|

市場調査レポート

商品コード

1692139

欧州の道路貨物輸送:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Europe Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の道路貨物輸送:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 300 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

欧州の道路貨物輸送市場規模は2024年に4,968億3,000万米ドルと推定・予測され、2030年には6,015億9,000万米ドルに達し、予測期間中(2024年~2030年)のCAGRは3.24%で成長すると予測されます。

小売eコマースの急増が卸売・小売業エンドユーザー・セグメントの進歩を牽引

- 2022年、製造業エンドユーザー部門は、人間とロボットの協働が増加し、生産が促進されたことで成長しました。ドイツは世界第5位のロボット市場であり、2万2,000台の産業用ロボットが様々な産業で活用されており、2021年時点で世界のロボット設置台数の6%を占めています。さらに、2021年には、ドイツの食品小売企業であるシュワルツ・グループが、欧州域内の総売上高が1,537億5,000万米ドルに達し、欧州随一の小売企業に浮上しました。ドイツでは、2022年に耐久消費財の小売売上高が前年比1.50%増加すると予測されました。これは、2022年の個人消費の推定5.40%増に支えられています。

- 欧州の石油・ガス、鉱業、採石部門では、ドイツの再ガス化計画が石油・ガスエンドユーザーセグメントの成長を促進する要因のひとつとなっています。同国の天然ガス需要はロシアが供給しています。その結果、ドイツは2022年から2026年の間に欧州で最も高いLNG再ガス化能力を追加すると予想され、2026年までに同地域の総追加能力の36%を占めることになります。2022年には、イタリアのエネルギー純輸入コストは2倍以上となり、1,132億4,000万米ドルに達すると予想されます。

- 卸売・小売業のエンドユーザー部門は、主に欧州のeコマース産業の拡大が予想され、2023年から2027年にかけてCAGR8.85を記録すると予測されていることから、今後数年間で大幅な成長を遂げる構えです。ドイツのeコマース市場に関しては、2025年までに6,840万人のユーザーが市場に参入し、2022年の80.1%から81.9%の普及率を達成すると予測されています。

欧州全域での道路貨物輸送量の開拓とインフラ整備に向けた政府の取り組みが市場成長を牽引

- 2022年、フランスの国際道路貨物輸送によるEU域内および域外輸送トン数は主要なものでした。例えば、フランスとスイス間の道路輸送によるEU/域外EUの総輸送トン数は、道路輸送による総輸送トン数の7.3%のシェアを占め、フランスと英国間の道路輸送によるEU/域外EUの総輸送トン数は、2022年に6.5%のシェアを占めました。2022年上半期の道路輸送量はイタリア貨物の68.1%を占め、輸送量(トンキロ)は前年比1.5%増加しました。イタリアの道路運送部門の企業数は、2022年末時点で約100,797社に達し、2021年末時点の99,465社から1.34%増加しました。

- 道路貨物輸送市場では、ドイツでは約35,000社の道路貨物会社に約430,000人の従業員が働いており、過去5年間は安定しています。2021年のドイツにおける積載量3.5トンの車両は96万4,696台で、2020年比で1.3%、5年間で3.4%の伸びを示しました。すべての主要国の経済活動の低下とインフレによる燃料費と賃金コストの上昇により、オランダでは2022年の第27週から第30週にかけてトラックによる貨物輸送が減少しました。第25週以降、トラックによる荷動きの減少幅は、2021年同週比で週当たり9~21%減少しました。

- 北欧では、2022年のトラックの海外輸送量は6.7%増加しました。デンマークからのトラック輸出の主な仕向地はオランダ、ポーランド、ドイツで、輸出全体の54%のシェアを占めています。英国では、輸出と輸入の上位5カ国は長期にわたって比較的一定しています。しかし、ドイツへの輸出は2000年の140万トンから2021年には19万トンに減少しています。

欧州の道路貨物輸送市場の動向

欧州連合(EU)、景気回復を後押しする135の輸送プロジェクトに57億6,000万米ドルを割り当て

- 輸送・倉庫部門は、さまざまな業界の業務をサポートする上で重要な役割を担っており、ドイツがフランスや英国を抜いて圧倒的なトップとなっています。世界的に見ても、ドイツは商品の輸出入ともに第3位です。ドイツ連邦政府は交通インフラへの投資を拡大する意向を表明し、2022年には連邦高速道路に120億ユーロ(128億米ドル)以上、水路に約17億ユーロ(18億1,000万米ドル)を割り当て、交通網の改善へのコミットメントを示しました。

- ドイツ政府は、道路網よりも鉄道網に投資する意向です。2022年には、ドイツ鉄道、連邦政府、地方政府が鉄道インフラにおよそ136億ユーロ(145億1,000万米ドル)を投資します。ニーダーザクセン州、ハンブルク州、ブレーメン州、メクレンブルク=西ポメラニア州、シュレースヴィヒ=ホルシュタイン州はDBと提携し、2030年までに鉄道網の近代化に投資します。

- 2022年、欧州連合(EU)は約135の交通インフラプロジェクトへの助成金54億ユーロを承認しました。これらのプロジェクトは、EU加盟国の大洪水後の経済回復を支援し、交通網を強化し、持続可能な輸送を促進し、安全性を高め、雇用機会を創出することを目的としています。支援されるプロジェクトはすべて欧州横断交通ネットワークの一部であり、EU加盟国を結び、2030年までにTEN-Tコアネットワークを、2050年までに包括的ネットワークを完成させるというEUの目標に沿うものです。

2023年2月以降、ロシアからの輸入禁止により、中東、アジア、北米からのディーゼル輸入が増加しています。

- ガソリン価格は2022年第1四半期にユーロ圏19カ国の大半で1リットル当たり2ユーロ(2.13米ドル)を超えました。価格上昇の主な理由は、ロシアとウクライナの紛争による供給問題で、ロシアはEUの石油需要の4分の1以上を供給していました。2021年、ユーロ圏のガソリン1リットルの平均価格は1.30ユーロ(1.38米ドル)だったが、2022年の年初には1リットル当たり約1.55ユーロ(1.65米ドル)となりました。

- ロシアは欧州最大のディーゼル供給国です。2023年、欧州ではディーゼル価格が下落しました。EUがロシアからの石油製品輸入禁止を実施した2023年2月以降、ロシアから欧州へのディーゼル輸出は平均24,000バレル/日で、2022年にロシアが欧州に送った630,000バレル/日から96%減少しました。2月から5月までの欧州向けディーゼル輸出は、中東から51%(16万b/d)、アジアから97%(14万7,000b/d)、北米から65%(4万7,000b/d)増加しました。

- デンマークはガソリン価格が最も高く、フィンランドはディーゼル価格が最も高いです。オーストリアはガソリンが最も安く、スペインはディーゼルが最も安いです。英国の燃料価格は2022年に過去最高を記録し、7月の平均ガソリン価格は191.53ペソ/リットル、ディーゼル価格は199.05ペソ/リットルに達しました。2023年に入ってから、英国のガソリンスタンドの平均価格はリッター150ペソ(1.80米ドル)を突破し、ディーゼルはリッター152.41ペソ(1.83米ドル)に上昇しました。2023年1月のスペインの燃料価格は、英国よりもガソリンでリッターあたり約20セント、ディーゼルで40セント低くなりました。

欧州の道路貨物輸送産業の概要

欧州の道路貨物輸送市場は細分化されており、上位5社で5.99%を占めています。この市場の主要企業は以下の通り。 Dachser, DB Schenker, DHL Group, DSV A/S(De Sammensluttede Vognmaend af Air and Sea)and XPO, Inc.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 経済活動別GDP分布

- 経済活動別GDP成長率

- 経済パフォーマンスとプロファイル

- eコマース産業の動向

- 製造業の動向

- 運輸・倉庫業のGDP

- 物流実績

- アルバニア

- ブルガリア

- クロアチア

- チェコ共和国

- デンマーク

- エストニア

- フィンランド

- フランス

- ドイツ

- ハンガリー

- アイスランド

- イタリア

- ラトビア

- リトアニア

- オランダ

- ノルウェー

- ポーランド

- ルーマニア

- ロシア

- スロバキア共和国

- スロベニア

- スペイン

- スウェーデン

- スイス

- 英国

- 道路の長さ

- 輸出動向

- 輸入動向

- 燃料価格動向

- トラック輸送コスト

- タイプ別トラック保有台数

- 主要トラックサプライヤー

- 道路貨物トン数の動向

- 道路貨物価格動向

- モーダルシェア

- インフレ率

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 農業、漁業、林業

- 建設業

- 製造業

- 石油・ガス、鉱業、採石業

- 卸売・小売業

- その他

- 輸出先

- 国内

- 国際貨物

- トラック積載量

- 全トラック積載(FTL)

- 小口貨物(LTL)

- コンテナ輸送

- コンテナ輸送

- コンテナなし

- 距離

- 長距離輸送

- 短距離輸送

- 商品構成

- 流体商品

- 固体商品

- 温度制御

- 非温度制御

- 温度制御

- 国名

- フランス

- ドイツ

- イタリア

- オランダ

- 北欧

- ロシア

- スペイン

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- A.P. Moller-Maersk

- C.H. Robinson

- Dachser

- DB Schenker

- DHL Group

- DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

- Kuehne+Nagel

- Mainfreight

- Scan Global Logistics

- XPO, Inc.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の物流市場の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界バリューチェーン分析

- 市場力学(市場促進要因、抑制要因、機会)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

- 為替レート

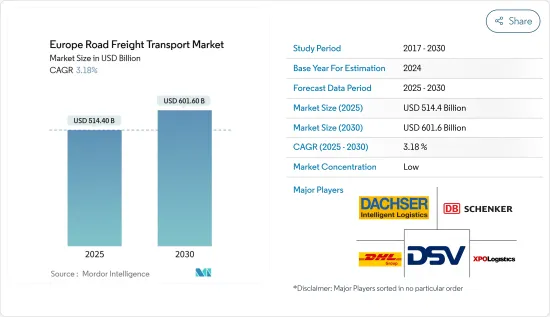

The Europe Road Freight Transport Market size is estimated at 496.83 billion USD in 2024, and is expected to reach 601.59 billion USD by 2030, growing at a CAGR of 3.24% during the forecast period (2024-2030).

Retail e-commerce surge driving advancements in the wholesale and retail trade end user segment

- In 2022, the manufacturing end-user segment grew due to the rise in human-robot collaboration, which boosted production. Germany is the fifth largest robot market globally, with 22,000 industrial robots utilized in various industries, accounting for 6% of the global robot installations as of 2021. Moreover, in 2021, the Schwarz Group, a German food retailer, emerged as the foremost retail company in Europe, with a total revenue of USD 153.75 billion within the region. In Germany, the retail sales of consumer durables were projected to increase by 1.50% YoY in 2022. This was supported by an estimated 5.40% increase in private consumption in 2022.

- In Europe's oil and gas, mining, and quarrying sectors, German regasification plans are one of the factors driving growth in the oil and gas end-user segments. Russia supplies the country's natural gas needs. As a result, Germany is expected to add the highest LNG regasification capacity in Europe between 2022 and 2026, accounting for 36% of the region's total capacity additions by 2026. In 2022, Italy's net energy import costs are expected to more than double, reaching USD 113.24 billion.

- The wholesale and retail trade end-user segment is poised for substantial growth in the upcoming years, primarily driven by the anticipated expansion of the European e-commerce industry, projected to register a compounded annual growth rate (CAGR) of 8.85 from 2023 to 2027. In the context of the German e-commerce landscape, it is projected that the market will encompass 68.4 million users by 2025, achieving a penetration rate of 81.9%, marking an increase from 80.1% in 2022.

Increasing road freight volume transported across Europe and government initiatives to develop the infrastructure are driving the growth in the market

- In 2022, the EU and extra-EU tons transported by international road freight transportation in France were major. For instance, the total EU/extra-EU transported by road between France and Switzerland held a share of 7.3% of the total tonnage transported by road, and the total EU/extra-EU transported by road between France and the United Kingdom held a share of 6.5% in 2022. Road haulage transported 68.1% of Italian goods during the first half of 2022, resulting in a 1.5% increase in transport (measured in tonne-km) compared to the previous year. The number of companies in the Italian road haulage sector reached approximately 100,797 units at the end of 2022, a rise of 1.34% from 99,465 at the end of 2021.

- The road freight transport market employs about 430,000 employees in Germany in about 35,000 road freight companies, which has been stable over the past five years. The fleet with a carrying capacity of 3.5 tons in 2021 was 964,696 in Germany and had a growth of 1.3% compared to 2020 and 3.4% over five years. The declining activity in all major economies and inflation, which led to a rise in fuel and wage costs, resulted in the decline of freight transportation through trucks between the 27th and 30th week of 2022 in the Netherlands. Since week 25, the weekly decrease in the movement of trucks was 9-21% lower than the same week in 2021.

- In the Nordics, the overseas shipments of trucks increased by 6.7% in 2022. The main destinations for truck exports from Denmark are the Netherlands, Poland, and Germany, with a combined 54% share of total exports. In the UK, the top five countries for exports and imports have remained relatively constant over time. However, exports to Germany decreased from 1.4 million tons in 2000 to 0.19 million tons in 2021.

Europe Road Freight Transport Market Trends

European Union allocated USD 5.76 billion to 135 transportation projects to boost economic recovery

- The transportation and warehouse sector plays a crucial role in supporting operations across various industries, with Germany leading as the dominant player, surpassing France and the United Kingdom. Globally, Germany ranks third in both imports and exports of goods. The German federal government expressed its intention to increase investments in transportation infrastructure, allocating over EUR 12 billion (USD 12.80 billion) for federal highways and around EUR 1.7 billion (USD 1.81 billion) for waterways in 2022, thereby demonstrating its commitment to improving transportation networks.

- The German government intends to invest more in rail than road network. In 2022, Deutsche Bahn, the federal government, and the local and regional governments invested roughly EUR 13.6 billion (USD 14.51 billion) in rail infrastructure. Lower Saxony, Hamburg, Bremen, Mecklenburg-Western Pomerania, and Schleswig-Holstein are partnering with DB to invest in modernizing their rail network by 2030.

- In 2022, the European Union approved EUR 5.4 billion through grants for approximately 135 transport infrastructural projects. These projects aim to aid post-pandemic economic recovery in the EU Member States, enhance transport links, promote sustainable transportation, boost safety, and create job opportunities. All supported projects are part of the Trans-European Transport Network, which connects EU Member States and aligns with the European Union's goal of completing the TEN-T core network by 2030 and the comprehensive network by 2050, all while aligning with climate objectives outlined in the European Green Deal.

Since February 2023, diesel imports from the Middle East, Asia, and North America have increased due to the ban on imports from Russia

- Gasoline prices surpassed EUR 2 (USD 2.13) per liter in most of the 19 eurozone countries in Q1 2022. The main reason behind the increased prices was supply issues due to the conflict between Russia and Ukraine, as Russia supplied more than a quarter of the EU's petroleum needs. In 2021, the average price for a liter of gasoline in the eurozone was EUR 1.30 (USD 1.38); at the start of 2022, the price was about EUR 1.55 (USD 1.65) per liter.

- Russia has been Europe's largest supplier of diesel. In 2023, diesel prices declined in Europe. Since February 2023, when the European Union implemented the ban on petroleum product imports from Russia, diesel exports from Russia to Europe have averaged 24,000 barrels per day (b/d), down by 96% from the 630,000 b/d Russia sent to Europe in 2022. From February through May, diesel exports to Europe increased by 51% (160,000 b/d) from the Middle East, by 97% (147,000 b/d) from Asia, and by 65% (47,000 b/d) from North America.

- Denmark is the most expensive country for petrol, and Finland is the most expensive for diesel. Austria has the cheapest petrol, and Spain is the cheapest for diesel. Fuel prices in the United Kingdom reached record highs in 2022, with the average price of petrol hitting 191.53 p-per-litre and diesel reaching 199.05 p-per-litre in July. The average cost of petrol at UK forecourts has risen to break 150p a liter (USD 1.80) since the start of 2023, and diesel has risen to 152.41p a liter (USD 1.83). Spanish fuel prices were lower than in the United Kingdom by about 20 cents per liter for petrol and 40 cents per liter for diesel in January 2023.

Europe Road Freight Transport Industry Overview

The Europe Road Freight Transport Market is fragmented, with the top five companies occupying 5.99%. The major players in this market are Dachser, DB Schenker, DHL Group, DSV A/S (De Sammensluttede Vognmaend af Air and Sea) and XPO, Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 GDP Distribution By Economic Activity

- 4.2 GDP Growth By Economic Activity

- 4.3 Economic Performance And Profile

- 4.3.1 Trends in E-Commerce Industry

- 4.3.2 Trends in Manufacturing Industry

- 4.4 Transport And Storage Sector GDP

- 4.5 Logistics Performance

- 4.5.1 Albania

- 4.5.2 Bulgaria

- 4.5.3 Croatia

- 4.5.4 Czech Republic

- 4.5.5 Denmark

- 4.5.6 Estonia

- 4.5.7 Finland

- 4.5.8 France

- 4.5.9 Germany

- 4.5.10 Hungary

- 4.5.11 Iceland

- 4.5.12 Italy

- 4.5.13 Latvia

- 4.5.14 Lithuania

- 4.5.15 Netherlands

- 4.5.16 Norway

- 4.5.17 Poland

- 4.5.18 Romania

- 4.5.19 Russia

- 4.5.20 Slovak Republic

- 4.5.21 Slovenia

- 4.5.22 Spain

- 4.5.23 Sweden

- 4.5.24 Switzerland

- 4.5.25 United Kingdom

- 4.6 Length Of Roads

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Pricing Trends

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Major Truck Suppliers

- 4.13 Road Freight Tonnage Trends

- 4.14 Road Freight Pricing Trends

- 4.15 Modal Share

- 4.16 Inflation

- 4.17 Regulatory Framework

- 4.18 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 Truckload Specification

- 5.3.1 Full-Truck-Load (FTL)

- 5.3.2 Less than-Truck-Load (LTL)

- 5.4 Containerization

- 5.4.1 Containerized

- 5.4.2 Non-Containerized

- 5.5 Distance

- 5.5.1 Long Haul

- 5.5.2 Short Haul

- 5.6 Goods Configuration

- 5.6.1 Fluid Goods

- 5.6.2 Solid Goods

- 5.7 Temperature Control

- 5.7.1 Non-Temperature Controlled

- 5.7.2 Temperature Controlled

- 5.8 Country

- 5.8.1 France

- 5.8.2 Germany

- 5.8.3 Italy

- 5.8.4 Netherlands

- 5.8.5 Nordics

- 5.8.6 Russia

- 5.8.7 Spain

- 5.8.8 United Kingdom

- 5.8.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 A.P. Moller - Maersk

- 6.4.2 C.H. Robinson

- 6.4.3 Dachser

- 6.4.4 DB Schenker

- 6.4.5 DHL Group

- 6.4.6 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.7 Kuehne + Nagel

- 6.4.8 Mainfreight

- 6.4.9 Scan Global Logistics

- 6.4.10 XPO, Inc.

7 KEY STRATEGIC QUESTIONS FOR ROAD FREIGHT CEOS

8 APPENDIX

- 8.1 Global Logistics Market Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate