|

市場調査レポート

商品コード

1692539

ドイツの道路貨物輸送:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Germany Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ドイツの道路貨物輸送:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

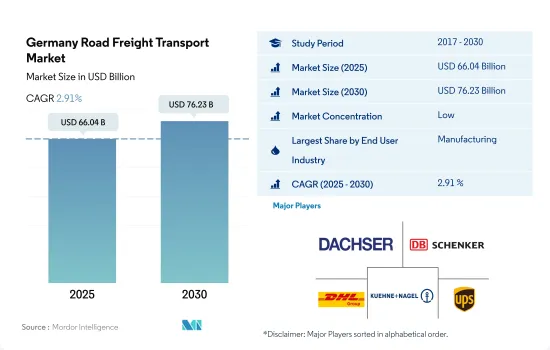

ドイツの道路貨物輸送市場規模は2025年に660億4,000万米ドルと推定・予測され、2030年には762億3,000万米ドルに達し、予測期間中(2025~2030年)のCAGRは2.91%で成長すると予測されます。

ドイツでは2024年から建設生産高が回復し、道路貨物サービスの需要を牽引すると予想されます。

- アディティブマニュファクチャリングは世界的に普及しつつあります。欧州では、積層造形は2023年から2030年の間にCAGR 20.7%を記録すると予想されます。ドイツは欧州最大の市場であり、今後数年間で最大15%の成長が見込まれています。航空宇宙、医療機器、輸送、自動車などいくつかの産業が主な成長要因となっています。ここ数年、積層造形は消費財や宝飾品などの新たな用途にも広がっています。アディティブマニュファクチャリングの成長に伴い、道路貨物需要も増加すると予想されます。

- インフラプロジェクトに対する政府支出の増加は、建設エンドユーザーセグメントの成長を促進すると予想されます。建設生産高は、運輸、再生可能エネルギー、住宅、製造セクターへの投資に支えられて、2024年から回復すると予想されます。さらに、農産物輸出の増加が農業・漁業・林業エンドユーザーセグメントを支えるものと予想されます。ドイツの新連立政権は、2030年までに国内の耕作地の30%を有機農法で管理することを目指しているため、有機農法による農業生産は今後数年間で増加すると予想されます。

ドイツの道路貨物輸送市場の動向

ドイツは欧州のロジスティクスと輸送をリードし、環境に優しい輸送モードに焦点を当てた投資イニシアティブが高まっています。

- 2024年7月、ドイツ政府は大型車向けの急速充電ネットワークを構築する全国プロジェクトを開始しました。このイニシアチブは、2045年までにカーボンニュートラルな輸送部門を達成するというベルリンの野心的な目標に沿ったものです。2023年には温室効果ガス排出量が顕著に減少し、欧州最大の経済国としては70年ぶりの低水準を記録するもの、運輸部門は環境ベンチマークを達成するのに苦労しています。ドイツは、2030年までに大型道路輸送のおよそ3分の1を電動式にするか、合成メタンや水素のような電動式燃料を利用することを目標としています。

- ドイツ政府は、環境保護、持続可能性、効率的な輸送を促進するため、道路よりも鉄道に投資する意向です。2022年、ドイツ鉄道、連邦政府、地方政府は、鉄道インフラにおよそ136億ユーロ(145億1,000万米ドル)を投資しました。ニーダーザクセン州、ハンブルク州、ブレーメン州、メクレンブルク=西ポメラニア州、シュレースヴィヒ=ホルシュタイン州はドイツ鉄道とともに、2030年までに鉄道網の近代化に投資しました。

欧州の整備シーズン終了によりドイツのE5ガソリン価格が急落

- 2024年5月末、E5ガソリン価格は4月に比べ大幅に下落し、最終週には4.91米ドル/100L値下がりしました。この下落は、欧州でメンテナンス・シーズンが終了し、製油所の生産が増加し、輸入が増加したためです。アムステルダム・ロッテルダム・アントワープからドイツへのガソリン輸入は着実に増加しており、ドイツの港湾では5月に8,500b/dを受け入れたが、輸出は3,700b/dに減少しました。供給過剰とメンテナンス・シーズンの終了が、ドイツのE5ガソリン価格を押し下げています。一方、南部と東部ではディーゼル価格が市場の混乱を引き起こしています。

- ドイツの消費者は最も早い物価上昇に直面し、年間インフレ率の高さは主にロシア・ウクライナ戦争以降のエネルギーと食料品の極端な値上がりに起因します。ドイツは世界有数の天然ガス輸入国です。ガス消費量の約95%を輸入で賄っています。2022年には、ガス輸入の55%がロシアから、30%がノルウェーから、13%がオランダから輸入されます。さらにドイツは、2027年のEU排出権取引から燃料価格が跳ね上がると予想しています。2026年に比べ、2027年初頭にはガソリンが1リットル当たり38セント、天然ガスが1キロワット時当たり約3セント上昇します。

ドイツの道路貨物輸送産業の概要

ドイツの道路貨物輸送市場は断片化されており、この市場の主要5社はDACHSER、ドイツ鉄道AG(DBシェンカーを含む)、DHLグループ、Kuehne+Nagel、United Parcel Service of America, Inc.(UPS)である(アルファベット順)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 経済活動別GDP分布

- 経済活動別GDP成長率

- 経済パフォーマンスとプロファイル

- eコマース産業の動向

- 製造業の動向

- 運輸・倉庫業のGDP

- 物流実績

- 道路の長さ

- 輸出動向

- 輸入動向

- 燃料価格動向

- トラック輸送コスト

- タイプ別トラック保有台数

- 主要トラックサプライヤー

- 道路貨物トン数の動向

- 道路貨物価格動向

- モーダルシェア

- インフレ率

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 農業、漁業、林業

- 建設業

- 製造業

- 石油・ガス、鉱業、採石業

- 卸売・小売業

- その他

- 輸出先

- 国内貨物

- 国際貨物

- トラック積載量

- 全トラック積載(FTL)

- 小口貨物(LTL)

- コンテナ輸送

- コンテナ輸送

- コンテナなし

- 距離

- 長距離輸送

- 短距離輸送

- 商品構成

- 流体商品

- 固体商品

- 温度制御

- 非温度制御

- 温度制御

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- A.P. Moller-Maersk

- DACHSER

- Deutsche Bahn AG(including DB Schenker)

- DHL Group

- DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

- Expeditors International of Washington, Inc.

- Kuehne+Nagel

- Raben Group

- United Parcel Service of America, Inc.(UPS)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の物流市場の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界バリューチェーン分析

- 市場力学(市場促進要因、抑制要因、機会)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

- 為替レート

目次

Product Code: 92356

The Germany Road Freight Transport Market size is estimated at 66.04 billion USD in 2025, and is expected to reach 76.23 billion USD by 2030, growing at a CAGR of 2.91% during the forecast period (2025-2030).

Construction output is expected to pick up from 2024 in Germany and drive the demand for road freight services

- Additive manufacturing is becoming more popular worldwide. In Europe, additive manufacturing is expected to record a CAGR of 20.7% between 2023 and 2030. Germany is the largest market in Europe and is expected to grow up to 15% in the coming years. Several industries, such as aerospace, medical devices, transportation, and automotive, are the main growth drivers. In the last few years, additive manufacturing has been extended to new applications like consumer goods and jewelry. With the growth of additive manufacturing, road freight demand is expected to increase as well.

- The increased government spending on infrastructure projects is expected to drive the growth of the construction end-user segment. Construction output is expected to pick up from 2024, supported by investments in the transport, renewable energy, housing, and manufacturing sectors. Moreover, the rise in agricultural exports is expected to support the agriculture, fishing, and forestry end-user segment. Organic agricultural production is expected to increase in the coming years as Germany's new coalition government aims to have 30% of the country's cultivated land under organic management by 2030.

Germany Road Freight Transport Market Trends

Germany leads European logistics and transportation, with rising investment initiatives focused on Eco-friendly mode of transport

- In July 2024, the German government initiated a nationwide project to establish a fast-charging network tailored for heavy-duty vehicles. This initiative aligns with Berlin's ambitious goal to achieve a carbon-neutral transport sector by 2045. Despite a notable drop in greenhouse gas emissions in 2023, marking a 70-year low for Europe's largest economy, the transport segment has struggled to hit its environmental benchmarks. Germany is targeting that roughly one-third of its heavy road haulage will be electrically powered or utilize electrically produced fuels like synthetic methane or hydrogen by 2030.

- The German government intends to invest more in rail than roads to promote environmental protection, sustainability, and effective transportation. In 2022, Deutsche Bahn, the federal government, and the local and regional governments invested roughly EUR 13.6 billion (USD 14.51 billion) in rail infrastructure. Lower Saxony, Hamburg, Bremen, Mecklenburg-Western Pomerania, and Schleswig-Holstein, together with DB, invested in modernizing their rail networks by 2030.

E5 gasoline prices in Germany dropped sharply due to end of maintenance season in Europe

- At the end of May 2024, E5 gasoline prices dropped significantly compared to April, with prices USD 4.91/100L lower in the last week. This decline is due to the end of the maintenance season in Europe, leading to increased refinery production and rising imports. Gasoline imports from Amsterdam-Rotterdam-Antwerp to Germany have steadily risen, with German seaports receiving 8,500 b/d in May, while exports fell to 3,700 b/d. The oversupply and end of maintenance season are driving down E5 gasoline prices in Germany. Meanwhile, diesel prices in the south and east are causing market disruptions.

- German consumers faced the fastest price rise, and the high annual inflation rate was primarily driven by extreme price increases for energy and groceries since the Russia-Ukraine War. Germany is among the world's biggest natural gas importers. Around 95% of its gas consumption is met by imports. In 2022, 55% of gas imports came from Russia, 30% from Norway, and 13% from the Netherlands. Moreover, Germany anticipates a fuel price jump from 2027 EU emissions trading. An increase of 38 cents per liter of petrol and around 3 cents per kilowatt hour of natural gas at the beginning of 2027 compared to 2026.

Germany Road Freight Transport Industry Overview

The Germany Road Freight Transport Market is fragmented, with the major five players in this market being DACHSER, Deutsche Bahn AG (including DB Schenker), DHL Group, Kuehne+Nagel and United Parcel Service of America, Inc. (UPS) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 GDP Distribution By Economic Activity

- 4.2 GDP Growth By Economic Activity

- 4.3 Economic Performance And Profile

- 4.3.1 Trends in E-Commerce Industry

- 4.3.2 Trends in Manufacturing Industry

- 4.4 Transport And Storage Sector GDP

- 4.5 Logistics Performance

- 4.6 Length Of Roads

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Pricing Trends

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Major Truck Suppliers

- 4.13 Road Freight Tonnage Trends

- 4.14 Road Freight Pricing Trends

- 4.15 Modal Share

- 4.16 Inflation

- 4.17 Regulatory Framework

- 4.18 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 Truckload Specification

- 5.3.1 Full-Truck-Load (FTL)

- 5.3.2 Less than-Truck-Load (LTL)

- 5.4 Containerization

- 5.4.1 Containerized

- 5.4.2 Non-Containerized

- 5.5 Distance

- 5.5.1 Long Haul

- 5.5.2 Short Haul

- 5.6 Goods Configuration

- 5.6.1 Fluid Goods

- 5.6.2 Solid Goods

- 5.7 Temperature Control

- 5.7.1 Non-Temperature Controlled

- 5.7.2 Temperature Controlled

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 A.P. Moller - Maersk

- 6.4.2 DACHSER

- 6.4.3 Deutsche Bahn AG (including DB Schenker)

- 6.4.4 DHL Group

- 6.4.5 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.6 Expeditors International of Washington, Inc.

- 6.4.7 Kuehne+Nagel

- 6.4.8 Raben Group

- 6.4.9 United Parcel Service of America, Inc. (UPS)

7 KEY STRATEGIC QUESTIONS FOR ROAD FREIGHT CEOS

8 APPENDIX

- 8.1 Global Logistics Market Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate