|

市場調査レポート

商品コード

1687488

英国の外食産業:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)United Kingdom Foodservice - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国の外食産業:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 231 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

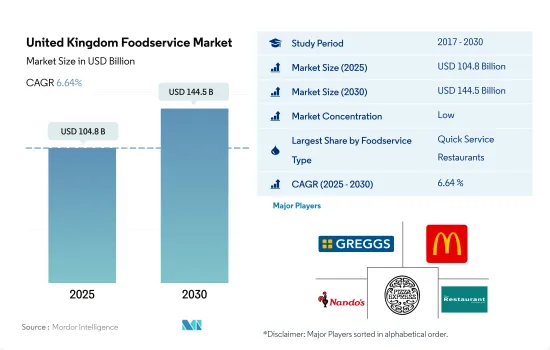

英国の外食産業市場規模は2025年に1,048億米ドルと推定・予測され、2030年には1,445億米ドルに達し、予測期間(2025年~2030年)のCAGRは6.64%で成長すると予測されます。

国内でのコーヒー・紅茶消費の増加、特にスペシャルティ茶・コーヒーが市場成長を牽引

- クイックサービス・レストラン分野は、雰囲気、衛生面、サービス時間、アクセスのしやすさなどの点で、食品アウトレットチェーン全体で標準化が進んでいるため、予測期間中に金額ベースでCAGR 5.25%を記録すると予想されます。これにより、消費者の関心が高まり、全体的な来店者数が増加すると予想されます。

- しかし、クラウドキッチンは、特にCOVID-19の流行後、消費者によるオンラインデリバリー嗜好が活況を呈しており、予測期間中にCAGR 32.39%の急成長を記録すると予想されます。同国では2021年にオンライン・デリバリーが110%増加しました。さらに、クラウドキッチンが少ない投資でメーカーに提供する手頃な価格が、英国におけるクラウドキッチンの成長を後押ししています。

- フルサービスレストラン市場は、調査期間中に金額ベースでCAGR 6.83%を記録しました。2022年の市場シェアは欧州料理が約47%を占め、最大でした。このセグメントの成長は、レストランが伝統的な欧州料理にビーガン、低糖質、グルテンフリーのオプションを導入したことに起因しています。英国では栄養食に対する需要が高まっているため、FSR店舗はこれらの料理をよりヘルシーで消費者にアピールできるものにしようとしています。

- カフェ&バーの成長は、同国における紅茶とコーヒーの消費量の増加、特にスペシャルティーティー/コーヒーカテゴリーに支えられています。英国の消費者の約70%は、1日に少なくとも2杯以上のコーヒーを飲みます。さらに、コーヒーを飲む人の23%が1日3杯以上、21%が1日4杯以上のコーヒーを定期的に飲んでいます。したがって、英国のカフェ&バー分野は予測期間中に金額ベースで5.01%のCAGRで推移すると予測されます。

英国の外食産業市場動向

英国のQSR市場は緩やかに成長し、米国系チェーンが人気を集める

- 英国のクイックサービスレストランの数は、調査期間中にCAGR 2.24%を記録しました。成長率が緩やかなのは、主にパンデミックによる経営上の制約が原因です。英国の世界的に有名なブランドの中では、グレッグスPLCが英国国民の間で最も高い評価を得ており、67%の好意的な意見でした。ピザ・エクスプレス、KFC、ピザ・ハット、コスタ・コーヒーも2022年時点で上位5ブランドに入っています。英国国民は、ハンバーガー、タコス、ピザなど、アメリカのファーストフードチェーンが提供するファーストフードに旺盛な食欲を示しており、アメリカの大手企業が進出する良いきっかけを与えています。例えば、世界第3位のハンバーガー・チェーンであるウェンディーズは、2022年から2023年にかけて50店舗を新規オープンする計画を発表しました。

- 2022年には、カフェとバーが外食産業業態の中で最も多くの店舗数を記録しました。2020年には、一人当たり平均130ミリリットルの温かい飲み物(コーヒー、紅茶、ホットチョコレート)が自宅以外で週に消費されており、これらの店舗が成長する十分な機会を与えています。現在、国内のコーヒーショップの数はバーやパブの数を下回っているが、逆転する見込みです。英国では毎日3軒のコーヒーショップが新規開店しており、パブの数は減少しています。ロンドンのパブやバーの数は2001年の4,835軒から2016年には3,615軒に減少しているが、コーヒーショップは2倍以上に増加しています。

- クラウドキッチンは予測期間中に14.79%のCAGRで推移すると予測されています。2022年には、このセグメントは英国の外食産業店舗総数の0.57%を占めていたが、予測期間中にインターネット普及率の増加により増加すると予想されます。

英国では鶏肉と肉料理の人気がQSRとFSRチェーンのメニュー拡大を促進

- 英国では、クラウドキッチンのAOVが最も高く、2022年の価格は11.68%。クラウドキッチン市場の拡大は、オンライン食事デリバリー需要の増加が牽引しています。英国人は2022年、持ち帰り食品の宅配に平均636米ドルを費やしました。パンデミックの後、オンライン食事注文と配達サービスの人気が高まりました。2022年に英国でクラウドキッチンが提供した人気料理はピザとチキン・シシ・ケバブで、価格は300グラム当たり平均10.25米ドルでした。2022年、最も人気のある料理のコストは平均注文額の50%に固定されました。

- 英国の食品産業は、顧客の要求と消費者行動に合わせて進化・変化してきました。英国では過去10年間にテイクアウトやファーストフード店の数が増加しました。2022年には、英国は4万6,200以上の持ち帰り・ファーストフード店を占めています。ハンバーガーは、その風味と原材料の良さから、消費者の間で最も人気のあるファストフードとなっています。ハンバーガーやチキン・ラップのオプションや、鹿肉、牛肉、その他数種類のタンパク質を使用した製品が豊富にあることが、ハンバーガーやチキン・ラップの需要拡大の要因となっています。英国では、2022年のハンバーガーとチキンラップの平均価格は、1食あたりそれぞれ4.5米ドルと5.4米ドルでした。

- 近年のチキン人気により、英国のアメリカ系レストラン・チェーンはメニュー・セレクションを拡大しています。英国では、1人当たりの平均肉食量は世界平均のほぼ2倍の1日220グラムです。そのため、多くのQSRレストランやFSRレストランが、チキンビリヤニ、チキンナゲット、チキンラップなどのチキン料理をメニューに取り入れました。チキンビリヤニは同国では500グラム当たり12.5米ドルで販売されています。

英国外食産業の概要

英国の外食産業市場は断片化されており、上位5社で2.88%を占めています。この市場の主要企業は以下の通り。 Greggs PLC, McDonald's Corporation, Nando's Group Holdings Limited, PizzaExpress(Restaurants)Limited and The Restaurant Group PLC(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- アウトレット数

- 平均注文額

- 規制の枠組み

- 英国

- メニュー分析

第5章 市場セグメンテーション

- 外食産業タイプ

- カフェ&バー

- 料理別

- バー&パブ

- カフェ

- ジュース/スムージー/デザートバー

- コーヒー&ティー専門店

- クラウドキッチン

- フルサービスレストラン

- 料理別

- アジア料理

- ヨーロピアン

- ラテンアメリカ料理

- 中東料理

- 北米料理

- その他のFSR料理

- クイックサービスレストラン

- 料理別

- ベーカリー

- ハンバーガー

- アイスクリーム

- 肉料理

- ピザ

- その他QSR料理

- カフェ&バー

- アウトレット

- チェーン店

- 独立店舗

- ロケーション

- レジャー

- 宿泊施設

- 小売

- 独立型

- 旅行

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Admiral Taverns Ltd.

- Co-operative Group Limited

- Costa Coffee

- Doctor's Associates, Inc.

- Domino's Pizza Group PLC

- Greggs PLC

- Marston's PLC

- McDonald's Corporation

- Mitchells & Butlers PLC

- Nando's Group Holdings Limited

- Pizza Hut(U.K.)Limited

- PizzaExpress(Restaurants)Limited

- Starbucks Corporation

- Stonegate Group

- Tesco PLC

- The Restaurant Group PLC

- Whitbread PLC

- Yum!Brands, Inc.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The United Kingdom Foodservice Market size is estimated at 104.8 billion USD in 2025, and is expected to reach 144.5 billion USD by 2030, growing at a CAGR of 6.64% during the forecast period (2025-2030).

Rising coffee and tea consumption in the country especially in specialty tea/coffee is driving the market growth

- The quick service restaurants segment is expected to register a CAGR of 5.25% by value during the forecast period, owing to the standardization across food outlet chains in terms of ambiance, hygiene, service time, and ease of access. This is expected to raise consumer interest, thereby increasing overall footfall.

- However, cloud kitchens are anticipated to register the fastest growth at a CAGR of 32.39% during the forecast period, with booming online delivery preference by consumers, especially after the COVID-19 pandemic. The country experienced a growth in online delivery by 110% in 2021. Moreover, the affordability that cloud kitchens offer to manufacturers with less investment is boosting the growth of cloud kitchens in the United Kingdom.

- The market for full-service restaurants registered a CAGR of 6.83% by value during the study period. European cuisine held the largest share of the market in 2022, with around 47% value stake. The growth of the segment can be attributed to the introduction of vegan, low-sugar, and gluten-free options to traditional European dishes by restaurants. FSR outlets have tried to make these dishes healthier and more appealing to the consumer due to a growing demand for nutritional diets in the United Kingdom.

- The growth of cafes & bars is supported by the rising consumption of tea and coffee in the country, especially in the specialty tea/coffee category. Around 70% of consumers in the United Kingdom drink at least two cups of coffee or more per day. Moreover, 23% of coffee drinkers regularly downed more than three cups of coffee per day, and 21% drank more than four cups per day in 2021. Hence, the cafes & bars segment in the United Kingdom is projected to register a CAGR of 5.01% by value during the forecast period.

United Kingdom Foodservice Market Trends

The UK QSR market grows moderately, with American chains gaining popularity

- The number of quick service restaurants in the United Kingdom registered a CAGR of 2.24% during the study period. The moderate growth rate can primarily be attributed to the operational restrictions posed by the pandemic. Among the world-renowned brands of the United Kingdom, Greggs PLC had the highest rating among the British public, with 67% positive opinion. Pizza Express, KFC, Pizza Hut, and Costa Coffee were also rated among the top five brands as of 2022. British citizens have exhibited a good appetite for fast food offered by American fast food chains like burgers, tacos, and pizzas, giving a good opening for American giants to expand. For instance, Wendy's, the third largest burger chain in the world, announced its plan to open 50 new restaurants during 2022-2023.

- Cafes and bars had the most outlets of all the foodservice types in 2022. In 2020, an average of 130 milliliters of hot beverages (coffee, tea, and hot chocolate) was consumed per person per week outside their home, giving ample opportunity for these outlets to grow. Currently, number of coffee shops in the country stands lower than the number of bars and pubs but projections are made to reverse the tally. Three new coffee shops are opening their doors in the United Kingdom every day, while the number of pubs is declining, supporting the projection claims. It was observed that the number of pubs and bars in London fell from 4,835 in 2001 to 3,615 in 2016, while coffee shops have more than doubled.

- Cloud kitchens are anticipated to register a CAGR of 14.79% during the forecast period. In 2022 and the segment represented 0.57% of the total number of foodservice outlets in the United Kingdom but they are expected to increase owing to increasing internet penetration during the forecast period.

Chicken and meat dishes' popularity in the United Kingdom drives menu expansion at QSR and FSR chains

- In the United Kingdom, the AOV was highest for the cloud kitchen, priced at 11.68% in 2022. The expansion of the cloud kitchen market is being driven by an increase in demand for online meal delivery. Britons spent an average of USD 636 on takeaway food delivery in 2022. Online meal ordering and delivery services grew in popularity after the pandemic. In 2022, popular dishes offered by cloud kitchens in the United Kingdom were pizza and chicken shish kebabs, priced at an average of USD 10.25 per 300 grams. In 2022, the cost of the most popular dishes was fixed at 50% of the average order value.

- The United Kingdom's food industry has evolved and changed to meet customer demands and consumer behavior. The number of takeaway and fast-food restaurants in the United Kingdom increased over the past decade. In 2022, the United Kingdom accounted for over 46.2 thousand takeaway and fast food restaurants. Due to the flavors and ingredients used in the products, burgers have been the most popular fast food among consumers. The vast availability of burgers and chicken wrap options or products with protein options, such as venison, beef, and several others, can be attributed to the growing demand for burgers and chicken wraps. In the United Kingdom, the average price of burgers and chicken wraps was USD 4.5 and USD 5.4, respectively, per serving in 2022.

- The popularity of chicken in recent years has led American restaurant chains in the United Kingdom to expand their menu selections. In the United Kingdom, the average amount of meat eaten per person is almost double the world average at 220 grams per day. Thus, owing to rising demand, many QSR and FSR restaurants included chicken dishes on menus, such as chicken biryani, chicken nuggets, and chicken wraps. The chicken biryani is priced at USD 12.5 per 500 grams in the country.

United Kingdom Foodservice Industry Overview

The United Kingdom Foodservice Market is fragmented, with the top five companies occupying 2.88%. The major players in this market are Greggs PLC, McDonald's Corporation, Nando's Group Holdings Limited, PizzaExpress (Restaurants) Limited and The Restaurant Group PLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Number Of Outlets

- 4.2 Average Order Value

- 4.3 Regulatory Framework

- 4.3.1 United Kingdom

- 4.4 Menu Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Foodservice Type

- 5.1.1 Cafes & Bars

- 5.1.1.1 By Cuisine

- 5.1.1.1.1 Bars & Pubs

- 5.1.1.1.2 Cafes

- 5.1.1.1.3 Juice/Smoothie/Desserts Bars

- 5.1.1.1.4 Specialist Coffee & Tea Shops

- 5.1.2 Cloud Kitchen

- 5.1.3 Full Service Restaurants

- 5.1.3.1 By Cuisine

- 5.1.3.1.1 Asian

- 5.1.3.1.2 European

- 5.1.3.1.3 Latin American

- 5.1.3.1.4 Middle Eastern

- 5.1.3.1.5 North American

- 5.1.3.1.6 Other FSR Cuisines

- 5.1.4 Quick Service Restaurants

- 5.1.4.1 By Cuisine

- 5.1.4.1.1 Bakeries

- 5.1.4.1.2 Burger

- 5.1.4.1.3 Ice Cream

- 5.1.4.1.4 Meat-based Cuisines

- 5.1.4.1.5 Pizza

- 5.1.4.1.6 Other QSR Cuisines

- 5.1.1 Cafes & Bars

- 5.2 Outlet

- 5.2.1 Chained Outlets

- 5.2.2 Independent Outlets

- 5.3 Location

- 5.3.1 Leisure

- 5.3.2 Lodging

- 5.3.3 Retail

- 5.3.4 Standalone

- 5.3.5 Travel

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Admiral Taverns Ltd.

- 6.4.2 Co-operative Group Limited

- 6.4.3 Costa Coffee

- 6.4.4 Doctor's Associates, Inc.

- 6.4.5 Domino's Pizza Group PLC

- 6.4.6 Greggs PLC

- 6.4.7 Marston's PLC

- 6.4.8 McDonald's Corporation

- 6.4.9 Mitchells & Butlers PLC

- 6.4.10 Nando's Group Holdings Limited

- 6.4.11 Pizza Hut (U.K.) Limited

- 6.4.12 PizzaExpress (Restaurants) Limited

- 6.4.13 Starbucks Corporation

- 6.4.14 Stonegate Group

- 6.4.15 Tesco PLC

- 6.4.16 The Restaurant Group PLC

- 6.4.17 Whitbread PLC

- 6.4.18 Yum! Brands, Inc.

7 KEY STRATEGIC QUESTIONS FOR FOODSERVICE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms