中東の赤身肉:市場シェア分析、産業動向、成長予測(2025年~2030年)

Middle East Red Meat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1692046

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

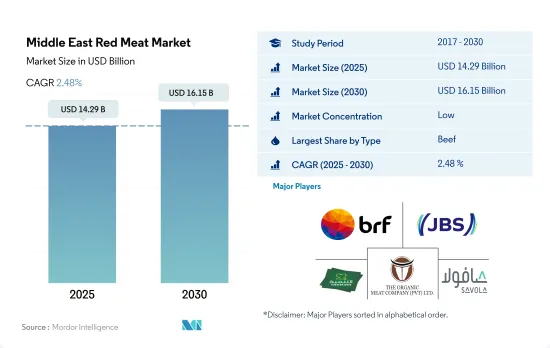

中東の赤身肉市場規模は2025年に142億9,000万米ドルと推定され、2030年には161億5,000万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは2.48%で成長する見込みです。

多様な美食の嗜好が各種食肉製品の需要を牽引する

- マトンは、バーレーンの人口の宗教的な帰属意識に大きく起因して消費される主要な赤身肉の種類です。2023年のバーレーンの人口は1,485,509人で、2022年から0.9%増加しました。バーレーン、カタール、クウェートの一人当たりのマトン消費量はこの地域で最も多いです。バーレーンにおけるマトン消費量の増加は、可処分所得の増加に起因しています。バーレーンの国民1人当たりの可処分所得は、2022年には22,707.50米ドルでした。また、過去20年間に欧米やアジア諸国からの外国人駐在員人口が増加し、ハンバーガーのような品目を含め、より多様な美食の嗜好が見られるようになりました。

- マトンやその他の肉類を除けば、豚肉がこの地域で最も急速に消費される肉類となり、予測期間中のCAGRは10.50%と予想されます。同地域では、外国人人口の増加により豚肉の需要が増加しています。2022年には、UAEの人口の12.9%がキリスト教徒でした。同様に、キプロス(クリスチャン人口78%)、レバノン、エジプトなどの他の中東諸国もクリスチャン人口が多いです。この層は豚肉を含むあらゆる種類の赤身肉を消費するため、消費量が多くなります。

- 牛肉はこの地域で2番目に消費量の多い肉であり、バーレーンは1人当たりの牛肉消費量が最も多く、2023年には15.80kgに達しました。同国はニュージーランド、パキスタン、アラブ首長国連邦からの牛肉輸入に依存しています。オンライン・チャネルで購入できる生鮮肉のほとんどは、ニュージーランドのビーフ・サーロイン、トップサイド・ステーキ、シルバーサイド・ステーキです。今後の開発は、特にサウジアラビアのような観光産業の発展を目指す国々での高級外食に期待されます。

自給自足への取り組みが市場の成長を後押しすると予想される

- 中東における赤身肉の消費量は、2017年から2022年にかけて金額ベースで20.61%の伸びを示しました。中東、特に湾岸協力会議(GCC)諸国では、豊かな人口が増えているため、輸入肉への支出が高くなる傾向があります。中東の消費者が赤身肉の購入を決定する際に考慮する主な要因は、品質、ハラル保証、味です。しかし、中東の消費者が牛肉や羊肉を購入する主な理由は持続可能性ではないです。

- 2022年にはサウジアラビアが金額ベースで主要シェアを占め、CAGRも最高となりました。サウジアラビアの赤身肉市場は2017年から2022年にかけて17.36%成長しました。消費の増加は、可処分所得の増加と現地生産に起因する需要の増加の結果です。サウジアラビアは、サウジアラビア食品医薬品局(SFDA)が定めるハラル基準が非常に高く、これが消費者、特にイスラム教徒のサウジアラビア製製品に対する信頼を高めるのに役立っています。同国では、多忙なライフスタイルや働く女性の増加などを背景に、加工赤身肉が最も急成長しています。

- オマーンは予測期間中、赤身肉の消費国として2番目に急成長すると予想されます。金額ベースでは2.23%の成長が見込まれます。自給自足を支援するための政府からの投資の増加が成長に重要な役割を果たすと予想されます。赤身肉企業を含む国営企業は、引き続き生産を強化し、投資機会を提供しています。オマーンにおける赤身肉の消費は、主にオマーンの消費者の宗教的信条に起因するマトンが大部分を占めています。マトンはシャワルマ、ケバブ、ビリヤニなどの伝統料理によく使われます。

中東の赤身肉市場の動向

域内のサプライチェーンが未発達なことが牛肉生産の足かせに

- 同地域の牛肉生産量は2022年には2021年から7.92%減少しました。サウジアラビアがこの地域の牛肉生産の主要シェアを占める。しかし、サウジアラビアでは牛肉生産が減少しています。2022年の同国の牛肉生産量は21.63%減少し、2021年の4万トンから2022年には3万1,000トンに減少しました。サウジアラビアの主要な牛肉供給源は輸入です。サウジアラビアの牛肉輸入量は、2021年と比較して2022年には1.54%増加しました。2021年にはインド、ブラジル、オーストラリアがサウジアラビアへの主な牛肉輸出国であり、インドは約2万7,000トンを輸出しています。輸入冷凍製品の最大賞味期限が変更されたことで、米国のメーカーはサウジアラビアでの売上増を期待しています。

- カタールの牛肉生産量は指数関数的に減少しており、2022年には前年比43.74%減となりました。カタールの牛肉生産量は2021年の1,644トンから2022年には925トンに達しました。しかし、ウシのバリューチェーンは未発達であり、生きたウシは輸入され、現地で食肉処理されています。牛のような大型動物の肥育には大量の水と飼料が必要です。

- バーレーンの生産量はこの地域で最も少ないです。しかし、2022年の牛肉生産量は3.40%増加しました。バーレーンの牛肉市場はラマダン(断食月)シーズンに大きな需要があります。自治体・農業省の畜産資源担当次官によると、同国は十分な在庫を確保するため、羊10,500頭、牛1,077頭、ラクダ40頭を含む11,611頭の家畜を輸入し、2023年のラマダン・シーズンには合計27,000頭の家畜が入手可能となります。

この地域では、高級食肉製品に対する需要が高まっています。

- クウェートとバーレーンは湾岸地域で最も高い価格を記録しました。2022年、牛肉1kgの価格はバーレーンで4.91米ドル、クウェートで4.93米ドルであったのに対し、アラブ首長国連邦とサウジアラビアでは4米ドル以下でした。

- 中東諸国では富裕層が多いため、高級肉への支出が多いです。過去8年間、アラブ首長国連邦(UAE)とサウジアラビアは、オーストラリアにとって最も価値のある牛肉輸出市場トップ20に常にランクインしています。2022年10月、オーストラリアの牛肉価格は2.82米ドル/1kgに達し、輸出の増加により前週比5.3%、前年同月比5.1%上昇しました。急速な都市化による経済成長の加速、可処分所得の増加、観光客の増加により、洋風外食はここ10年で急成長しました。このため、高品質の牛肉等級とカットへの需要が高まっています。

- サウジアラビア食品医薬品局(SFDA)は、米国産チルド牛肉の賞味期限を70日から120日に拡大しました。この措置により、米国の輸出業者は海上輸送による輸送コストの削減により、1kgあたり少なくとも4米ドルのコスト削減が期待できる一方、サウジアラビアの輸入業者は米国産牛肉をより大量に購入する柔軟性を得ることができます。サウジアラビアの輸入業者が米国産牛肉を販売できる期間は、従来の規制ではわずか数週間であったが、現在では少なくとも70日間となりました。賞味期限が延びることで、直前になって急な値引き販売をする必要が最小限に抑えられるため、この余分な時間によって収益性が向上することが期待されています。

中東の赤身肉産業の概要

中東の赤身肉市場は細分化されており、上位5社で2.64%を占めています。この市場の主要企業は以下の通り。 BRF S.A., JBS SA, Tanmiah Food Company, The Organic Meat Company Ltd and The Savola Group(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 価格動向

- 牛肉

- マトン

- 豚肉

- 生産動向

- 牛肉

- マトン

- 豚肉

- 規制の枠組み

- サウジアラビア

- アラブ首長国連邦

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- タイプ

- 牛肉

- マトン

- 豚肉

- その他の食肉

- 形態

- 缶詰

- 生鮮・冷蔵

- 冷凍

- 加工

- 流通チャネル

- オフ・トレード

- コンビニエンスストア

- オンライン・チャネル

- スーパーマーケットとハイパーマーケット

- その他

- オン・トレード

- オフ・トレード

- 国名

- バーレーン

- クウェート

- オマーン

- カタール

- サウジアラビア

- アラブ首長国連邦

- その他中東

第5章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Almunajem Foods

- BRF S.A.

- Golden Gate Meat Company

- JBS SA

- Kibsons International LLC

- Tanmiah Food Company

- The Organic Meat Company Ltd

- The Savola Group

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 90341

The Middle East Red Meat Market size is estimated at 14.29 billion USD in 2025, and is expected to reach 16.15 billion USD by 2030, growing at a CAGR of 2.48% during the forecast period (2025-2030).

A diverse range of gastronomic preferences drives the demand for various meat products

- Mutton is the major red meat type consumed largely due to the religious affiliations of Bahrain's population. The population of Bahrain in 2023 was 1,485,509, a 0.9% increase from 2022. Bahrain, Qatar, and Kuwait have the highest per capita consumption of mutton in the region. The rise in mutton consumption in Bahrain can be attributed to increased disposable incomes. Bahrain's gross national disposable income per capita was USD 22,707.50 in 2022. The country also saw an increase in the ex-pat population from Western and Asian nations in the past two decades, leading to a more diverse range of gastronomic preferences, including items like hamburgers.

- Apart from mutton and other meat, pork is expected to be the fastest-growing meat consumed in the region, with an anticipated CAGR of 10.50% during the forecast period. The demand for pork increased in the region due to the increased ex-pat population. In 2022, 12.9% of the UAE population was Christian. Similarly, other Middle Eastern countries like Cyprus (which has a 78% Christian population), Lebanon, and Egypt have a high Christian population. This population group consumes all types of red meat, including pork, resulting in higher consumption.

- Beef is the second most consumed meat in the region, and Bahrain has the highest per capita beef consumption, which amounted to 15.80 kg in 2023. The country relies on beef imports from New Zealand, Pakistan, and the United Arab Emirates. Most fresh meat cuts available through online channels are New Zealand's Beef Sirloin, Topside Steak, and Silverside Steak. Future growth is expected to be in high-end food service, particularly in countries such as Saudi Arabia that are looking to develop their tourism industries.

Initiatives for self-sufficiency are anticipated to boost the market's growth

- The red meat consumption in the Middle East observed a growth of 20.61% by value from 2017 to 2022. The expenditure on imported meat tends to be higher in the Middle East, particularly in the Gulf Cooperation Council (GCC) countries, owing to a growing and affluent population. Quality, halal assurance, and taste are the major factors considered by consumers in the Middle East when making red meat purchasing decisions. However, sustainability is not the main reason Middle Eastern consumers buy beef and lamb.

- Saudi Arabia held the major share and highest CAGR by value in 2022. The red meat market in Saudi Arabia grew by 17.36% from 2017 to 2022. The increased consumption was a result of increased demand attributed to the increased disposable income and local production. Saudi Arabia has very high halal standards set by the Saudi Food and Drug Authority (SFDA), and this helps increase the confidence of consumers, especially the Muslim population, in Saudi-made products. Processed red meat is the fastest growing segment in the country owing to the busy lifestyles, increasing number of working women, and other factors.

- Oman is anticipated to be the second fastest-growing red meat-consuming country during the forecast period. It is anticipated to register a growth of 2.23% by value. Increasing investments from the government to support self-sufficiency are expected to play an important part in the growth. State-backed enterprises, including the red meat companies, continue to enhance production and are offered investment opportunities. Consumption of red meat in Oman is largely dominated by mutton, mainly due to the religious affiliation of Omani consumers. Mutton is often used in traditional dishes such as shawarma, kebabs, and biryani.

Middle East Red Meat Market Trends

Underdeveloped local supply chain in the region is a restraint to the production of beef

- Beef production in the region declined by 7.92% in 2022 from 2021. Saudi Arabia accounted for the region's major share of beef production. However, beef production is declining in Saudi Arabia. In 2022, beef production in the country dropped by 21.63%, registering a decline from 40 thousand tons in 2021 to 31 thousand tons in 2022. Imports account for the major beef source in Saudi Arabia. The country's beef imports grew at a rate of 1.54% in 2022 compared to 2021. India, Brazil, and Australia were the major exporters of beef to Saudi Arabia in 2021, with India exporting around 27 thousand tons. With the change in the maximum shelf life of imported frozen products, manufacturers from the United States are hoping that will result in increased sales growth in the Kingdom.

- Qatar has an exponential decline in beef production, and it had a decline of 43.74% in 2022 compared to the previous year. Qatar's beef production reached 925 tons in 2022 from 1644 tons in 2021. However, the local value chain of the bovine category is underdeveloped, and live bovine animals are imported for local slaughtering. Large amounts of water and animal feed are required for fattening large animals such as cattle.

- Bahrain accounted for the lowest production in the region. However, the country saw growth in the production of beef by 3.40% in 2022. The beef market in Bahrain sees a huge demand during the Ramadan season. According to the Ministry of Municipalities Affairs and Agriculture Undersecretary for Animal Wealth Resources, the country imported 11,611 heads of livestock, including 10,500 heads of sheep, 1,077 heads of cattle, and 40 heads of camels, to ensure sufficient stock, bringing the total availability to 27,000 heads of livestock during the Ramadan season of 2023.

The region has observed a growing demand for premium meat products

- Kuwait and Bahrain recorded the highest prices for essential goods in the Gulf region. In 2022, 1 kg of beef was priced at USD 4.91 in Bahrain and USD 4.93 in Kuwait, whereas in the United Arab Emirates and Saudi Arabia, it was priced below USD 4. The reliance of Gulf countries on imports for necessities, including beef and beef products, is one of the leading causes of price increases.

- Spending on premium meat is high in Middle Eastern countries owing to their large affluent populations. For the past eight years, the United Arab Emirates (UAE) and Saudi Arabia have consistently ranked among Australia's top 20 most valuable beef export markets. In October 2022, the price of beef in Australia reached USD 2.82/1 kg, up by 5.3% week on week and 5.1% year on year (Y-o-Y), owing to rising exports. Western-style food services have grown rapidly in the last decade due to accelerated economic growth driven by rapid urbanization, rising disposable incomes, and increased tourism. This has increased demand for high-quality beef grades and cuts.

- The Saudi Food and Drug Authority (SFDA) has expanded the shelf life for chilled beef from the United States from 70 to 120 days. This measure is expected to help US exporters save at least USD 4 per kg due to lower transportation costs using sea transportation while providing Saudi Arabian importers with the flexibility to purchase larger quantities of US beef. Instead of just a few weeks as per the prior regulation, Saudi Arabian importers now have at least 70 days to sell American beef. The extra time is expected to increase profitability since a longer shelf life minimizes the need for last-minute panic sales at steep discounts.

Middle East Red Meat Industry Overview

The Middle East Red Meat Market is fragmented, with the top five companies occupying 2.64%. The major players in this market are BRF S.A., JBS SA, Tanmiah Food Company, The Organic Meat Company Ltd and The Savola Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Beef

- 3.1.2 Mutton

- 3.1.3 Pork

- 3.2 Production Trends

- 3.2.1 Beef

- 3.2.2 Mutton

- 3.2.3 Pork

- 3.3 Regulatory Framework

- 3.3.1 Saudi Arabia

- 3.3.2 United Arab Emirates

- 3.4 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Type

- 4.1.1 Beef

- 4.1.2 Mutton

- 4.1.3 Pork

- 4.1.4 Other Meat

- 4.2 Form

- 4.2.1 Canned

- 4.2.2 Fresh / Chilled

- 4.2.3 Frozen

- 4.2.4 Processed

- 4.3 Distribution Channel

- 4.3.1 Off-Trade

- 4.3.1.1 Convenience Stores

- 4.3.1.2 Online Channel

- 4.3.1.3 Supermarkets and Hypermarkets

- 4.3.1.4 Others

- 4.3.2 On-Trade

- 4.3.1 Off-Trade

- 4.4 Country

- 4.4.1 Bahrain

- 4.4.2 Kuwait

- 4.4.3 Oman

- 4.4.4 Qatar

- 4.4.5 Saudi Arabia

- 4.4.6 United Arab Emirates

- 4.4.7 Rest of Middle East

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 Almunajem Foods

- 5.4.2 BRF S.A.

- 5.4.3 Golden Gate Meat Company

- 5.4.4 JBS SA

- 5.4.5 Kibsons International LLC

- 5.4.6 Tanmiah Food Company

- 5.4.7 The Organic Meat Company Ltd

- 5.4.8 The Savola Group

6 KEY STRATEGIC QUESTIONS FOR MEAT INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

中東の赤身肉:市場シェア分析、産業動向、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日