|

市場調査レポート

商品コード

1913354

車載決済サービス市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測In-Vehicle Payment Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 車載決済サービス市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月05日

発行: Global Market Insights Inc.

ページ情報: 英文 240 Pages

納期: 2~3営業日

|

概要

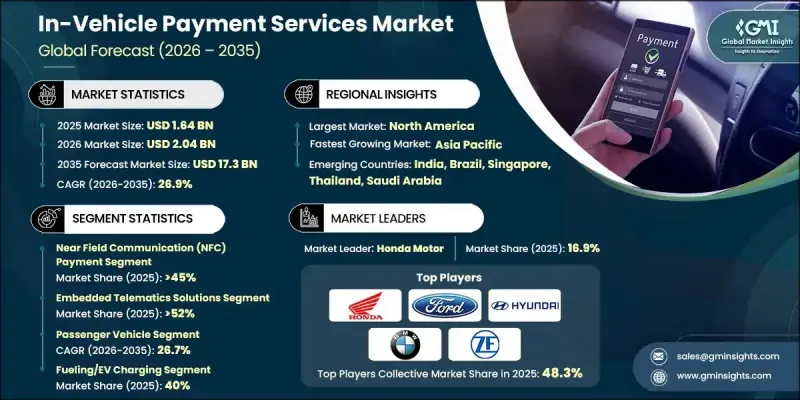

世界の車載決済サービス市場は、2025年に16億4,000万米ドルと評価され、2035年までにCAGR26.9%で成長し、173億米ドルに達すると予測されています。

市場の勢いは、モビリティ関連活動におけるシームレスで非接触型のデジタル取引への嗜好の高まりによって牽引されており、自動車メーカーやモビリティサービスプロバイダーが安全な決済機能を車両に直接組み込むことを促進しています。高度なインフォテインメントおよびテレマティクスアーキテクチャを備えたコネクテッドカープラットフォームの急速な拡大は、統合決済機能とリアルタイム取引処理のための強固な基盤を構築しています。消費者のデジタルウォレットやキャッシュレス決済ソリューションへの依存度が高まることで、車両システムと広範な金融エコシステム間の互換性がさらに加速しています。自動車メーカーは、開発サイクルの効率化、規制要件への対応、コネクテッドサービスからの新たな収益機会の創出を目的として、金融機関、決済処理業者、テクノロジー企業との提携を積極的に進めております。並行して、IoT、AI、高速接続などの先進技術の統合により、車両、決済インフラ、サービスプラットフォーム間の通信が強化され、車載コマースソリューションのスケーラビリティと信頼性が向上しております。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 16億4,000万米ドル |

| 予測金額 | 173億米ドル |

| CAGR | 26.9% |

2025年、近距離無線通信(NFC)決済セグメントは45%のシェアを占め、2035年までに87億米ドルに達すると予測されています。非接触型決済方法の広範な普及と、車両ハードウェアエコシステム内での統合の進展が採用を後押ししています。

組み込みテレマティクスソリューションセグメントは2025年に52%のシェアを占め、8億5,290万米ドルの収益を生み出しました。これらのソリューションは、安全なネイティブ決済機能を実現すると同時に、データ所有権の強化、システムの信頼性向上、長期的なサービス収益化を可能にする点で高く評価されています。

米国の車載決済サービス市場は2025年に6億5,310万米ドルに達し、2035年まで堅調な成長が見込まれています。市場拡大は、コネクテッドカーの高い普及率と、利便性を重視したデジタル決済体験への強い需要によって支えられています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 非接触決済の需要増加

- コネクテッドカー普及率の成長

- デジタルウォレット・エコシステムの拡大

- OEMとフィンテックのパートナーシップ

- 電気自動車の普及拡大と充電インフラの拡充

- 業界の潜在的リスク&課題

- サイバーセキュリティとデータプライバシーに関する懸念事項

- 高いシステム統合コストとコンプライアンスコスト

- 市場機会

- EV充電決済統合の拡大

- フリートおよび商用車両における決済自動化の成長

- パーソナライズされた車載コマースサービスの開発

- 生体認証および音声対応決済認証の導入

- 成長可能性分析

- 規制情勢

- 北米

- 米国:安全な車載決済処理のためのPCI DSS(ペイメントカード業界データセキュリティ基準)

- カナダ:PIPEDA(個人情報保護及び電子文書法)による決済及びユーザーデータ保護の規制

- 欧州

- 英国:車載デジタル決済における英国GDPRおよびPCI DSS準拠

- ドイツ:組み込み決済システム向けGDPRおよびISO/IEC 27001情報セキュリティ管理

- フランス:安全な電子決済および車載決済のためのPSD2(改正決済サービス指令)

- イタリア:デジタルおよび組み込み決済プラットフォーム向けPSD2およびGDPRコンプライアンスフレームワーク

- スペイン:車載決済データセキュリティにおけるGDPRおよびPCI DSS要件

- アジア太平洋地域

- 中国:PIPL(個人情報保護法)によるコネクテッドカー及び車載決済データの規制

- 日本:自動車決済データセキュリティにおける個人情報保護法(APPI)

- インド:車載決済サービスに適用されるRBIデジタル決済セキュリティガイドライン

- ラテンアメリカ

- ブラジル:車載およびコネクテッド決済システムにおけるLGPD(一般データ保護法)

- メキシコ:自動車デジタル決済を規定する個人情報保護法(LFPDPPP)

- アルゼンチン:車載決済プラットフォームに関連する個人情報保護法(法律第25,326号)

- 中東・アフリカ

- アラブ首長国連邦:UAEデータ保護規制および組み込み決済サービス向けPCI DSS

- 南アフリカ:コネクテッドカー決済データに関するPOPIA(個人情報保護法)

- サウジアラビア:車載決済システム向けサウジデータ・AI庁(SDAIA)データ保護規制

- 北米

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- コスト内訳分析

- 開発コスト構造

- 研究開発コスト分析

- マーケティング及び販売コスト

- 特許分析

- 持続可能性と環境面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率化

- 環境に配慮した取り組み

- 将来の市場展望と機会

- OEMの収益化とビジネスモデル分析

- 直接取引収益モデル(収益分配、MDRベース)

- サブスクリプション型車載コマースモデル

- プラットフォームおよびエコシステム収益化(アプリストア、マーケットプレース)

- データ駆動型収益化の機会(利用状況、行動分析)

- OEM対フィンテック対決済ネットワークの収益所有権

- OEM統合・導入フレームワーク

- エコシステムの力学と戦略的コントロールポイント

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:お支払い方法別、2022-2035

- 近距離無線通信(NFC)決済

- QRコードベースの決済

- 組み込み型ウォレット

- その他

第6章 市場推計・予測:技術別、2022-2035

- 組み込みテレマティクスソリューション

- モバイルアプリケーションベースの統合

- クラウドベースの決済プラットフォーム

第7章 市場推計・予測:車両別、2022-2035

- 乗用車

- SUV

- セダン

- ハッチバック

- 商用車

- 軽商用車(LCV)

- MCV

- 大型商用車(HCV)

第8章 市場推計・予測:用途別、2022-2035

- 燃料補給/電気自動車充電

- スマートパーキング

- 自動料金収受システム

- 電子商取引

- その他

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- ポルトガル

- クロアチア

- ベネルクス

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- シンガポール

- タイ

- インドネシア

- ベトナム

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

第10章 企業プロファイル

- 世界プレイヤー

- Amazon Web Services

- Ford Motor Company

- Hyundai Motor Company

- IBM

- Mastercard

- PayPal

- Shell

- Visa

- Volkswagen

- BMW

- Jaguar Land Rover Automotive

- ParkMobile

- ZF

- 地域プレイヤー

- General Motors Company

- Honda Motor

- Daimler/Mercedes-Benz

- Toyota Motor

- Telenav

- Parkopedia

- CarPay Diem/Kwalyo

- SiriusXM Connected Vehicle

- Gentex

- Thales

- Emerging/Disruptor Players

- Car IQ Pay

- Cerence

- PayByCar

- Verra Mobility

- Apple

- Samsung Electronics

- Parkwhiz

- Xevo