|

市場調査レポート

商品コード

1693432

欧州の代替肉:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Meat Substitutes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の代替肉:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 222 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

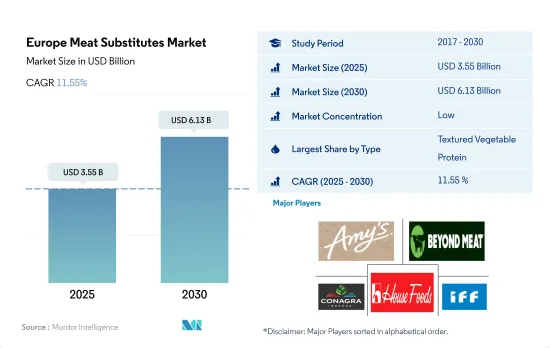

欧州の代替肉市場規模は2025年に35億5,000万米ドルと推定・予測され、2030年には61億3,000万米ドルに達し、予測期間中(2025-2030年)のCAGRは11.55%で成長すると予測されます。

欧州のフレキシタリアンにおける代替肉消費の新たな動向が市場を牽引する

- 2021年には、欧州諸国のフレキシタリアンの約19%が豆腐、テンペ、セイタンを週1~3回の頻度で消費しています。欧州の消費者の約10%が週に4回以上豆腐を消費しています。豆腐の消費に伴う健康上の利点に対する認識が高まっていることも、豆腐の需要増加に寄与しています。豆腐は飽和脂肪酸が少なく、コレステロールを含まず、カルシウムや鉄分などの必須栄養素を豊富に含んでいます。豆腐は、肉由来のタンパク質に代わる健康的な食品と考えられています。豆腐分野は予測期間中、金額ベースで10.97%のCAGRで推移すると予測されています。

- タイプ別では、テクスチャードベジタブルプロテイン(TVP)が最も広く消費されている代替肉です。2022年のセグメント別数量では16%を占めています。様々なタイプの代替肉製造に幅広く応用されていることが、その売上を牽引しています。Cargill、Ingredion、ADMのような地域メーカーは、食代替肉品業界向けにテクスチャード大豆タンパク質やエンドウ豆タンパク質の生産を増強しています。これらの企業は、欧州の食代替肉物市場の成長をさらにサポートすると予測されています。エンドウ豆ベースのTVPの需要は急速に伸びており、これが市場プレイヤーを、より多くの非大豆ベースのグルテンフリーの代用肉作りに駆り立てています。

- テンペは予測期間中、金額ベースで11.17%の最速CAGRで推移すると予測されます。メーカーは、オーガニックテンペ、カレーテンペピース、地中海テンペピース、バーベキューテンペピース、スモーキーテンペラッシャーなど、いくつかのテンペ製品を発表しており、この地域の成長を後押しすると予想されます。さらに、この地域の企業は小売企業と提携してテンペ製品を販売しています。

ビーガンおよびフレキシタリアン人口の増加が市場成長を後押し

- 欧州における代替肉消費の成長動向は2021年まで横ばいでした。予測期間中に急速に勢いを増すと予想されます。2022年には、欧州の全人口の18~21%がフレキシタリアンであり、従来の雑食に比べ肉や魚の摂取頻度が低い人々で構成されます。人々は、タンパク質の必要量を満たすために、肉の代用品を消費する方向に徐々に移行しています。フレキシタリアン人口は、環境安全性や持続可能な食生活といった要因から、さらに29~33%程度まで増加すると予想されています。フレキシタリアン人口は雑食動物に次ぐ最大の食生活グループであるため、代用肉市場に大きな影響を与えます。

- 英国はこの地域で最大の代用肉消費国であり、欧州で最も急成長している代用肉市場になると予想されます。予測期間中、金額ベースでCAGR 10.92%を記録すると予測されています。スーパーマーケットやカントリーパブで代用肉を入手できる機会が増えており、これが代用肉市場の成長を後押ししています。Z世代は、2022年には英国の総人口の約14~16%を占める。同国のZ世代は、植物性食品の消費や菜食主義といった最新の動向を試すことに熱心で、予測期間中の欧州の代用肉市場の成長を促進しています。

- その他欧州では、より良い健康のため、また環境のために、より植物ベースの食事へのシフトが主な原因となって代用肉が消費されています。スウェーデンのような国々では、多くの消費者が週に2~6回程度、代替肉食品を含むベジタリアン食のみを摂取しています。

欧州の代用肉市場動向

高価格が植物性製品購入の大きな制約に

- テンペの価格は、主にインフレと大豆価格のわずかな上昇に対抗するために、ここ数年徐々に上昇しています。欧州では、テンペの価格は2017年から2022年にかけて2.61%上昇しました。同地域では大豆生産量が増加しているため、大豆価格は安定しており、これがテンペ価格の安定に寄与しています。

- 欧州では、大豆生産量は前シーズンから9.16%増加し、2021年には1,156万トンに達します。大豆以外では、ひよこ豆のような原料もテンペの生産に広く使用されています。ひよこ豆の価格は大豆よりも高いです。ドイツのような欧州諸国ではひよこ豆の生産がほとんど行われていないため、これらの国ではひよこ豆はすべて輸入に頼っています。Proveg International(植物性食品を推進するNGO)が発表した植物性食品に関する調査によると、植物性食品を食べる人、減らす人の両方を含む消費者にとって、価格が主な不満点でした。消費者は植物性食品を高すぎると認識しており、より幅広い消費者層が利用できるよう、業界は価格帯を下げるべきだと考えています。

- 2022年のテンペの価格は豆腐より約27%高かったが、これは欧州市場でのテンペの人気が豆腐より低かったためです。欧州の主要国の中では、イタリアとドイツが2022年にテンペの価格が最も高くなり、同地域の最低価格を約24%上回りました。菜食主義者の人口が多いため、これらの国々では製品に対する需要が高まっています。それに伴い、これらの市場では手作りのテンペの提供が増加しており、これが価格上昇の一因となっています。テンペ大豆フィレやマリネテンペなどの加工テンペの価格は、2022年にはプレーンテンペよりもほぼ5~7%高くなります。

欧州の代替肉品産業の概要

欧州の代替肉食品市場は断片化されており、上位5社で12.17%を占めています。この市場の主要企業は以下の通りです。 Amy's Kitchen Inc., Beyond Meat Inc., Conagra Brands Inc., House Foods Group Inc. and International Flavors & Fragrances Inc.(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 価格動向

- テンペ

- テクスチャード・ベジタブル・プロテイン

- 豆腐

- 規制の枠組み

- フランス

- ドイツ

- イタリア

- 英国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- タイプ

- テンペ

- テクスチャード・ベジタブル・プロテイン

- 豆腐

- その他の代替肉食品

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンラインチャネル

- スーパーマーケットとハイパーマーケット

- その他

- オントレード

- オフトレード

- 国名

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- 英国

- その他欧州

第5章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Amy's Kitchen Inc.

- Associated British Foods PLC

- Beyond Meat Inc.

- Conagra Brands Inc.

- House Foods Group Inc.

- International Flavors & Fragrances Inc.

- JBS SA

- Monde Nissin Corporation

- Plant Meat Limited

- The Tofoo Co. Ltd

- VBites Food Limited

- Vitasoy International Holdings Ltd

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Europe Meat Substitutes Market size is estimated at 3.55 billion USD in 2025, and is expected to reach 6.13 billion USD by 2030, growing at a CAGR of 11.55% during the forecast period (2025-2030).

Emerging trends in the consumption of meat substitutes among flexitarians in Europe are driving the market

- Approximately 19% of flexitarians in European countries consumed tofu, tempeh, or seitan on a weekly basis, typically ranging from one to three times per week, in 2021. Around 10% of consumers in Europe consume tofu more than four times a week. The rising awareness of the health benefits associated with tofu consumption has also contributed to its increasing demand. Tofu is low in saturated fat, is cholesterol-free, and is a good source of essential nutrients like calcium and iron. It is often considered a healthier alternative to meat-based protein. The tofu segment is anticipated to register a CAGR of 10.97% by value during the forecast period.

- Based on type, textured vegetable protein (TVP) is the most widely consumed meat alternative. It accounted for a segmental volume of 16% in 2022. Its extensive application in producing different types of meat alternatives drives its sales. Regional manufacturers like Cargill, Ingredion, and ADM are augmenting the production of textured soy protein or pea protein for the meat alternatives industry. These companies are projected to support the growth of the European meat substitutes market further. The demand for pea-based TVP is growing rapidly, which is driving market players to create more non-soy-based, gluten-free meat alternatives.

- Tempeh is projected to record the fastest CAGR of 11.17% in terms of value during the forecast period. Manufacturers have introduced several tempeh products, such as organic tempeh, curry tempeh pieces, Mediterranean tempeh pieces, BBQ tempeh pieces, and smoky tempeh rashers, which is anticipated to boost the growth in the region. Moreover, players in the region are partnering with retail players to market their tempeh products.

Rise in vegan and flexitarian population boosts market growth

- The growth trend of the consumption of meat substitutes in Europe was static till 2021. It is expected to gain momentum rapidly during the forecast period. In 2022, 18-21% of the total European population was flexitarian, consisting of people who consumed meat and fish less frequently compared to traditional omnivores. People are slowly moving toward the consumption of meat substitutes to fulfill their protein requirements. The flexitarian population is further expected to increase to around 29-33% due to factors like environmental safety and sustainable diets. The flexitarian population has a significant impact on the meat substitute market as it is the largest dietary group after omnivores.

- The United Kingdom is the largest consumer of meat substitutes in the region and is expected to be the fastest-growing meat substitute market in Europe. It is projected to register a CAGR of 10.92% in value during the forecast period. There is an increasing availability of meat substitutes in supermarkets and country pubs, which is aiding the growth of the meat substitute market. Gen Z accounted for around 14-16% of the total population of the United Kingdom in 2022. The Gen Z population in the country is eager to try out the latest trends, such as the consumption of plant-based food and veganism, promoting the growth of the European meat substitute market during the forecast period.

- The Rest of Europe consumes meat substitutes primarily due to the shift to a more plant-based diet for better health and for the sake of the environment. Many consumers in countries like Sweden consume only vegetarian food, including meat substitutes, for about two to six times a week.

Europe Meat Substitutes Market Trends

Higher price is observed as a major constraint in purchasing plant-based products

- The price of tempeh has been gradually increasing over the years, mostly to combat inflation and a minimal increase in soybean prices. In Europe, the price of tempeh increased by 2.61% from 2017 to 2022. Due to rising soybean output in the region, the price of soybeans has remained consistent, which has contributed to the stability of tempeh prices.

- In Europe, soybean production increased by 9.16% from the previous season to reach 11.56 million tons in 2021. Other than soybeans, raw materials like chickpeas are also widely used to produce tempeh. The price of chickpeas is higher than soybeans. As there is hardly any production of chickpeas in European countries like Germany, these countries depend entirely on imported chickpeas. As per a study released by Proveg International (an NGO promoting plant-based food) on plant-based foods, price was the main area of dissatisfaction for consumers, including both plant-based eaters and reducers. Consumers have perceived plant-based foods as too expensive and believe that the industry should lower the price point to make them available to a broader consumer base.

- The price of tempeh was about 27% more than tofu in 2022, owing to the lower popularity of tempeh in the European market compared to tofu. Among major European countries, Italy and Germany witnessed the highest tempeh prices, amounting to about 24%, more than the lowest price in the region, in 2022. The bigger vegan populations have led to higher demand for the product in these countries. Accordingly, a rise in the offering of hand-made tempeh was observed in these markets, which contributed to the higher prices. The price of processed tempeh, such as tempeh soy fillet and marinated tempeh, was almost 5-7% higher than plain tempeh in 2022.

Europe Meat Substitutes Industry Overview

The Europe Meat Substitutes Market is fragmented, with the top five companies occupying 12.17%. The major players in this market are Amy's Kitchen Inc., Beyond Meat Inc., Conagra Brands Inc., House Foods Group Inc. and International Flavors & Fragrances Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Tempeh

- 3.1.2 Textured Vegetable Protein

- 3.1.3 Tofu

- 3.2 Regulatory Framework

- 3.2.1 France

- 3.2.2 Germany

- 3.2.3 Italy

- 3.2.4 United Kingdom

- 3.3 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Type

- 4.1.1 Tempeh

- 4.1.2 Textured Vegetable Protein

- 4.1.3 Tofu

- 4.1.4 Other Meat Substitutes

- 4.2 Distribution Channel

- 4.2.1 Off-Trade

- 4.2.1.1 Convenience Stores

- 4.2.1.2 Online Channel

- 4.2.1.3 Supermarkets and Hypermarkets

- 4.2.1.4 Others

- 4.2.2 On-Trade

- 4.2.1 Off-Trade

- 4.3 Country

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 Netherlands

- 4.3.5 Russia

- 4.3.6 Spain

- 4.3.7 United Kingdom

- 4.3.8 Rest of Europe

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 Amy's Kitchen Inc.

- 5.4.2 Associated British Foods PLC

- 5.4.3 Beyond Meat Inc.

- 5.4.4 Conagra Brands Inc.

- 5.4.5 House Foods Group Inc.

- 5.4.6 International Flavors & Fragrances Inc.

- 5.4.7 JBS SA

- 5.4.8 Monde Nissin Corporation

- 5.4.9 Plant Meat Limited

- 5.4.10 The Tofoo Co. Ltd

- 5.4.11 VBites Food Limited

- 5.4.12 Vitasoy International Holdings Ltd

6 KEY STRATEGIC QUESTIONS FOR MEAT SUBSTITUTES INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms