|

市場調査レポート

商品コード

1692482

米国のITサービス:市場シェア分析、産業動向、成長予測(2025年~2030年)United States (US) IT Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のITサービス:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

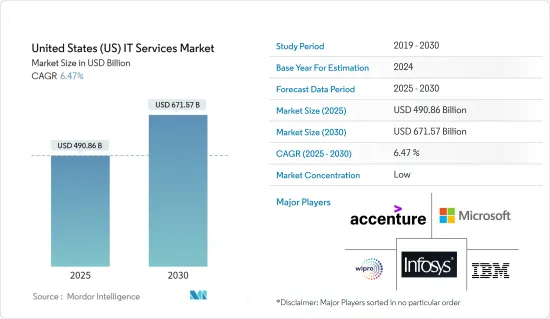

米国のITサービス市場規模は2025年に4,908億6,000万米ドルと推定され、2030年には6,715億7,000万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは6.47%です。

企業は、コストを削減しながら成長を促進するための先進技術へのアクセスや、クラウド技術の利用拡大、収益増加のための予測や企業運営の最適化のためのビジネスインテリジェンスの利用など、デジタル化に重点を置いています。データ・セキュリティとプライバシー保護への配慮の高まりが、さまざまな業種の企業のITサービス需要を促進しています。

主なハイライト

- デジタルトランスフォーメーション時代の企業は、オンプレミスのITインフラサービスをアップグレードし、業務の一部をクラウドに移行するため、IT意思決定者は規制遵守、セキュリティ、リスク削減の問題に直面しています。

- さらに、クラウド・コンピューティング・ソリューションに対する需要、ひいてはこの地域におけるオンデマンドITサービスの採用は、新たな情報ストレージを構築したり維持したりするよりも、データをクラウドに移行した方がコストとリソースを節約できるという企業意識の高まりに後押しされています。

- 同地域のITサービスは、5G、ブロックチェーン、AR、AIといった動向の影響を受ける可能性が高いです。5G技術の登場により、企業は自社内にネットワークを構築できるようになると思われます。デジタルトランスフォーメーションにより、ローカル周波数帯に基づく新たなネットワークの構築や、既存ネットワークのLTEへのアップグレードが可能になると予想されます。

- ITサービス市場の見通しは明るいです。しかし、データ漏えいの増加、製品のカスタマイズに対するコスト懸念、データ移行などの要因が、市場に脅威を与えています。

- 米国国勢調査局によると、COVID-19以降、米国の小売eコマース売上高は前期比で増加しました。パンデミック後に市場企業が成長するチャンスは、このような電子商取引の売上高の大幅な増加によって生まれると思われます。パンデミック以降、ITサービス市場に大規模な投資を行う企業が目立って増えています。さまざまなエンドユーザー業界における進化するデジタルトランスフォーメーションの要件に対応し、ハイブリッドワークプレイス環境を強化する必要性が、主にこの成長を後押ししています。

米国のITサービス市場の動向

ITアウトソーシングが大きな市場シェアを占める

- 米国企業の大半は、人件費を節約するためにIT業務を新興経済諸国にアウトソーシングしてきました。米国には、IBM、DXC、コグニザントといった大手ITアウトソーシング企業が進出しており、予測期間中、同国のオフショアおよびオンショアITアウトソーシング市場を活性化させる要因となっています。

- 同国では、民間企業や政府系企業のデジタル化が急速に進んでおり、TCSやInfosysなどのベンダーがITアウトソーシングサービスを提供する企業と契約することで、事業を拡大する機会を生み出しています。

- 例えば、米国に拠点を置く雇用主は、米国に拠点を置く従業員を雇用する際、一連のコストパラメータを考慮します。これらのコストには、採用、オフィススペース、コンピュータ機器、オフィス家具、監督/トレーニング、品質保証、賃金/給与、連邦保険拠出法(FICA)、メディケア、失業保険、労災保険、福利厚生、退職金制度、有給休暇、病欠、従業員の離職率、事務用品、人事部門、政府規制の遵守監督などが含まれます。

- このようなコストの積み重ねの中で、ITアウトソーシングという選択肢がより現実的になってくる。世界ITサービス・ベンダーもまた、世界ITサービス・ベンダーは、国内での足跡を拡大することに頼りました。こうした動きは、地元企業のITアウトソーシング需要が急増していることを明確に示しています。スマート製造、保険、航空宇宙、防衛分野の顧客にデジタルトランスフォーメーション・サービスを提供するため、HCLテクノロジーズは同国に世界・デリバリー・センターを設立しました。

- Onix Networking Corp、Innowise Incなど、米国で事業を展開する多くの中規模ITサービス企業は、マイクロソフトやグーグルなどの世界・テクノロジー企業と提携し、ITアウトソーシング・サービス能力を高め、同国の市場成長を支えています。例えば、オニックスは2023年2月、Google Cloud Partner Advantageプログラムに協力し、アプリケーション開発パートナー専門資格を取得したと発表しました。これにより、同社のITアウトソーシング・サービスは拡大し、Google Cloudテクノロジーを利用したアプリケーション開発分野で顧客ソリューションを構築する能力とキャパシティを提供することになりました。

- インダストリー4.0に伴う米国のデジタル化動向は、ITサービスのリショアリング、すなわち米国へのオペレーション回帰につながりました。政府が国内雇用の創出と米国経済の復活を目指していることから、この動きはますます活発になっており、同国におけるITアウトソーシング企業の市場拡大を支え、予測期間中の市場を牽引する可能性があります。

- 米国労働統計局は、現在から2026年の間に雇用が31%増加すると予測しています。また、この期間に約25万5,400人のIT雇用が創出される見込みです。米国内では、公共部門で約36万人、情報産業で約8万3,000人が雇用されています。

最大のエンドユーザー産業はヘルスケア

- 先端技術や新興技術は、近年、米国のヘルスケアを一変させました。規制環境の変化に対応して、病院や医院は患者の治療の質を向上させる新技術を導入しています。国内の医療施設ではハイテク業務が行われるようになり、有能な専門家の手に高度な技術が委ねられています。

- ヘルスケア分野のITサービスは、効率的でデジタルアクセスが可能なヘルスケアのための洞察力主導型ソリューションの実装を可能にし、個々の組織から小規模または大規模のマルチサービス組織やフランチャイズまで対応します。さらに、これらのサービスは、ヘルスケアの顧客が統合されたケア提供を合理化し、臨床的、財務的、運営上の成果を向上させるのに役立ちます。

- さらに、ヘルスケア部門におけるITサービスの導入は、ヘルスケア組織がケア向上のためにヘルスケア業務のデジタル化に注力していることから、米国全土で急速に増加しています。そのため、さまざまなITサービス・プロバイダーがこの地域でヘルスケアITサービスを導入しています。

- 例えば、DamcoのHIPAAに準拠した遠隔医療ソリューションは、ヘルスケアプロバイダーが従来の医療モデルに代わる、高品質で安全な遠隔医療サービスを提供することを可能にします。インターネットやモバイル機器を利用して医師と接続し、テレビ会議や音声通話を利用したり、オンライン予約をしたり、リアルタイムの診察を受けたり、遠隔地から治療に関する詳細な情報を得たりすることで、この会社のITサービスにより、患者はどこにいてもヘルスケア・サービスにアクセスすることができます。

- さらに、政府は医療費が7兆1,470億米ドルに達すると予測しており、これが市場の成長に寄与しています。米国では、ヘルスケアにおけるデジタルトランスフォーメーションとは、支払者、医療提供者、その他の組織など、企業全体のデジタル機能やプロセスの統合を意味します。

- デジタルシステムとプロセスを組み合わせることで、デジタル変革されたヘルスケアは、患者に個別化されたオムニチャネル体験を提供することができます。電子カルテの進歩や、医療相互運用性を目指すその他のイニシアチブは、米国におけるヘルスケアのデジタル変革への最近のシフトを反映しています。こうした開発は、米国におけるITサービスの導入を後押ししています。

米国のITサービス市場の概要

米国のITサービス市場は断片的であり、現在調査中であるが、IBM、TCS、Wipro、Microsoft、Capgeminiといった大手企業によって支配されています。これらの業界大手は、市場での存在感を維持し、顧客を維持するために、強固な競争戦略を採用し、継続的に自社のサービスを向上させています。このような激しい競争が市場情勢を特徴づけており、これらの企業が顧客の多様なニーズに合わせてサービスをカスタマイズしているため、競争企業間の敵対関係は予測期間を通じて続くと予想されます。

- 2023年10月、IBMは、アラートの85%までを自動的にエスカレーションまたはクローズする機能を含む、新しいAI技術によるマネージド検知・対応サービスの次の進化を発表しました。新たな脅威検知・対応サービス(TDR)は、既存のセキュリティツールや投資、クラウド、オンプレミス、運用技術(OT)など、顧客のハイブリッドクラウド環境全体にわたるあらゆる関連技術からのセキュリティアラートの24時間365日の監視、調査、自動修復を提供します。

- 2023年7月、タタ・コンサルタンシー・サービシズ(TCS)は、GEヘルスケア・テクノロジーズ・インク(GEヘルスケア)との長年にわたるパートナーシップを拡大し、GEヘルスケアのITオペレーティング・モデルの変革を促進します。この提携は、GEヘルスケアのアプリケーション・ポートフォリオを監督し、イノベーションを促進する斬新なオペレーティング・モデルを導入することで、GEヘルスケアの世界IT機能をデジタルに刷新することに主眼が置かれます。TCSは、エンタープライズITアプリケーションの開発、保守、合理化、標準化を監督します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 競合の程度

- 代替品の脅威

- 業界バリューチェーン分析

- COVID-19の市場への影響評価

- 規制状況

第5章 市場力学

- 市場促進要因

- 各業界におけるデジタルトランスフォーメーションの加速と新技術の採用

- 非中核業務のアウトソーシングによるコアコンピテンシーの活用重視の高まり

- 市場抑制要因

- データセキュリティ、カスタマイズ、データ移行

- 比較分析ティア1(大手)対ティア2(中堅)ITサービスベンダー

- インハウスとアウトソーシングの分析

第6章 市場セグメンテーション

- タイプ別

- ITコンサルティングとインプリメンテーション

- ITアウトソーシング

- ビジネス・プロセス・アウトソーシング

- その他のタイプ

- エンドユーザー別

- 製造業

- 政府機関

- BFSI

- ヘルスケア

- 小売・消費財

- 物流

- その他のエンドユーザー

第7章 競合情勢

- 企業プロファイル

- IBM Corporation

- Accenture PLC

- Microsoft Corporation

- Infosys Limited

- Wipro Limited

- TATA Consultancy Services Limited

- Capgemini SE

- Atos SE

- HCL Technologies Limited

- Leidos Holdings, Inc.

- Sphere Partners LLC

- Kanda Software

- Fingent Corp.

- Intetics Inc.

- Integris

- Synoptek, LLC

- Simform

- MAS Global Consulting

- Algoworks Solutions Inc

- Icreon Holdings Inc

- DevDigital LLC

- Slalom, Inc.

- VATES S.A.

- Computer Solution East, Inc.

- Perficient, Inc.

- Innowise Group

- Velvetech LLC

- CHI Software

- Edafio Technology Partners

- VLink, Inc.

- Ardem Incorporated

- Unity Communications

- Accedia

- Intersog

- Galaxy Weblinks LTD

- Wave Access USA

- Centricsit LLC

- A3 Logics

- Bottle Rocket LLC

- Premier BPO, LLC

- Sumerge

- Peak Support, LLC

- Progent Corporation

- Sciencesoft USA Corporation

- Intellectsoft US LLC

第8章 投資分析

第9章 市場の将来

The United States IT Services Market size is estimated at USD 490.86 billion in 2025, and is expected to reach USD 671.57 billion by 2030, at a CAGR of 6.47% during the forecast period (2025-2030).

Firms focusing more on digital with access to advanced technologies for driving growth while decreasing cost, growing usage of cloud technologies, and using business intelligence for forecasting and optimizing company operations to earn more increased revenues are a few of the critical IT Services Market drivers and trends fueling the growth of the market. Growing data security and privacy protection considerations drive the demand for IT services from companies across various industry verticals.

Key Highlights

- IT decision-makers face regulatory compliance, security, and risk reduction issues as businesses in the digital transformation era upgrade their on-premises IT infrastructure services and move some of their operations to the cloud.

- Moreover, The demand for cloud computing solutions and, consequently, the adoption of ondemand IT services in the region is driven by increasing awareness amongst businesses that they can save money and resources by shifting their data to a cloud rather than building or maintaining new information storage.

- The IT services acorss the region are likely to be influenced by trends such as 5G, Blockchain, AR and AI. It's likely that companies will be able to set up networks in their premises with the arrival of 5G technology. It is expected that digital transformation will allow the establishment of new networks based on local frequency bands or to upgrade existing ones for LTE.

- IT service market has a positive outlook in the country. Still, factors such as growing data breaches, cost concerns over product customization, and data migration are some of the reasons posing a threat to the market.

- According to the US Census Bureau, post-COVID-19, retail e-commerce sales in the United States were rise over the previous quarter. The opportunity for market players to grow after the pandemic would be created by such a huge increase in ecommerce sales. There has been a noticeable increase in organisations that have made significant investments to the IT services market since the pandemic. The need to address evolving digital transformation requirements in different end user industries and to strengthen the hybrid workplace environment is primarily driving this growth.

United States (US) IT Services Market Trends

IT Outsourcing to Hold Major Market Share

- The majority of US companies have long outsourced IT work to developing economies to save on labor costs. The country houses major IT outsourcing players such as IBM, DXC, and Cognizant, which fuels the country's offshore and onshore IT outsourcing market during the forecast period.

- The country has been registering significant digital transformations across all private and government-owned businesses, creating an opportunity for market vendors, such as TCS, Infosys, etc., to expand their businesses by contracting with the enterprises for their IT outsourcing service offerings.

- A US-based employer, for instance, considers a set of cost parameters while hiring a US-based employee. These costs include recruiting, office space, computer equipment, office furniture, supervision/training, quality assurance, wage/salary, Federal Insurance Contributions Act (FICA), Medicare, unemployment insurance, workman's comp, benefits, retirement plan, paid holidays, sick days, employee turnover, office supplies, human resources department, and government regulations compliance oversight.

- Amongst these cost stacks, the IT outsourcing option becomes more viable. The global IT services vendors also Additionally, the global IT services vendors resorted to expanding their footprints in the country. Such action clearly indicates demand soaring for IT outsourcing from local companies. In order to offer digital transformation services to clients in the smart manufacturing, insurance, aerospace and defence sectors, HCL Technologies has established a global delivery centre in the country.

- Many midscale IT service companies operating in the US, such as Onix Networking Corp, Innowise Inc., etc., have been partnering with global technology companies, such as Microsoft and Google, to increase their IT outsourcing service capabilities, supporting the market growth in the country. For instance, in February 2023, Onix announced that it has collaborated in the Google Cloud Partner Advantage program to gain the application Development Partner Specialization. It expanded its IT outsourcing service, offering the capability and capacity to build customer solutions in the Application Development field using Google Cloud technology.

- The digitization trend in the country with Industry 4.0 has led to the reshoring of IT services, i.e., bringing operations back to the US shores. This has become increasingly popular as the government has been aiming to create domestic jobs and help in the resurgence of the American economy, which can support the market expansion of IT outsourcing companies in the country and drive the market during the forecast period.

- The Bureau of Labor Statistics in the United States estimates that there will be a 31% increase in employment between now and 2026. In addition, in this period, approximately 255,400 IT jobs are expected to be created. About 0.36 million people were employed by the public sector and about 0.083 million for information industries within the United States.

Healthcare to be the Largest End-user Industry

- Advanced and emerging technologies have recently transformed healthcare in the United States. In response to the changing regulatory environment, hospitals and doctor's offices have introduced new technology that improves quality of care for patients. High technology operations are now being carried out at medical facilities in the country, placing advanced technologies in the hands of talented professionals.

- IT services in the healthcare sector enable the implementation of insights-driven solutions for efficient and digitally accessible healthcare that suit individual organizations to small or big multiservice organizations and franchises. Additionally, these services help healthcare customers streamline integrated care delivery for better clinical, financial, and operational outcomes.

- Moreover, the implementation of IT services in the healthcare sector is rapidly rising across the United States as healthcare organizations focus on digitizing healthcare practices for improved care. Therefore, various IT service providers are introducing healthcare IT services in the region.

- For example, Damco's HIPAA complaint telemedicine solution enables healthcare providers to offer quality and safe telehealth services that give a more favourable alternative to traditional medical models. By using the Internet and mobile devices to connect with doctorsleveraging videoconferencing or audiophone call communications, booking online appointments, undergoing real time consultations, getting more information about medical treatments remotely, this company's IT service enables patients to access healthcare services from wherever they are.

- Furthermore, the government has forecasted the healthcare expenditure to reach USD 7.147 trillion, thereby contributing to the market growth. In the United States, digital transformation in healthcare involves the integration of digital functions or processes across the enterprise - be it a payer, a provider, or another organization.

- By combining digital systems and processes, digitally transformed healthcare can offer its patients individualized and omnichannel experiences. Advancements in electronic medical records or other initiatives striving for medical interoperability reflect the recent shift toward the digital transformation of healthcare in the United States. Such developments are boosting the adoption of IT services in the United States.

United States (US) IT Services Market Overview

The USA IT service market is fragemnted and is under examination is currently dominated by major players, including IBM, TCS, Wipro, Microsoft, and Capgemini, all of whom boast substantial client bases. These industry leaders are continuously elevating their offerings, employing robust competitive strategies to maintain their market presence and retain their clientele. This intense competition characterizes the market landscape, with high levels of rivalry expected to persist throughout the forecasted period as these players tailor their services to meet the diverse needs of their customers.

- In October 2023 - IBM has announced the next evolution of its managed detection and response service offerings with new AI technologies, including the ability to automatically escalate or close up to 85% of alerts, while helping to accelerate security response timelines for clients. Where the new Threat Detection and Response Services (TDR) provide 24x7 monitoring, investigation, and automated remediation of security alerts from all relevant technologies across client's hybrid cloud environments - including existing security tools and investments, as well as cloud, on-premise, and operational technologies (OT)

- In July 2023, Tata Consultancy Services (TCS) extended its longstanding partnership with GE HealthCare Technologies Inc. (GE HealthCare) to facilitate the transformation of GE Healthcare's IT operating model. This collaboration will primarily focus on digitally revamping GE HealthCare's global IT function by introducing a novel operating model for overseeing its application portfolio and fostering innovation. TCS will oversee the development, maintenance, rationalization, and standardization of its enterprise IT applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Degree of Competition

- 4.2.5 Threat of Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the market

- 4.5 Regulatory Landscape

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Acceleration of Digital Transformation Across Industries and Adoption of New Technologies

- 5.1.2 Growing Emphasis on Leveraging the Core Competencies by Outsourcing Non-core Operations

- 5.2 Market Restraints

- 5.2.1 Data Security, Customization, and Data Migration

- 5.3 Comparative Insights: Tier 1 (Large) vs Tier 2 (Medium) IT Services Vendors

- 5.4 In-housing and Outsourcing Analysis

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 IT Consulting and Implementation

- 6.1.2 IT Outsourcing

- 6.1.3 Business Process Outsourcing

- 6.1.4 Other Types

- 6.2 By End-User

- 6.2.1 Manufacturing

- 6.2.2 Government

- 6.2.3 BFSI

- 6.2.4 Healthcare

- 6.2.5 Retail and Consumer Goods

- 6.2.6 Logistics

- 6.2.7 Other End-Users

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Accenture PLC

- 7.1.3 Microsoft Corporation

- 7.1.4 Infosys Limited

- 7.1.5 Wipro Limited

- 7.1.6 TATA Consultancy Services Limited

- 7.1.7 Capgemini SE

- 7.1.8 Atos SE

- 7.1.9 HCL Technologies Limited

- 7.1.10 Leidos Holdings, Inc.

- 7.1.11 Sphere Partners LLC

- 7.1.12 Kanda Software

- 7.1.13 Fingent Corp.

- 7.1.14 Intetics Inc.

- 7.1.15 Integris

- 7.1.16 Synoptek, LLC

- 7.1.17 Simform

- 7.1.18 MAS Global Consulting

- 7.1.19 Algoworks Solutions Inc

- 7.1.20 Icreon Holdings Inc

- 7.1.21 DevDigital LLC

- 7.1.22 Slalom, Inc.

- 7.1.23 VATES S.A.

- 7.1.24 Computer Solution East, Inc.

- 7.1.25 Perficient, Inc.

- 7.1.26 Innowise Group

- 7.1.27 Velvetech LLC

- 7.1.28 CHI Software

- 7.1.29 Edafio Technology Partners

- 7.1.30 VLink, Inc.

- 7.1.31 Ardem Incorporated

- 7.1.32 Unity Communications

- 7.1.33 Accedia

- 7.1.34 Intersog

- 7.1.35 Galaxy Weblinks LTD

- 7.1.36 Wave Access USA

- 7.1.37 Centricsit LLC

- 7.1.38 A3 Logics

- 7.1.39 Bottle Rocket LLC

- 7.1.40 Premier BPO, LLC

- 7.1.41 Sumerge

- 7.1.42 Peak Support, LLC

- 7.1.43 Progent Corporation

- 7.1.44 Sciencesoft USA Corporation

- 7.1.45 Intellectsoft US LLC