|

市場調査レポート

商品コード

1690978

北米のエンドウタンパク原料:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)North America Pea Protein Ingredients - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のエンドウタンパク原料:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 223 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

北米のエンドウタンパク原料市場規模は2025年に4億9,270万米ドルと推定され、2030年には6億800万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは4.30%で成長すると予測されます。

2022年は代替食肉製品の需要増で飲食品セグメントが大きなシェアを占める

- 北米では、飲食品セグメントがエンドウタンパクの主要ユーザーとして際立っており、特に代替肉とRTE/RTC食品に重点を置いています。2022年現在、これらのサブセグメントは合計で同地域のエンドウタンパク消費量の57%を占めています。さらに、調査期間中にCAGRが4.47%になると予測されるサプリメントセグメントは、エンドウタンパクのもう一つの重要な市場として台頭してくると予想されます。この成長は、サプリメントが毎日の食事に不可欠で栄養価の高い添加物としてますます受け入れられているという、より広範な変化を浮き彫りにしています。

- 植物性タンパクベースの食品や飲食品への嗜好の高まりは、この産業への戦略的投資の主要企業へとつながっています。北米は植物性食肉にとって世界的に確立された主要市場のひとつになりつつあり、エンドウタンパクに関しては食肉と食肉代替物部門が最も急成長すると予想されています。このセグメントは予測期間中にCAGR 10.48%を記録すると予測されています。

- 北米では菜食主義が普及しています。菜食主義に切り替え、植物由来の製品のみを購入する人が増えています。ヴィーガン食の受け入れ拡大は、植物性タンパクサプリメントメーカーにとって有利になると予想されます。2021年には、米国人口の0.5%(162万人)が菜食主義者になると推定されています。少数のアメリカ人が菜食主義者ではあるが、実際には、完全な菜食主義者ではないが、菜食主義者を目指している人の数ははるかに多いです。アメリカ人の約39%が、食生活は植物性食品だけではないが、できるだけ動物性食品を避けて完全菜食主義者になりたいと述べています。

主に米国が支配的なこの地域では、飲食品全般に多用途性が広く受け入れられており、これがセグメントの成長に影響を及ぼしています。

- 米国は2022年に同地域でトップの座を維持し、2017~2022年に金額ベースで36.83%の成長を記録しました。エンドウタンパクは、様々な用途における汎用性が消費者に広く受け入れられているため、同国で大きな支持を得ています。製造業者もまた、栄養的、機能的、表示上の目的を満たす能力を引用して、エンドウタンパクを好んでいます。米国に次いで、メキシコ、カナダが食品・飲食品セグメントに牽引され、市場規模を伸ばしています。

- エンドウタンパクの需要増に対応し、米国企業は生産を拡大しています。2021年、カーギルのピュリスはエンドウタンパク生産量の倍増を目指し、新施設を稼働させました。同様に、イングレディオンは植物由来のソリューションを拡大し、ネブラスカ州の施設で2種類のエンドウ豆ベースの原料を導入しました。こうした競合の躍進が飲食品セグメントの成長を後押しし、予測期間中のエンドウタンパクのCAGRは数量ベースで5.49%に達する見込みです。

- メキシコは世界のエンドウタンパク市場のトップランナーとして際立っており、2023~2029年の予測CAGRは金額ベースで8.05%です。メキシコの伝統的肉食中心の食生活に関連する、特に心血管疾患や肥満といった健康問題に対する懸念の高まりが、より健康的な選択肢へのシフトを促しています。メキシコ人の約73%が太りすぎと分類されていることから、エンドウ豆ベースのタンパク製品への動向が大きく高まり、市場調査が強化されると予想されます。

北米のエンドウ豆タンパク原料市場の動向

植物性タンパク消費の成長が原料産業の主要企業に機会を与える

- 2017~2022年にかけて、同地域では投資と技術革新が原動力となり、一人当たりの植物性タンパク消費量が2.42%増加しました。この急増は主に、動物愛護への懸念が主要動機となってヴィーガンまたはベジタリアン食にシフトする消費者の増加によって促進されました。2020年には、さらに約960万人の米国人が植物ベースの食生活を採用し、米国人口の3%近くを占めることになります。COVID-19の大流行後、植物性タンパクの消費量が急増したが、これは動物性タンパクのウイルス汚染に対する懸念や、動物性と植物性の両方を含むタンパク配合の一般的な増加も一因となっています。

- ほとんどのアメリカ人は肉の摂取量を減らしているが、厳格な菜食主義やベジタリアンというよりは、フレキシタリアン的な食事に傾いています。植物性タンパクは、スポーツ栄養学や肉の代替品として重要な用途を見出しています。特に大豆と乳清タンパクは、飲食品、サプリメント、スポーツ栄養に広く使われています。2021年までに、米国の消費者の36%が大豆タンパクをよく知り、摂取したことがあり、ホエイ・タンパクを試したことがある人の割合は31%とやや低いです。

- カナダは第2位のフレキシタリアン人口を誇り、消費者の間でフレキシタリアニズムと菜食主義への大きなシフトが見られます。この動向は、メーカーが植物性タンパク市場をさらに革新する絶好の機会を提供しています。2021年、カナダ政府は、持続可能で高品質な植物性タンパクに対する消費者の欲求の高まりに合わせて、同国の豆類・特別栽培作物農業従事者を強化するために430万米ドル以上を拠出することを約束しました。

米国とカナダは北米の主要エンドウ豆生産国です。

- 乾燥エンドウ豆は、エンドウ豆タンパクを抽出する主原料となります。カナダは北米における乾燥エンドウ豆の主要生産国として際立っており、米国が僅差で続いています。カナダでは、サスカチュワン州、アルバータ州、マニトバ州などがドライエンドウの栽培でリードしています。北米では、2015~2020年にかけてエンドウ豆の生産量が32%増加しました。2020年までに、この地域の焦点は乾燥エンドウ豆の生産に顕著に移行し、エンドウ豆生産量全体の95%を占めるようになりました。

- 予測では、収量の向上に牽引され、乾燥エンドウ豆の生産は引き続き増加するとしています。注目すべきは、収穫面積が少ないにもかかわらず、アルバータ州では2020年の収量が増加することです。カナダ政府の予測では、アルバータ州とサスカチュワン州を合わせて410万トンのドライエンドウ生産を目標とし、残りをマニトバ州、ブリティッシュコロンビア州、カナダ東部で分け合うとしています。対照的に、米国は主にノースダコタ州での播種量の減少により、収量の低下と放棄豆の増加という生産課題に直面しました。米国農務省の2020~2021年の予測では、米国のドライエンドウ生産量は17%減少し、80万トンをわずかに上回る程度にとどまる。

- カナダの堅調な乾燥エンドウ豆生産は、エンドウ豆タンパク加工工場を国内に設置するメーカーを誘致しています。この戦略的な動きは、カナダの生産力を活用するだけでなく、サプライチェーンのコスト、特に輸送と保管にかかるコストの削減にも役立ちます。その代表的な例が、北米の大手エンドウ豆タンパクメーカーであるロケット社で、同社は2021年11月、カナダのポーテージ・ラ・プレーリーに世界最大のエンドウ豆タンパク施設を開設しました。この最先端工場は、黄えんどう豆を繊維、タンパク、デンプンに加工することに特化しており、特に製薬セグメントなど多様な用途に対応しています。

北米エンドウ豆タンパク原料産業概要

北米のエンドウ豆タンパク原料市場はセグメント化されており、上位5社で21.59%を占めています。この市場の主要企業は、 Archer Daniels Midland Company、Bunge Limited、International Flavors & Fragrances、Inc.、Kerry Group PLC、The Scoular Companyなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- エンドユーザー市場規模

- ベビーフードと乳児用調製粉乳

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品と乳製品代替製品

- 高齢者栄養・医療栄養

- 肉・鶏肉・魚介類と肉代替製品

- RTE/RTC食品

- スナック

- スポーツ/パフォーマンス栄養

- 動物飼料

- パーソナルケアと化粧品

- タンパク消費動向

- 植物

- 生産動向

- 植物

- 規制の枠組み

- 米国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 形態

- 濃縮物

- 単離液

- テクスチャー/加水分解

- エンドユーザー

- 飼料

- 飲食品

- サブエンドユーザー別

- ベーカリー

- 飲料

- 朝食用シリアル

- 調味料/ソース

- 菓子類

- 乳製品・乳製品代替品

- 肉・鶏肉・魚介類と肉代替製品

- RTE/RTC食品

- スナック

- パーソナルケアと化粧品

- サプリメント

- サブエンドユーザー別

- ベビーフードと乳児用調製粉乳

- 高齢者栄養と医療栄養

- スポーツ/パフォーマンス栄養

- 国別

- カナダ

- メキシコ

- 米国

- その他の北米地域

第5章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Archer Daniels Midland Company

- Bunge Limited

- Cargill Incorporated

- Farbest-Tallman Foods Corporation

- Glanbia PLC

- Ingredion Incorporated

- International Flavors & Fragrances, Inc.

- Kerry Group PLC

- Roquette Freres

- The Scoular Company

第6章 CEOへの主要戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

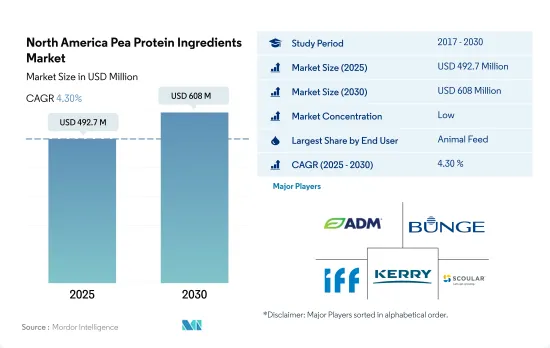

The North America Pea Protein Ingredients Market size is estimated at 492.7 million USD in 2025, and is expected to reach 608 million USD by 2030, growing at a CAGR of 4.30% during the forecast period (2025-2030).

The food and beverage segment accounted for a major share in 2022, with a growing demand for alternative meat products

- In North America, the food and beverage segment stands out as the primary user of pea proteins, with a particular focus on meat alternatives and RTE/RTC food items. As of 2022, these sub-segments collectively dominated, accounting for 57% of the region's pea protein consumption. Additionally, the supplements segment, projected to witness a CAGR of 4.47% during the study period, is expected to emerge as another pivotal market for pea proteins. This growth underscores a broader shift, where supplements are increasingly embraced as integral, nourishing additions to daily diets.

- The increasing preference for plant protein-based foods and beverages is leading companies to invest strategically in the industry. North America is becoming one of the prime established markets for plant-based meat globally, with the meat and meat alternatives segment expected to grow the fastest with respect to pea protein. The segment is projected to register a CAGR of 10.48% during the forecast period.

- In North America, veganism is becoming more popular. More people are switching to vegan diets and only buying plant-based products. The increasing acceptance of vegan diets is anticipated to be advantageous for manufacturers of plant-based protein supplements. In 2021, 0.5% of the US population (1.62 million) was estimated to be vegan. While a small number of Americans are vegan, in reality, the number of people who are not completely vegan but aspire to be is far higher. About 39% of Americans state that their diets do not consist entirely of plant-based foods, but they want to become fully vegan by avoiding as many animal-related foods as possible.

Widespread acceptance of versatility across food and beverages in the region, primarily dominated by the United States, impacts the segmental growth

- The United States retained its top position in the region in 2022 and registered a growth of 36.83% by value during 2017-2022. Pea protein has gained significant traction in the country due to widespread consumer acceptance of versatility across different applications. Manufacturers also prefer pea protein, quoting its ability to meet nutritional, functional, and label objectives. The United States was followed by Mexico and Canada in terms of market value, driven by the food and beverages segment.

- Responding to the escalating demand for pea protein, US companies are scaling up their production. In 2021, Cargill's Puris inaugurated a new facility, aiming to double its pea protein output. Likewise, Ingredion broadened its plant-based solutions, introducing two pea-based ingredients at its Nebraska facility. These competitive strides are set to fuel the growth of the food and beverages segment, with pea protein poised to achieve a CAGR of 5.49% by volume during the forecast period.

- Mexico stands out as the frontrunner in the global pea protein market, with a projected CAGR of 8.05% by value during 2023-2029. Rising concerns over prevalent health issues, notably cardiovascular diseases and obesity, linked to Mexico's traditional meat-heavy diet, are prompting a shift toward healthier options. With approximately 73% of Mexicans classified as overweight, the trend toward pea-based protein products is expected to flourish significantly, bolstering the market studied.

North America Pea Protein Ingredients Market Trends

Plant protein consumption growth fuels opportunities for key players in the ingredients industry

- From 2017 to 2022, the region saw a 2.42% increase in per capita plant protein consumption, driven by investments and innovations. This surge was primarily fueled by a growing number of consumers shifting toward vegan or vegetarian diets, largely motivated by concerns for animal welfare. Notably, in 2020, approximately 9.6 million more Americans adopted plant-based diets, constituting nearly 3% of the US population. After the COVID-19 pandemic, plant protein consumption surged, partly due to concerns over viral contamination in animal-sourced proteins and a general increase in protein blends, including both animal and plant sources.

- While most Americans are reducing their meat intake, they are not eliminating it, leaning more toward a flexitarian diet than strict veganism or vegetarianism. Plant proteins find significant usage in sports nutrition and as meat alternatives. Soy and whey proteins, in particular, are prevalent in food and beverage, supplements, and sports nutrition. By 2021, 36% of US consumers were familiar with and had consumed soy protein, with a slightly lower share of 31% having tried whey protein.

- Canada boasts the second-largest flexitarian population, showcasing a significant shift toward flexitarianism and veganism among consumers. This trend presents a ripe opportunity for manufacturers to further innovate in the plant protein market. In 2021, the Canadian government pledged over USD 4.3 million to bolster the country's pulse and special crop farmers, aligning with the rising consumer appetite for sustainable, high-quality plant-based proteins.

United States and Canada are the major pea producers across North America

- Dry peas serve as the primary raw material for extracting pea protein. Canada stands out as the leading producer of dry peas in North America, closely trailed by the United States. In Canada, provinces such as Saskatchewan, Alberta, and Manitoba lead in dry pea cultivation. North America witnessed a substantial 32% rise in pea production from 2015 to 2020. By 2020, the region's focus had notably shifted toward dry pea production, representing a dominant 95% of the total pea output.

- Forecasts indicate a continued rise in dry pea production, driven by improving yields. Notably, despite a smaller harvested area, Alberta saw heightened yields in 2020. The Canadian government's projections highlight Alberta and Saskatchewan targeting a combined dry pea production of 4.1 million metric tons, with the rest shared among Manitoba, British Columbia, and Eastern Canada. In contrast, the US faced production challenges, primarily due to reduced seeding in North Dakota, leading to both lower yields and increased abandonment. The USDA's estimates for 2020-2021 suggested a 17% drop in US dry pea production, settling just above 0.8 million metric tons.

- Canada's robust dry pea production is enticing manufacturers to set up pea protein processing plants in the country. This strategic move not only leverages Canada's production strength but also helps in curtailing supply chain costs, especially in transportation and storage. A prime example is Roquette, a major North American pea protein producer, which, in November 2021, inaugurated the world's largest pea protein facility in Portage la Prairie, Canada. This cutting-edge plant specializes in processing yellow peas into fibers, proteins, and starch, catering to diverse applications, notably in the pharmaceutical sector.

North America Pea Protein Ingredients Industry Overview

The North America Pea Protein Ingredients Market is fragmented, with the top five companies occupying 21.59%. The major players in this market are Archer Daniels Midland Company, Bunge Limited, International Flavors & Fragrances, Inc., Kerry Group PLC and The Scoular Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 End User Market Volume

- 3.1.1 Baby Food and Infant Formula

- 3.1.2 Bakery

- 3.1.3 Beverages

- 3.1.4 Breakfast Cereals

- 3.1.5 Condiments/Sauces

- 3.1.6 Confectionery

- 3.1.7 Dairy and Dairy Alternative Products

- 3.1.8 Elderly Nutrition and Medical Nutrition

- 3.1.9 Meat/Poultry/Seafood and Meat Alternative Products

- 3.1.10 RTE/RTC Food Products

- 3.1.11 Snacks

- 3.1.12 Sport/Performance Nutrition

- 3.1.13 Animal Feed

- 3.1.14 Personal Care and Cosmetics

- 3.2 Protein Consumption Trends

- 3.2.1 Plant

- 3.3 Production Trends

- 3.3.1 Plant

- 3.4 Regulatory Framework

- 3.4.1 United States

- 3.5 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Form

- 4.1.1 Concentrates

- 4.1.2 Isolates

- 4.1.3 Textured/Hydrolyzed

- 4.2 End User

- 4.2.1 Animal Feed

- 4.2.2 Food and Beverages

- 4.2.2.1 By Sub End User

- 4.2.2.1.1 Bakery

- 4.2.2.1.2 Beverages

- 4.2.2.1.3 Breakfast Cereals

- 4.2.2.1.4 Condiments/Sauces

- 4.2.2.1.5 Confectionery

- 4.2.2.1.6 Dairy and Dairy Alternative Products

- 4.2.2.1.7 Meat/Poultry/Seafood and Meat Alternative Products

- 4.2.2.1.8 RTE/RTC Food Products

- 4.2.2.1.9 Snacks

- 4.2.3 Personal Care and Cosmetics

- 4.2.4 Supplements

- 4.2.4.1 By Sub End User

- 4.2.4.1.1 Baby Food and Infant Formula

- 4.2.4.1.2 Elderly Nutrition and Medical Nutrition

- 4.2.4.1.3 Sport/Performance Nutrition

- 4.3 Country

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.3.4 Rest of North America

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 5.4.1 Archer Daniels Midland Company

- 5.4.2 Bunge Limited

- 5.4.3 Cargill Incorporated

- 5.4.4 Farbest-Tallman Foods Corporation

- 5.4.5 Glanbia PLC

- 5.4.6 Ingredion Incorporated

- 5.4.7 International Flavors & Fragrances, Inc.

- 5.4.8 Kerry Group PLC

- 5.4.9 Roquette Freres

- 5.4.10 The Scoular Company

6 KEY STRATEGIC QUESTIONS FOR PROTEIN INGREDIENTS INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms