coming years.

Africa Specialty Fertilizer Industry Overview

The Africa Specialty Fertilizer Market is fragmented, with the top five companies occupying 29.76%. The major players in this market are ICL Group Ltd, K+S Aktiengesellschaft, Kynoch Fertilizer, UPL Limited and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Speciality Type

- 5.1.1 CRF

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 SRF

- 5.1.4 Water Soluble

- 5.1.1 CRF

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

- 5.4 Country

- 5.4.1 Nigeria

- 5.4.2 South Africa

- 5.4.3 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Gavilon South Africa (MacroSource, LLC)

- 6.4.2 Haifa Group

- 6.4.3 ICL Group Ltd

- 6.4.4 K+S Aktiengesellschaft

- 6.4.5 Kynoch Fertilizer

- 6.4.6 UPL Limited

- 6.4.7 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

アフリカの特殊肥料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 197 Pages

- 納期

- 2~3営業日