|

市場調査レポート

商品コード

1686538

アジア太平洋地域の作物保護化学品:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia Pacific Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域の作物保護化学品:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 262 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

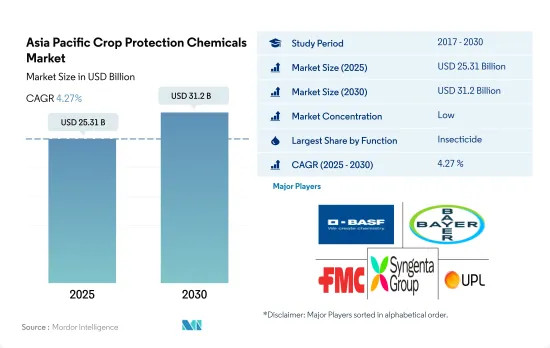

アジア太平洋地域の作物保護化学品市場規模は2025年に253億1,000万米ドルと推定され、2030年には312億米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは4.27%で成長すると予測されます。

害虫と雑草の攻撃増加によるアジア太平洋地域市場での殺虫剤と除草剤の優位性

- アジア太平洋地域の農業は多様性に富み、多くの国の経済において重要な役割を果たしています。この地域は熱帯から温帯まで幅広い気候を持ち、米、大豆、小麦、様々な果物や野菜の栽培で知られています。2022年、アジア太平洋地域は世界の作物保護化学品市場で金額ベースで24.7%のシェアを占めました。

- より良い収量を達成するための作物保護化学品の使用は、同地域の人口増加による食用作物需要の増加によって奨励されています。同時に、技術の進歩は農業のやり方を変え、害虫駆除の新技術は作物と農家に大きな利益をもたらしています。

- 殺虫剤はアジア太平洋地域の作物保護化学品市場で50.8%と最も高いシェアを占めています。稲は多くの地域で栽培されている主要作物です。しかし、さまざまな害虫の被害を受けやすく、その結果、作物、ひいてはその収量に深刻なダメージをもたらしています。

- 除草剤は2022年に金額ベースで28.5%と第2位のシェアを占めました。主食作物、商業作物、園芸作物における雑草の害は、この地域の農業生産性に大きな課題をもたらしています。この地域の経済成長には果実産業が大きく貢献しているため、果実雑草は大きな経済的損害をもたらします。Amaranthus retroflexus(Redroot pigweed)とEchinochloa crus-galli(Barnyard grass)は、地域の果樹産業で最も一般的な雑草です。

- 食料安全保障への関心の高まりと様々な市場開拓により、農家は作物への害虫の影響を最小限に抑えながら、効率的で持続可能な食料生産を行うようになっています。これが市場を牽引しており、予測期間中(2023~2029年)のCAGRは4.5%を記録すると予測されています。

害虫、病気、雑草から農作物を守るための作物保護化学品消費の増加により市場は成長している

- 2022年、アジア太平洋地域は世界の殺虫剤市場で金額ベースで24.7%の市場シェアを占めました。同地域の殺虫剤分野は非常に重要であり、絶えず進化しています。複数の国々において、生産的で持続可能な農業慣行を促進する上で重要な役割を果たしています。過去一定期間、アジア太平洋地域の殺虫剤市場は一貫した成長を遂げ、CAGRは5.5%でした。

- 中国やインドをはじめとするアジア太平洋地域諸国では、多様な農業景観のために作物保護化学品の使用量が増加しており、病害虫に弱い作物もあります。集約的な作物栽培や単一栽培の普及も、病害虫の繁殖に好条件を与えています。多くの人口を維持するため、食糧安全保障の確保が最優先課題となり、作物の収量を守り、病害虫による損失を最小限に抑える必要性が高まり、その結果、作物保護化学品への依存度が高まっています。

- また、近代的手法の導入や耕作地の拡大による農業の拡大も、市場の成長をもたらしています。同地域の農地面積は2019年の6億2,450万haから2022年には6億6,220万haに拡大します。農業活動の拡大に伴い、作物を害虫から守る効率的なソリューションに対する需要も拡大しています。

- 予測期間中(2023~2029年)、タイは金額ベースでCAGR 6.8%と、この地域で最も速い成長率を示すと予測されています。この急成長は、害虫の脅威の高まりと作物損失の増加により、同国の農家による作物保護化学品使用の増加が予想されることに起因しています。

アジア太平洋地域の作物保護化学品市場動向

害虫の増加により作物保護化学品の使用量が増加

- アジア太平洋地域の2022年の作物保護化学品の平均消費量は、農地1ヘクタール当たり2.9kgでした。殺菌剤は化学作物保護化学品の中で最も使用量が多く、平均消費量は1ヘクタール当たり10.6キログラムに達しました。これは、真菌病原体が農業生産に大きな脅威をもたらし、その結果、殺菌剤の必要性が高まっていることを示しています。水稲のいもち病の原因菌はMBI-D殺菌剤に対する耐性を獲得しており、殺菌剤散布の必要性が高まっています。

- 殺菌剤の次は除草剤で、2022年の1ヘクタール当たりの散布量は10.4kgとなります。ヘクタール当たりの除草剤使用量の増加は、農業人口の高齢化、労働力不足、農地の拡大など、さまざまな要因に起因しています。これらの要因は、手作業による除草から、稲や大豆のような重要作物における効果的な雑草管理のための除草剤の利用への移行を促しています。また、雑草が既存の除草剤に対して耐性を獲得しつつあるため、雑草の管理は非常に難しくなっており、その結果、除草剤の散布量が増えています。

- 殺虫剤はアジア太平洋地域諸国では作物保護化学品の中で3番目に散布量が多く、2022年の1ヘクタール当たりの散布量は8kgになります。地球温暖化と気候変動は、さまざまなメカニズムで害虫を増加させることによっても、農業生産にさまざまな課題を突きつけています。例えば、稲の主要害虫であるヒメトビウンカ(Nilaparvata lugens)は、アジアの一部で気温の上昇に反応して個体数が増加し、分布が拡大することが観察されています。同様に、殺線虫剤や殺軟体動物剤の使用も、農家の間でその利点に対する認識が高まり、必要性が高まる中で増加しています。

シペルメトリンの入手可能性と需要が限られているため、アジア太平洋地域市場では有効成分の価格が上昇しています。

- シペルメトリンは、鱗翅目、鞘翅目、双翅目、半翅目など幅広い害虫に有効な合成ピレスロイド系殺虫剤として、この地域で主に使用されています。インド、中国、ベトナムといった国々では、様々な作物の害虫駆除に主にシペルメトリンが使用されています。特に、中国とベトナムはシペルメトリンの主要輸入国です。2022年現在、有効成分の価格は1トン当たり21,037.7米ドルに上昇し、2017年以降21.1%の顕著な上昇を反映しています。この価格高騰は、サトウキビ、綿花、果物、野菜などの作物におけるシペルメトリン需要の増加に起因しています。

- アトラジンは、この地域で広く利用されている除草剤として重要な位置を占めており、トリアジンクラスの塩素系除草剤として分類されています。アトラジンは、出芽前および出芽後の除草剤として、大豆、トウモロコシ、サトウキビ、芝草などの作物の一年生広葉雑草やイネ科雑草を効果的に防除します。この有効成分の価格は、さまざまな作物への広範な適用により、前年比で一貫した伸びを示しています。2022年の最新記録では、価格は1トン当たり13,817.2米ドルで、2017年から29.8%の大幅な上昇を示しました。

- Mancozebは接触殺菌剤であり、穀物、果実、野菜、豆類などの幅広い菌類病害を効果的にターゲットとする多用途な適用形態で知られています。この有効成分の価格は現在1トン当たり7,776.9米ドルであり、アジア太平洋地域諸国で広く利用されている主要な殺菌剤有効成分の1つです。

- 有効成分の価格は、原料コストの上昇、輸入関税、物流費の高騰により年々上昇しています。

アジア太平洋地域作物保護化学品産業の概要

アジア太平洋地域の作物保護化学品市場は細分化されており、上位5社で33.97%を占めています。この市場の主要企業は以下の通りです。BASF SE, Bayer AG, FMC Corporation, Syngenta Group and UPL Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの作物保護化学品消費量

- 有効成分の価格分析

- 規制の枠組み

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 機能

- 殺菌剤

- 除草剤

- 殺虫剤

- 殺軟体動物剤

- 殺線虫剤

- 使用モード

- 薬剤散布

- 葉面散布

- 燻蒸

- 種子処理

- 土壌処理

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 国

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Rainbow Agro

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 52421

The Asia Pacific Crop Protection Chemicals Market size is estimated at 25.31 billion USD in 2025, and is expected to reach 31.2 billion USD by 2030, growing at a CAGR of 4.27% during the forecast period (2025-2030).

Dominance of insecticides and herbicides in the Asia-Pacific market due to a rise in pest and weed attacks

- Agriculture in Asia-Pacific is diverse and plays a significant role in the economies of many countries. The region has a wide range of climates, from tropical to temperate, and is known for the cultivation of rice, soybeans, wheat, and various fruits and vegetables. In 2022, Asia-Pacific occupied a share of 24.7% by value of the global crop protection chemicals market.

- The use of pesticides in order to achieve better yields is encouraged by the increasing demand for food crops due to population growth in the region. At the same time, technological advancements have changed the way farming is done, and new technologies in pest control are benefiting crops and farmers a great deal.

- Insecticides occupied the highest share of 50.8% in the Asia-Pacific crop protection chemicals market. Rice is the major crop cultivated across many regional countries. However, it is also susceptible to various pests, which have led to severe damage to the crop and, subsequently, its yield.

- Herbicides occupied the second-largest share of 28.5% by value in 2022. Weed attacks in staple, commercial, and horticultural crops pose a significant challenge to the region's agricultural productivity. As there is a significant contribution by the fruit industry to the region's economic growth, fruit weeds cause substantial economic damage. Amaranthus retroflexus (Redroot pigweed) and Echinochloa crus-galli (Barnyard grass) are the most common weeds in the regional fruit industry.

- Increased concerns for food security and various market developments have facilitated the efficient and sustainable production of food by farmers while minimizing the impact of pests on their crops. This has driven the market, which is anticipated to register a CAGR of 4.5% during the forecast period (2023-2029).

The market is growing due to the rising consumption of pesticides to protect crops from pests, diseases, and weeds

- In 2022, Asia-Pacific held a market share of 24.7% by value of the global insecticide market. The pesticide segment in the region is of great importance and is constantly evolving. It plays a vital role in promoting productive and sustainable agricultural practices in multiple countries. During the historical period, the pesticide market in Asia-Pacific experienced consistent growth, with a CAGR of 5.5%.

- Asia-Pacific countries like China and India, along with other countries, experience increased pesticide usage due to their varied agricultural landscape, making some crops more vulnerable to pests and diseases. The prevalence of intensive cropping practices and monocultures also contributes to the favorable conditions for pests to thrive. With substantial populations to sustain, ensuring food security becomes a top priority, leading to a heightened need to protect crop yields and minimize losses caused by pests, thus resulting in a greater reliance on pesticides.

- The market is also experiencing growth due to the expansion of agriculture, with the adoption of modern practices and the expansion of cultivated land. The region's agricultural land area grew from 624.5 million ha in 2019 to 662.2 million ha in 2022. As agricultural activities expand, the demand for efficient solutions to protect crops from pests is also growing.

- During the forecast period (2023-2029), Thailand is projected to exhibit the fastest growth rate in the region, with a CAGR of 6.8% by value. This rapid growth can be attributed to the anticipated increase in the usage of pesticides by farmers in the country due to the rising threat of pests and increasing crop losses.

Asia Pacific Crop Protection Chemicals Market Trends

Increasing pest proliferation is leading to higher application of pesticides

- The average consumption of crop protection chemicals in Asia-Pacific was 2.9 kg per hectare of agricultural land in 2022. Fungicides were the highest used among all chemical pesticides, with average consumption amounting to 10.6 kg per hectare. This indicates the significant threat posed on agricultural production by fungal pathogens, resulting in a higher need for fungicides. Fungus-causing rice blast in paddy has developed resistance to MBI-D fungicides, leading to a higher need for fungicidal applications.

- Fungicides are followed by herbicides, with a per hectare application rate of 10.4 kg per hectare in 2022. The increase in herbicide usage per hectare can be attributed to various factors, including an aging farming population, labor shortages, and the expansion of agricultural land. These factors have prompted a transition from manual weeding practices to the utilization of herbicides for effective weed management in significant crops like rice and soybeans. Weeds are also becoming very tough to manage as they are developing resistance to existing herbicides, leading to higher dosages of application.

- Insecticides are the third most applied among pesticides in Asia-Pacific countries, with a per hectare application rate of 8 kg in the year 2022. Global warming and climate change are posing various challenges to agricultural production, even by increasing the pest population through various mechanisms. For instance, the brown planthopper (Nilaparvata lugens), a major pest of rice, has been observed to increase in population and expand its distribution in response to rising temperatures in parts of Asia. Similarly, the usage of nematicides and molluscicides has been increasing amid growing awareness among farmers of their benefits, along with the increasing need.

Limited availability and demand for cypermethrin have increased the price of active ingredients in the Asia-Pacific market

- Cypermethrin is the dominant insecticide used in the region, being a synthetic pyrethroid effective against a wide range of insect pests such as Lepidoptera, Coleoptera, Diptera, and Hemiptera. Countries like India, China, and Vietnam primarily rely on cypermethrin for pest control in various crops. Notably, China and Vietnam are the major importers of cypermethrin. As of 2022, the price of the active ingredient had risen to USD 21,037.7 per metric ton, reflecting a notable increase of 21.1% since 2017. This surge in price can be attributed to the growing demand for cypermethrin in crops like sugarcane, cotton, fruits, and vegetables.

- Atrazine holds a prominent position as a widely utilized herbicide in the region, classified as a chlorinated herbicide of the triazine class. It serves as both a pre- and post-emergence herbicide, effectively controlling annual broadleaf weeds and grasses in crops like soybeans, maize, sugarcane, and turf grasses. The active ingredient's price has experienced consistent year-on-year growth due to its extensive application across various crops. As of the latest recording in 2022, the price stood at USD 13,817.2 per metric ton, marking a significant increase of 29.8% since 2017.

- Mancozeb is a contact fungicide known for its versatile application modes, effectively targeting a wide array of fungal diseases in cereal crops, fruits, vegetables, and pulses. The price of the active ingredient currently stands at USD 7,776.9 per metric ton, making it one of the principal fungicide active ingredients extensively utilized in the Asia-Pacific countries.

- The prices of active ingredients are experiencing annual increases due to the rise in raw material costs, import tariffs, and escalating logistics expenses.

Asia Pacific Crop Protection Chemicals Industry Overview

The Asia Pacific Crop Protection Chemicals Market is fragmented, with the top five companies occupying 33.97%. The major players in this market are BASF SE, Bayer AG, FMC Corporation, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Myanmar

- 4.3.7 Pakistan

- 4.3.8 Philippines

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

- 5.3 Crop Type

- 5.3.1 Commercial Crops

- 5.3.2 Fruits & Vegetables

- 5.3.3 Grains & Cereals

- 5.3.4 Pulses & Oilseeds

- 5.3.5 Turf & Ornamental

- 5.4 Country

- 5.4.1 Australia

- 5.4.2 China

- 5.4.3 India

- 5.4.4 Indonesia

- 5.4.5 Japan

- 5.4.6 Myanmar

- 5.4.7 Pakistan

- 5.4.8 Philippines

- 5.4.9 Thailand

- 5.4.10 Vietnam

- 5.4.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.7 Rainbow Agro

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms